Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

I enjoyed this letter which was printed in the Times last Saturday.

Sir, The selling and buying of Northern Rock mortgages between banks reminds me of a wartime story. It involved the busy exchange of corned-beef between black-marketeers.

One purchaser complained that the beef he had just bought was unfit for human consumption. He was told that the beef was not intended for human consumption, but for trading purposes only.

N.ELLIOTT

Stockton-onTees

The strains in the money market persist. In the UK, the focus for bank treasurers is to make sure they have liquidity over year end. This has pushed up interbank interest rates way above the Bank of England’s official rate of 5.75%. The forward cost of money over New Year is 7.23% (one month rate, one month forward), nearly 1.5% above the Bank rate. Good news for those who are long of cash (money market funds for example) but otherwise a drag on economic growth – and remember that corporate loan rates are fixed from these interbank rates too.

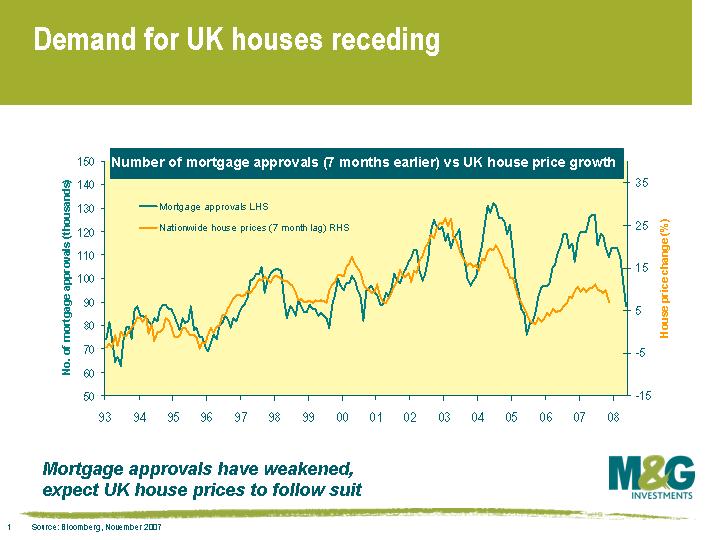

In this comment early last month, I posed the question as to whether the UK housing market was on the brink. Well, today’s data leads me to the conclusion that it has gone over the edge and we are entering a bear market for homeowners. This view is based on one of my favourite indicators of the future direction of the housing market – the level of mortgage approvals. Mortgage approvals are akin to blank cheques for homebuyers. As the attached chart shows, just 88,000 mortgages were approved in October, which was 7,000 less than expected and the smallest number since February 2005.

In this comment early last month, I posed the question as to whether the UK housing market was on the brink. Well, today’s data leads me to the conclusion that it has gone over the edge and we are entering a bear market for homeowners. This view is based on one of my favourite indicators of the future direction of the housing market – the level of mortgage approvals. Mortgage approvals are akin to blank cheques for homebuyers. As the attached chart shows, just 88,000 mortgages were approved in October, which was 7,000 less than expected and the smallest number since February 2005.

This points to prices falling (and indeed data released by Nationwide today indicate that house prices fell by 0.8% in October) as demand slackens. Approvals fall if fewer people ask for a mortgage, or less firms are willing to grant them. On the first point, the consumer is already stretched, and is also now well aware that prices may slide further, so sentiment has eased and buyers are hesitant. And on the other side of the equation, lenders fear a similar slowdown and face a credit crunch, so are tightening lending criteria, raising mortgage rates, or pulling out of the business altogether.

Looking forward, I think interest rates will have to come down as the economy slows. But how far we fall is not yet known.

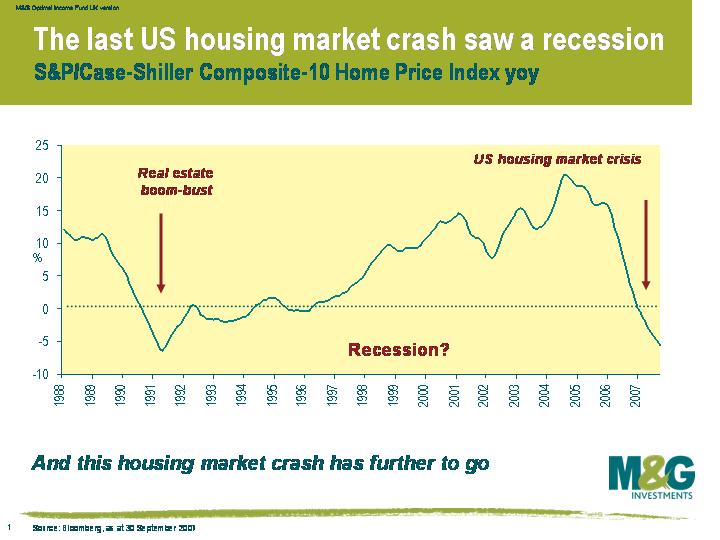

US house prices fell by 5.5% in the year to the end of September, according to the S&P Case-Shiller Composite-10 Index (see opposite chart). The pace of decline is quickening – prices fell by the most in at least 20 years during the third quarter, a very painful event for the US home owner.

US house prices fell by 5.5% in the year to the end of September, according to the S&P Case-Shiller Composite-10 Index (see opposite chart). The pace of decline is quickening – prices fell by the most in at least 20 years during the third quarter, a very painful event for the US home owner.

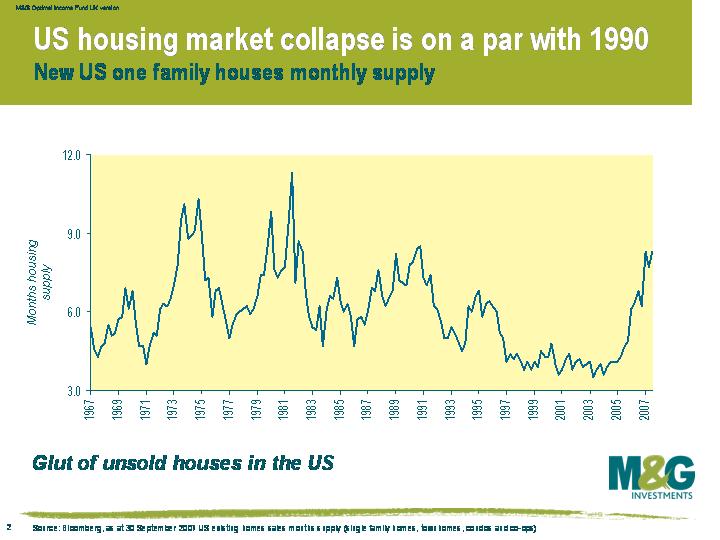

Prices will need to continue falling until the huge excess supply on the market is cleared. This chart shows the monthly supply of houses in the US, which is a commonly used indicator of how long it will take to take sell all the houses on the market at the current sales pace. The total supply of houses on the market is now at levels last seen in the housing slump of 1991-92.

Prices will need to continue falling until the huge excess supply on the market is cleared. This chart shows the monthly supply of houses in the US, which is a commonly used indicator of how long it will take to take sell all the houses on the market at the current sales pace. The total supply of houses on the market is now at levels last seen in the housing slump of 1991-92.

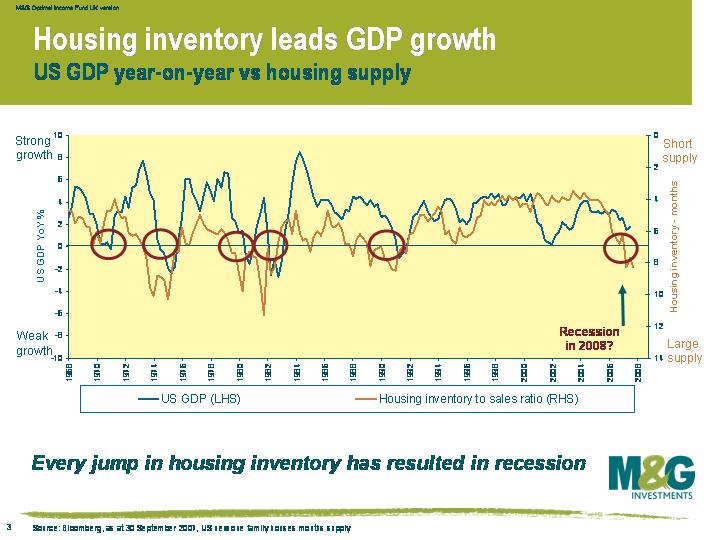

What does a surge in housing supply mean for US growth? See this chart – the housing supply is on the right hand axis and inverted, and US economic growth is on the left hand axis. Data going back to 1968 shows that the five previous times that housing inventory has jumped, recession has followed about a year later. The monthly supply broke above 7 months in the first quarter of 2007, which has historically been about the level that tips the economy into recession.

What does a surge in housing supply mean for US growth? See this chart – the housing supply is on the right hand axis and inverted, and US economic growth is on the left hand axis. Data going back to 1968 shows that the five previous times that housing inventory has jumped, recession has followed about a year later. The monthly supply broke above 7 months in the first quarter of 2007, which has historically been about the level that tips the economy into recession.

Even though the US bond market has been suggesting a US recession for a while (see previous yield curve blog), economists generally seem to be much more positive, with this month’s survey of 70 economists by Bloomberg predicting growth next year of 2.4% on average. However, the current housing market dynamics paint a gloomier picture than suggested by the economists’ crystal balls.

A couple of weeks ago I wrote about the possibility of the Post Office and National Savings taking a larger and larger share of the UK’s savings if confidence in the banking sector continues to wobble (see here). In the Japanese recession their Post Office at one stage held 25% of all the world’s savings! The weekend press has been full of adverts for the “People’s Post Office“, offering an interest rate of 6% – “Let’s see the high street beat that one”, they boast. The Post Office is 100% government owned, so you might think that your deposits are 100% risk free. Sadly this doesn’t seem to be the case, and your money is actually being put into an account “provided by Bank of Ireland“. This isn’t intended to be a comment on the credit worthiness of that institution in particular – I would be concerned if it was any institution other than HM Government. The Bank of Ireland is AA rated at the senior level, but its borrowing costs have risen steeply in the recent credit crisis as the market worries about the state of the Irish property market. Its 5 year credit default swaps (insurance premium against default risk) have risen from just 10 bps per year in June, to over 90 bps now. If the government wishes to outsource the management of the Post Office savings account to a third party it should add its own guarantees for capital, interest and liquidity to prevent even the whiff of losses to depositors. Could the UK economy cope with rolling news coverage of long winding queues outside the Post Office (insert gag here about there already being long winding queues at every Post Office )? The government should offer a lower rate than the market on its savings products, but give absolute security of investment. As a comment left by a reader on the blog that I wrote about NS&I noted, the government is offering the highest cash ISA rate in the market, for the highest level of security. How can that work without crowding out the banking sector?

A digression – a colleague popped into a certain high street bank last week to pay in a cheque. As he queued for a cashier, a salesperson went up and down the line offering customers unsolicited information about taking out buy-to-let mortgages. They used to say that for short-memoried bankers “never again” meant seven years. Is it now less than seven weeks?

Over a pint with relatives the other night in the Anglesea Arms in Hammersmith (incidently the best pub in London), I discovered that the Leaviss family fortune was wiped out by a banking collapse. Whilst the size of the supposed fortune has doubtless grown with the telling over the years (from “miniscule” to “tiny”), some googling shows that the bank holding Great Grandpa Leaviss’s savings did indeed go under, back in 1920. Farrow’s, a bank with 75 branches went bust, and its directors ended up in prison. The bank’s founder, Thomas Farrow, set up the institution as “the foe of money lenders”, offering high interest rates on current accounts (high for the time, albeit only 0.5%) and “permitting his customers, however small their accounts, to borrow freely”. At least we’ve learned since then not to allow poor credits to borrow freely haven’t we? Oh. Anyway, playing the Mervyn King role in this banking failure, the then Chancellor of the Exchequer announced in the Commons that the government “had known for some time of the bank’s difficulties, but did not see that it could usefully or prudently intervene”. Thanks a bunch. Where was the Alistair Darling of the age when Great Grandpa Leaviss needed him?

US economist Hyman Minsky came to the public eye after his model on asset bubbles unerringly predicted the boom and bust of tech stocks (unfortunately Minsky didn’t live to see his fame – he died in 1996). The credit bubble deflation that global financial markets are now facing is following a similar pattern.

Minsky’s underlying theory was that stability breeds instability. Long periods of economic stability result in investors taking more and more risk. As demand for risky assets increase, there is a compression in the risk premium. Leverage begins to grow in predictable stages as investors take advantage of easy credit access to borrow excessively, and end up overpaying for assets.

Minsky believed there were three types of borrower, who are increasingly risky in nature. Hedged borrowers are able to meet debt payments from cash flows. Speculative borrowers can meet interest payments, but have to keep rolling the debt over to pay back the original loan (think Northern Rock). Ponzi borrowers (named after the Ponzi pyramid scheme in the US) aren’t able to repay interest or the original debt, and rely on rising asset prices to allow the debt to be refinanced (think sub-prime borrowers). The longer economic stability lasts, the greater the portion of Ponzi borrowers. Financial institutions react to stability and low risk premiums by increasing leverage and devising ways of getting around regulations in an effort to drive profits higher (think of off-balance sheet financing such as SIVs).

The ‘Minsky Moment’ comes when risk appetite goes into reverse. “This is likely to lead to a collapse of asset vales”, wrote Minsky. It looks like May this year marked the inflexion point, when the spread (ie excess yield over government bonds) available on US and European high yield bonds reached all-time lows. Spreads have widened considerably over the past few months, but as we’ve argued on this blog, we think the repricing of risk has only just begun. The Ponzi sub-prime borrowers have already been hit, but the speculative borrowers are only starting to be hit, and the hedged borrowers are still sitting comfortably. We’re still at the early stages of forced selling, as CDOs liquidate, hedge funds unwind, and investors reduce leverage.

Many thanks to George Magnus, Senior Economic Adviser at UBS, who has written a number of pieces on Minsky this year.

Sotheby’s share price fell a whopping 37% in one day last week. Surely this was something of an overreaction to a poor auction? – cue a discussion with our resident art specialist Jim Leaviss. It turns out that in the increasingly competitive art world, auctioneers have turned to underwriting auctions in a bid to keep business flowing. Sotheby’s, it seems, went into the autumn auctions after getting board approval for $500 million of guarantees, meaning that Sotheby’s promised fixed prices to sellers whether their art sold or not. And when Sotheby’s failed to shift Van Gogh’s ‘The Fields (Wheat Fields)’ and Georges Braque’s L’Echo last week, they were left with the paintings themselves. Who knows what their mark-to-market value is.

Sound anything like the leveraged loan market? By the start of the summer ’07 banks had underwritten several hundred billion dollars worth of loans to sub investment grade borrowers. The ‘originate to distribute model’ meant that banks were willing to underwrite loans in massive size. The working assumption was that the banks would off-load the risk through the usual syndication process whilst commanding a very lucrative fee from the borrower. It had proved a very profitable approach for as long as markets were rosy. However, the summer’s credit crunch arrived and the buyers were either demanding better terms or were nowhere to be found. Banks, who had effectively bought the loans, were forced to take large write downs on their undertakings. They continue to struggle to sell on large portions of their commitments with current estimates in the $250bn arena.

The comparisons between the two models are all too obvious. The similar reaction from the equity market, now, all too understandable.

Not another bearish comment on the financial system, it’s just that I went to see the Sex Pistols at Brixton Academy last night, and that song was their encore. They were ace, but now I can’t hear. Back when they got famous in inflation-ridden 1976, oil was only $50 a barrel in today’s money. Them were the days.

OK – I can’t resist. Let’s turn it into a bearish comment on the UK financial system. There’s a much quoted fact that modern society is just three missed meals from anarchy. I tried to track down the source of this wisdom – Marx perhaps, or Che Guevara? It turns out that it comes from here: “They say that every society is only three meals away from revolution. Deprive a culture of food for three meals, and you’ll have an anarchy”. Arnold Rimmer, from sci-fi comedy Red Dwarf. How far away were we from a full blown banking collapse in mid September? I think that if the Government hadn’t guaranteed all Northern Rock deposits when it did, late on Monday 17th, we would have been there. The share prices of two similarly funded mortgage banks had started to slide dramatically, which would have been negatively reported in the next day’s press, leading to queues in all directions on the UK’s high streets for the rest of the week. And queuing was not an irrational response – as my dad likes to say whenever there’s talk of a petrol blockade, “if you’re going to panic, panic early”, and off he drives to the BP garage. Deposit protection is of course limited, and who knows how long it would take to get your money back? For all the criticism the authorities have had thrown at them recently, they averted a run on the UK banking system. They did the right thing.

Which brings me to my next thought – what happens when a population loses faith in the banking sector? What happens if something like the run on Northern Rock happens again? Well we saw what happened in Japan over the last decade following the bubble bursting there, with its associated banking crisis – people put their money into the state backed Japan Post savings bank. As a result Japan Post became the largest holder of savings in the world, and accounted for 25% of all Japanese household assets. Japan Post invested a lot of these savings into Japanese Government Bonds (JGBs) and yields on those assets fell to around 0.5%. We have already started to see something similar happen here – National Savings & Investments reported record inflows around the time of the Northern Rock crisis, with sales doubling or trebling for many of its products. Sales of such products help finance the government’s budget deficit, so as a result gilt issuance will be lower than it would have been. If it does happen again, expect massive inflows into these 100% safe products, and into AAA rated gilts. And watch gilt yields fall, and fall, and fall…

This is a link to a recent sketch between John Bird and John Fortune on ITV’s ‘The South Bank Show‘. They discuss in brilliant satirical style the problems we have seen in the financial markets in the last few months. At the time of writing, the clip has been viewed by almost a quarter of a million people (and judging by the comments, many of these viewers are from the US).

Carina Ltd, a CDO managed by State Street, is being liquidated after the credit quality of its collateral fell below predetermined levels, allowing senior note holders to force a fire-sale of assets. Carina was originally a $1.5bn CDO when it was launched in September 2006, and is the first CDO to begin unwinding since the credit crunch began. The rating on an AAA rated portion of the CDO was downgraded 18 notches by S&P, taking the rating to CCC-.

S&P has been informed of the default of 13 other CDOs. The dumping of assets on the market should see prices in all forms of structured credit continue to spiral downwards, which will inevitably cause spreads in the conventional corporate bond and high yield bond market to widen in sympathy.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.