The fiscal cliff is bad news, but is likely to be resolved – so don’t ignore the extremely positive developments in the US housing market

There are some big risks to the US economy, but the potential for the US housing market to surprise on the upside, and deliver massive gains to US employment might well be the bigger story for 2013.

The real damage that the fiscal cliff is causing is mainly psychological at the moment, discouraging both capital investment and hiring. I’m not allowed to use the phrase that involves metal food containers being moved further along transport routes by means of the foot, as we have a “cliché box” at work, and saying it would cost me dearly – but that is both the obvious solution to the problem, and indeed the only solution. The size of the US debt is now too big for any politician to deal with decisively, and some sort of default (against bond holders if a default against the population’s pension or healthcare expectations isn’t possible) or devaluation (currency or inflation) sometime in the future will be likely.

The focus on the fiscal cliff has taken attention away from what we think are extremely positive developments elsewhere in the US economy – and particularly in the housing market, as alluded to in September. US housing became the centre of the global financial crisis from 2007 onwards, when the credit bubble burst as sub-prime mortgage loans started to go bad. Too many houses had been built, and the overhang of unsold inventory together with foreclosures and falling real incomes and unemployment led to a sharp fall in house prices. The banking system went bust, and a huge number of construction jobs were lost in the economy. From a peak of 7.7 million Americans employed in construction in 2006, by the start of 2010 the sector had lost 2.2 million jobs. But we’re now seeing a large number of positive signs in the US housing market, and just as the negative multiplier effects spread through the economy when the sector tanked, the reverse might be true next year.

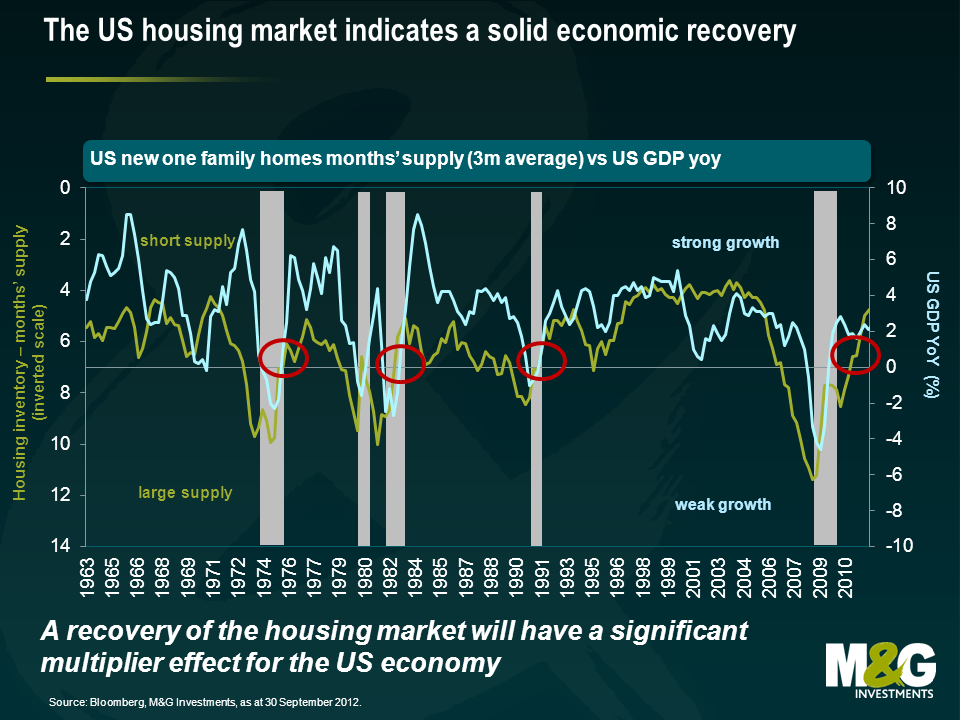

The chart below was very important to us in 2007, when it led us to expect not just weak growth in the US, but an outright recession with huge damage to the banking sector. It showed that there had been so much overbuilding in US residential property that the supply of inventory had moved from about 4 months to over 7 months. This had historically been a leading indicator of recession. In fact unsold inventory moved much further than 7 months, hitting 1 year in 2008, presaging US GDP falling by 4% year on year. You can see that the available inventory of housing is now contracting sharply, to the extent that US growth should continue positive. It’s also at a level where house-building should resume – and the multiplier effect from that will be extremely powerful.

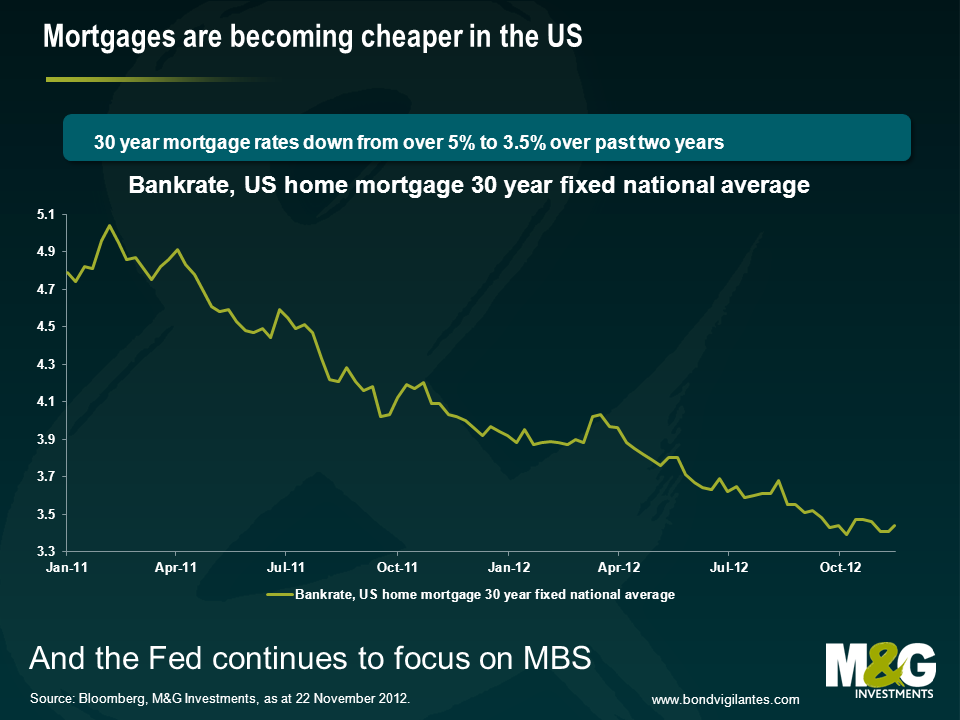

Other reasons to be cheerful about US housing? Well house prices have been rising, according to the S&P/Case-Shiller index, since March this year (but remain “cheap”, 30% below the peak in nominal terms, even weaker in real terms). So the negative sentiment around the sector will be fading somewhat – nobody wants to buy into a falling market. And the Federal Reserve has almost entirely moved its Quantitative Easing programme away from purchases of US Treasuries and towards the purchase of Mortgage Backed bonds. This should eventually help get the transmission mechanism working again. In theory American mortgage investors should be able to refinance existing mortgages at high rates into new lower rate loans. This hasn’t been happening – banks have dragged their heels on paperwork (the time from agreeing a loan to it closing has anecdotally risen from a month to three months for example), and lending standards for the new mortgages are often higher than they were for the outstanding stock of mortgages. So new 30 year mortgage rates are around 3.31%, (a record low). But as at 2011 (it’s probably lower now) 28 million Americans had outstanding mortgages with rates over 1% higher than the rate for new mortgages – in theory these are all refinanceable at lower levels. You could read this as bad news – but it represents a possible windfall gain for consumers if the transmission mechanism does start working again (lower interest payments equals more spending power). And the Fed is now focused on making the transmission mechanism work – it will get better.

So if the price of US housing is attractive, and mortgage rates have fallen, and there’s an increasing level of demand relative to low supply, how powerful can this be? Well we saw how powerful the negative impact was post 2007 – the multipliers involved with housing construction and household formation (people starting households for the first time, as a result of population growth and immigration, or moving out of a parental home) are very strong. A new housing construction project might result in a contractor hiring more workers, who buy pick-up trucks and power drills, and have wages to spend in their neighbourhoods. They buy cement (from Cemex hopefully, a high yield company we like!) and wood. And the people who move in buy carpets, chairs and flat screen TVs (is it time to stop saying flat screen when it comes to TVs? Probably). The Australian Bureau of Statistics calculated construction multipliers back in 2002 (the link is here). They found that there was an initial effect (the employment of construction workers and what they produce), a first round effect (the output and employment of those that produce the goods and services to the construction industry needs), an industrial support effect (the extra output impact on the suppliers to that first round effect), and a consumption induced effect (increased spending resulting from the wages resulting from all of those efforts). The ABS calculated that every US$1 million spent on construction output results in US$2.9 million of output in the economy as a whole. And, better still, gives rise to 13.5 jobs in construction and 55.5 jobs in the economy as a whole (I’ve pro-rated the jobs upwards from the Australian example, as their original calculations were using the Aussie $). The ABS did warn about the multiplier being overstated from the theory to the actuality, and Australia is obviously not America – but the numbers show the power of housing and construction, and could make you very bullish on the US economy over the next couple of years.

Which brings me on to my final, and tenuously related point – I had a coffee with George Trefgarne last week, the former economics editor of the Daily Telegraph, and the author of Metroboom, a paper about Britain’s recovery from the 1930s slump. We can debate about whether it was austerity or currency devaluation that got the UK out of depression – but house building was certainly part of the solution. Between 1931 and 1939 we were building from 200,000 to (in 1936) over 350,000 new houses per year. Compare that to the UK today, where despite the much bigger population, we’re building under 150,000 houses per year, whilst rents rise and affordability remains very poor for most. In some ways we are lucky – we have a potential solution to the UK’s weak growth – allow house building to take off (by loosening planning restrictions, incentivising house builders to release land banks). If you are Spain, and you have a huge glut of housing, this is not a way out of the ongoing crisis – but for the UK, or the US, building homes could be the answer.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox