We are there – nothing to fear

The Bank of England’s Monetary Policy Committee (MPC) are due to meet on Thursday and most economists expect a dovish set of minutes to accompany the announcement of no change in the BoE base rate. Additionally, the minutes will likely emphasise the risks of a persistent undershoot in UK inflation given the continued fall in commodity prices and waning global demand. Despite these risks, the MPC are also likely to indicate that the first interest rate hike remains on the horizon. The decision to eventually hike interest rates will not be taken lightly, and the MPC will be having a long think about the potential labour market impact when a rate hike eventually occurs.

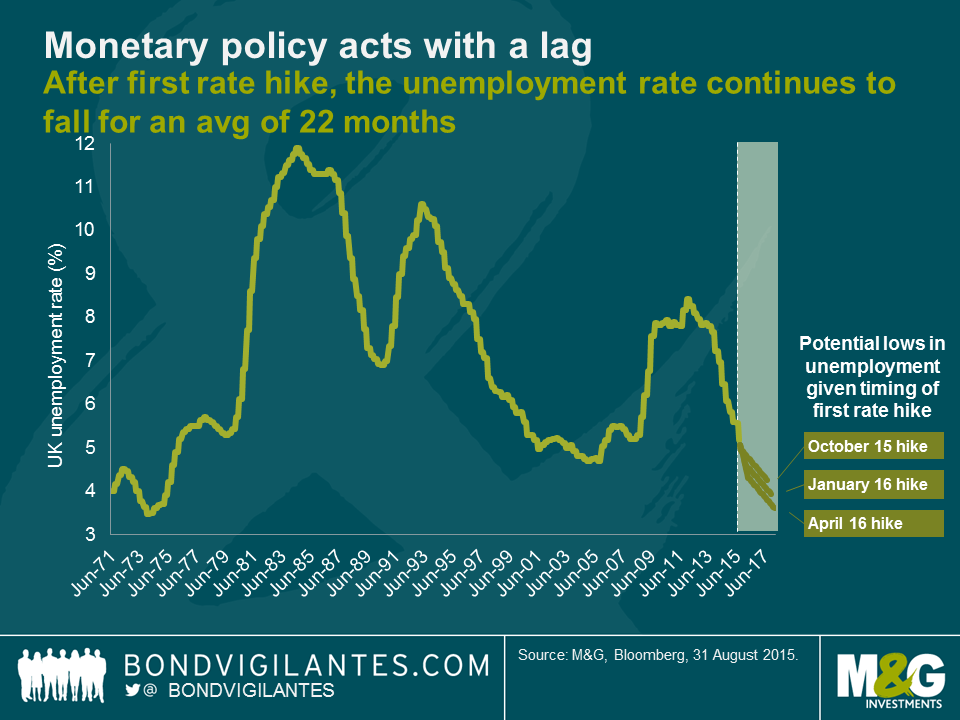

Monetary policy works with a lag; the BoE estimates this to be approximately two years in the UK. The relationship between rate hiking cycles and unemployment figures has therefore historically taken time to fully feed through the economy.

Since 1971, the BoE have undertaken six separate rate hiking cycles in the UK. After the initial rate increase in each of these, unemployment has continued to fall on average for the next 22 months, which is just shy of the BoE estimation of a 24 month lag. Given that the UK unemployment rate has been on a downward trajectory since mid-2012, history suggests that even if the MPC hikes rates, it will likely fall significantly further from the current level of 5.2%.

Indeed, if the BoE rate hiking cycle were to commence in October of this year, the graph above forecasts that the corresponding unemployment rate could potentially bottom out at 4.25% in August 2017. Building on this idea, if we extrapolate the current downward trajectory in unemployment and assume a later rate hiking cycle starting in April 2016, this predicts an unemployment rate trough as low as 3.61% by February 2018. Unless the BoE acts soon, the anticipated fall in UK unemployment from current levels could potentially return us to the multi-decade low unemployment rates last seen in the inflationary early 1970’s.

The trauma the BoE experienced during the recession was typified by Sir Mervyn King’s comments which I wrote about in 2012, when he said that we were not yet half way through the crisis. Sir Mervyn suggested that rates would stay at 0.5% until the end of 2015. Well, we are now approaching the end of that time frame window and the BoE has only fear itself as to when to take the economic action to slow a potential inflation problem. The current members of the MPC should take inspiration from the appropriately titled Lily Allen song “The Fear” which was the UK no.1 single the last time the committee moved rates in March 2009:

“And when do you think it will all become clear?

‘Cause I’m being taken over by the fear”

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

17 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox