A new source of supply in the ABS market

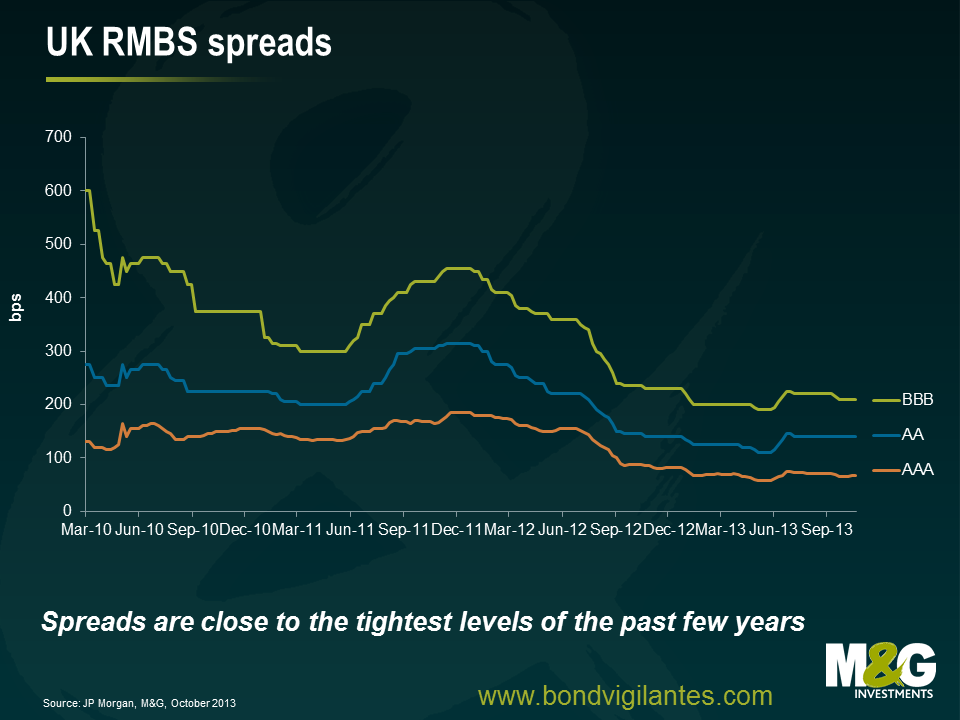

One of the features of the ABS market this year has been the lower levels of primary issuance. That, coupled with increased comfort in the asset class and higher risk/yield appetite has caused spreads to tighten.

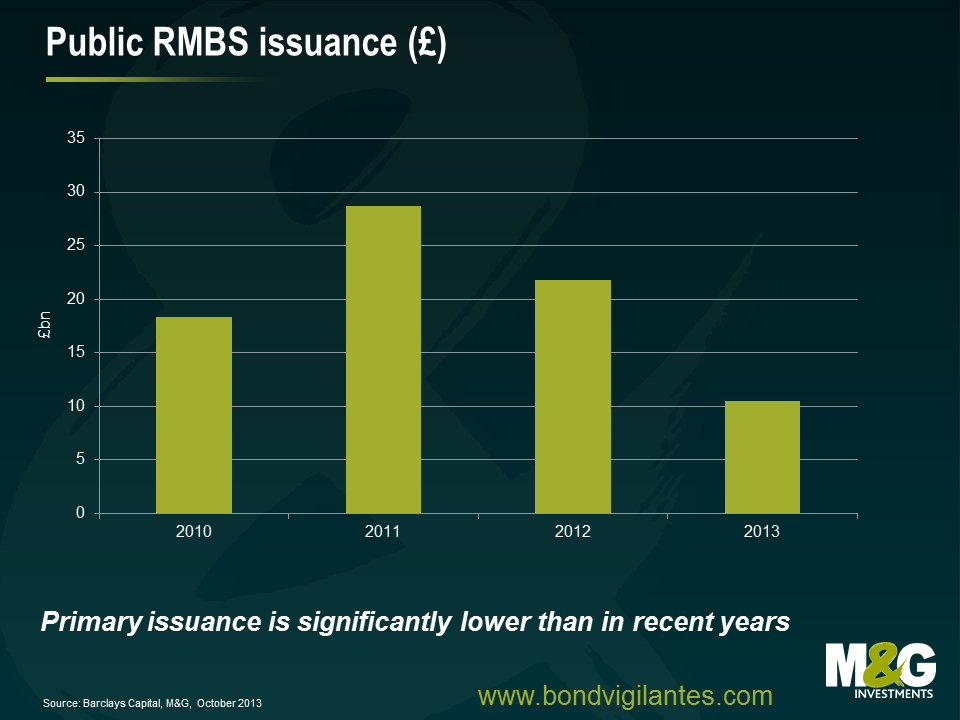

We have had a few new deals, but 10 months in and new issuance volume is only about half the amount seen in 2012, and just a third of 2011 issuance.

What we’ve seen of late, despite the subdued new issuance, is an increase in the number of these securities available in the market. In the not-so-distant past, banks would structure a securitised deal, place some with the market and keep some to pledge to their central bank as collateral for cheap cash.

Now spreads have tightened, and the market feels healthier, some of these issuers are taking the opportunity to wean themselves off the emergency central bank liquidity and are offering the previously retained securities to the public market.

Another dynamic in ABS at the moment is that ratings agency Standard and Poor’s is considering changing its rating methodology for structured securities in the periphery. S&P is considering tightening the six notch universal ratings cap – countries rated AA or above will not be affected, but bonds issued from countries with a rating below AA could be downgraded as they won’t be allowed to be rated as many notches above their sovereign as they were before.

The implication is that securities that get downgraded will become less attractive for banks to pledge as collateral because of the haircuts central banks apply to more risky (lower rated) securities. Our thinking is that southern European issuers will be hit hardest by this change. So unless the ECB loosens its collateral criteria (which it can and has done previously), one would expect to see more of those previously retained deals coming to the market as well.

So whilst we haven’t seen too much in the way of new issuance, it looks like we could be about to see an increasing number of opportunities in the secondary market.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

17 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox