oil

Not all oil-exporting countries are the cracking winners you think.

By Charles de Quinsonas

4 June 2026

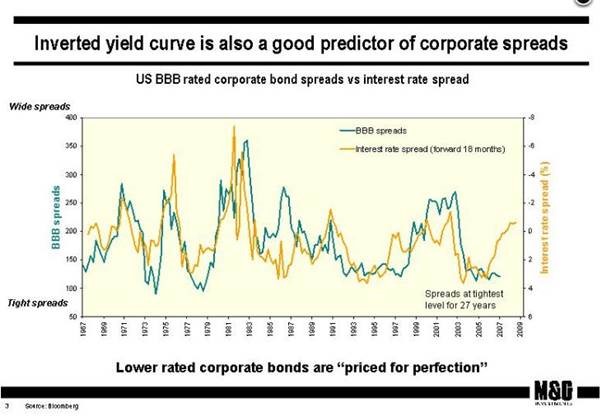

As the U.S. yield curve flattened to just 45 bps (2s-10s) last week, we dug out something I wrote back in 2007, in the early days of this blog. A chart that accompanied the blog showed that a) U.S. BBB credit spreads had hit their tightest level for nearly 3 decades and b) that the yield curve had flattened substantially (and in fact inverted). If you pushed the yield curve shape chart 18 months into the future it seemed to have a remarkable predictive power for what credit spreads would do next (not entirely surprisingly, as a flatter yield curve is traditionally a good indicator of economic slowdown). Thus, in 2007 it appeared to predict a big selloff in corporate bonds. Of course, all that happened, and more – credit spreads jumped to levels far higher than the 200 bps implied by the curve, as the Great Financial Crisis hit. But the directional call was sound.

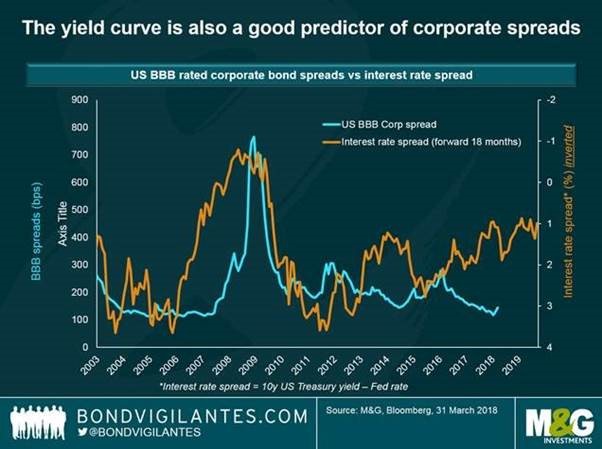

By popular demand. we’ve just updated the slide for the period since the Great Financial Crisis. As in the earlier chart we have extremely tight credit spreads (at similar levels to those seen in 2007), and like then the yield curve is very flat, although not in inverted, recession predicting territory.

Similar to 2007, there is a gap between the continued strong performance of BBB credit spreads, and the shape of the U.S. yield curve. Looking at the most recent data you would think that there is a good chance that credit underperforms from here. However, eyeballing the chart it’s also clear that the directional relationship between the two series is nowhere near as strong as it was pre-GFC. Look at the period 2012 to 2015 for example: the yield curve flattened substantially from +375 bps to just over +100 bps. Yet BBB credit spreads tightened aggressively over the same period. Of course, the post GFC world is also a world where quantitative easing from central banks drove an aggressive search for yield from investors, which not only reduced credit spreads, but consequently allowed corporates to borrow at lower rates of interest. Thus, default rates plummeted and the credit cycle has been incredibly elongated. Perhaps though the tailwind for this cycle is ending as quantitative easing tapers away, and central banks raise rates. The flattening yield curve must at least be a warning that credit valuations are now stretched.

Whilst I’m blogging again (I took most of the year to date off, having a social media break) I’d like to pay tribute to my friend and old Bank of England boss Hamish Watson, who died recently. Hamish gave me the chance to move out of the world of financial statistics (remember M4?) at the Bank and taught me everything I know about bond maths on the Bank’s gilt desk which he ran. He subsequently was one of the first staff members at the new Debt Management Office set up after Gordon Brown made the Bank independent in 1997. Hamish was a massive sports fan, and saw his beloved Aberdeen FC lift the Cup Winners’ Cup in Gothenburg in 1983. He was also Eddie George’s bridge partner (rather him than me – I trembled when the Governor even entered the room in his cloud of smoke). I doubt anybody knew more about gilts than Hamish did, and he was a genuine expert in his field, saving the taxpayer money by getting us a good price for ever increasing bond issuance. We’d meet for beers after he retired in the Blue Anchor by Hammersmith Bridge. He’ll be missed.

This year’s Davos World Economic Forum (WEF) comes at a time where equity and credit valuations look high, where we have “obvious” bubbles in cryptocurrencies, and where bond yields – perhaps an anchor for all financial asset valuations – finally seem to be moving higher. Global borrowing across governments, financial institutions, companies and households is at record levels. Can the global economy cope with higher interest rates? In this short video I talk to our CEO, Anne Richards, who has been talking on a panel at the Davos WEF on this very subject. Are we going to see another financial crisis?

Happy New Year to you all. Thank you for another bumper crop of entries for our Christmas quiz. This year’s winner and new reigning champion is Adam Begg of UBS Investment Bank. Many congratulations. As you know, this year we donated £500 to Cancer Research UK in lieu of a trophy. Via CASCAID, the fund management community in the UK this year decided to try to raise £1 million for Cancer Research UK and I’m very happy to say that it hit, and more than doubled that target. The totaliser now stands at £2.25 million. The money that you all kindly donated will do good. Thanks very much. If you enjoyed the quiz and wanted to bung a fiver into the pot, here’s your very last chance to do so: https://uk.virginmoneygiving.com/fundraiser-display/showROFundraiserPage?userUrl=JimLeaviss&faId=772830&isTeam=false.

Second place went to Michael Haslam of Barclays Investment Solutions, and third was Grant Robertson of Kuwait Investment Office. Well done.

Right, the answers:

Have a great 2018.

Here’s a short video I recorded with my multi-asset colleagues Steven Andrew and Tristan Hanson, in which we debate the highlights of 2017 and look ahead to 2018. After a year that has turned out to hold fewer surprises than many might have expected, what lies in store for financial markets in the coming 12 months?

Here is the 11th annual Christmas Quiz. 20 questions, and the closing date for entries is midday on Friday 22nd December. Please email your answers to us at bondteam@bondvigilantes.co.uk. The winner will get glory, and in lieu of a golden trophy, M&G has donated £500 to Cancer Research UK, through CASCAID. CASCAID is the UK asset management industry’s effort to raise £2 million for this brilliant charity over the course of 2017.

Breaking news: we did it! But please help us raise a few final pounds by the end of the year. If you’d like to donate a fiver as you enter, please do so at my charity page here https://uk.virginmoneygiving.com/fundraiser-display/showROFundraiserPage?userUrl=JimLeaviss&pageUrl=2 but it is totally optional, and I know a) many of you have been incredibly generous already, and b) I have bored on about cycling up hills enough for one year.

Good luck! Conditions of entry of down below somewhere.

Good luck!

I made what is turning into an annual pilgrimage to the brilliant Kilkenomics festival in Kilkenny, Ireland, last weekend, this time along with Eric Lonergan and Tristan Hanson from M&G’s multi-asset fund management team.

En route, we met some clients in Dublin and then took the opportunity to set the world to rights over a pint or two in legendary pub Kehoes. In these three short videos, we share our thoughts on, amongst other things, why economies are still struggling to generate inflation, whether interest rates can finally start to rise, inequality and the rise of nationalism, global debt levels and implications of all of these for markets.

(1) Central banks out of control? Political and economic confusion

(2) Do we have a global debt problem?

(3) Memories of ‘08 and implications for equities

I did it! On 12th November I rode up the 100th and final hill of my challenge, Cheddar Gorge in Somerset.

The UK asset management industry has now raised nearly £2 million over the course of this year through CASCAID. All this money will be going directly to Cancer Research UK. The target was £1 million, so a huge thanks to all those who have donated to the huge variety of different events and challenges that have taken part so far in 2017. We’re still a few quid short of £2 million though, so if you haven’t got round to sponsoring me yet, there’s still time to donate…

Here’s the link.

http://uk.virginmoneygiving.com/fundraiser-web/fundraiser/showFundraiserPage.action?userUrl=JimLeaviss&faId=772830&isTeam=false

The challenge.

I set myself the target of riding up 100 hills, mountains, or kops over the course of the year, roughly two per week. Most of the hills came from Simon Warren’s excellent series of guide books, starting with “100 Greatest Cycling Climbs”. I also allowed myself to cycle up steep things that aren’t covered in any of his guides if they met the criteria of being very steep and horrible; this let me ride climbs like Sa Calobra in Mallorca, and Tabayesco in Lanzarote too.

I rode my first hill of the year on New Year’s Day – Swain’s Lane in Highgate, London. It was raining, setting the pattern for virtually all of my UK climbing days (it was generally nice in Kent, but that was a rare treat for me). I moved on to the Chilterns, then a work trip to Hong Kong gave me a chance to ride up The Peak. Next were the Surrey Alps, some lumps and bumps in Oxfordshire, before heading out east to the short, sharp ascents of the Downs in Kent. My favourite day on the bike of the year was in Flanders, Belgium where I ticked off a number of cobbled climbs like the Paterberg and Oude Kwaremont (I also got to see Paris-Roubaix live the next day). Then up to the Midlands before a trip to Mallorca with my oldest friends. I did not achieve a PB on Sa Calobra. Boo.

West Sussex, Hampshire and “un jour sans” on the Isle of Wight where I bonked into headwinds, got lost, and made the ferry home only by throwing myself under a closing barrier. The Lake District threw up the hardest hill of my year – Honister Pass, which directly after Newlands Hause, had me seeing stars by the top. The hardest hill was followed by the funniest – a client meeting in Bristol gave me a chance to ride up Vale Street, the steepest residential road in the UK. On a hire bike and in suit and leather soled shoes which kept slipping off the pedals, it took me many attempts to get to the top.

Rides in Gloucestershire were followed by a day in the Manchester Peaks. None of us managed to even get 5 metres up The Corkscrew on another rainy day, but we did tick off five great hills that day, including the Cat & Fiddle. Kent again with a chain-gang that was a stretch to hang on to, before more trips to the south coast, including the nasty Ditchling Beacon which will be familiar for anyone who’s ever done the London-Brighton bike ride. A family holiday to Lanzarote let me ride up Tabayesco, the Ironman hill climb in the incredible volcanic landscape.

And finally this last weekend I did a couple of Bath hills, and ended up riding up Cheddar Gorge. Not the steepest of the year’s efforts, but long, beautiful, and for somebody with a 1989 vintage Geography A Level, somehow very familiar. I got a cheque from the Royal Geographical Society for £25 that year, such was the beauty of my exam paper – I’m not sure I have ever mentioned this to my friends and colleagues. You can see all of my climbs on Strava (follow Jim Leaviss).

Thank you.

Firstly thanks to all of you for the superb sponsorship support I’ve had over the year, and for encouragement from friends, family, and colleagues here at M&G. Thanks to Helen and all at CASCAID for running a fantastic effort, and nearly doubling the amount we all raised for Cancer Research UK. Finally thanks to Isobel and the kids for putting up with me disappearing off on the bike at weekends – it’s much appreciated.

See you on top of a hill.

Jim

The list of hills.

President Trump is likely to announce his choice for the next Fed Chair by the end of this month. Whilst current Chair Janet Yellen is still in the running, she has been slipping down the betting over the past few weeks. There are three good reasons why (from his perspective) Trump should re-appoint Yellen to the position.

Yet over the weekend “people familiar with the matter” suggested to Bloomberg that Trump “gushed” over Stanford University economist John Taylor, having interviewed him in the past week. Presumably Trump is aware that the famous Taylor Rule would likely result in the Fed hiking rates much more aggressively than the market currently expects (if you assume a neutral rate of 2% the Fed Funds rate might currently be at over 3.5%. Many believe the neutral rate is much, much lower nowadays, but even then a “rules based” Fed seems more inflexible than a businessman like Trump might desire).

Whilst he’s surging, Taylor’s not yet overtaken Powell at the bookies. But at 10-1 Janet Yellen is now a firm outsider. If I were Trump she would be my pick.

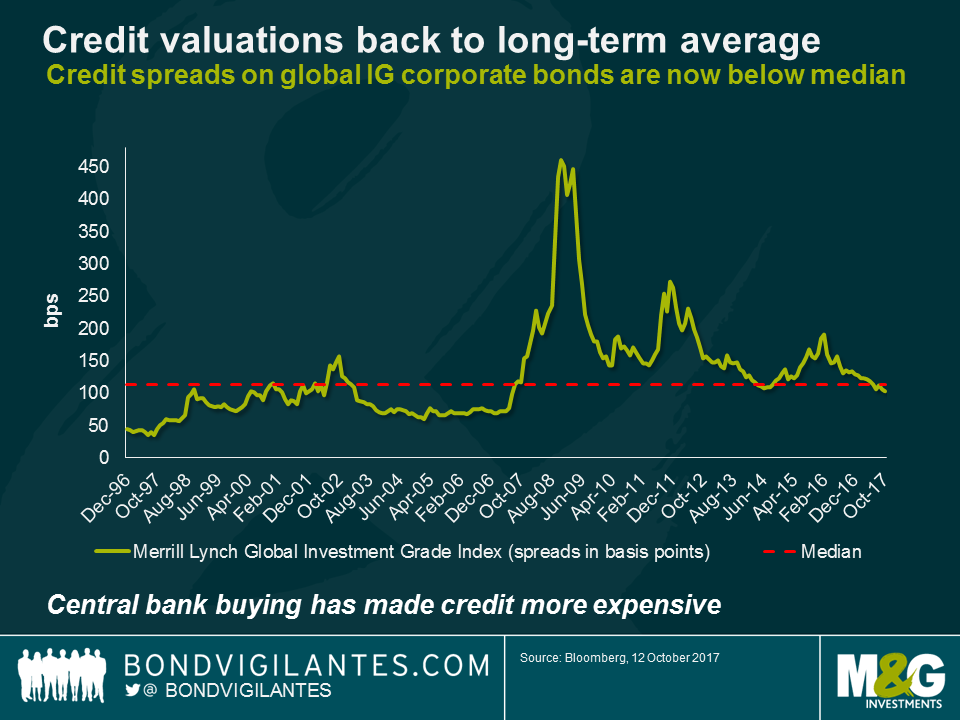

If you just looked at the overall global investment grade universe spread level, you could take comfort that despite the rally in corporate bond prices in the past couple of years (and particularly post the ECB’s decision to buy credit in its QE programme), valuations are simply back to their long term average.

Unfortunately the global investment grade bond universe has changed dramatically since the financial crisis, to an extent that makes this long term average almost meaningless. The quality of investment grade credit has seen significant deterioration in recent years. Partly this has been voluntary, with companies believing that adding leverage to their balance sheets can enhance equity returns (as well as taking advantage of the so-called “tax shield” of interest deductibility), but it also reflects the wide-scale credit downgrades that banks and financial institutions experienced during and after the credit crisis. For example, the issuer rating of Barclays Bank in 2007 was Aa2 with Moody’s, but today it is Baa2. Looking at the market as a whole we can see that in 2000, the nascent Eurozone credit market contained under 10% in BBB rated securities, and the US credit market a little over 30%.

Today, global credit markets are almost 45% exposed to BBB rated issuers, and trending higher. Remember also that credit ratings are not linear, but exponential – as you move closer to the boundary with high yield the risk of default increases significantly. Today’s global credit market has a much riskier credit profile than it did a decade ago.

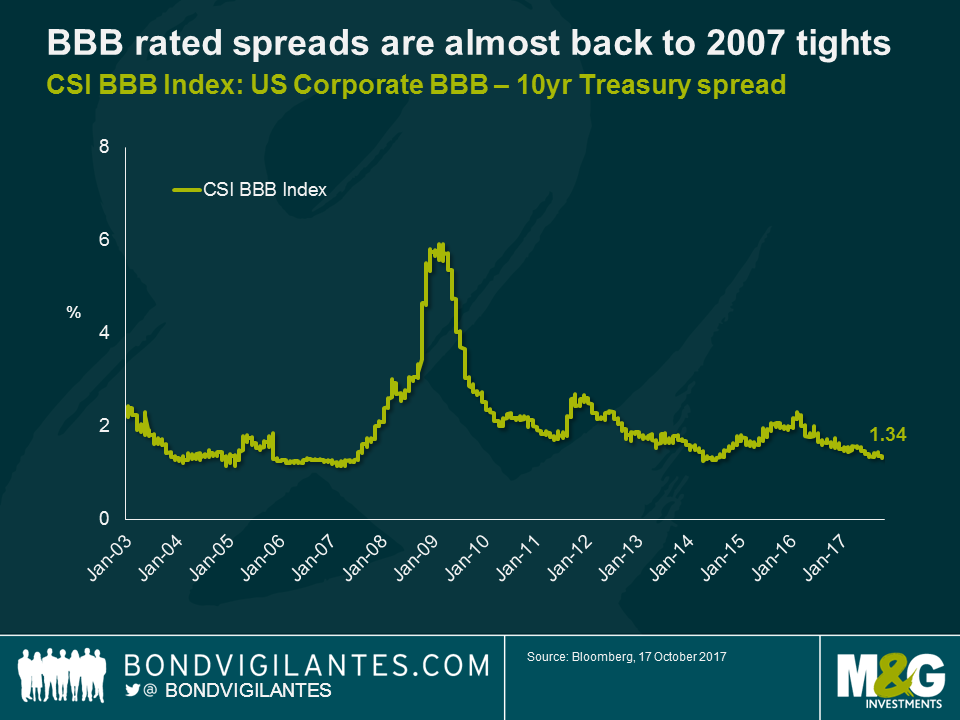

If we just look at the global BBB credit index spread, it’s clear that at 134 bps we are now near the 120 bps low spread that we saw in 2007, the peak bubble year before the GFC, and well below the average 200 bps spread that BBB rated assets have paid since 2002.

So rather than being “fair” value, global credit has moved into expensive territory. There are some good reasons for this, including the aforementioned QE buying of credit by the ECB, the fact that default rates remain very low (for all credit including high yield the default rate could be 1.5% for 2017, compared with over 2% in 2016), and the ongoing, huge, demand from US investors in particular for income producing assets (look at ETF flows into US$ IG funds). But the plain fact is that this is a market where credit quality has deteriorated, and the rewards for risk taking are much lower than they were.

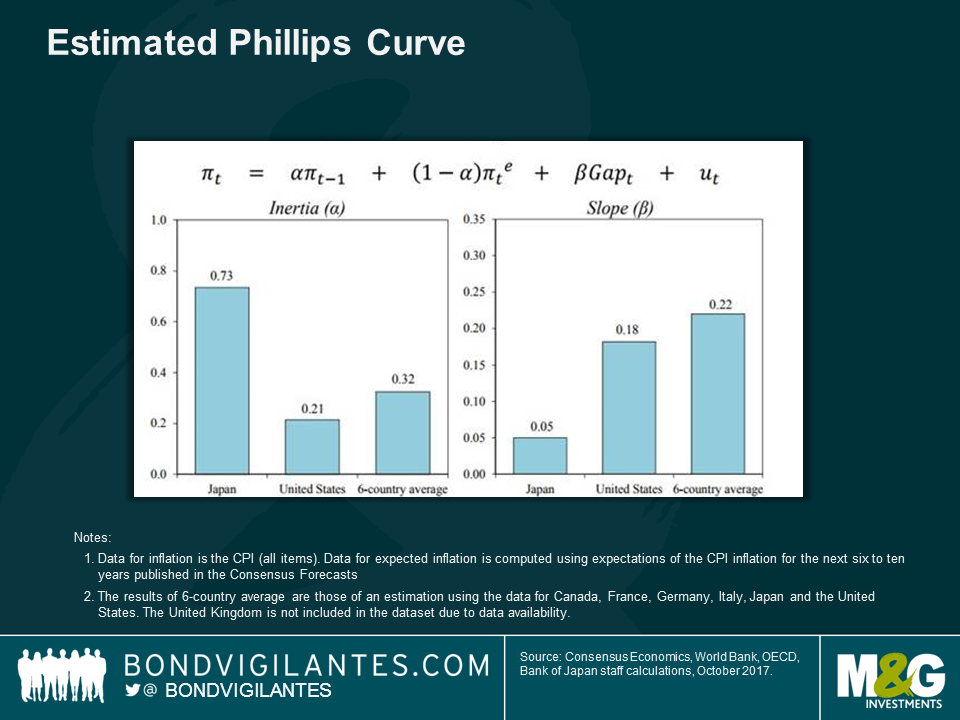

The Deputy Governor of the Bank of Japan, Hiroshi Nakaso, was in London a couple of weeks ago, with an upbeat assessment of the potential growth of the Japanese economy. You can see his slides here. Of Abe’s “3 Arrows” (fiscal policy, monetary policy and structural reform), the speech sensibly seemed to suggest that only the latter would really have any impact on Japan’s growth prospects. In particular Nakaso was bullish on the prospect for labour force growth from the elderly and non-Japanese workers (Japan’s female participation rate is now above that in the UK and US). But on the monetary policy side I thought the below slide was interesting. It shows a Bank of Japan decomposition of Japan’s Philips Curve compared to other nations. Firstly we should note that Japan’s Philips Curve is MUCH flatter than those in the US and elsewhere (right hand chart). Its unemployment rate has fallen to 2.9% from 5.5% with virtually no wage growth. But secondly we should be worried about the left hand chart. The “inertia” shows that low inflation in Japan is largely driven by the fact that inflation was low in past periods. In other words the expectations element of the Philips Curve is much more important in Japan than in the US or elsewhere, and shows how important it is that a) Japan breaks the psychological mind-set of stagnant prices (through wages policies? By hiking rates to show the economy has healed?) and b) that western central banks don’t allow deflationary mind-sets to develop here too.

I really enjoyed this article by Tom Standage in the Economist’s spin-off magazine, 1843. The Blanc brothers, bankers in Bordeaux, bribed operators of a system of mechanical telegraph towers to introduce deliberate errors into messages sent over the network which indicated the previous day’s bond market movements. This allowed them to trade bonds before the news arrived through other means, perhaps days later. The scam worked for a couple of years before the brothers were caught. They were prosecuted, but not convicted as “there was no law against misuse of data networks”. Worth a read.

Whilst we are on the subject of technology, everybody’s favourite car manufacturer (stock up around 66% this year so far) made the news during Hurricane Irma with “an unexpected lesson in modern consumer electronics along the way” (Guardian article here). Cheaper models of Tesla cars were remotely given an extra 30 miles of charge through a software upgrade, to help their drivers get safely away from Irma’s path. These cars have exactly the same battery as the more expensive models, but software limits them to 80% of the range.

“Damaged Goods” is a 1996 MIT paper which showed how tech companies may “intentionally damage a portion of their goods to price discriminate”. In some cases companies may add additional technology to, say, a printer in order to slow it down relative to its more expensive offerings, meaning that the cheap version costs more to produce than the expensive one. Tesla’s gesture was obviously a good thing to have done, but it did bring the concept of “Damaged Goods” back into the public gaze.

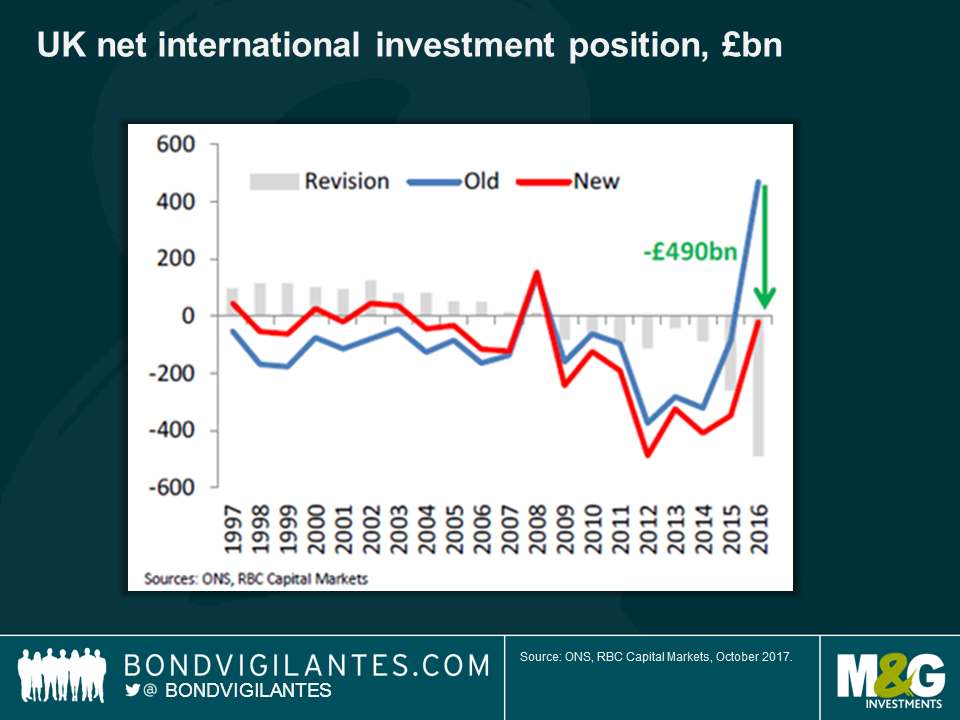

The Daily Telegraph published this article yesterday suggesting that the UK is nearly half a trillion pounds “poorer than previously thought”. Thanks to ONS revisions to the data, a substantial positive position in the UK’s net assets owned overseas has turned into a deficit of £21 billion. In other words the total value of UK investments abroad is worth less than overseas investments in the UK. The chart below, from RBC, shows the extent of this revision, but also that UK investments abroad have jumped in the past year or so. This jump is due to the post-Brexit collapse in the pound making the UK’s overseas assets appear more valuable in sterling terms. As Peter Schaffrik of RBC says “the revision for 2016 doesn’t create a new problem, it serves as a reminder to refocus on an existing one”. As we have a deficit on our international investment position it becomes difficult to generate enough net foreign income to reduce the size of the UK’s large current account deficit. Another sterling depreciation needed?

Art Laffer, the economist who is credited with the idea that cutting taxes would result in higher tax revenues and hence lower government borrowing as stronger economic growth increases the size of the cake is back in the news. Whilst the theory hasn’t necessarily stood the test of time (under Reaganomics debt to GDP increased dramatically as the President cut taxes), the current US President was tweeting approvingly about Laffer yesterday, and Trump wants to see aggressive tax cuts in the US as soon as possible.

Laffer is in the news for another reason, as our colleague Anjulie Rusius discovered in Washington D.C. this weekend at the IMF/World Bank meetings. Bored of Washington, as it’s possible to be after more than an hour or two in the place, she headed to the Smithsonian Museum as she has always wanted to see the famous napkin on which Laffer scribbled his “curve” over dinner back in the day. Literally as she was googling it on her way to the museum, the New York Times ran a story claiming that the Smithsonian’s napkin is a copy, recreated years later. She went anyway (what else is there to do in D.C. once you’ve been to the air and space museum?).

I’m just back from a fascinating research trip to Mexico City, to meet with policymakers, bankers, politicians, analysts, pension funds and regulators. Like many emerging market economies, the Mexican economy has suffered over the past couple of years due to lower commodity prices and weak global demand for goods. Of course, Mexico has had its own unique challenge with Donald Trump’s election and the potential impact that might have on trade and remittances from Mexican migrants to the US.

In this quick primer on the Mexican economy I look at the five areas that I found especially interesting. In particular there could be significant changes to Mexico’s political landscape.

Thanks go to HSBC for organising some extremely interesting meetings.

Just as the UK, US and Europe have seen their electorates support populist parties and policies in the last couple of years, so too has Mexico. The Morena party is just three years old, but with the experienced anti-system left-winger Andres Manuel Lopez Obrador (“AMLO”) as its presidential candidate it could pull off a big shock in the 2018 Presidential election. AMLO has stood in previous presidential elections for the established PRD party, and is well-known to the electorate. AMLO’s campaign focuses on corruption, and in particular on an assertion that the ruling PRI party, which has had an effective 80-year hegemony in Mexican politics, is rotten. In an August poll, AMLO had the highest voting intention percentage of all the potential presidential candidates, and momentum is currently on his side.

Whilst no-one expects AMLO to win control of Congress as well as the Presidency, he would still be well placed to delay planned reforms to the energy and education sectors, halt some private sector-led infrastructure developments (for example the expansion of Mexico City airport), and tighten Mexico’s NAFTA negotiating stance with the US. AMLO may also reintroduce the gasoline subsidies which have only recently been eliminated. Comparisons with Venezuela’s Chaves are unfair though; AMLO was the mayor of the vast City of Mexico region and ran it responsibly. Nevertheless, comparisons will be made, and investors could start to get nervous as the election approaches. One analyst I met was worried about the potential impact of an election loss given AMLO’s belief that elections are rigged against him: “there won’t be a revolution, but…”.

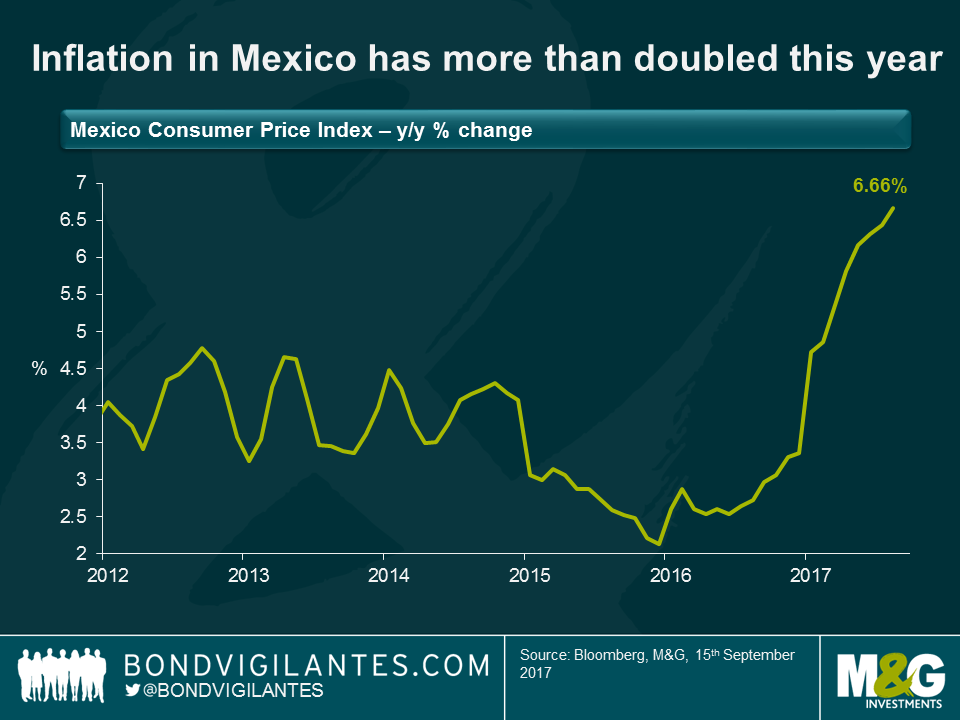

In 2012 the IMF made recommendations that the Mexican inflation and national income statistics needed to be brought up to international standards. Data had traditionally been collected from larger towns and cities, but smaller, rural settlements were not surveyed. As these tend to be poorer areas, the household spending patterns which were used for the inflation component weights had been skewed to the spending patterns of relatively richer Mexicans. This meant that services have had a relatively high weight in CPI.

From July next year the weights in the inflation data will include far more rural communities: as a result the goods weight in the inflation basket rises from 34% to 41%, and within this, food rises from 15% to 21%. The implication for monetary policy, and holders of inflation linked bonds, is that inflation will become even more volatile as food prices are erratic (onion and tomato prices have skyrocketed in Mexico lately), and because goods prices are very sensitive to the level of the Mexican peso. It seems politically impossible for the Bank of Mexico to target only “core” inflation rates – the headline number is everything.

Mexico’s inflation rate has more than doubled this year, to the devilishly high level of 6.66%. Part of this move is as a lagged result of higher import prices following the peso’s depreciation to MXN 22, partly it’s due to those tomatoes (red AND green) and onions, and the rest is explained by the liberalisation of gasoline prices in January (itself adding 1.3% to inflation). The Bank of Mexico’s target is 3%. Whilst breakeven inflation rates derived from linker prices don’t suggest the Bank will quite achieve that target over the medium term, 2018 will see a significant fall in inflation, simply reflecting the base effects of 2017’s price rises falling away, and a stronger peso. Whether this will allow the central bank to cut rates is another question…

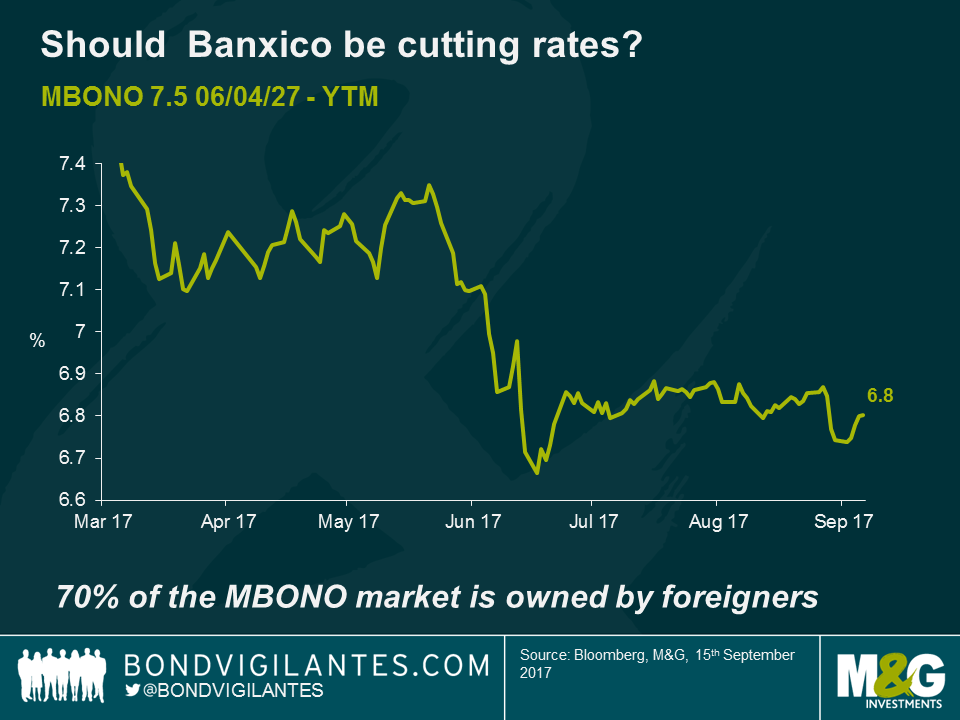

Emerging markets central banks have a different approach to managing monetary policy compared to their developed market counterparts. Whilst both set rates to manage consumer, business and market inflation expectations, the Fed for example will hike rates to influence demand, whilst the Mexican central bank knows that the penetration of variable rate loans, especially amongst consumers, is extremely low and that a rate hike (or cut) will thus have little impact on economic activity.

The transmission mechanism for EM central bankers works disproportionately through the exchange rate. Cutting rates will cause the exchange rate to weaken, which will result in more expensive imported goods prices (and significant second round effects – for example taxi drivers in Mexico put their peso fares up to keep the dollar value of those fares constant, above and beyond what might be the direct rise in imported fuel costs). A rate cut might therefore result in a drag on economic growth, rather than a stimulus. The Bank of Mexico, unlike the Fed, has just one policy target, which is inflation (not inflation and employment, and as mentioned, it is headline inflation, not core). With inflation almost certain to fall sharply in 2018, should the Bank be cutting rates already? And does this make the bond market look cheap (the 10 year MBONO yields 6.75% at the moment)? In theory yes, but the policymakers have two potentially peso-negative shocks to worry about; firstly the aforementioned presidential election volatility, and secondly a possible failure of the NAFTA negotiations. 70% of the MBONO market is owned by foreigners – a huge percentage, and most do not hedge the currency risk. Falls in the peso due to these factors and rate cuts could see the peso retest or exceed the “Trump-fear” lows, and selling could threaten financial stability. So the Bank of Mexico is yet to cut, and may be more cautious than the pure inflation forecast would predict. Perhaps they pay more attention to the level of foreign participation in their asset markets than I previously imagined.

Elsewhere, the Bank is puzzled over the same issues as developed market policy makers – why is there no wage pressure, despite falling unemployment rates? And is their neutral real rate estimate (r*) for Mexico too high at, say, 2.5% if the US’s r* is actually zero rather than an assumption that it’s 1%?

With the Trans-Pacific Partnership (TPP) scrapped by Donald Trump immediately upon taking office, attention now turns to his pledge to renegotiate the NAFTA agreement between the US, Canada and Mexico. Trump has three main areas of contention. Firstly, that the trade deficit that the US runs with Mexico must fall. Secondly, that Mexico should increase workers’ wages towards those in the US. Thirdly, that the “Rules of Origin” must be tightened such that more of the regional content in manufactured goods comes from within the NAFTA area (and preferably from within the US).

All three goals are contentious, and difficult to deliver without damaging the Mexican (and probably the US) economy. The third (of seven) round of NAFTA renegotiation talks begins in October. One trade expert we talked to suggested that the subsequent 4th and 5th rounds later this year would be the most precarious, and that Trump might be minded to withdraw from NAFTA then.

The good news is that most experts suggest that Mexico’s “Plan B” would mitigate much of the damage that NAFTA’s scrapping would cause. It would still trade under WTO’s Most Favoured Nation status with the US, with generally moderate tariffs; it’s possible that those WTO tariffs would not deter trade if a likely peso depreciation made Mexico’s goods cheaper to US dollar buyers; and it is negotiating other trade deals around the world to open up new markets (the EU, Brazil).

It’s difficult to imagine that a Trump tweet in November announcing the end of NAFTA wouldn’t send Mexican assets lower however, at least in the short term.

Historically many emerging market governments have subsidised the price of fuel for their populations, and especially those with ample reserves of oil. It’s a popular policy with voters, and helps to insulate a low income economy from volatility in global energy markets. However, it became very expensive for Mexico when oil prices were $100 per barrel a few years ago while its “cash cow”, the Cantarell Oil Field (named after the fisherman who discovered it), saw production collapse (from 2.1 million barrels per day to 400,000) causing its gasoline imports to increase.

In recent years then, government policy has been to liberalise gasoline prices, and allow them to move higher towards market levels. As we saw, this has been a big upwards influence on Mexican inflation, especially in January 2017.

Additionally, the government is trying to reduce the influence that the state owned oil giant Pemex has on the nation’s energy supply. Over the years Pemex has provided revenues to finance a huge chunk of Mexico’s fiscal needs, but by prioritising crude oil production at all costs, it neglected investing in maintenance (resulting in unplanned shutdowns 10 times higher than the industry standard), refining capability (resulting in Mexico importing gasoline from the US), and a nation where 40% of towns have no petrol station. In the US there’s one gas station per 2500 people, in Brazil it’s 1 per 5000, in Mexico 1 per 10000.

So on top of a move to end gasoline subsidies, Mexico is now open to competition all across the supply chain. Companies can bid for exploration blocks in the Gulf of Mexico, to build new pipelines, to import fuel by truck from the US, and to run and build gas stations. More competition should result in lower prices for consumers, higher efficiencies in the oil supply chain, and an end to the drag on Mexico’s growth rate that the energy sector has delivered in recent years.

I ate one of these. I’d like to say it tasted of chicken, but it tasted of worm.

Further reading

Claudia wrote about Trump and Latin American remittances here: https://bondvigilantes.com/blog/2021/12/14/the-central-american-remittance-crunch-who-would-lose-most-from-a-trump-presidency/

Charles wrote about NAFTA here: https://bondvigilantes.com/blog/2021/12/26/research-trip-mexico-trump-key-call-emerging-markets/

I’m now more than three quarters of the way through my attempt to climb 100 iconic hills, bergs, kops and mountains on my bike in 2017. It’s been amazing fun so far, and I’ve ridden a huge variety of different types of hill and mountain with some great people. The hardest? Well it took me six tries to get up Bristol’s Vale Street, the steepest residential road in the UK – but I was on a station hire bike and my leather shoes kept slipping off the pedals. I guess Corkscrew Hill outside Manchester should also qualify. Wet and roughly cobbled, none of our group made it more than a couple of metres up the 45 degree slope before falling off. It is not included in the honour roll below. As a region, I found that the hills of the Lake District were both consistently brutal, and the most beautiful I’ve ever seen. I can’t believe I made it to my mid 40s without ever properly visiting this area of the UK – go!

By now you probably know why I’m doing these climbs. Unbelievably, after only six months, Cascaid has already raised over £1.37 million for Cancer Research UK (CRUK), and has doubled its target to £2 million for 2017. This now seems very achievable. You can read about some of these efforts and the work of CASCAID and Cancer Research UK on the link below. I’m especially blown away by former M&G marketing guru Anne-Marie McConnon and team’s effort to row the Irish Sea from Wales to Dublin, which they did in heavy seas a couple of weeks ago. That’s the good news. The bad news is that even £2 million doesn’t go far – research is incredibly expensive. But survival rates from cancer have doubled from the 1970s, and Cancer Research UK is targeting a 75% survival rate by 2034, in particular by trying to improve the chances of those with pancreatic and lung cancer where the outlook is currently poor. Just two weeks ago CRUK announced the results of a large scale trial in prostate cancer, which showed a 37% improvement in survival rates. The money that you have kindly donated so far will make a difference.

http://www.cascaidcharity.com/

Cascaid’s fundraising page is now the most successful ever on the Virgin Giving platform, earning a “thumbs up” from Richard Branson himself last week. My fundraising page is linked below. Many thanks to all of you who have already donated.

I promised that if I raised an extra £500 then I’d shave my legs. You donated, and I am now silky smooth. I thought it might help me to a PB on Dark Hill in Richmond Park this weekend, but it turns out the aero impact is not as significant as I had hoped. Silky though.

A few thank yous. So as a reminder, I’m cycling up famous climbs featured mainly in Simon Warren’s excellent series of books called things like “100 Greatest Cycling Climbs” and “Another 100 Greatest Cycling Climbs”. Simon has very kindly helped me to plan some routes. The books are ace, buy them! Thanks to everybody who has ridden with me so far this year – I’ll do a full rollcall when I’m finished, but the company has been invaluable. Thanks also to Will Masi at Nuffield gym, and Athlete Lab at Monument for getting me in a state to get up the hills. Finally thanks to my family for support car services, and for tolerating me disappearing for a morning or two when on holiday. I promise it was coincidence that our trip to Bruges took place at the same time as Paris-Roubaix.

You’ll find the evidence of climbs on my Strava feed.

Here’s the list of all the climbs that I’ve done so far:

What’s next? Kent and East Sussex still have a few hills left for me, but before I finish I want to get up to the Derbyshire Peak District, I want to ride up a hill in Calverton which I could never get up on my Raleigh Grifter as a schoolboy in Nottinghamshire, and I think I should tick off some of the Yorkshire hills that featured in the Tour de France a couple of years ago. Thanks for all of your support. Here’s a picture of The Struggle near Windermere. An awful hill.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.