oil

Not all oil-exporting countries are the cracking winners you think.

By Charles de Quinsonas

4 June 2026

As investors we get used to living within certain recognised bounds. For example, it has been commonly assumed that interest rates cannot be sub-zero. There has been the odd historical quirk when we’ve seen negative rates (Switzerland in the 1970s), but that’s more for amusement than general investment consumption. However, there now appears to be the potential for a major investment climate change.

There are already plenty of bond markets now living in the sub zero ice age, such as Switzerland, Denmark, Germany, Finland and the Netherlands. In these cases, the existence of negative rates could be down to the desire to express a currency or re-denomination view (as Mike previously wrote), so may be seen as a by-product of external factors and not of domestic monetary policy. However, there is now the potential for G7 monetary policy to enter the previously unbelievable reality of official sub-zero rates.

Many G7 economies have implemented very low rates and quantitative easing for a number of years, yet still appear to be in the economic doldrums with high unemployment, low growth and limited fiscal room. It could now be time for a significant change in the investment text book as central banks experiment with rates below zero.

Theoretically, a negative interest rate sounds simple – you put £100 in the bank and you get £99 back a year later if the rate is -1%. A rational investor would of course have the alternative of simply keeping their cash under the mattress and not suffering the negative rate, although the incentive to behave rationally would be limited by the administrative burden and security risk of holding cash. The central bank could simply limit this activity by basically not printing enough cash. Therefore the vast majority of money would have to be held electronically and could therefore suffer a penal negative rate. Implementation of sub zero rates is possible.

From a central bank’s point of view this should be stimulative, as it would discourage saving and encourage consumption like any traditional interest rate cut. At the extreme you could create exceptionally low, zero, or even negative borrowing rates.

The challenges faced by central banks and governments are still there despite traditional and unconventional policy action. Maybe it will soon be time to use the conventional tool of cutting interest rates in an unconventional way by making them negative. The next step to be taken by the authorities might mean economies working in a below zero interest rate climate (bzirc monetary policy).

EM debt is a bit like Converse shoes; it seems almost everyone I speak to owns some.

Readers will no doubt be familiar with the EM ‘grand narrative’ (eg EM will surely outperform because of low debt levels, high growth, strong demographics etc etc). We’ve written an in-depth note, which is part of our Panoramic series for professional investors, in an attempt to bash away this EM ‘grand narrative’.

It explores what really have been the primary performance drivers of the three main investable subsets of EM debt (EM local currency sovereign, EM external sovereign, EM external corporates). It touches on themes I’ve previously written about on the risks to EM debt posed by Eurozone instability and the associated risks posed by a reversal of the huge decade-long portfolio flows that have supported the asset class. But the main focus of the note is on the sizeable additional long term risk posed to EM debt by the inevitable economic rebalancing of the world’s second largest economy – China.

EM debt is still ‘cool’ within the investment universe. However, it’s curious that people now say EM debt is a good investment ‘in the long term’, a subtle change brought about by the miserable performance of some EM countries over the past year. This miserable performance has been most notable within the BRIC economies* , where in recent months, the Brazilian Real and Russian Ruble hit three year lows against the US Dollar, the Indian Rupee hit a record low against the US dollar, and this year the Chinese Yuan has had the biggest drop against the US dollar since its big devaluation in 1994.

I’m not saying that EM debt will never offer good value; it’s important to stress that there is no such thing as a good or bad asset class, only a good or bad valuation. I’m simply saying that it’s important to understand the performance characteristics of EM debt, the risks facing EM debt appear to be rising, and while some exchange rates have begun to move, the asset class does not appear to be pricing in these risks. Fashions rarely last – EM debt has been very trendy before, but favourable demographics and previously strong growth rates didn’t save emerging markets in 1981-3, 1997-98 and 2001-02. And Converse shoes haven’t always been ‘cool’ either – Converse had to file for bankruptcy protection in 2001 and ended up being bought out by Nike.

* Societe Generale’s Albert Edwards has amusingly and rightly described BRIC as a ‘Bloody Ridiculous Investment Concept’

High yield and equities have historically been seen as highly correlated in terms of their returns, and before 2008, this was true. However, what we have witnessed in the post-Lehman environment is a structural shift that requires a more nuanced appreciation of the relationship between fixed income and equities. This is something we looked at in a more in depth piece we published earlier this year.

This point has been reinforced by the surprisingly divergent performance of the European high yield market and the European equity markets so far this year.

The chart below shows that European high yield performance has been strong, returning a little over 12% year to date. This contrasts sharply with lacklustre equity returns. The MSCI Europe ex UK index is down 1.3% at the time of writing whereas the more concentrated DJ Euro Stoxx 50 is showing a negative 8.4% return.

Accordingly, whilst high yield returns will always be sensitive to the economic cycle and market sentiment, in a world of zero interest rates, financial repression, deleveraging and slow growth, we continue to believe that the relationship between equities and high yield bonds has shifted in a subtle but meaningful way.

First the the answer. Denmark cut official interest rates on its certificates of deposit to MINUS 0.2%. We now have negative nominal interest rates on short dated government bills or bonds in several countries – including Switzerland, Finland, France, Denmark, and Germany.

We had 167 correct answers, and out of the hat came the following 10 winners who each get of a copy of “Debt: The First 5,000 Years” by David Graeber. And yes, we are aware that David Graeber isn’t the greatest fan of capitalism and markets – but even bond fund managers sometimes need to take a break from reading “Atlas Shrugged” and Milton Friedman.

Richard Cavey (The Chester Partnership Ltd), Mark Wharrier (Newsmith), Robert Harper (Brewin Dolphin), Paul Wilson, Stephen Buckle (Kingsfleet Wealth Ltd), David Thornton (Premier Asset Management), Andrew Wilson (Brooks Macdonald), Gary Laing (Deutsche Bank Private Wealth Management), Tom Winstanley, Edward Fane (Thesis Asset Managment plc)

We’ll be in touch with the winners for your contact details and your books will be with you shortly. Congratulations and thanks for all the entries

It seems that the wettest “summer” on record in England is not only playing havoc with the M&G cricket team’s schedule, it is also having a massive impact on the nation’s butterflies. Sir David Attenborough is asking people to participate in the world’s biggest butterfly survey – The Big Butterfly Count – to see how the butterfly population has fared after all the wet weather we have been having. So get out in your garden and see how many butterflies and moths you can count in 15 minutes – counting butterflies has been described as “taking the pulse of nature”.

It should be noted though that England is not the only country that has been experiencing adverse weather conditions. In the US there have been wildfires in Colorado, a heatwave across the eastern seaboard, and a “super derecho” which caused mass destruction from west of Chicago to east of Washington, D.C. Russia has experienced flash flooding in the Krasnodar region and the drought experienced in southern Russia has expanded into western Ukraine and southeastern Europe.

For investment markets, extreme weather events tend to result in a lower supply of soft commodities like maize, wheat, soybeans and corn. Because supply is now expected to fall due to these extreme weather events, the price of soft commodities has sky rocketed over the course of 2012.

Of course, higher food prices means higher inflation numbers. In the UK, food makes up 11.4% of the RPI index and 9.8% of the CPI index. In Europe, food makes up 13.9% in the HICP. In the US, food is 14.2% of the CPI. The recent price increases for soft commodities are currently not expected to result in higher overall inflation.

Of course, higher food prices means higher inflation numbers. In the UK, food makes up 11.4% of the RPI index and 9.8% of the CPI index. In Europe, food makes up 13.9% in the HICP. In the US, food is 14.2% of the CPI. The recent price increases for soft commodities are currently not expected to result in higher overall inflation.

That said, if we do get some pass-through, central bankers would tend to describe the increase in inflation as temporary. Central bankers prefer to look at “core” measures of inflation that exclude potentially volatile categories like food and energy. Mike recently wrote that the state of the global economy is quite poor, so it is more than likely that the central bank authorities will describe any increase in inflation as temporary and that real economies remain weak. We have been describing central bank regime change for a while now, and it appears clear to us that central banks aren’t really all too fussed about inflation anymore. It’s all about unemployment and debt.

However, inflation affects everyone. We can debate whether this is fair or not, as the average consumer doesn’t exclude food and energy from their basket of goods, but rising food prices are arguably an even bigger issue in EM countries. The following chart highlights the weight of food in the inflation basket across the continent of Europe. For EM countries like Romania (29.7%), Turkey (24.3%) and Lithuania (23.6%), the food bill is a substantial amount of money to the average citizen of these nations. In China, the weight of food is close to a third and in India it is almost half. Many of these countries are currently embarking on monetary policy easing and if food inflation continues for a sustained period of time, then this could put these policy easing plans at risk.

As I mentioned last year, the Food and Agriculture Organisation (FAO) of the United Nations is a great source of information on agricultural production and the outlook for food commodity prices. And as I said last year, their agricultural outlook does not make for comforting reading. The chart below shows their nominal price forecasts for crops, livestock and fats out to 2021. There is a continued increase in commodity prices particularly for oilseeds, beef, and fish. The FAO highlight that the key issue facing global agriculture is how to increase productivity in a more sustainable way to meet the rising demand for the “four F’s” – food, feed, fuel and fibre. It is forecast that agricultural production will need to increase by 40% over the next 40 years but total arable land will increase by only 5%. Increasing productivity and developing new technologies will be crucial.

As I mentioned last year, the Food and Agriculture Organisation (FAO) of the United Nations is a great source of information on agricultural production and the outlook for food commodity prices. And as I said last year, their agricultural outlook does not make for comforting reading. The chart below shows their nominal price forecasts for crops, livestock and fats out to 2021. There is a continued increase in commodity prices particularly for oilseeds, beef, and fish. The FAO highlight that the key issue facing global agriculture is how to increase productivity in a more sustainable way to meet the rising demand for the “four F’s” – food, feed, fuel and fibre. It is forecast that agricultural production will need to increase by 40% over the next 40 years but total arable land will increase by only 5%. Increasing productivity and developing new technologies will be crucial.

So keep an eye on those butterflies. They could very well be a leading indicator to food prices and inflation outcomes.

So keep an eye on those butterflies. They could very well be a leading indicator to food prices and inflation outcomes.

Staying with the Bon Jovi theme, ‘Ugly’ was a track released by Jon Bon Jovi on his second solo album in 1998. It isn’t well known, or any good for that matter, but it does aptly describe the price action of Spanish and Italian corporate paper of late.

Plenty of attention has been paid to the yield on Spanish and Italian govies – currently around 7% and 6% for 10-year bonds – but their bellwether non-financial corporate issuers have also seen their yields come under significant pressure. 5-year CDS levels for the likes of Iberdrola, Gas Natural, Repsol and Enel are trading near their all-time wides at 500, 525, 475 and 455 bps respectively. And it isn’t just the utilities that have come under pressure: Telefonica and Telecom Italia have also seen their risk premia balloon to over 500bps. (see chart 1)

Whilst the aforementioned companies are still rated investment grade – some by many notches – they are actually trading wide of the Merrill Lynch BB Euro High Yield Non Financial Index (current asset swap of +440). Put another way, the market does not believe that these businesses represent investment grade risks.

Such a view isn’t without logic. The current ratings for the largest Spanish and Italian non-financial issuers (see chart 2) suggest that the market is right to be nervous. On average, the four largest Spanish issuers are only two notches above high yield status; for Italy’s five largest issuers it’s about three notches. That may seem like a fair bit of runway until you think about the pace of downgrades suffered by their sovereigns of late. Keep in mind that as late as July 2011 Moody’s rated Spain at Aa2, seven notches higher than its current Baa3 rating. Italy has also seen its rating cut a full four notches between June 2011 and Feb 2012 by the agency. And S&P hasn’t been much kinder, slashing Spain’s rating from AA- to BBB+ in under a year and reducing Italy from A+ to BBB+.

Both Spanish and Italian corporates saw negative rating actions as a consequence of those sovereign downgrades. Moody’s allows non-financial corporates a maximum two-notch rating uplift versus the sovereign, whereas S&P permits a maximum of six in extremis, with a couple of notches uplift far more common. The impact on Greek and Portuguese corporate bonds – such as EDP, OTE and Portugal Telecom – after their sovereigns lost their investment grade status serves to reinforce the potentially significant relationship between sovereign and corporate credit ratings.

So, in a hypothetical mass downgrade scenario what quantum of debt could be downgraded to high yield? If all Italian and Spanish non-financial paper were eventually to lose its investment grade status, we calculate that €47bn nominal of Spanish paper and €59bn nominal of Italian paper could fall into high yield territory. That would be a massive €106bn worth of paper – or 80% of the existing non-financial Euro High Yield index – heading into the high yield market. That’s a lot of paper for it to swallow.

Of course, the actual amount of debt that would end up for sale is difficult to quantify. This would depend, among other things, on index rules and investors’ willingness and ability to hold high yield bonds. However, it seems reasonable to assume that over the coming months and even years a significant amount of paper will need to find a new home. Yields may well have to climb further, potentially a lot further, before traditional high yield investors see value in these names.

