The M&G YouGov Inflation Expectations Survey – Q2 2014

Today we are launching the next wave of the M&G YouGov Inflation Expectations Survey which aims to assess consumer expectations of inflation over the short and medium term.

With interest rates at multi century lows, central banks continue to inject large amounts of monetary stimulus into the global economy. Recent inflation rates in the US, UK and Germany have proved central to the current market focus, as actions from policymakers have become increasingly sensitive to inflation trends. This is true for the Fed and the BoE, as markets assess their possible exit strategies/timing, but especially for the ECB, whose last round of action is perceived to have been largely motivated by disinflationary pressures in the Euro area. In that context, market focus on inflation expectations has increased.

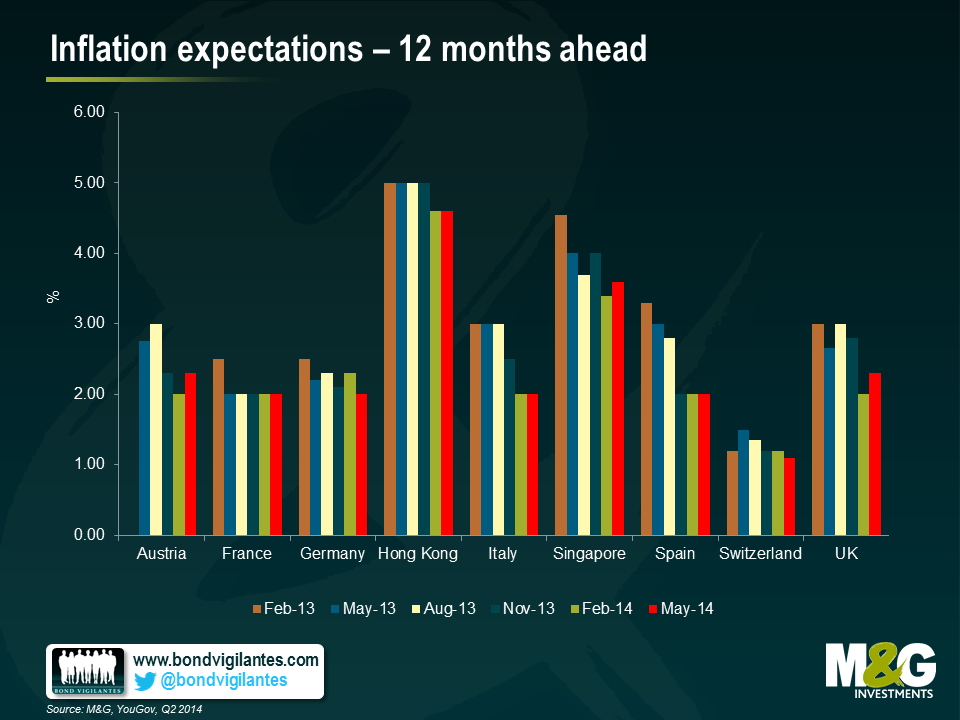

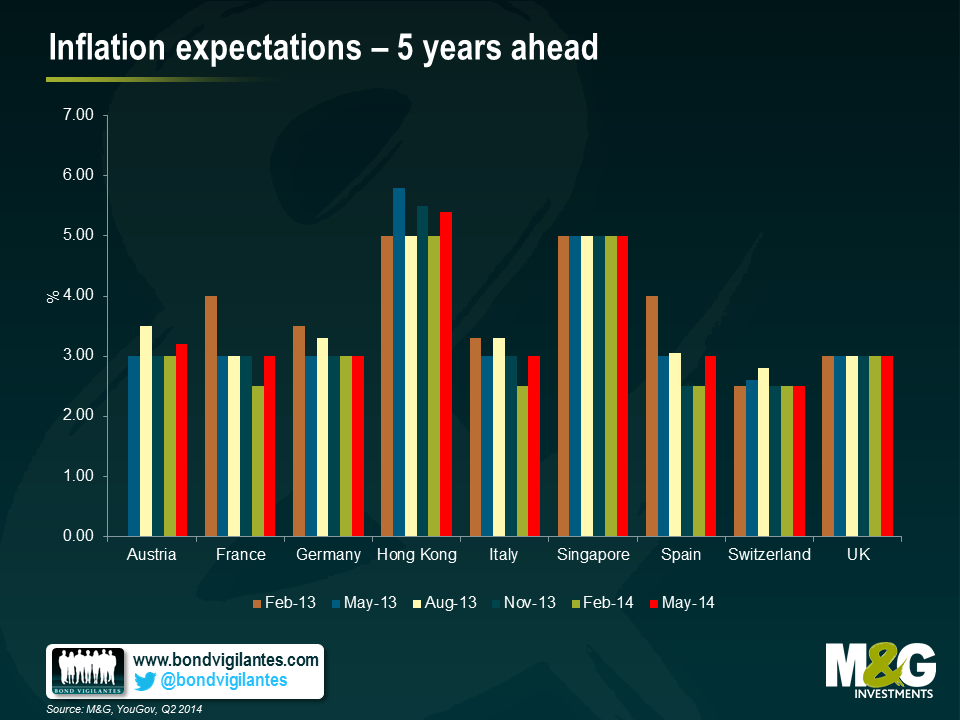

The results of the May 2014 M&G YouGov Inflation Expectations Survey suggest that both short and medium-term inflation expectations remain well anchored across most European countries.

Short-term expectations have risen from 2% to 2.3% in the UK as the country showed further signs of economic growth and reaccelerating wage pressure. On the other hand, inflation expectations for German consumers moderated in the last quarter as the downward trend in German HICP (1.1% YoY in April) may have added to the expectation that German inflation will remain subdued over the next year.

The general downward trend in short-term inflation expectations seems to have largely receded in all EMU countries and the UK. This may be somewhat surprising with much of Europe still experiencing low and falling inflation.

Over the medium term, inflation expectations remain above central bank targets in all countries surveyed, suggesting that consumers may lack confidence in policymakers’ effectiveness in achieving price stability. Over 5 years, UK inflation is expected to remain well anchored at a remarkably stable 3%. Despite recent low inflation rates across Europe, the majority of consumers in France, Italy and Spain continue to view inflation as a concern, and long-term expectations in those countries has risen back to 3%.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

17 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox