China Renminbi: the USD $50,000 question

Last week, in line with expectations, China announced the renewal of the $50,000 limit of dollar purchases by individuals. What’s changed however is that the foreign exchange commission (SAFE) has tightened the scrutiny on the foreign exchange purchases. Applicants are now required to detail the purpose behind their transactions in order to ensure that the purchase is for “suitable purposes” (e.g. overseas studies, outbound tourism, business abroad, overseas medical treatment, the purchase of non-investment insurance and consulting services), adding a new layer of bureaucracy, in an attempt to reduce the purchases.

I was in Hong Kong on a business trip last year, opining on China’s regime and capital controls with an analyst. During our discussion I touched upon my blog where I put the capital outflows into perspective by calculating the appropriate level of international reserves by looking at a common metric, the Assessing Reserve Adequacy ratio (ARA), which measures reserves versus debt levels, monetary aggregates and trade. This time around, I’m making things simpler by answering a straightforward question:

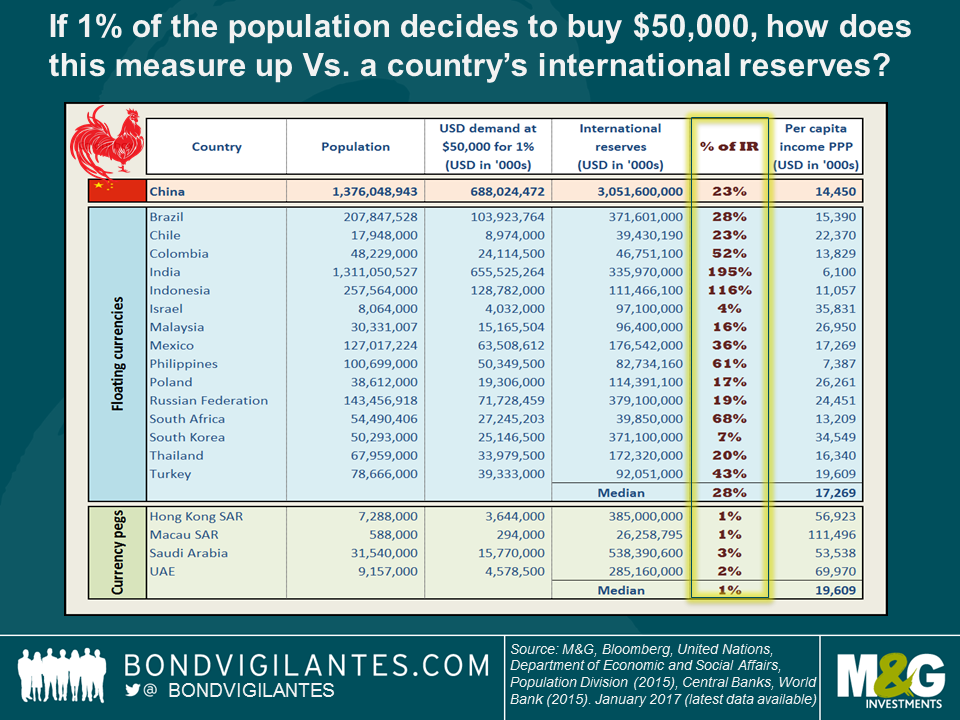

If 1% of the population decides to buy $50,000, how does this measure up versus a country’s actual international reserves?

At first glance, China’s potential retail USD demand, at 23% of foreign exchange reserves, is not too far off the 28% median result. However, the countries are not homogeneous. Indeed, most countries with a floating currency regime have an open capital account. It’s also important to note that the exercise includes countries with large current account surpluses, such as Korea and Israel, which have in the past accumulated large amounts of reserves through past interventions to prevent further currency appreciation[i]. Finally, countries such as India have a large population but low per capita income (see final column in the table). Therefore although we do not have details on the per capita income skew beyond Gini coefficients (so it is difficult to estimate how easy it is for 1% of Indian citizens to tap into $50,000 worth of savings), in all likelihood, it will be more difficult to do so than, say, the Indonesians.

Countries with a fixed exchange regime and an open capital account need to have much higher reserve buffers, which is precisely what the table indicates, with this measure coming in much lower at 1-3.

China finds itself somewhere in the middle. It does not have a free floating regime and the capital account restrictions remain significant. Corporate debt levels are very high, so tightening monetary policy aggressively to make Renminbi assets more attractive is not an easy option. With a high level of household savings (there is no household savings data for all countries, so I omitted this relevant fact in my calculations, but China potentially has the highest household savings of the countries listed), the pent-up USD demand will linger as long as there is the perception that inflow and outflow of dollars remain imbalanced. On a cheerier note, the gradual changes to China’s currency regime are moving in the right direction, towards a more flexible arrangement[ii]. But based on the crude metrics above, a free floating currency with full capital mobility is still a long-term prospect.

The Chinese new year is fast approaching and we will soon be celebrating the year of the Rooster, let’s hope that the tighter capital controls calm things down so that the chickens do not come home to roost.

[i] Should Mr Trump decide to label a country as a currency manipulator, the US Treasury should be targeting countries like Korea, not China. Korea remains on the US Treasury monitoring list. See here for more details on the monitoring criteria.

[ii] PBoC just announced a reweighting of its CFETS currency basket index to include 11 additional currencies, namely the KRW and a few other EM currencies, which will help to reduce the CNY broad appreciation should USD strength continue or should, for example, Korea be labelled a currency manipulator by the US Treasury.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

17 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox