Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

Taken as a whole, the Eurozone economy had until recently been relatively robust in the face of the credit crunch. This is about to change. There have already been some worrying data releases this month, particularly in the manufacturing area. Things got worse yesterday, when the European Commission economic sentiment index collapsed. The index saw the second biggest monthly drop since the survey began in 1985 – only October 2001 saw a bigger fall – and economic sentiment is now running at the lowest level since 2003. The survey showed that sentiment falls were widespread across both sectors and countries – Germany was not immune, while the drop in economic sentiment in Italy was bigger even than the fall post 9/11.

Today’s worrying data release was that inflation accelerated from 4.0% to 4.1%, the fastest rate since April 1992. The ECB aims to keep inflation below 2%, so it clearly has a big problem. A few weeks ago the European bond market was pricing in another couple of rate hikes, although the wave of weak economic data this month has meant that rates are now expected to remain on hold. However, as the ECB demonstrated at the beginning of this month, it’s prepared to hike rates, even in the face of a slowing economy. Another such move will serve to inflict even more pain on European companies, and would make me even more nervous about taking on a lot of European credit risk right now.

While Leonard Lauder was chief executive of Estee Lauder, he noticed that sales of his firm’s lipsticks tended to rise during economic downturns – not what one might expect, particularly of a luxury good. The rationale is that people like to treat themselves, and when times are hard, a shopper may refrain from purchasing that pair of shoes she has had her eyes on and instead opt for a new shade of lipstick.

Some other companies that seem to be doing fairly well out of the credit crunch are McDonalds and Dominos, who have reported increased sales as people look for cheaper treats (not exactly luxury goods – perhaps more a case of comfort eating). Meanwhile Hershey on Wednesday reported the biggest jump in sales since 2006, while Cadbury’s expect higher profit margins than in H1 2007, and that’s despite a 40% jump in cocoa prices this year.

L’Oreal’s recent results were disappointing, although sales growth actually increased 3% in North America. If the theory holds, the deteriorating outlook on this side of the Atlantic should soon lead to that figure picking up.

Attached is a link to the best article I have yet read on the twists and turns of the Bear Stearns saga. In my opinion, it is really worth a read. The article highlights that when confidence (which is essentially the life-blood for highly levered financial institutions) disappears, liquidity soon follows. The fall from grace can take place in a matter of days, if not hours.

The article emphasises the role that the rumour-mill played in Bear’s downfall. This is made all the more relevant at the moment given the Fed’s decision this week to cease all uncovered short-selling of brokers and the governmentally sponsored entities Fannie Mae and Freddie Mac. In passing, we were discussing the potential ramifications of this Fed decision around the desk this morning, and the following is worth noting: what will happen to all those players that have had short views on the US economy and on the financial markets in the US – players who have no doubt been shorting the highly levered financial institutions included in the Fed’s ‘out of reach’ list? If they are no longer able to hold these profitable shorts, then where will they look to next to express this same view?

Watch out all those financial institutions who thus far have been off the shorters’ radars, and in particular the currently troubled US regional banks, because this capital may soon be seeking new homes. I don’t think we have heard the last of these stories. Not by a long shot.

It’s difficult to remain relaxed about the outlook for inflation in the UK given today’s strong CPI and RPI numbers (all above expectations), but, if oil is still at $145 a barrel, and food prices remain at these levels in a year’s time, we’ll be facing deflation. Not because these elevated prices levels will cause a collapse in consumer spending and reduce the demand for discretionary goods – though that too will happen – but because of simple mathematics.

Core inflation, which strips out food and energy prices, is at 1.6% in the UK. It’s been at, or about, this level now for 7 years, averaging 1.4%. Headline inflation is at 3.8%, above the Bank of England’s target because of the strength of the food and energy component. Food accounts for 10.9% of headline inflation, and energy is 7.3%. Put together then, food and energy are 18.2% of headline inflation. Now let’s assume that oil stays up at $145 for the next year, and that food prices also stay at current levels. Although those prices will still be hurting us as consumers, the food and energy inflation rate will fall to 0% – it’s all about the year on year comparisons. Now let’s also assume that core inflation keeps rising at its seven year average rate of 1.4%. Simple maths shows that if core is 81.8% of the headline rate, and is increasing at 1.4%, and the remaining 18.2% is at zero, then the headline rate of inflation in the UK in a year’s time could be as low as 1.1%.

The Governor of the Bank has to write a letter to the Chancellor if that headline rate falls below 1%, explaining why he is allowing the economy to flirt with deflation. If the oil price starts to come off, perhaps in response to the slowing global economy, then that letter might just get written at some point in 2009, and we’ll be asking ourselves how a major modern economy copes with deflation – just don’t ask Japan, a decade after its own bubble burst it’s only now starting to move back into positive inflation, albeit tentatively.

Spectators at recent ECB press conferences may well have come away thinking that there is little, if any, evidence of a credit crunch in Europe. According to the ECB, ‘the growth of bank loans to non-financial corporations has remained very robust despite the rises in short-term rates’ and ‘the availability of bank credit has, as yet, not been significantly affected by the tensions.’

We suspect that the reported numbers significantly overstate banks’ willingness and ability to lend. To understand why, it’s worth having a look at a comment that Richard wrote in February about how Porsche outmanoeuvred the banks. In short, earlier this year, Porsche took advantage of a credit facility with a bank, where the facility had been set up before the credit crunch hit. The bank was forced to lend billions to Porsche at unprofitable rates for the bank.

Credit facility drawdowns are becoming more and more widespread. A report released this week by JP Morgan estimates that over the first five months of 2008, circa 46% or $165bn, of credit growth in the Euro area could be attributed to the drawing down on such credit lines. Despite the best efforts of banks to incentivise companies not to use these facilities, irrevocable credit facilities (often made at the height of the credit bubble) remain some of the most attractive funding available for companies. The report estimates that if the entirety of the $4.6 trillion of credit lines outstanding at the end of 2007 were drawn during the next 12 months, capital in the region of $184 billion would have to be posted by the banks.

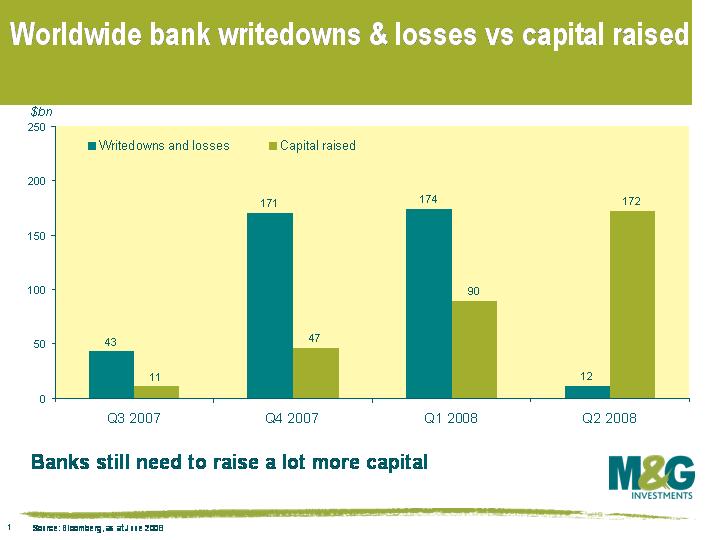

Clearly the potential for further drawdowns is another in a long line of headaches for the banking sector. All is not well, despite noises to the contrary from the ECB. Banks have raised $320 billion of capital since Q3 2007. As this chart shows, banks still need to raise another $80bn to cover losses and write-downs that have occurred to date (and they’ll need to raise even more to cover bank losses and write-downs that occur in future) . Add in the credit facility problem, and it seems that banks will continue to hoard capital and see their profit margins challenged.

Clearly the potential for further drawdowns is another in a long line of headaches for the banking sector. All is not well, despite noises to the contrary from the ECB. Banks have raised $320 billion of capital since Q3 2007. As this chart shows, banks still need to raise another $80bn to cover losses and write-downs that have occurred to date (and they’ll need to raise even more to cover bank losses and write-downs that occur in future) . Add in the credit facility problem, and it seems that banks will continue to hoard capital and see their profit margins challenged.

The soaring oil price has meant that UK National newspapers and the trade press are rife with stagflation fears. The fears are understandable – following the 1973 oil crisis, UK inflation surged, reaching an all time high of 26.9% by August 1975. By the beginning of 1979, UK inflation had fallen below 10%, but the 1979 oil crisis helped propel UK inflation back up to 21.9% by May 1980. The oil price shock we are experiencing now is far more severe in nominal terms, and on a similar scale in real terms, so comparisons with the experience of the 1970s are inevitable.

Inflation was nasty in the 1970s because of what’s called a ‘cost-push inflationary spiral’. The surge in the oil price was a supply shock, and represented a jump in costs for companies. Producer prices surged. Companies then shunted these higher costs onto consumers by putting up prices. Consumer prices surged. The workers and trade unions reacted by negotiating higher wages. Higher wages formed another jump in costs for producers, producers prices rose higher, consumer prices rose higher, wage demands were increased, and so on.

Is something similar happening today? So far, it doesn’t appear so. We’ve had a major oil shock, and producer prices have risen sharply. UK Producer Price Inflation (PPI) was 2.4% in August 2007 and leapt up to 8.9% in the year to this May, the highest figure since March 1982. And yet companies are only having limited success in passing this onto consumers. The Bank of England’s official inflation measure of consumer prices is at 3.3% – worryingly high, but only 0.8% higher than a year ago. Inflation according to the Retail Price Index (RPI) was actually 4.3% in May, the same rate as a year earlier. The gap between RPI and PPI is now the biggest since 1975 (as an aside, if companies aren’t able to pass on costs, then it doesn’t bode very well for profit margins or credit quality).

Perhaps even more importantly, the moderately higher consumer prices don’t appear to be translating into higher wages either. Nominal wage growth has barely moved in the last year, and is a bit below the average rate for the last ten years. Real wage growth has in fact been negative in the UK since the second half of 2006. In other words, workers have generally failed to negotiate wages even in line with inflation, let alone in excess of inflation.

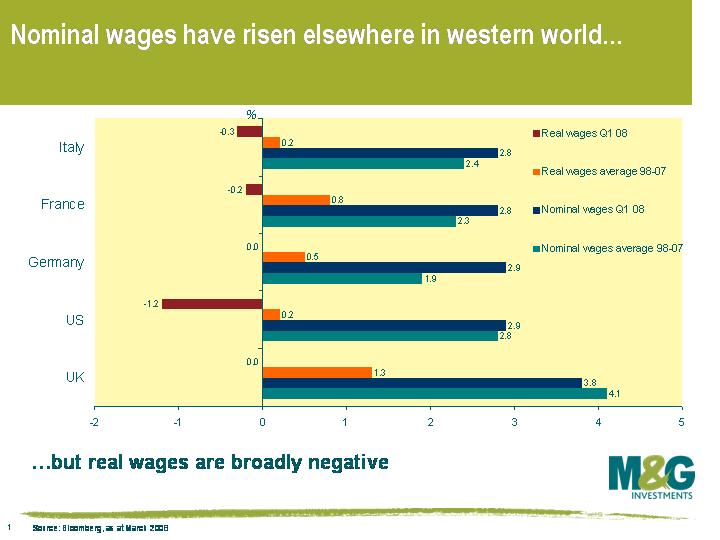

It’s a similar story in the rest of the western world. This chart illustrates that nominal wages have increased at a greater rate in the western economies than in the UK, but real wage growth is either flat or negative (all figures as at end Q1). The economic picture is hardly that of a 1970s style inflationary rout. Labour market reforms (eg reduced trade union power) have combined with greater worker mobility (eg Polish builders) to prevent this oil shock from turning into an inflationary spiral – so far. If long term inflationary expectations rise, which is probably the central banks’ biggest fear, then we may start to see wages creeping up. But for wages to rise from here, workers will need greater negotiating power. This scenario seems unlikely, given the financial deleveraging going on and the rapidly deteriorating UK and global economic outlook. If workers aren’t happy with their pay, there will be soon be quite a few people without jobs who are willing to work for less.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.