Another year over – 2012 returns in fixed income markets

It’s been another massive year for the global economy. Europe saw LTROs, Greece got a haircut, sovereign downgrades and record high unemployment rates. The peripheral European nations attempted to implement austerity measures with limited success. The US re-elected President Obama and the focus quickly shifted to the upcoming fiscal cliff. In the UK, an Olympics induced bounce in growth was the sole bright spark for an economy which appears to be stuck in quick sand and may well lose its prized AAA rating in 2013.

The IMF, being unusually succinct, probably summed up the state of the global economy the best by entitling their latest World Economic Outlook “Coping with High Debt and Sluggish Growth”. The advanced economies account for around two-thirds of global GDP and if they are sluggish then global growth will be sluggish too.

With all this uncertainty and risk in 2012, how have fixed income markets performed? Surely government bonds will be the safe haven of choice?

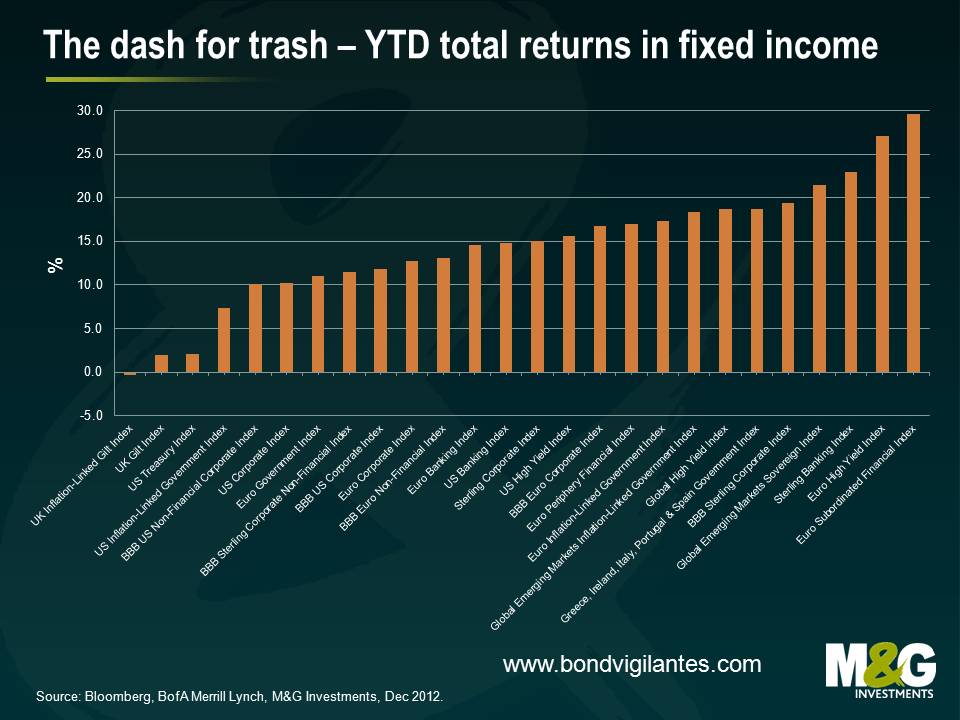

In absolute and local currency terms, it’s been another great year for the markets with everything generating a positive return except UK linkers. It’s been a fall in grace for UK linkers, which were actually one of the best returning asset classes of 2011. The UK linker market was buffeted in 2012 by weak growth expectations and uncertainty surrounding proposed changes to the RPI calculation.

But looking elsewhere, investors had the opportunity to secure some excellent returns in 2012 by taking some risk. The best performing asset class of our sample was European subordinated financial debt which registered a return of 29.5%. European high yield wasn’t far behind with a return of 27.1%, followed by Sterling banks which returned 23.0%.

ECB President Mario Draghi and the ECB’s measures to support the Eurozone also had a positive effect of debt investors in peripheral Eurozone debt, with an index made up of bonds from Greece, Ireland, Italy, Portugal and Spain government bonds up 18.7%. Not a bad return for investors considering the question marks hanging over the ability of these nations to service their respective debt obligations in an environment of political uncertainty and recessionary levels of growth.

Other highlights include global high yield (up 18.7%), European peripheral financials (up 17.0%) and US high yield (up 15.6%). At the less risky end of the spectrum, European investment grade corporates returned 12.8% and US investment grade corporates returned 10.2%. Emerging market debt also did well, with EM sovereigns debt posting a fantastic return of 21.4%.

