oil

Not all oil-exporting countries are the cracking winners you think.

By Charles de Quinsonas

4 June 2026

The US bond market expects the Fed to start raising rates again at the start of 2010, if not earlier. The bond market is usually right, but maybe not this time. A speech last week by influential San Francisco Fed President Janet Yellen (seen as a possible candidate for Bernanke’s job, should he not get reappointed next year) suggested that keeping Fed funds rate at zero for several years is “not outside the realm of possibility”, and also talked about the problem of not being able to cut interest rates below zero (“if we were not at zero, we would be lowering the funds rate”). The risks involved in returning to “normal” too quickly were echoed in a guest article in the Economist by one of President Obama’s economic advisers, Christina Romer. Called The Lessons of 1937, it warned that the withdrawal of monetary and fiscal stimulus just as the Great Depression appeared to be coming to an end led to a second, severe downturn.

Historically, bond markets don’t enter a bear market until the Fed starts hiking (see charts), and the Fed doesn’t start hiking until unemployment is falling. Of course explosive government borrowing and massive bond issuance are factors which haven’t been present to this degree in the episodes we show, and we must accept that revulsion from the sheer quantity of bond issuance might trigger a bond bear market even if inflation and rates are low – but neither have we ever seen western governments doing quantitative easing and buying back their own debt.

One of the most widely read economics speeches in history is Bernanke’s Deflation: Making Sure “It” Doesn’t Happen Here of November 2002. I remember seeing a well connected economist around the time that it came out, when the Fed was petrified that core CPI was heading towards just 1%. The economist claimed that the Fed was discussing various “helicopter drop” type scenarios to inject liquidity into the consumer sector, to try to avoid becoming Japan. One of these ideas was that the Fed would drive armoured cars full of dollar bills into football stadia around America, and buy secondhand cars directly from anyone who wanted to sell them one. I told this as an aside to a client yesterday, as an illustration as to what the authorities might do in extremis – before suddenly realising that we are already there. Click here if you want to sell your secondhand car to the government. We must understand that we are now in extremis.

Two deflation anecdotes. Unprompted, I’ve had two drivers from a major corporate cab provider tell me that they wished that head office would cut the rates that they get paid to help reverse a huge collapse in demand, and a friend who’s a personal trainer for a national gym chain said the same – his charge out rates are much too high, and he’d rather take a pay cut and get a bit more work. The latest June employment data show that there is now zero wage growth in the US economy – perhaps unsurprisingly in an economy that has lost 6.5 million jobs since the start of this recession. Perhaps the scariest chart I have for you today shows you capacity utilisation rates in the US, EU and UK. All are now at record lows, and still falling. With a third of US capacity currently unused, the scope for further radical restructuring and job cuts must remain high.

And finally, and completely unrelated to bond markets, but combining three of my favourite things – Manchester, Kraftwerk, and cycling – I give you a video of Kraftwerk playing Tour de France at the Manchester Velodrome last week, complete with surprise appearance on the circuit by Team GB at around 4 1/2 minutes in. Altogether now – “En danseuse jusqu’au sommet/Pedaler en grand braquet/Sprint final a l’arrivee”. And “chapeau!” to Mark Cavendish.

Some interesting ideas about how Japan (and by extension the rest of us) can get out of the deflation trap in today’s Times. The article, "To fight deflation, abolish cash", proposes that getting rid of physical money will allow policy makers to do something not possible in a world where the population can hoard bundles of bank notes in sock drawers – namely to set an effective negative nominal interest rate. Many economists suggest that Japan needs interest rates of around -4% (and a similar number has been talked about for the Euro area). Abolishing yen notes and moving fully to electronic payment systems would allow policy makers to apply negative interest payments to "hoarded" money, and thus encourage spending rather than saving. Whether it would simply encourage spending on gold bullion and foreign banknotes is another question, but whether it’s spending on non yen financial assets or on domestic consumption, negative nominal rates should eventually generate inflation. Such a radical measure in an economy where the amount of cash circulating is over 6 times higher than in most developed economies is unlikely to be implemented, despite some political support, which in part explains why the Japanese government bond market continues to expect average deflation of -2% per year for the next decade.

Today we saw the release of May’s inflation data, which came in a little higher than the market expected. CPI is running at 2.2% on an annual basis, and RPI remains in deflation, at -1.1%. Food and energy prices continue to be disinflationary factors, whilst the prices of DVDs, TVs, clothing and footwear rose. There was a rise in average mortgage payments too, which impacted the RPI number, probably due to people coming off low fixed rate deals – not good news for consumer spending going forwards.

We’ve just seen the Bank of England’s Q2 Quarterly Bulletin, which contains a paper called Public Attitudes to Inflation and Monetary Policy. Median perceptions of current UK inflation have fallen from over 5% at their peak in August 2008 to 4% now, but they remain much higher than actual inflation. The biggest cohort of respondents (about a third) thinks that inflation now is over 5%. The Bank’s survey shows that people pay relatively little note of falls in their mortgage payments when they think about their own personal inflation rate, which explains why perceptions of inflation remain elevated at a time when RPI (which takes account of lower mortgage payments) has moved into deflation. People are much more sensitive to household energy bills, food and drink, and transport costs (you go grocery shopping and fill up your car more often than you have a mortgage direct debit go out, and so inflation in food and petrol is much more noticeable). This is a bit of a shame, for the Bank of England’s monetary policy can only really target (and then only indirectly) the mortgage rate.

The research paper also discusses the role of the media in setting price perceptions. It’s interesting to note that for the first time, the number of UK newspaper headlines about falling prices has overtaken those about rising prices. Perhaps this in part explains why, looking forwards, expectations for future inflation have fallen significantly. 25% of participants think that there will be zero inflation, or deflation in a year’s time. The biggest factor in the perception of future inflation is now “the strength of the British economy” – the Bank suggests that this too might be down to a deluge of negative headlines on the economy (over 1,400 such headlines in the past quarter, and not just in the Daily Mail).

The Bank’s own conclusion is interesting – the Bank of England’s inflation target is not very important in the public’s one year ahead expectations of future inflation! The Bank does still hope however, that longer term expectations are influenced by the MPC’s 2% target.

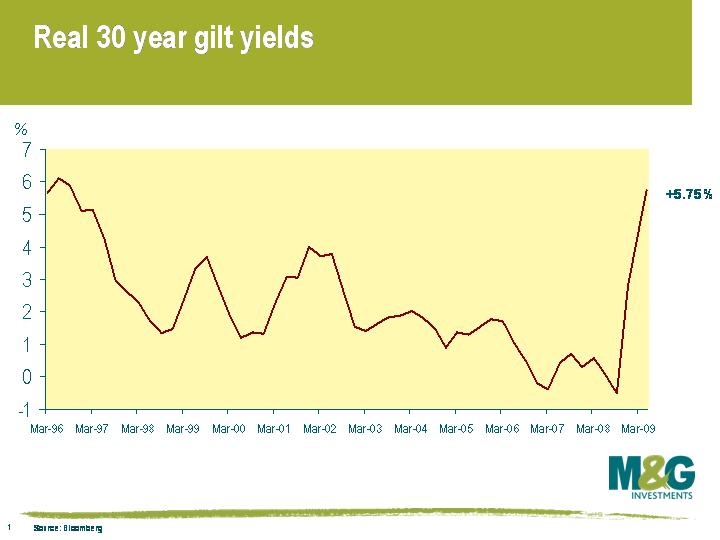

Right now the most commonly submitted question to this blog is about the impact of QE, high budget deficits and zero rates on inflation. Most people are inclined to think that after a brief period of deflation, largely as a result of lower year on year energy prices, we’re heading into hyperinflation. I guess my cop out answer to that question is that we just don’t know – it is uncharted territory, and of course, as good bond vigilantes, we are very nervous in particular about the levels of government borrowing (even though the relationship between high deficits and low bond prices is poor) and also about the way in which central banks will manage to exit QE (do gilts tank on the day that the BoE says it’s ending, or reducing, its repurchase programme?). As a result we have small short duration (i.e. bearish) positions on in our portfolios. But it isn’t a strong conviction position, and with the recent selloff in government bonds, real yields are as high as they’ve been since 1997 and perhaps we should be buying government bonds again. The real yield (the bond yield adjusted for inflation) of the 30 year gilt is now 5.75%, having been at minus 0.5% in 2008.

