China’s investment/GDP ratio soars to a totally unsustainable 54.4%. Be afraid.

“Once upon a time, Western opinion leaders found themselves both impressed and frightened by the extraordinary growth rates achieved by a set of Eastern economies. Although those economies were still substantially poorer and smaller than those of the West, the speed with which they had transformed themselves from peasant societies into industrial powerhouses, their continuing ability to achieve growth rates several times higher than the advanced nations, and their increasing ability to challenge or even surpass American and European technology in certain areas seemed to call into question the dominance not only of Western power but of Western ideology. The leaders of those nations did not share our faith in free markets of unlimited civil liberties. They asserted with increasing self-confidence that their system was superior: societies that accepted strong, even authoritarian governments and were willing to limit individual liberties in the interest of the common good, take charge of their economies, and sacrifice short-run consumer interests for the sake of long-run growth would eventually outperform the increasingly chaotic societies of the West. And a growing minority of Western intellectuals agreed.

The gap between Western and Eastern economic performance eventually became a political issue. The Democrats recaptured the White House under the leadership of a young, energetic new president who pledged to “get the country moving again” – a pledge that, to him and his closest advisers, meant accelerating America’s economic growth to meet the Eastern challenge.”

The passage is the opening to the highly readable and hugely influential 1994 paper The Myth of Asia’s Miracle. The period referenced is the early 1960s, the dynamic president was John F. Kennedy (read Bill Clinton), and the rapidly growing Eastern economies were the Soviet Union and its satellite nations (read East Asia). Author Paul Krugman took on the prevalent East Asian euphoria by drawing disturbing parallels between the unsustainable way that the Asian Tigers were managing to generate supersonic growth, and how the recently obsolete Soviet Union had also once achieved seemingly miraculous growth rates. Krugman’s paper gained widespread attention at the time (even more so post the 1997 Asian crisis), and succeeded in refocusing attention on the concept of productivity. It mattered not what the growth rate was, but how it was achieved.

To explain this and briefly summarise, consider what actually drives economic growth. Growth accounting shows that GDP per capita growth comes from two main sources; inputs and efficiency. The ‘inputs’ can be split into labour (e.g. growth in employment) and capital (e.g. the accumulation of physical capital stock such as machines and buildings). But long term, sustained per capita economic growth tends to come not from increases in the ‘inputs’, but from increases in efficiency, of which the main driver is technological progress. Nobel Laureate Robert Solow showed in his seminal 1956 paper that technological progress had accounted for 80% of US per capita growth between 1909 and 1949, although more recent studies have suggested a still substantial figure of more like 45-55% thereafter.

Krugman pointed to previous research showing that the Soviet Union’s rapid growth had not been due to efficiency gains. Indeed, the USSR was considerably less efficient than the US, and showed no signs of closing the gap. Soviet growth had been solely due to the ‘inputs’, and input-driven growth has diminishing returns (e.g. there is a finite number of workers you can educate). The USSR’s growth was largely ‘built on perspiration rather than inspiration’.

In a similar way, the Asian Tigers’ rapid growth was due to an ability to mobilise resources. There was no great improvement in efficiency, and no ‘miracle’ – it could be fully explained by the employed share of the population rocketing, education improving dramatically, and an enormous investment in physical capital (in Singapore, investment as a share of output jumped from 11% to more than 40% at its peak). But these were one time changes; they weren’t repeatable.

Fast forward to 21st century China.

There is a perception that China’s rocketing growth rate has always been reliant on heavy investment, but that’s not the case. Investment, or capital formation, has of course been an important driver, but the ‘pre 2008’ China did achieve rapid productivity gains thanks to the rise of the private sector and technological catch-up as the economy slowly began to open its borders.

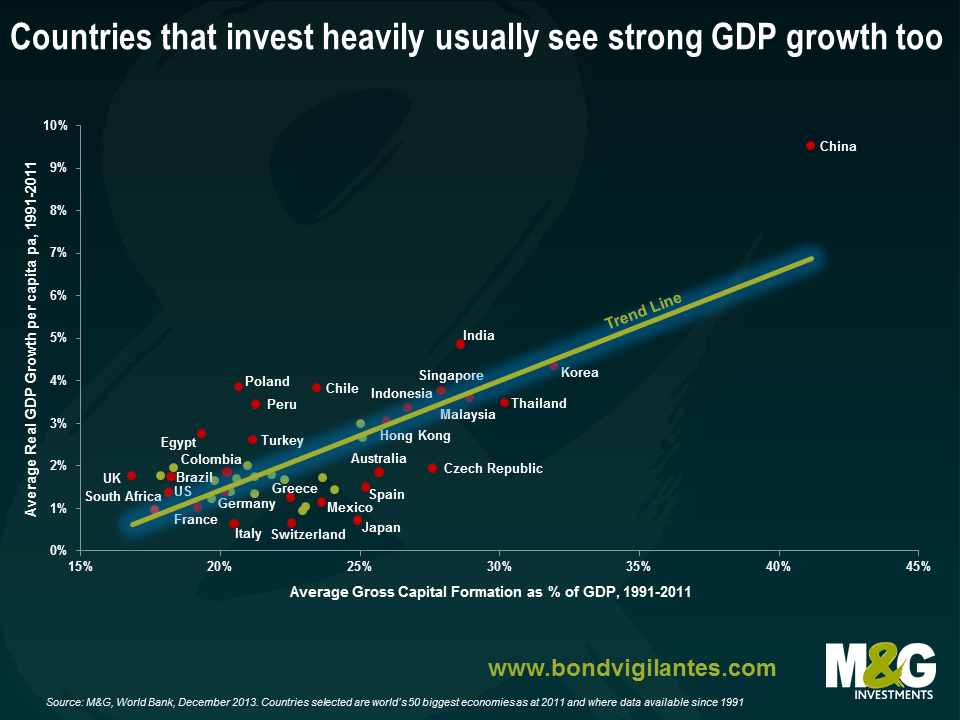

In the chart below, I’ve looked at how much the world’s biggest economies have invested as a percentage of their GDP, and compared this to the countries’ GDP per capita growth rates. Countries with higher investment rates tend to have higher GDP growth rates and vice versa, which is intuitive and supports the discussion above. Since the 1990s, most (but not all) emerging/developing countries have been positioned towards the top right hand side with higher investment and higher growth rates, and the more advanced economies have typically been towards the bottom left with lower investment and lower growth rates. In one extreme you have China, where investment has averaged over 40% of GDP, and the GDP per capita growth has averaged a phenomenal 9.5%. The fact that China’s growth rate is well above the trend line in the chart is indicative of the productivity gains that China has achieved over the period as a whole on average. The country with the weakest investment rate is the UK.

‘Post 2008’ China looks a different animal. Productivity and efficiency seem to be plummeting, where GDP growth is becoming dangerously reliant on the ‘inputs’, namely soaring investment. We’ve all heard about how China’s leaders desire a more sustainable growth model, featuring a rebalancing of China’s economy away from investment and export dependence and towards one that is more reliant on domestic demand and consumer spending (e.g. see the 12th 5 year plan covering 2011-2015 or the Third Plenum). In practice, what we’ve instead consistently seen is an inability or unwillingness to meaningfully reform, where any dip in economic growth has been met with yet another wave of state-sponsored overinvestment. (Jim recently blogged about economist Michael Pettis’ expectation that China long term growth could fall to 3-4%, a view with which I have a lot of sympathy. Please see also If China’s economy rebalances and growth slows, as it really must, then who’s screwed? for an additional analysis of the implications of China’s economic slowdown).

It was widely reported earlier this week that China’s 2013 GDP growth rate fell to a 13 year low of 7.7%, a slowdown that seems to have continued into 2014 with the release of weak PMI manufacturing reading yesterday. But much more alarming is how the makeup of China’s growth has changed: last year investment leapt from 48% of China’s GDP to over 54%, the biggest surge in the ratio since 1993.

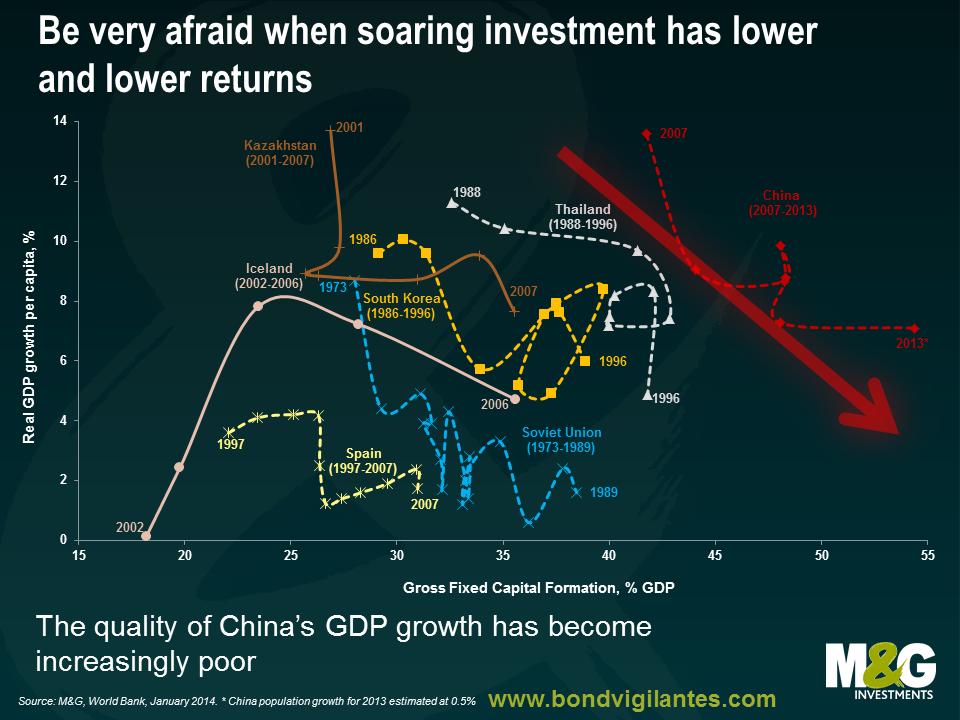

The chart below puts China’s problems into perspective. As already demonstrated, there is a strong correlation between different countries’ investment rates and GDP growth rate. There also tends to be a reasonable correlation over time between an individual country’s investment rate and its GDP growth rate (Japan’s experience from 1971-2011 is a good example, as shown previously on this blog). Over time, therefore, a country should be broadly travelling between the bottom left and top right of the chart, with the precise location determined by the country’s economic model, its stage of development and location in the business cycle.

It should be a concern if a country experiences a surge in its investment rate over a number of years, but has little or no accompanying improvement in its GDP growth rate, i.e. the historical time series would appear as a horizontal line in the chart below. This suggests that the investment surge is not productive, and if accompanied by a credit bubble (as is often the case), then the banking sector is at risk (e.g. Ireland and Croatia followed this pattern pre 2008, Indonesia pre 1997).

But it’s more concerning still if there is an investment surge accompanied by a GDP growth rate that is falling. This is where China finds itself, as shown by the red arrow.

Part of China’s growth rate decline is likely to be explained by declining labour productivity – the Conference Board, a think tank, has estimated that labour productivity growth slowed from 8.8% in 2011 to 7.4% in 2012 and 7.1% in 2013. Maybe this is due to rural-urban migration slowing to a trickle, meaning fewer workers are shifting from low productivity agriculture to higher productivity manufacturing, i.e. China is approaching or has arrived at the Lewis Turning Point (see more on this under China – much weaker long term growth prospects from page 4 of our July 2012 Panoramic).

However the most likely explanation for China’s surging investment being coupled with a weaker growth rate is that China is experiencing a major decline in capital efficiency. Countries that have made the rare move from the top left of the chart towards the bottom right include the Soviet Union (1973-1989), Spain (1997-2007), South Korea (1986-1996), Thailand (1988-1996) and Iceland (2004-2006). Needless to say, these investment bubbles didn’t end well. In the face of a labour productivity slowdown, China is trying to hit unsustainably high GDP growth rates by generating bigger and bigger credit and investment bubbles. And as the IMF succinctly put it in its Global Financial Stability Report from October 2013, ‘containing the risks to China’s financial system is as important as it is challenging’. China’s economy is becoming progressively unhinged, and it’s hard to see how it won’t end badly.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox