Never a dull moment – trying to make sense of last week

Political turmoil in Italy and Spain, escalating trade tensions and, for good measure, unexpectedly strong US employment data – to say that markets had a turbulent few days would be an understatement. Taking a step back, here are three lessons I took away from last week.

(1) Market sentiment shifts can be brutal

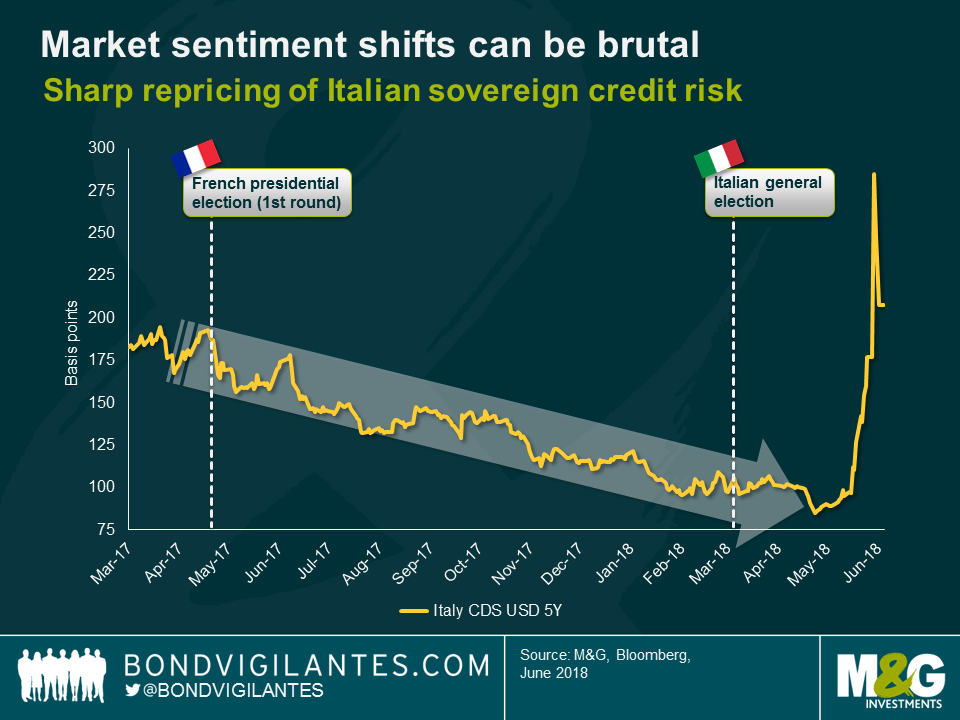

Political risks in the European periphery are real – a statement that might sound trivial now, but let’s not forget how much optimism there had been until very recently. After the first round of the French presidential elections in late April last year, Italy’s 5-year credit default swap (CDS) levels had moved essentially only in one direction (from close to 200 bps to around 100 bps), indicating that the market perceived Italian sovereign credit risk to have subsided substantially. Even the uncertainty created by the result of the Italian general election in early March this year didn’t change the constructive market sentiment. In fact, in late April and early May when credit spreads of corporate bonds were already drifting wider, Italian CDS contracts kept rallying to around 85 bps.

Only when the 5-Star/Lega coalition took shape and anti-Euro rhetoric dialled up, market sentiment made a sharp U-turn and switched into ‘risk off’ mode, pushing Italian CDS levels to around 290 bps. To put this into context, based on CDS levels, mid last week the market assigned higher sovereign credit risk to Italy than many emerging market countries, such as Turkey and Brazil, demonstrating just how violent market moves can be when sentiment changes abruptly.

For active investors these episodes of heightened volatility can present interesting opportunities though. The bearish tone last week quickly spread from Italian assets to other parts of the market due to indiscriminate shunning of risk. European financials and higher-beta securities, such as corporate hybrids, came under pressure, presenting appealing entry points to add exposure.

(2) Return correlations matter

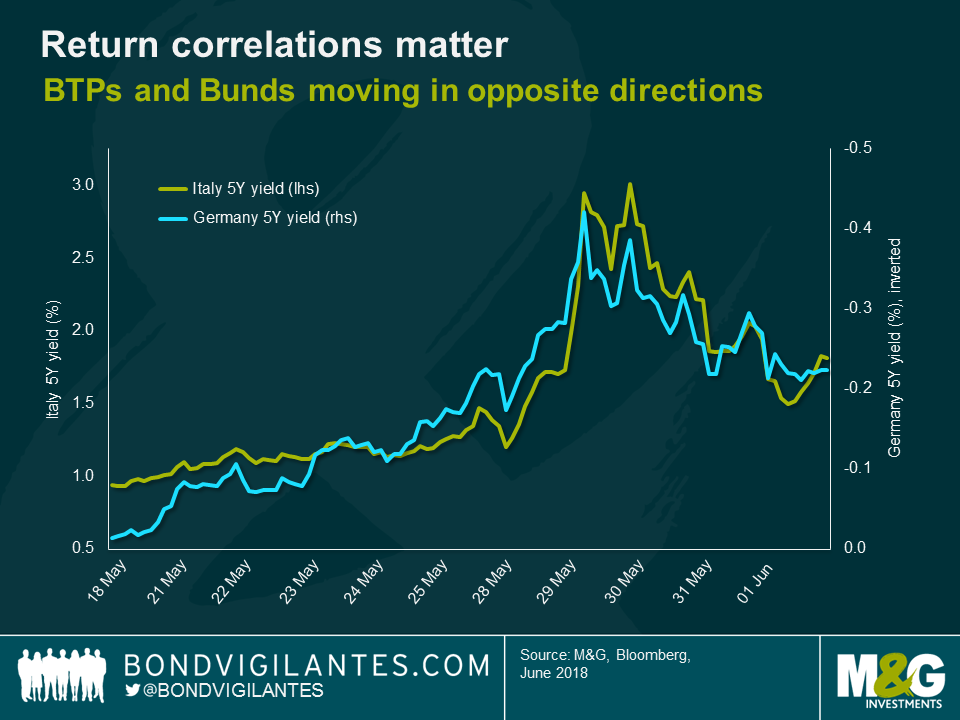

The last couple of days have been a textbook example of asset class return correlations at work. Most noticeably, Italian government bonds (BTPs) and German Bunds have behaved pretty much like polar opposites. When Italian BTP yields soared last week, driven by fears of new elections and further gains for anti-Euro Lega, German Bunds lived up to their ‘safe haven’ image. Their yields plummeted, benefitting from the market’s ‘flight to quality’ impulse. Subsequently, when the Italian government finally formed, the BTP relief rally was met by rising Bund yields.

For any investor concerned about portfolio volatility and drawdowns, these correlation patterns matter. As unattractive as Bunds – and other core government bonds for that matter – may look from an outright yield perspective, they can be valuable portfolio stabilisers in times of violent ‘risk off’ market moves.

Against the backdrop of continued robust (enough) economic fundamentals and corporate default rates close to zero, I still see value in risk assets such as investment grade credit. However, considering that political risk in the European periphery is likely to remain elevated with the potential for further escalation of global trade tensions, it doesn’t strike me as unreasonable to maintain some exposure to Bunds and other safe haven assets such as the Japanese Yen, for diversification purposes.

(3) Other topics are overlooked

When specific topics dominate conversations and market sentiment, it is very easy to be sucked into the relentless news flow. Every minute detail suddenly seems relevant and has the potential to move markets in either direction. In some sense, the recent fixation of the market on Italian politics gave me flashbacks of February 2016, when falling oil prices had been a similarly omnipresent and market-moving topic.

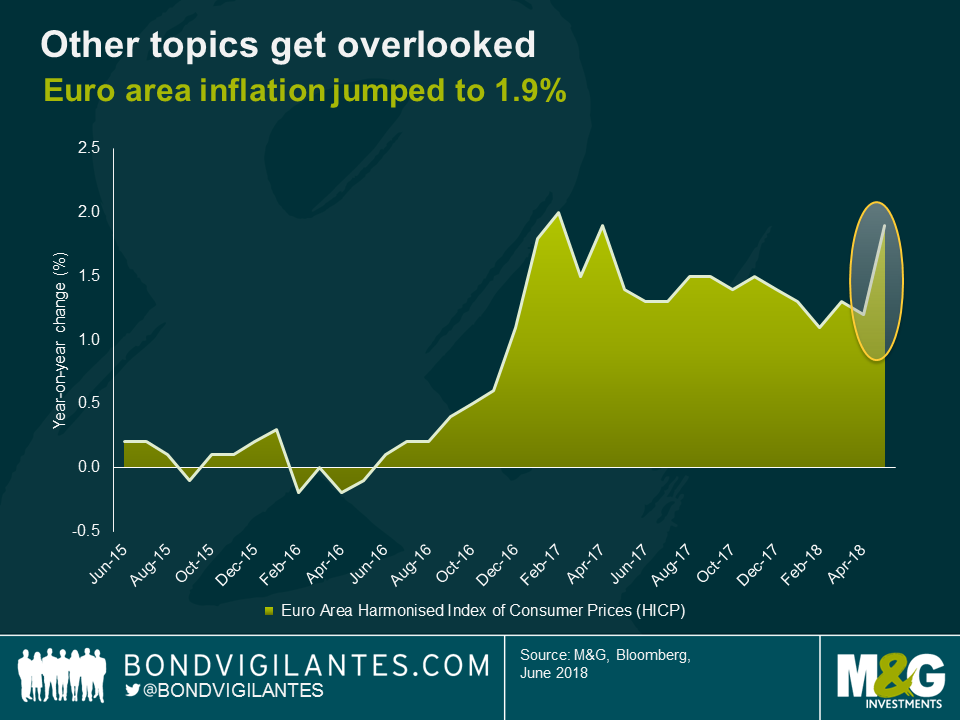

However, when preoccupied with a certain subject matter, the obvious risk is that other potentially significant developments might be overlooked. For instance, the release of the latest Euro area inflation data last Thursday barely made headlines, despite the big jump from 1.2% to 1.9% per year. Admittedly, surging energy prices and other transitory effects were the main drivers, while annual core inflation remained subdued at 1.1%. Nonetheless, an inflation print that perfectly meets the ECB’s price stability target of below, but close to 2% should at least raise a few eyebrows, considering the uncertainty around the future path of the ECB’s monetary policy stance.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

17 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox