oil

Not all oil-exporting countries are the cracking winners you think.

By Charles de Quinsonas

4 June 2026

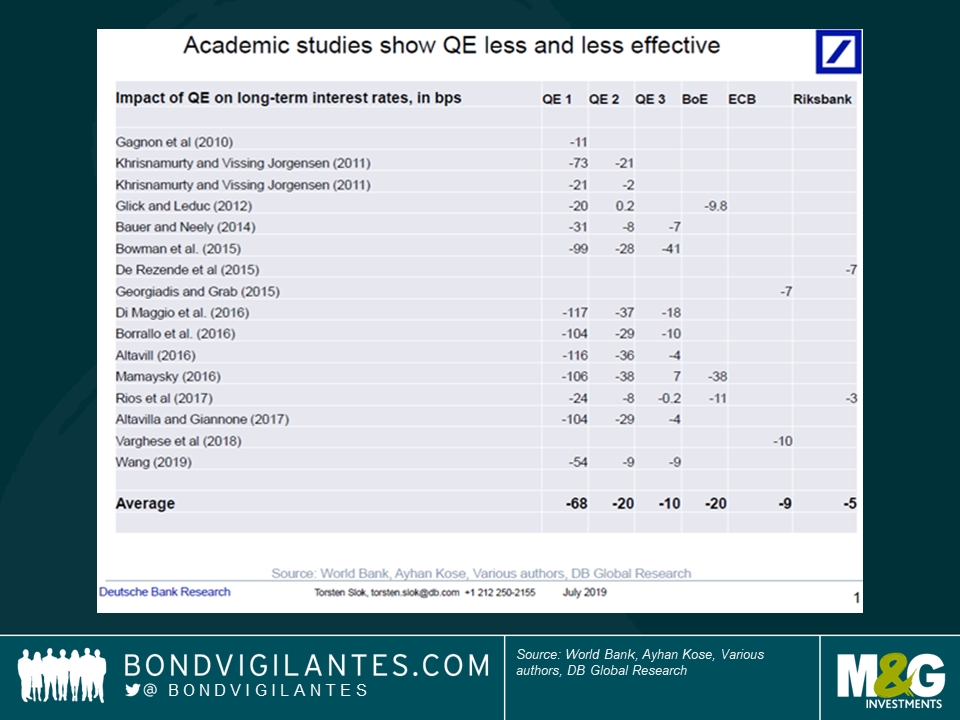

A decade on from the Global Financial Crisis after multiple rounds of QE across the developed economies, we are stuck with mediocre growth rates, the anticipation of renewed policy easing and the prospect of yet more bond buying from the ECB.

Yet much of the academic research into the impact of QE suggests there are diminishing returns from successive bouts of bond purchasing. It also seems likely that by boosting all asset prices in distorting the value of the risk free asset (gilts, treasuries, bunds etc) the unintended consequences – like a rise in inequality – might be doing more harm than good.

In this short video I interview the famous financial author, Frances Copolla, about her new book – ‘The Case for People’s Quantitative Easing’ – the cover of which shows a helicopter dropping bank notes on the town below. That should give you a clue as to some of her suggested alternative ways to stimulate economic activity! Whether policy makers are willing to go that far is debatable, but policies like student debt relief, or money printing to fund a Green New Deal could certainly find real world support.

We are also running a competition to win a copy of Frances’s book. To win a copy, answer this question: how much QE has the Bank of England done in the U.K.?

[This competition has ended]

Over my 25 years in bond markets, there’s always been one trade that becomes known as “The Widow-Maker”. Being underweight long-dated gilts was one, at a time when new pension regulations sent yields plummeting, and shorting the Japanese bond market also became deadly as the Bank of Japan slashed rates to zero. Today, widows and widowers are being made in the German bund market. Yields on the 10 year bund are now trading at record lows: bond investors pay 31 bps per year for the privilege of lending to the German government.

As yields collapse, forecasts and expectations are quickly revised lower. In the wake of Mario Draghi’s ECB speech last week we even saw one investment bank speculate that the 10 year bund yield could fall from that -0.31%, to -2%! Madness? Well Draghi was incredibly dovish, and it’s easy to read his speech as being as important as his famous “whatever it takes” line in the midst of the 2012 eurozone crisis. We’ve already had more than €2 trillion of quantitative easing (QE), negative rates, forward guidance promising to keep rates low, and cheap loans to banks – what more could we possibly get?

Well, more of all of the above. Draghi is petrified by the collapse in eurozone inflation expectations, and by core CPI at just 0.8%, on top of horrible manufacturing figures and looming trade wars. As the Fed readies for multiple rate cuts in the US the € is strengthening against the $ too, another headwind for the eurozone economies. So he talked of the ECB not resigning itself to “too low inflation”, and of downside risks to the economy. Clear improvement is needed or easing stimulus “will be required”. This is likely to involve a cut in the ECB’s deposit rate more deeply into negative territory (the ECB has made peace with its negative interest rate policy at last), and the resumption of QE.

That resumption of QE does create more problems for policymakers though. Whilst the European Court of Justice (ECJ) has said that QE is legal (unless it serves to mask market expectations of default), there are limits on how many bonds the ECB is allowed to buy. Presently this is set at 33% of any outstanding issue, and that’s a problem when the Germans ain’t making bunds anymore. In pursuit of what they call “Black Zero”, Germany is running a budget surplus every year, which has seen its debt to GDP ratio fall dramatically in recent years. This means that bund issuance is exceptionally low, and that the ECB will quickly reach the limit on how many it can buy as part of any new QE programme. The market expects the 33% limit to be lifted to 50% in the event of any new QE, but to quote that investment bank “-2% forecast” note, bunds are “scarce potatoes”. Quantitative Easing will reduce bond yields further, but for bunds this result will be magnified greatly.

So how do you get from -31 bps yield to -200 bps yield? Well you need aggressive deposit rate cuts, from the current -40 bps to -120 bps. What does this do to Europe’s fragile banks? Do they become less profitable? Do households and companies hoard banknotes in safes to avoid negative rates? You also need the German yield curve to flatten (long dated yields falling by more than shorter dated yields) to something that looks like Japan’s, and for those bund “scarce potatoes” to become more expensive relative to other European fixed income assets. We still come back to the question – is it logical to pay someone to be able to lend them money? But we must also come back to John Maynard Keynes’s overquoted words – “the markets can remain illogical for longer than you can remain solvent”. Beware the Widow-Maker.

This article originally appeared in Investment Week – Read here

This week the 10-year German bund yield hit a new record low of -0.33% in the wake of Draghi’s Sintra speech which had echoes of his 2012 “whatever it takes” declaration. Why so dovish? Manufacturing data from the eurozone has been universally bad lately, and inflation expectations are collapsing. The core inflation rate is now just 0.8% and the ECB’s 2% target looks an impossible goal. The market expects that, on top of the previously announced TLRTOs (cheap money for banks to encourage them to lend) and dovish forward guidance, the ECB may cut the deposit rate further from -0.4% and restart quantitative easing.

Germany had been a bright point of eurozone growth until a year ago. Annual GDP growth hit 2.8% at the end of 2017 with its export-led economy benefitting from strong global activity. However, as China slowed, Trump’s trade wars began, and with a perfect storm of factors leading to the stalling of auto sales, that annual growth rate has fallen to just 0.7%.

In the “good years”, the German unemployment rate fell sharply. It remains around 5%, down from over 8% a decade ago, and wage growth has been strong (+4.6% year on year). Yet consumption growth has been mediocre. The German household is famously a saver, not a spender. Private consumption growth has averaged just 1% per year since 2006, well below wider economic growth.

Back to the ECB. One of the factors that it has identified as holding back economic growth in the eurozone is the weakness of the region’s banks. In this paper from earlier this year, the ECB says “clearly, bank profitability matters for financial stability. Profits are the first line of defence against losses from credit impairment. Retained earnings are an important source of capital, enabling banks to build strong buffers to absorb additional losses. Those buffers ensure that banks are able to provide financial services to euro area households and businesses, even in the face of adverse developments, thereby smoothing rather than amplifying the impact of negative shocks on the real economy. Euro area banks have certainly improved their profitability in recent years. Their return on equity reached 6% at the end of 2018, up from 3% two years earlier. But their profitability remains below their long-run cost of capital, which most banks estimate to be in the range of 8-10%. Low profitability prospects translate into low bank valuations, as observed in price-to-book ratios well below one, hindering the ability to raise capital, where needed. Why do eurozone banks have lower profitability than their global peers? In part, there are way too many of them. This paper from the European Parliament says that “large European banks only earn half to three-quarters of what their American peers do relative to their asset base. Competition dynamics limit banks’ ability to charge fees”. In Germany, just 31.4% of total assets are at the 5 largest credit institutions; this is the second lowest percentage in the eurozone. Germany is arguably overbanked.

So, we have weak household consumption, and too many lowly profitable banks in Germany. What could kill two birds with one stone? Demutualising the German public savings banks, the Sparkassen.

There are over 400 German savings banks, with 50 million customers. These are run as commercial operations, but tend to be owned by cities, regional governments and charitable foundations. Some suggest that the low emphasis on profits, and “clubby” relationships with the businesses they lend to, result in a reluctance to deal with loss-making enterprises – a “zombification” of industry. Whether you think this is good or bad will depend on whether you think that keeping loss-making businesses alive holds back other ventures with higher growth/job creating potential. Their total assets are around €1 trillion, around 15% of Germany’s total banking assets. Politicians tend to be heavily involved in the running of these savings bank – in fact the Bruegel think-tank found that in North Rhine-Westphalia, politicians who chair a Sparkassen board receive an average of 12% of their income for doing so.

What would the demutualisation of the Sparkassen achieve? The UK gives some lessons, both good and bad. As a reminder, the 2007 Building Societies (Funding) and Mutual Societies (Transfers) Act (the Butterfill Act) allowed the UK’s 59 building societies to merge or demutualise. Around 15 of them did so, including Abbey National, C&G, Alliance & Leicester, the Halifax and Northern Rock. Savers in those institutions received a “windfall” of cash or shares. If you were in the Lambeth you got £500, whilst 7.5 million Halifax customers got 333 shares each, which were worth over £2000. This operated a little like helicopter money, although arguably the economy wasn’t in need of the stimulus at the time. The move from mutual to private ownership of the “builders” allowed many of them to merge or be acquired (the Woolwich went to Barclays for example). So there was less fragmentation in the banking market, and consumers received a boost, which is significant to many.

As well as being overbanked, Germany has a very weak equity culture. Only 13% of the population own shares (2014 data), compared with nearly half of American households – and the German number has been falling (down a third since 2001), meaning that households have not participated in the wealth effect of rising stock markets in recent years. Many Germans were frustrated by taking part in the popular Deutsche Telekom flotation, and as a result never bought shares again.

So, demutualisation of the Sparkassen could a) release windfall gains for German consumers and boost growth, b) provide less competition and boost profits for the banking sector (a double-edged sword this one, I know) and thus the wider economy, c) economies of scale and consolidation would improve banking efficiency, and d) there would be an equity market participation boost for German households.

So, did it work out well for the UK building societies? Up to a point, Lord Copper. Not one of the demutualised societies still exists as a separate entity, and some, like Northern Rock, went bust spectacularly. This excellent post-mortem from Phillip Inman suggests that only the CEOs benefitted from the demutualisations. And it is likely too that reduced competition in German banking, and higher fees, would reduce some of the macro benefits of a stronger banking sector, as well as eroding some of the “windfall” consumer gains.

A final thought. Does Germany “need” bright ideas to help it grow? In my years in bond markets, economists and strategists have been coming up with bright ideas to help Japan out of its terrible plight. This plight involves an almost negligible unemployment rate, low crime, high education, social cohesion and high levels of wealth per capita. That’s not much different from Germany today. Is low growth such a bad thing? Discuss.

In the years leading up to World War 1, and then the Russian Revolution in 1917, Russia had become the world’s largest net international debtor. It was borrowing heavily to finance industrialisation (railroads, oil, iron and cotton production) and as its population grew it saw rapid economic growth. WW1, and the earlier 1905 conflict with Japan had also resulted in rising debt. At the same time there was a globalisation of international finance, and French investors in particular were eager to lend to Tsarist Russia (Russian bonds are recommended investments, alongside British Consols, by a character in Proust’s Remembrance of Things Past, a book which, like me, you own but have not read).

Despite the rise of revolutionary pressures within Russia (Lenin had explicitly written that he’d repudiate the debt) and rising debt burdens that might have necessitated a restructuring even if there’d been no revolution, the money kept flooding in. An American bank (an ancestor of Citi) even opened a branch in Russia after the events of October 1917.

In 1918 the Soviets defaulted on the debts – in real terms this was a bigger loss for investors than suffered in Argentina in 2001, or Greece in 2012. Small investors in France suffered huge losses, and finance in post-revolutionary Russia came to depend on the “machine-gun of the People’s Commissariat of Finance”, aka the printing press.

In this short video I interview Hassan Malik, the author of Bankers & Bolsheviks, about this fascinating moment in economic history. You can also win a copy of his book by answering the question below.

Competition question: What was Leningrad known as at the time of the 1917 Russian Revolution?

Closing date is 5pm GMT on Thursday 14 February 2019.

[This competition has ended]

Whilst you can make some strong arguments for the negative returns from 90% of asset classes in 2018 based on the return of populist politics – think of Brexit, Italy’s political instability, AMLO’s election in Mexico and tariffs everywhere – the answer to those negative returns might be simpler: the de facto global discount rate, the 2-year US Treasury bond yield, has risen by almost 100 basis points (bps) over the year, and thus repriced global assets. Why did this happen?

For this and more, please view our 2018 review.

As we pass the 10-year anniversary of the Lehman default and we started thinking about what we were doing back in 2008 (desperately moving my savings out of certain banks was high on the list for me, whilst listening to MGMT and Los Campesinos; album of the year? TV On The Radio’s Dear Science), I went back to our blog, to see what the early warning signs were in the summer of that year.

It is useful to have a record to be able to look back on a market moving event to see what was actually the concern at the time, rather than just remembering the post-event narrative. We had been worried about the state of the US housing market (here’s just one example of our doom and gloom coverage of US housing in Richard Woolnough’s blog in January of 2008: but during trips to the US in June that year it was something else that was grabbing the 24 hour news channels’ headlines: oil.

House prices still get a mention in the June blog, but oil was at the top of America’s worry-list. And rightly so, as a spike in the oil price preceded 11 out of the last 12 US recessions. Rising energy prices slow the economy dramatically; the impact might be lesser today, especially in developed markets where energy efficiency is much higher than it was in, say, the 1970s, but higher oil prices hit both consumers and businesses. Which brings us to today. In the past 12 months the price of WTI oil in the US has risen from around $50 per barrel to $75 per barrel, a 50% jump. Gasoline prices remain way below the $4 per gallon they reached in 2008, but are still elevated at nearly $3. Growth will be slower in 2019 as a result.

If you don’t believe that this 50% rise is going to slow the US economy, then you might have more sympathy with the view that emerging market countries, with currencies that have fallen sharply in 2018, are going to be more severely hit. The chart below shows that for Turkey, an oil importer, the cost of oil has more than doubled year to date. I’d expect the US to outperform the rest of the world in growth terms in 2019, albeit with both at a lower level thanks to this mini energy shock.

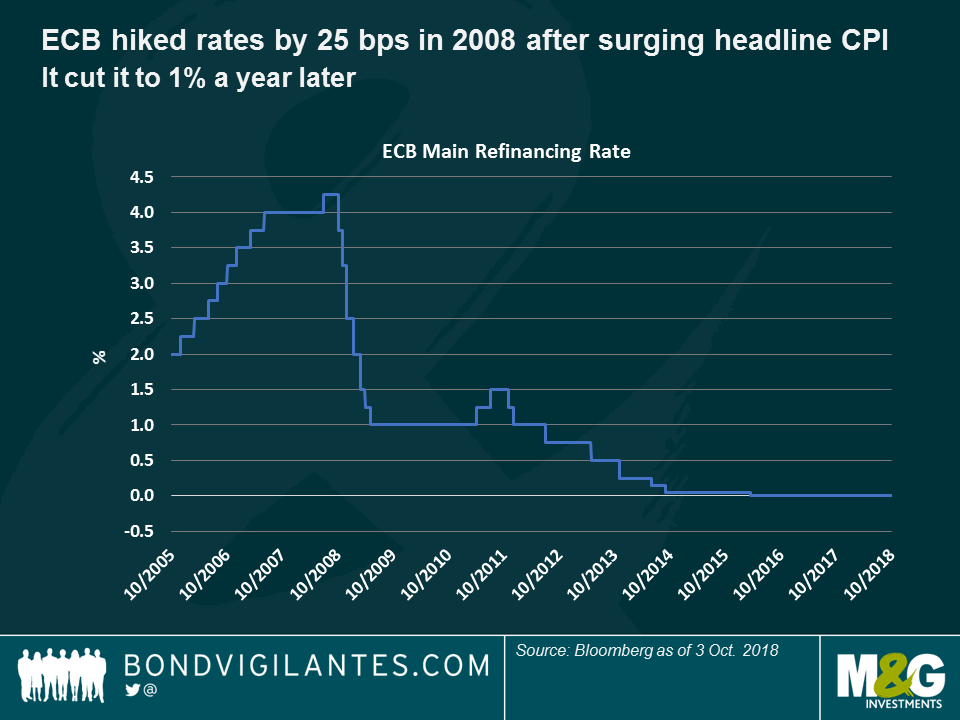

What else did I find in the “Summer of 2008” blogs? Well lots of talk about ECB tightening. The rise in energy prices had led to a headline CPI rate in the Eurozone of 4% in June 2008, double the central bank’s mandate. Short dated bunds were selling off as Jean-Claude Trichet stated that the ECB was on “heightened alert”. This is what we wrote at the time:

Trichet hiked rates by 25bps in July, despite the existence of a now defunct website http://www.stoptrichet.com/ collecting signatures to try to hold off rate rises. Rates at 4.25% would, of course, be the peak of that rate hiking cycle, and a year later rates would be at 1%.

Today we have an echo. Whilst we are not seeing anything like the 4% inflation that the Eurozone experienced in 2008, the recent trend is firmer, especially in Germany which just printed CPI at 2.3% year on year. And we have a central bank that is tightening in this environment. On 1st October the ECB halved its Asset Purchase Program (APP) from €30 bn per month to €15 bn, and anticipates that the programme will finish in December “subject to incoming data”.

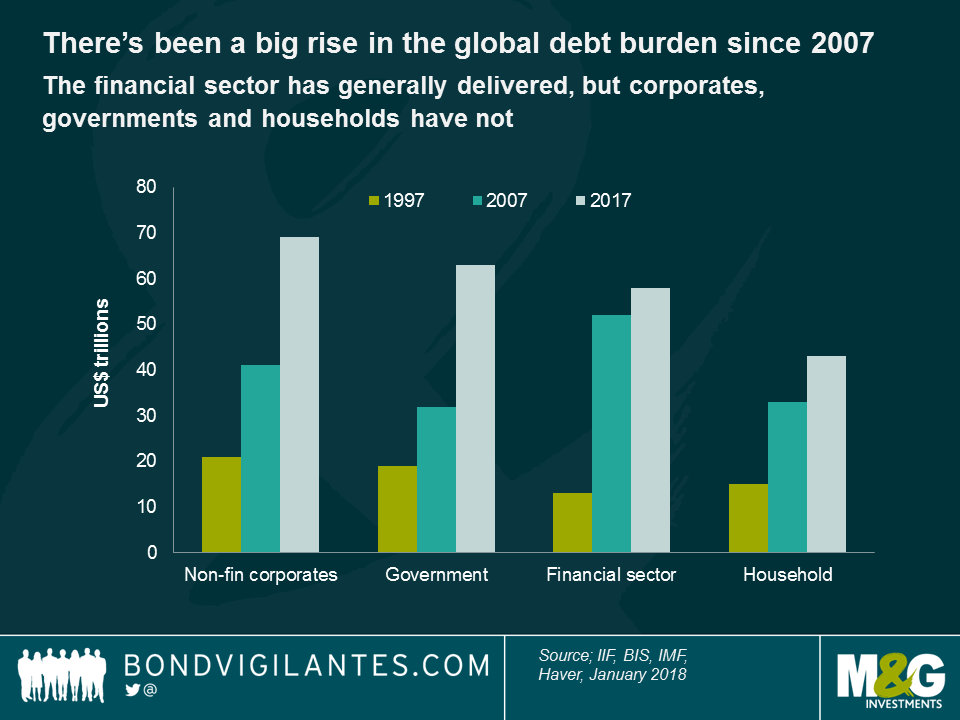

So, add monetary tightening from the European Central Bank (and of course from the Fed, Bank of England and many EM central banks) and a 50% rise in the oil price, and we have a scenario similar to the one we saw in the summer of 2008. But it IS different this time: we have substantially more debt in the global system than we did going into the last crisis. Gulp.