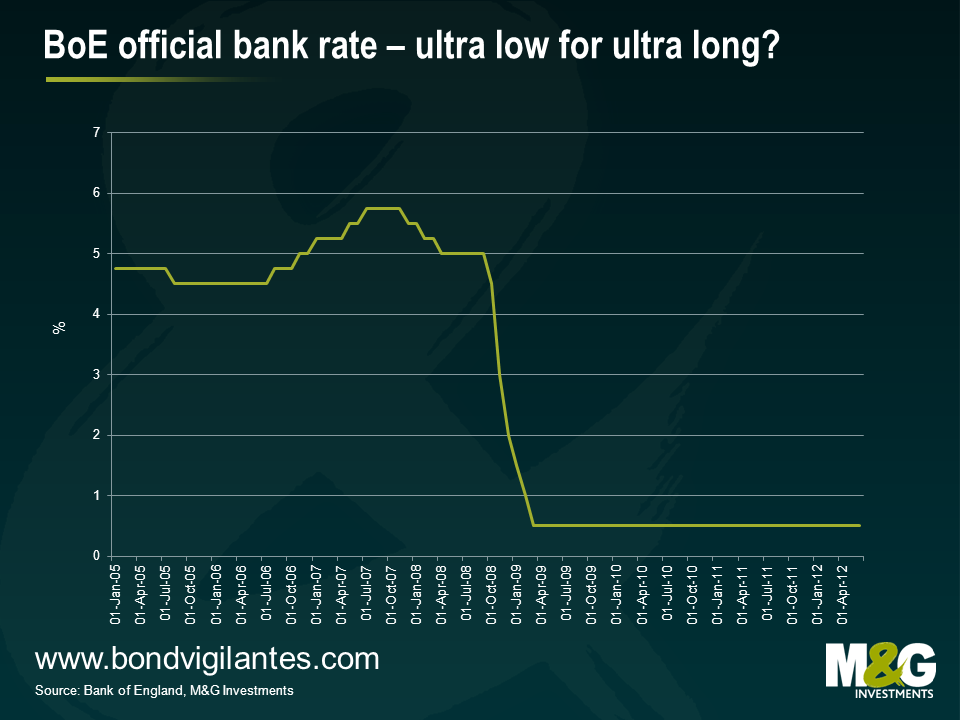

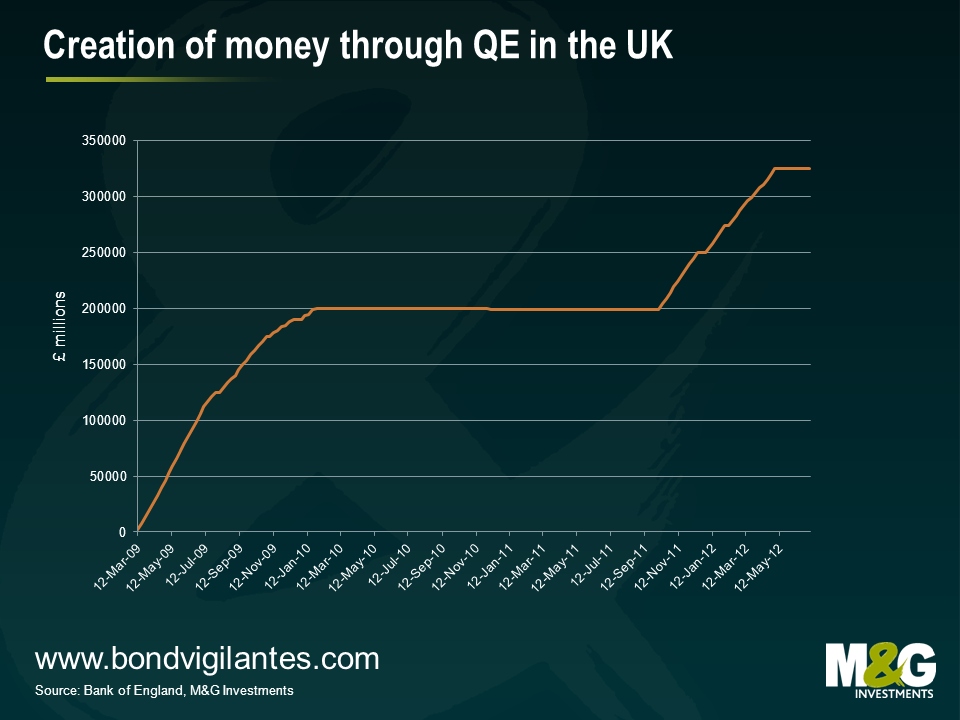

Last week the Bank of England announced a further round of quantitative easing of £50bn, bringing the total to £375bn. It is obvious that the MPC thinks that monetary policy is still not sufficiently loose to create the desired economic effect and hence further stimulus is needed.

We have written numerous times on QE. When we started scribing on this novel experiment we focused on why it needed to be done, and how it was meant to work (like walking on custard) and the bizarre effect this may have on the bond market.

One thing we did not focus on was the length of time monetary policy would have to be kept super accommodative, though we did expect it to be for an extended period of time (certainly until we begin to see a meaningful recovery in employment outcomes as outlined here).

Mervyn King appears surprised by the extent of the crisis. The MPC were slow in aggressively cutting rates after the onset of the credit crunch in 2007, but to his credit Mervyn and the UK authorities have been at the forefront of corrective action and have correctly realised the severity of the credit crisis. The MPC was correct to not interpret the inflation scare of 2008 or the economic rebound of 2009 as economic recovery. They have been spot on.

But how accurate is his current thinking?

The Governor is not one to pre-commit. However he did say something recently that shows how he feels about the potential long term outlook for rates. At the latest Treasury Select Committee he repeated that at this point in time – and he has said it at every committee meeting – that he believes we are not yet half way through the crisis.

“When this crisis began in 2007-2008, most people including ourselves did not believe that we would still be right in the thick of it, in the middle of it, quite this late. All the way through, I’ve said to this committee that I don’t think we are yet half-way through – I’ve always said that and I’m still saying it.” Mervyn King, June 26, 2012.

From the chart below we can see that BoE base rate has been set at 0.5% since March 2009, and over £325bn has been pumped into the financial system through QE. If we are not yet half-way through this crisis, then this implies that rates will stay at these levels for at least another 3 years to 2015, and a further round of £375bn of QE is potentially on the agenda.

If this interpretation of the outlook turns out to be correct then these very low levels of short and long term gilt yields begin to look more logical to gilt investors. And we can assume that the UK won’t recover fully until the US and Europe does as well, which means that ultra low yields on Treasuries and Bunds may also make sense.

Monetary policy is living on the edge, and if Mervyn King were to do a turn at a city karaoke machine, then the bar could well be ringing out to this Bon Jovi classic…

“Whoah we’re half way there, Whoah livin’ on a prayer…”

Naturally, his audience of gilt investors – despite the ultra low yield they are currently receiving – will sing back “We got to hold on to what we’ve got”.

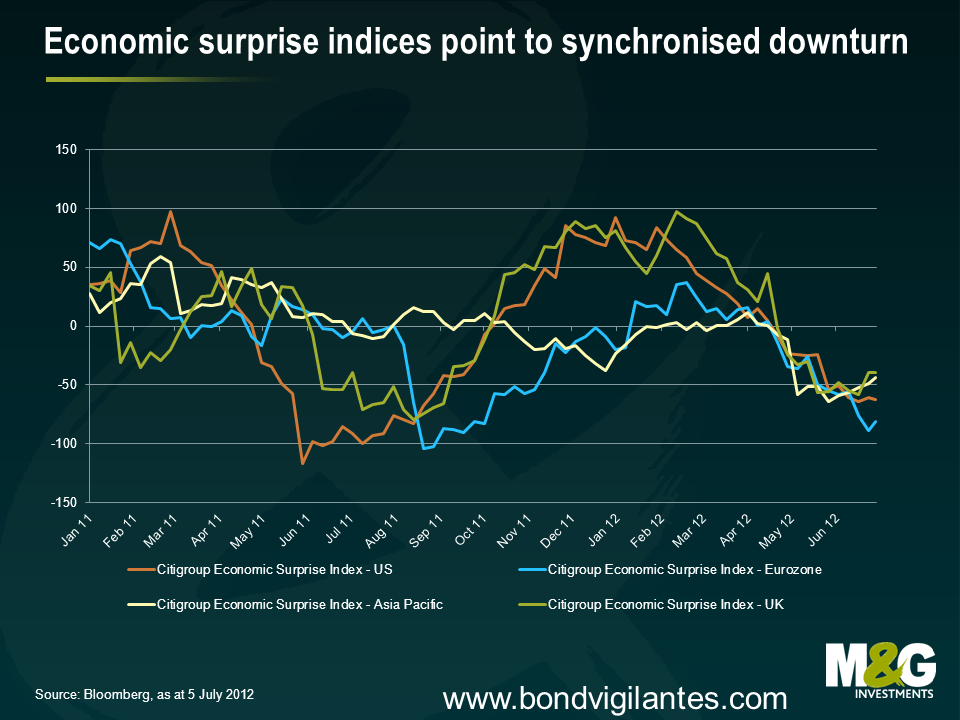

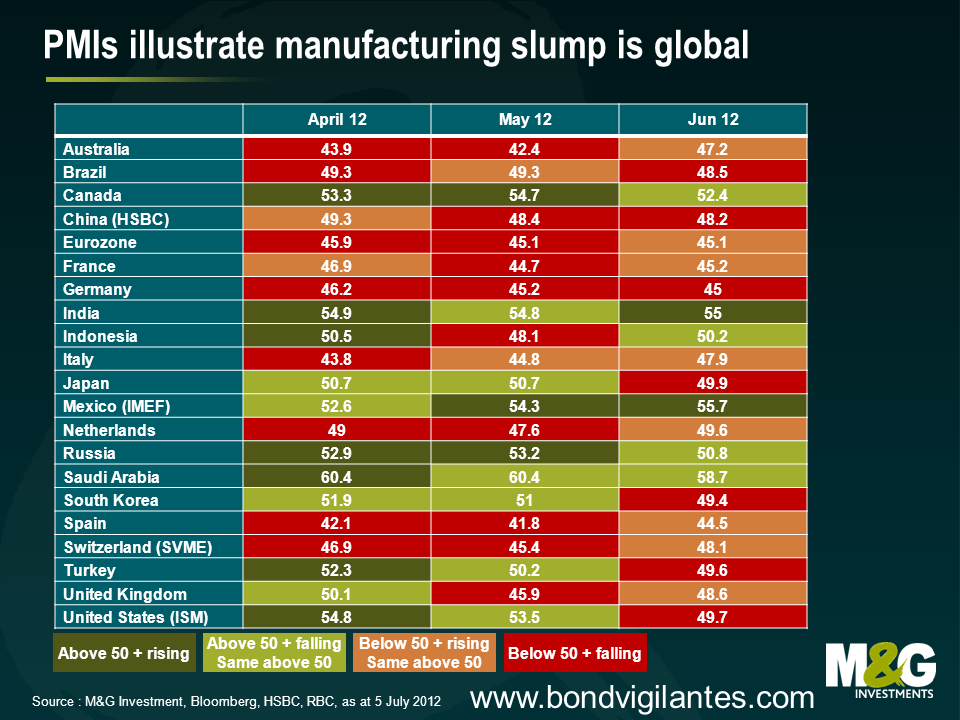

Q2 was a grim quarter, not just for the Eurozone economy but for the global economy. The downturn in Citigroup’s economic surprise indices that began in March picked up speed through to June, while PMIs in almost all corners of the world weakened in Q2 as can be seen by the PMI heatmap.

The good news is that the authorities have begun to respond to the downturn with more stimulus (as seen by yesterday’s actions from the BoE, ECB and PBoC). Some would argue that economic data are all different degrees of lagging indicators, so people may take more comfort from the forward looking financial markets having bounced since the end of June (although I think is misplaced optimism – political and fiscal union remains miles away, and the EFSF/ESM bailout mechanism is deeply flawed).

The bad news is that areas of the bond market are showing severe distress once more. Long dated Spanish government bond yields have jumped again, and yields are right on the intraday record high set on June 18th at the time of writing. Long dated Slovenian government bonds are yielding 7% amid mounting speculation that a bailout is imminent. And two year German government bond yields have again turned negative.

I’ve not read David Graeber’s “Debt: the First 5000 Years” yet – an anthropological investigation into the origins of money and debt – but have had it highly recommended to me and the reviews on Amazon suggest it’s a staggering original work. So I’ve bought a job lot for the team, and 10 extras for you to win in today’s competition.

Question: Denmark yesterday cut official interest rates on its certificates of deposit. To what level?

Please submit your answer by 5pm on Thursday 12th July 2012. The first 10 correct answers out of the hat will win a copy of the book. This competition is now closed.

I recently returned from Chicago after a research trip. We put together a short video to share a few of our findings with the wider world. The mood of most economists, investors and indeed the man on the street was noticeably more upbeat than in Europe. With positive GDP growth, a housing market showing the first signs of stabilisation, if not growth, and – in our opinion – a banking system that is in better shape than its European equivalent, the US continues to provide a more benign context for High Yield investors. Indeed, whenever we encountered concerns and pessimism it was firmly focused on this part of the world. Consequently, we continue to find some interesting themes and opportunities in the US, both from a top down perspective and also for individual issuers and bonds.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.