So rather than answer that question in detail, here is a link to a piece by the New York Times columnist Paul Krugman called The Big Inflation Scare, which debates these issues. It concludes that we are still very much in a deflationary world as output gaps increase, that the current forms of QE are having no inflationary impact, and finally that governments can cope with elevated levels of debt without having to resort to inflating it away. Krugman quotes economist Ralph Hawtrey’s comment about those who fretted about inflation during the Great Depression: “Fantastic fears of inflation were expressed. That was to cry, Fire, Fire in Noah’s Flood”.

So rather than answer that question in detail, here is a link to a piece by the New York Times columnist Paul Krugman called The Big Inflation Scare, which debates these issues. It concludes that we are still very much in a deflationary world as output gaps increase, that the current forms of QE are having no inflationary impact, and finally that governments can cope with elevated levels of debt without having to resort to inflating it away. Krugman quotes economist Ralph Hawtrey’s comment about those who fretted about inflation during the Great Depression: “Fantastic fears of inflation were expressed. That was to cry, Fire, Fire in Noah’s Flood”.

And could the recent sell off in government bond markets itself trigger a new wave downwards in economic activity, and an even bigger output gap? Yesterday in the US, Freddie Mac announced that the 30 year mortgage rate had hit 4.91%, a leap of over 75 bps in a handful of trading sessions. This means that millions of US homeowners will no longer find it possible to refinance their existing mortgages at attractive levels, and could cap any recovery in consumer spending. It’s also bad news for a banking sector that still owns billions of dollars of mortgage bonds. Risky assets have rallied hard as hopes of a V shaped recovery have multiplied – but it might be time to pause for breath.

In a speech this morning, the Shadow Chancellor George Osborne hinted that he might change the UK’s inflation target if the Tories form the next Government (and it’s difficult to see how they can muck it up from here). Currently the Bank of England must set monetary policy to keep CPI inflation within the band 1% to 3%, and must write a letter to the Chancellor in the event of "missing". With the benefit of a bit of hindsight, commentators are saying how stupid it was not to also target house price inflation (and to be fair to Mervyn King he had publicly criticized the CPI measure on that basis as long ago as 2006), and that by ignoring them, rates were kept too low for too long, and the property bubble resulted.

It’s hard to predict what a Conservative inflation target would look like, but let’s assume they are elected in May 2010, and that they include some measure of house price inflation (HPI) in their target. Let’s also assume that this house price crash is as long and severe as the last one from mid 1989 to mid 1995 (chart here). If that were the case, then although we’ve seen the steepest falls in prices, we might not see a rising trend in prices until 2012 or 2013. On this simple, and highly speculative analysis then, including house prices in the Bank’s inflation target could cause them to keep interest rates lower than under the current regime for the next few years (the electorate won’t complain about that). We could eventually therefore see higher levels of core inflation for a given level of interest rates. The bond markets won’t like that. It is also possible that if housing prices did boom again, that the Bank would have to live with negative core inflation rates (deflation) until house prices stabilised again. The appropriate weighting of asset prices within an inflation target is going to be the topic of a very interesting debate.

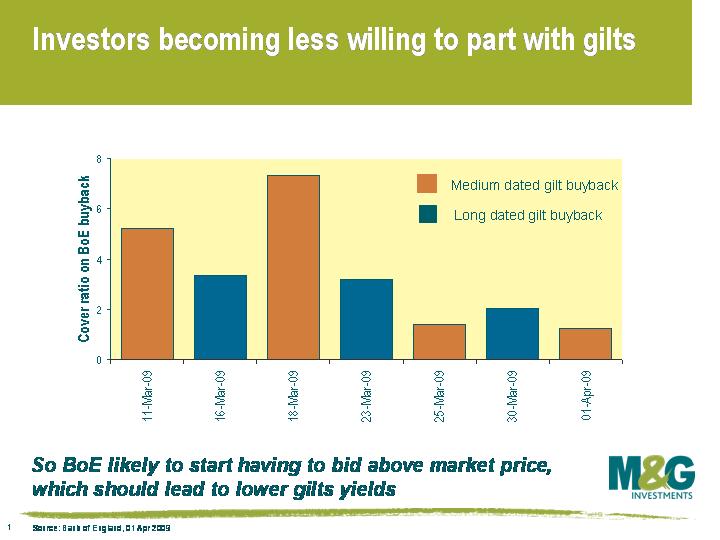

It’s still early days in the UK’s QE process, so the 7 data points we have from the gilt buyback programme to date are insufficient to draw too many conclusions from. However, this chart does seem to show that participation in the reverse auctions has been declining. The first 3 auctions had an average cover of 5.3 times – so for every gilt that the Bank bought back, there was over 5 times that amount offered. The last 3 auctions had an average cover of just 1.56 times. What’s more, the most recent buyback saw the Bank pay a healthy premium to the prevailing market prices.

It’s still early days in the UK’s QE process, so the 7 data points we have from the gilt buyback programme to date are insufficient to draw too many conclusions from. However, this chart does seem to show that participation in the reverse auctions has been declining. The first 3 auctions had an average cover of 5.3 times – so for every gilt that the Bank bought back, there was over 5 times that amount offered. The last 3 auctions had an average cover of just 1.56 times. What’s more, the most recent buyback saw the Bank pay a healthy premium to the prevailing market prices.

It’s possible that the "looser" holders of gilts (hedge funds, investment banks, market makers) have now got out of their positions, having made some profits by buying gilts ahead of, and immediately after, the Bank’s QE announcement. The next wave of gilts might prove to be harder to dislodge. These are the gilts owned by "real money" accounts, including pension funds and mutual funds. I run a gilt fund, what am I going to do if I sell my gilts to the Bank? I have to own the asset class. What’s more, isn’t QE the game that pays you not to play? The Bank wants to get gilt yields down substantially, so if I sell my gilts to them a little above the prevailing market, doesn’t the market move up to that level straight away, and then higher again at the next buyback? Paul Fisher of the Bank of England said that they are not price sensitive, and given that they are not even a third of the way through the first wave of buybacks (they will have bought back £25 bn of gilts by the end of next week), the next £50 billion of "sticky" gilts might come out at higher and higher levels.

A final thought – why have the £75 billion "quantity" target for purchases of gilts? Wouldn’t a statement that the Bank of England is going to buy gilts back in order to target 10 year gilt yields at, say 2% (they are currently 3.36%), cause the market to move there without the need for many purchases at all? And if they want to still pump the £75 bn into the market, both a quantity and level target might be a more powerful dual mechanism.

Central bankers passionately love inflation-linked bonds. Firstly, they keep governments honest by discouraging them from generating inflation in order to reduce their debts, and secondly they provide real “put your money where your mouth is” information as to where the financial markets think inflation is heading. Unfortunately, the Bank of England’s new QE regime makes the information derived from index-linked gilts useless – and in a perverse way too.

Just at the time when everybody is worrying that QE is the first step on the road to the issuance of Zimbabwe style One Hundred Trillion Dollar notes (I have one in front of me as I type, the watermark is a picture of a buffalo’s backside), we’ve seen a collapse in the expected future level of inflation in the UK, according to the gilt market. In February, before the Bank’s QE announcement, the 10 year breakeven inflation rate was just below 2.5%. It subsequently halved to 1.25%. In other words the bond market expected half the level of inflation over the next ten years than it had before the Bank turned on the printing presses. As I said, perverse.

The problem is that the Bank’s QE programme only targets ordinary gilts (£75 billion of them). Index linked gilts are excluded (for liquidity reasons) and have therefore missed out on some of this big rally. Conventional gilt yields have therefore fallen further, and dragged down the breakeven inflation rate (the difference between nominal (conventional) and real (index linked) yields). This is probably an unintended consequence – but in so far as this “information” is used by wage setters and policy makers, might it in itself prove deflationary?

Since the height of the QE driven conventional market rally, linkers have caught up a little (the implied inflation rate has risen to 1.75%) – but the fact remains, if QE excludes linkers, then the information contained within their prices will become less valuable. Perhaps this is why the Bank has recently placed more emphasis on survey data (the Bank of England/GfK NOP Inflation Attitudes survey) when they talk about future inflation expectations?

Today we get to see how the Bank of England’s Quantitative Easing process works. I will post again, in the comments section of this article, when we know the results of the Bank’s gilt buy back this afternoon (sometime after 2.45 pm). This is a £75 billion programme, with the first £2 billion of purchases being sought in gilts maturing from 2014 to 2018. These are as follows:

UKT 5% 2014

UKT 4 3/4% 2015

UKT 8% 2015

UKT 4% 2016

UKT 8 3/4% 2017

UKT 5% 2018

These bonds currently yield from 2.17% to 2.86%, and as Richard showed in yesterday’s blog, they have rallied aggressively since QE was announced alongside the last rate cut. The longest of these gilts has risen by nearly 4.5% in price since that announcement. The Bank will decide which stocks to buy, and in what proportions based on the highest yields submitted by market participants relative to where those gilts were trading before the reverse auction began. It’s therefore possible that the full £2 billion could come from as little as one gilt issue if that is where the “cheapest” offers come from. Other points to note: the Bank is not buying back sub 5 year paper as part of this programme, as that is where overseas Central Banks (big financers of the UK budget deficit) own gilts, and it could lead to a big reduction in the gilt market’s investor base and a possible knock on impact on the £ if overseas investors sold their gilts back to the authorities. Nor is the Bank buying gilts over 25 years in maturity, which would exacerbate the illiquidity in ultra long dated gilts, and possibly cause further problems for pension funds. The estimated UK deficit at the end of February according to the Pension Protection Fund (PPF) was £219 billion – but gilt market movements since then, even with no buy backs planned in ultra long gilts, could have increased this by £90 billion. The Bank also isn’t buying index linked gilts – but that’s worth a blog in its own right! Over the next 3 weeks, there will be a net reduction in the size of the 5 to 25 year gilt bucket of around 7%.

So how might today go? Perhaps the most important thing to note is that Paul Fisher, the new MPC member who is in charge of the Bank’s markets area (taking over from Paul Tucker who has been made Deputy Governor) has been intensively visiting market participants over the past few days. The explicit message to us is this: the Bank of England is not price sensitive. We will buy gilts at whatever level you want to sell them to us (because we want you to buy risky assets instead). This means that it is extremely dangerous to be short of the gilt market for the foreseeable future, and that far from being dear at 3% yields, ten year gilts could rally to 2%, or even lower (keep remembering that Japanese 10 year Government Bonds hit 0.5% yields in 2003). Incidently, the Wall Street Journal (subscribers only for the full article) is reporting today that the Fed has been impressed with the impact of the UK’s QE announcement and is ready to start buying back US Treasuries in a similar measure – Treasury Bond yields have marginally risen over the period that the UK gilt market has seen its mammoth rally.

Update to follow this afternoon, and we’ll let you know what we did, if anything, and whether it turned out to be a good idea.

We wrote about our January research visit to the States in our recent Letter from New York, but whilst we were there we also took along a £75 video camera and shot a few clips.

Bond Vigilantes – New York research trip – January 2009

The team has just watched I.O.U.S.A., the film about the future American disaster brought about by unbalanced government budgets (Dick Cheney: “Reagan proved deficits don’t matter”) and, in particular, unfunded Medicare and Social Security liabilities.

We’re giving away our copy of the DVD. To win it, send your answer to the following question to bondvigilantes@mandg.co.uk. The first correct answer we receive gets the film.

What happened when Dick Cheney went quail hunting in February 2006?

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.