The IMF recently held a two-day public conference on sovereign debt at its home in Washington DC. How do we measure it? How have governments reduced it in the past, for example in the periods after the two World Wars? How can Japan carry debts of over 200% of GDP while other sovereigns have defaulted with virtually no public debt? And when things do go wrong, how do we sort out the mess of a restructuring in the absence of common legal standards or a concept of state “bankruptcy”?

The conference was designed to allow various authors to present and discuss chapters of a new book, Sovereign Debt: A Guide for Economists and Practitioners, which will be published in 2019. It’s going to have some great data and history in it, and will be a “must have” for bond investors.

In this short video I give a roundup of some of these discussions. The IMF has a reputation for gloomy forecasts for the world, and especially around the volume of debt outstanding (now well above the total debt burden we faced going into the Great Financial Crisis), and there was plenty here to be gloomy about. In particular, the Lower Income Countries (LICs – the poorest subset of the EM nations) have dramatically ramped up borrowing in recent years. As well as public debt issuance, there’s concern about their undeclared state guarantees, as well as direct and opaque borrowing from China, which is likely to turn out to be structurally senior to the bonds. There’s also nervousness about the growing mutual fund/ETF ownership of less liquid EM debt in recent years. One speaker quoted what’s apparently a Belgian saying: “Trust arrives on foot, but leaves on horseback”.

The draft papers from the IMF conference can be found here.

I was in Tokyo last week, seeing a mix of economists, JGB experts and clients. I was also awesome at karaoke, dressed as an astronaut.

The last time I was in Japan, over a year ago, I came away thinking there was a decent chance that the Bank of Japan would abandon its zero interest rate policy (ZIRP) as it was damaging banks’ profits, and sending a negative signal to Japanese households and businesses. At the time we were also seeing an uptick in core inflation and positive growth. It doesn’t feel like the BOJ has that view now. There’s no economic despair, but both growth and inflation have weakened, and Abe’s falling popularity raises the prospect of a new LDP leader later this year with less fiscally expansive views. We also have a dreaded consumption tax hike on the horizon – we know from past hikes that it means higher spending now, and a slump thereafter. There’s still plenty of good news too – unemployment rates even lower than the US, and a continuous rise in the female participation rate. In this 4 minute video from the Tachikawa Velodrome (no good reason, sorry) you can hear my views from Japan, and look at a) some cool charts, and b) keirin racers.

Finally, some anecdata. Did you know that post the 2011 tsunami, 43 of Japan’s 54 nuclear power stations remain offline. Before the earthquake they made up 30% of Japan’s electrical power needs. In order to save electricity the government introduced a policy called “Cool Biz”. From the start of June and throughout the summer months, all government and state workers are forbidden to wear jackets and ties to work (and private companies are encouraged to follow this policy too). In government buildings air conditioning is not allowed to kick in until the temperature is above 28 degrees centigrade. Ouch. We are all desperately leafing through health and safety legislation in the hope of being sent home when our ailing aircon here sees temperatures of 24 degrees…

We interview the academic and TV presenter about her choices of history’s most important economists, and ask what we can learn from them in solving our current problems. Also, win a copy of Linda’s book in our competition.

From Adam Smith, to Robert Solow, Linda Yueh’s latest book examines twelve important economists and suggests how we might use their thinking as we tackle modern society’s economic problems. How do we explain low wages? Is the west likely to experience 1930s style debt deflation? Who wins in a trade war? In this short video I ask Linda about her choices and go on to get her thoughts on the state of modern economics. We’ve got another competition too – I think you’ll love this book and we have five copies of it to give away. You’ll find the question and how to enter below.

Competition question

Who are these two economists?

[This competition has ended]

Former Bank of England Deputy Governor Paul Tucker has written a book about accountability and central banking. Have central banks become “overmighty citizens”, with too much power and insufficient democratic input? If so, does it matter and what can we do about it? In an era of QE, and bailouts of commercial banks, wealth inequality has widened in most developed economies. Did society agree that this outcome was what it wanted when central bankers “saved the world” in the Great Financial Crisis? I think this is an incredibly important book.

In this short video I ask Paul about these important dilemmas and what democracies should do about this “unelected power”. We’re also running a competition to win one of five copies of the book. You’ll find the question and how to enter below.

[This competition has ended]

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.