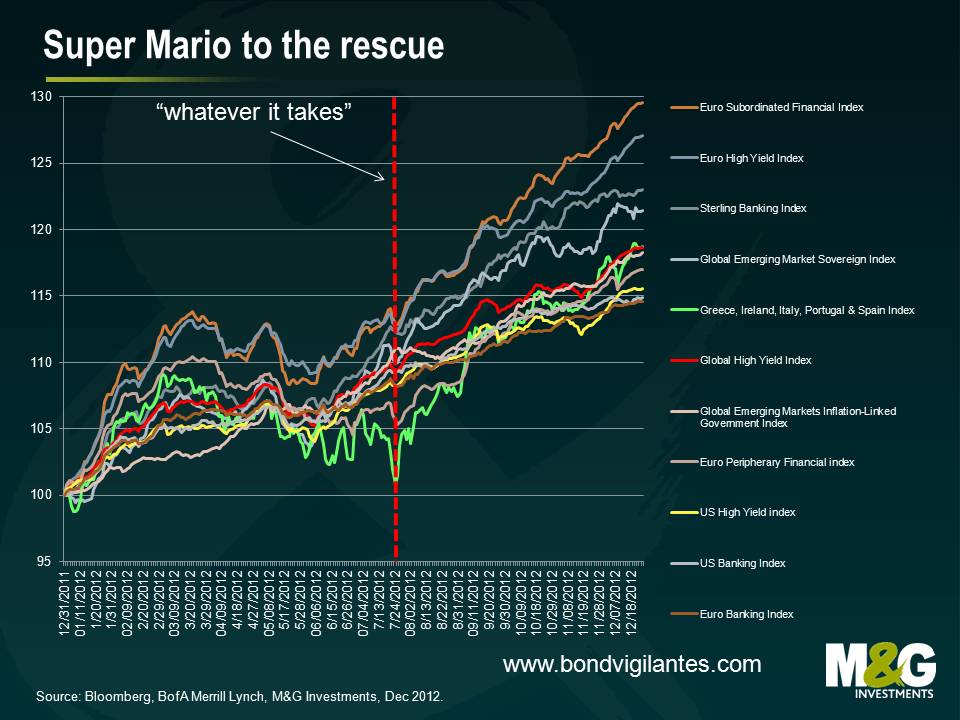

As outlined earlier, it appears that the global economy faces some substantial fundamental headwinds. So how was it that the riskiest asset classes in fixed income have performed the best? Three little words – “whatever it takes”. Mario Draghi’s speech in late July supercharged returns for the riskiest asset classes and stimulated the “dash for trash”. “Within our mandate, the ECB is ready to do whatever it takes to preserve the euro. And believe me, it will be enough”.

Well Mr Draghi, the markets have certainly believed you. For example, an index of government debt issued by Greece, Ireland, Italy, Spain and Portugal had up until the speech date generated a return of around 5%. The index ended up generating a 17% return, with investors comforted by Mr Draghi’s comments.

It seems to us that the Ostrich effect (the avoidance of apparently risky financial situations by pretending they do not exist) had a significant impact on markets in 2012. And in a world of ultra-low interest rates and negative real returns in cash, investors must take on risk. It is precisely what central banks are encouraging us to do. But uncertainty breeds volatility and in order to generate higher returns investors must face this volatility head on. It will be a feature of the market in 2013.

About the only thing we can say for certain is that it is unlikely that fixed income will continue to generate excellent returns across the spectrum from government bonds to high yield. For example, double-digit returns in European investment grade are not normal and has occurred only three times in the last seventeen years. On the other hand, the asset class has posted a negative return in only two of those seventeen years, with the largest loss being -3.3% in 2008. In US high yield, the consensus amongst analysts is that high yield markets will generate a return of around 4-6%, the result of coupon clipping. Analysing returns for the asset class shows that a coupon-clipping year has occurred only once in the past twenty-five years.

We posted our bond market outlook last week. It looks like the US may experience a housing induced growth spurt, Europe will eventually get round to dealing with its issues and the UK has a long way to go to secure economic growth. We like non-financial corporates, are worried about EM debt valuations and remain confident that there are still attractive investment opportunities in several areas of the fixed income universe. For an expansion of these views and more, please see here.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox