Emerging markets outlook: seven themes for 2021

Markets ended 2020 in a buoyant mood, with emerging market spreads tightening in the final quarter as the US election result and positive vaccine news provided a boost to investor sentiment. While nobody has been blind to the global recession, focus has shifted to expectations of an economic recovery.

Most people were happy to see the back of 2020. It was an eventful and challenging year, but one with plenty to distil, look back on and learn from. The year ahead is likely to be less ‘unprecedented’ – a frequently used phrase over the past 12 months. The new year looks like it could offer good opportunities for investors. Here are seven themes that we think will impact emerging market fixed income in 2021.

Theme 1: Virus and vaccines – a multi-speed economic recovery

The draconian but necessary pandemic response of authorities everywhere sent the global economy into recession in March and April. As the extent of the COVID-19 infection rate varied markedly between countries, so too did the economic fallout and resultant recoveries.

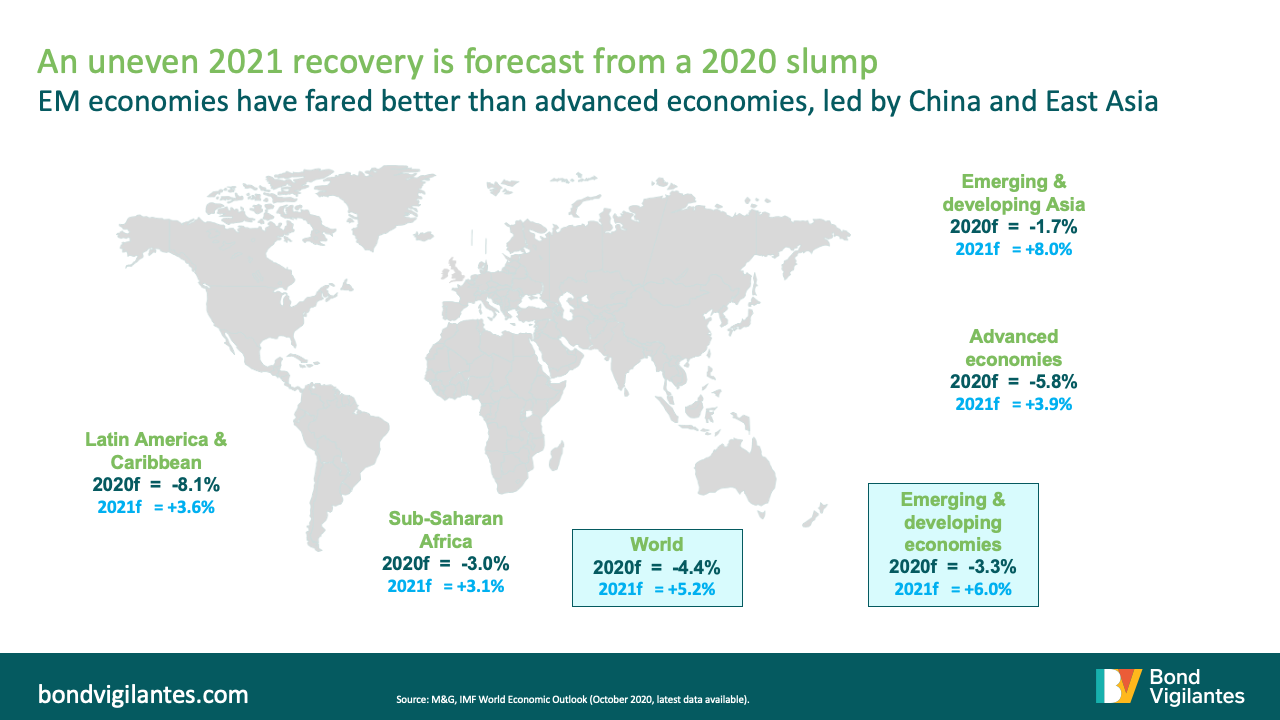

The East Asian economies, especially China, were more resilient in 2020, especially relative to Europe and the US. While world output tumbled over the course of the year, China’s grew. This provided a boost to emerging economies, which contracted less than advanced economies. The projections for a 2021 recovery also favour emerging markets over the advanced economies, as the recent growth forecasts from the IMF indicate (see chart below).

Projections for 2021 assume any further waves of the pandemic are either avoided or reduced by the vaccine rollouts. Clearly, some uncertainty over the path of the virus remains, and caution will be needed in many countries when considering what levels of stimulus or supportive policies are needed to nurture the recovery. A sudden withdrawal of stimulus or a hasty return to policy normalisation could kill off a recovery.

Theme 2: Effervescent stimulus and low global interest rates

Highly accommodative monetary policy from the large developed economies pulled markets back from the brink in March 2020. Once some of the dust had settled, a cross-market recovery eventually fed into demand for emerging market bonds. From May 2020, low interest rates and improved investor sentiment led to a search for yield that pushed the spreads of emerging market bonds back towards the levels they started the year at.

A lot of 2021 positivity is grounded in the view that global interest rates will stay lower for longer. Also, that the accommodative polices of central banks will continue, in tandem with further fiscal stimulus. Such an environment creates a positive backdrop for emerging markets. But market sentiment would be tested in 2021 if there were signs that bubbling stimulus was fading.

Theme 3: High-yield emerging market bonds to lag less

Investment grade emerging market bond spreads tightened from their highs in March and April 2020, swiftly back towards where they were pre-pandemic. While high-yield emerging market bonds benefited from a recovery in May, their spreads remained wide of where they started the year (see chart below). Performance lagged the investment grade space due to uncertainty about any delayed impact the virus may have on frontier economies. It was difficult to accurately assess the implications for debt sustainability for much of the year.

So throughout 2020, high-yield emerging market bond spreads remained elevated. The result of the US election and positivity over vaccine success helped narrow the gap with an and end-of-year rally, but frontier names still lagged as the year came to a close. In 2021, we believe high-yield emerging market bonds are likely to lag less and perform better than they did in 2020. But country and credit selection is going to be crucial as most countries face increased debt loads.

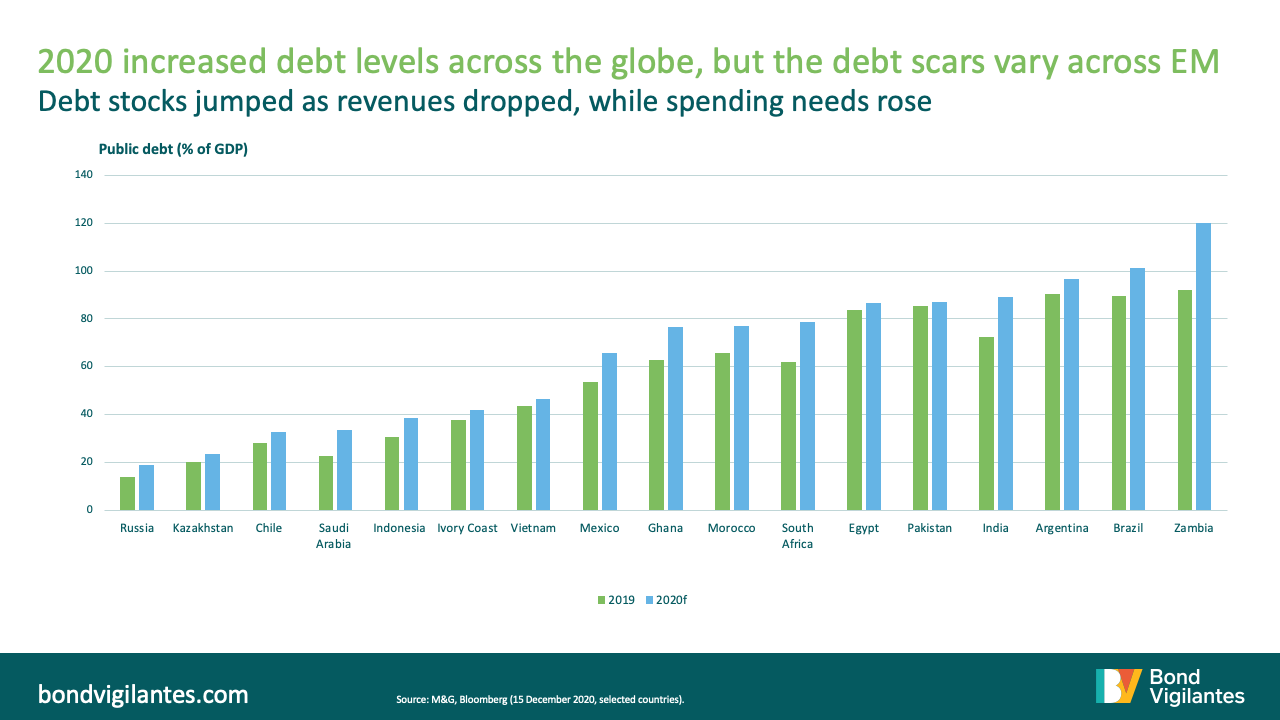

Theme 4: Deep debt scars

There was a global splurge in government borrowing in 2020 and emerging markets were not left out, although much of the borrowing took place domestically and in local currencies.

This differed from a textbook emerging market crisis, as governments were able to cut interest rates and borrow more cheaply. Many emerging markets, some even approaching the zero-bound in terms of rates, enlarged their central banks’ remits and embarked on quantitative easing-type policies to safeguard liquidity in their markets, or for outright financing for pandemic-related spending. Where frontier countries had higher inflation, or could not access all the needed finance at home, increased emergency lending was at hand. The IMF and other international financial institutions provided hard currency loans for countries on request. This financing source came without many of the usual list of policy conditions, as the focus became the rapid deployment of funds.

Towards the end of the year, it became possible to identify where the debt scars were most pronounced. Six sovereign nations saw a ratings downgrade in 2020, including several countries that had already faced severe solvency risks during 2019 (Argentina, Lebanon, and Zambia) and several countries whose economies were hit particularly hard by the pandemic (Ecuador, Belize and Suriname). The key question on investors’ minds is whether others might follow in 2021.

While debt risks have risen (see chart below), they do not indicate an imminent systemic emerging market debt crisis, in our opinion. The risks vary considerably by country. For example, both Brazil and Mexico had large budget deficits in 2020, but the debt pressures are very different. Brazil is expected to stabilise its public debt at around 103% of GDP while Mexico can do so at 65%.

The larger emerging markets have borrowed mainly in domestic markets, often with foreign flows, suggesting a currency crisis or the need to generate some inflation is more likely than an Argentina-style external debt default. But for the mostly frontier countries that have borrowed heavily externally, the foreign currency risks remain. For an investment portfolio, this is where country selection is key, as there is huge variance between countries. Some have lower risks, market access and can quickly shrug off liquidity concerns during a recovery, while solvency problems are likely to emerge for others.

Theme 5: A slightly softer US dollar

Emerging market bonds suffered from large outflows in March 2020, but financing flows recovered and ended the year in positive territory. However, the pace of local bond fund flows was slow initially and only began to pick up with any conviction as clearer forecasts for the US election result emerged. This trend was further boosted by the positive vaccine news. Better economic data in the third quarter and investor positioning helped even some of the hardest-hit emerging market currencies recover in the fourth quarter. Emerging markets currencies bore much of the adjustment brunt early in the crisis, but tended to recover over the course of the year (see chart below).

Despite the pandemic, 2020 saw record foreign inflows to China’s local bonds following its global bond index inclusion. We believe this trend is set to continue and is likely to create new investor demand that is diverted from developed markets, as opposed to redirecting flows from other emerging markets.

Our expectations are for a continued softening of the US dollar in 2021. We think this would give emerging market currencies a boost and be supportive of returns for emerging market local debt. However, any unexpected weakening in the global economy would see a moderation of investor interest.

Theme 6: Oil and OPEC agreements

Russia, the Gulf states and other emerging market oil exporters have experienced a lot of uncertainty and volatility in their economies as oil prices have swung from an early-year peak of close to US$69 per barrel to a low of around US$20 per barrel. The recovery in economic activity, plus sufficient unity among OPEC and OPEC+ members to honour planned production cuts, helped oil settle back close in on US$50 per barrel. Budget plans for 2020 had to be torn up and recast as pandemic spending needs rose while oil revenues slumped.

The oil price outlook remains uncertain for 2021. We believe the speed of the global recovery, tensions between the West and Iran, and success in maintaining OPEC+ harmony will all factor into it.

For oil exporters without large financial buffers, near-term reforms will be vital to restoring the sustainability of public finances. Many have never adjusted fully to an oil price below US$100 per barrel or made progress with diversification plans for their economies. This list includes Oman and Bahrain, Nigeria, Gabon and Angola.

For the Gulf countries with large financial asset bases, the choice has been to borrow rather than watch assets dwindle too fast. Here, reform and diversification is equally important, but not on such a pressing timetable. Since their inclusion, Gulf states have risen quickly among issuers in terms of size and now represent a large and growing portion of emerging market bond indices. Given current issuance plans, this trend looks set to continue in 2021.

Theme 7: Geopolitics hotspots unlikely to cool down

While a shift away from Trump-era US foreign policy is expected, the global political landscape has changed and we are not likely to return to policy that was familiar under the Obama presidency. However, a more expert-informed policy framework is expected, rather than knee-jerk reactions and late night Twitter posts. Nations such as Saudi Arabia, Turkey and Russia might find the going tougher, while Mexico and multi-lateralism could receive a boost. While foreign policy changes are likely in 2021, some will take time to develop and will feature later into Biden’s term, in our view.

Geopolitics looks set to play a big part in emerging markets, with some headwinds affecting the asset class, while some crosswinds may require a regional or country specific approach. US-China relations look set to remain a core theme and tensions are unlikely to cool as China grows and threatens America’s global hegemony. Meanwhile, Middle-eastern politics will need monitoring, alongside elections, including in Peru, Chile and Ecuador.

Outlook

We are looking forward to what 2021 will bring, after a tough and unpredictable 2020. Given that three quarters of developed market bonds are trading at negative yields once adjusted for inflation, there is added impetus for investing in emerging market bonds.

While there is some argument that the emerging market investment grade bond segment is now starting to look less attractive on valuation grounds, we believe spreads in the high yield bond segment remain at attractive levels and some emerging market currencies remain undervalued.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

17 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox