Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

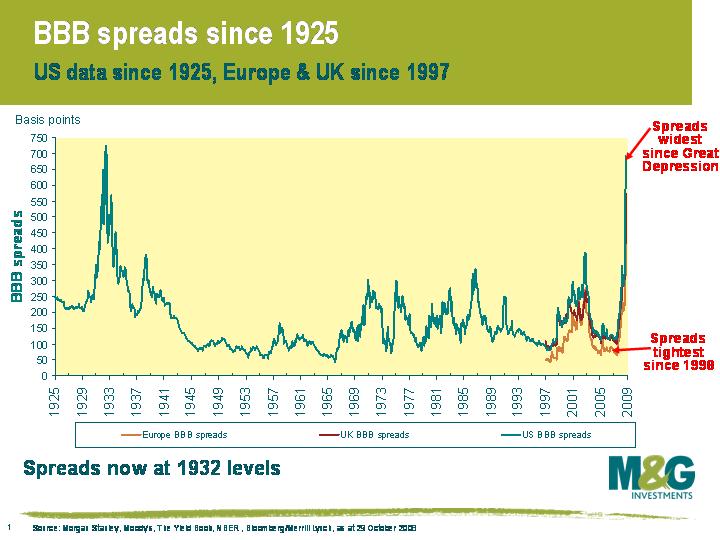

Since May 2007, we’ve seen the Great Credit Crash, with the fastest and sharpest sell off in credit that the modern world has ever seen. In the US, in May 2007, the average BBB corporate bond yielded just 120bps (ie 1.2%) over a government bond. The figure was 699bps as at the end of yesterday. BBB rated bonds now yield 10% on average in the US and UK, and almost 9% in Europe. This chart is a good illustration of the severity of the bear market. US BBB spreads have gone from being the tightest in a decade to the widest since July 1932. In fact, spreads were only wider than they are now in May-July 1932, when the excess yield was 720bps.

Now clearly the BBB index constituents have changed a bit over the past 76 years, with fewer railroad companies and more PC manufacturers, but what was considered BBB then can be roughly assumed to possess the same credit characteristics as a BBB now. This chart is therefore saying that the credit risk premium is as high now as in the depths of depression in 1932 . Put another way, a 7% excess yield means that an investor can afford for 7% of a portfolio of 10 year BBB rated bonds to default every year for 10 years, with a recovery rate of zero pence in the pound, just to break even with the return from a ‘risk free’ government bond. The investment grade corporate bond market is pricing in a horrific economic scenario.

Now clearly the BBB index constituents have changed a bit over the past 76 years, with fewer railroad companies and more PC manufacturers, but what was considered BBB then can be roughly assumed to possess the same credit characteristics as a BBB now. This chart is therefore saying that the credit risk premium is as high now as in the depths of depression in 1932 . Put another way, a 7% excess yield means that an investor can afford for 7% of a portfolio of 10 year BBB rated bonds to default every year for 10 years, with a recovery rate of zero pence in the pound, just to break even with the return from a ‘risk free’ government bond. The investment grade corporate bond market is pricing in a horrific economic scenario.

As readers of this blog will be well aware, we’ve been very gloomy on the global economy for a couple of years. Judging by where corporate bond yields were until this year, our gloomy economic outlook was not remotely believed by the market. This was particularly true in the high yield (junk) bond market.

But to believe that BBB rated bonds are unattractive now, you have to believe that things are going to be worse than in the 1930s. I believe the global economic outlook is very grim, with the developed world heading for a prolonged, nasty recession, however policy makers have learnt lessons from the 1930s and the many recessions since. Banks are being supported, fiscal stimulus is going to be undertaken and interest rates are being slashed.

For a number of years now, we have thought that the credit risk premium for owning corporate bonds was insufficient, and we positioned our portfolios very defensively in terms of credit risk. We favoured ‘AAA’ and ‘AA’ rated bonds over ‘A’ and ‘BBB’ rated bonds in investment grade bond funds, and focused our high yield portfolios away from unrewarding risky assets. Now that credit risk premia are extraordinarily high and policy actions are credit positive, we think BBB rated bonds are attractive and it is appropriate to be long of credit risk in investment grade funds.

Later today the Fed will probably cut US rates by 0.5%, down to 1%. After this we’re only a couple of cuts away from a zero percent Fed Funds rate. When rates are at 0%, what can a central bank do to stimulate the economy? Well some possible answers are found in Japan, although with its economy still struggling to print positive growth numbers a full 18 years after its bubble burst, it may not be the best role model. In March 2001, with Japanese short term rates at 0.15%, the Bank of Japan (BoJ) began a quantitative easing programme. With traditional monetary policy no longer effective (the so called liquidity trap), how could the BoJ stimulate economic activity? It flooded the economy with money by buying financial assets (bills, equity, ABS), and in so-called Rinban operations directly buying Japanese Government Bonds. Rinban operations were designed to make monetary policy effective at longer dated maturities than traditional central bank activities. By buying long dated government bonds the hope was that yields would be pulled down across the curve, and thus reduce borrowing costs for corporates and individuals where loans were benchmarked over government bond yields. The BoJ purchased about $120 billion JGBs per year as part of the plan.

Did it work? Quantitative easing ended 5 years later, with the BoJ having reached its stated aim of returning the economy to inflation (although it did subsequently return to deflation once more). Long dated (20 year) JGB yields did fall too, from about 1.8% in March 2001 to below 1% a couple of years later – but by the time quantitative easing came to an end yields were back up above 2% again, so it’s arguable whether this part of the plan was very successful.

Is quantitative easing something that the western economies will consider? Well to some extent it’s already here – central banks have turned on the printing presses (the $80 billion to bail out AIG for example), are flooding the money markets with liquidity, and have started to buy financial assets (the equity stakes in banks for example). Purchasing of US Treasury bonds might not be too far behind – and remember that the Fed discussed it once before around the time of the 2002 deflation scare. The FOMC talked about “unconventional measures” including purchasing many types of financial assets (and non-financial too – it’s rumoured that they discussed using the secondhand car market as a means of getting cash into the hands of the American public). The June 2002 Fed paper, Preventing Deflation: Lessons from Japan’s experience in the 1990s, is well worth revisiting as a route map for the next few years.

And this might well be a story that takes a few years to unfold – it seems difficult for us to believe that the amount of fiscal stimulus, rate cuts, printing press activity and bank recapitalisation thrown at the global economy won’t result in a sharp rise in inflation, but the Japan experience shows that even then the most extreme measures can’t guarantee that the authorities can generate a bit of lovely inflation.

The vast sums of money being thrown by governments at banks right now have clear implications for developed countries’ credit worthiness. Meanwhile, emerging market governments are facing a crisis of their own. I thought it would be useful to have a look at which countries the bond markets say are at greatest risk of default, both developed and developing.

The attached chart from Bloomberg tracks the 5 year CDS on a handful of developed European countries over the past year, where 5 year CDS is the annual cost of insuring an entity’s debt for five years. So a price of 0.5% means it costs $5000 to insure $1m of debt for a year. As you’d expect, sovereign default risk has risen sharply since September. The risk of the UK government defaulting is about the same as the risk of the Belgium government defaulting, and Belgium isn’t AAA rated – it’s actually rated AA+ by S&P and Aa1 by Moody’s (which is itself a bit generous).

Emerging markets held up bafflingly well until September, but are about to experience a crisis. Jim first warned about emerging market bonds on this blog two years ago (see here), and most recently commented on the asset class in February this year (see here). As this chart shows, South America is in trouble now, and Argentina is on the brink of default, while Venezuela and Ecuador are also distressed.

The rate of deterioration in Eastern Europe is also alarming. Hungary raised interest rates by 3% yesterday to try to stop its currency collapsing (once a country’s currency starts collapsing, then its euro, dollar and yen denominated debt becomes crippling). Today, Belarus has joined Hungary, Ukraine, Iceland and Pakistan in requesting help from the IMF. Russia is in a mess too, with spreads touching 1000bps over Treasuries yesterday after the Bank of Moscow said Russian companies may default on up to a third of all local currency debt.

As recently as July this year, US BBB corporate bond spreads were in line with junk rated emerging market sovereign bonds. This was plain wrong – historically, sovereign defaults have coincided with global economic slowdown, but the substantial risk of default wasn’t being priced in. At the end of yesterday, junk rated emerging market sovereign bonds were trading at a more reasonable 968bps over treasuries, versus 657 bps for US BBB corporates. Emerging market bonds are better value now, but similarly rated high yield corporate bonds still look more attractive. And you have to wonder – while the IMF can help a few governments, how is it going to be able to afford to bail out a whole string of emerging market countries, not to mention the odd developed country?

Inflation-linked bonds around the world have seen heavy losses in the past couple of months. 30 year UK index linked gilts are down by nearly 20 points (15%) since August, with similar selloffs seen in the US and European markets. After the inflation scare of the first half of 2008, with oil hitting $140 per barrel and food prices rocketing, the markets are suddenly realising how quickly global growth is slowing, and that we should be more worried about deflation than inflation. Whilst many people had believed us to be right in predicting very low levels of inflation in 2009, the question we got asked the most was about wage inflation. In the UK particularly, with the Labour Party so weak, wouldn’t the government cave-in to its backers, the Trade Unions, and hike public sector pay? Well with unemployment rising rapidly, it’s not surprising that private sector workers are unable to demand big wage rises (and I spoke to two people over the weekend who volunteered that they have been told they are getting pay cuts with immediate effect). Private sector average earnings growth for the UK has fallen to 3.1% from 4.6% in March – but public sector wage growth is also falling (down from 4% to 3.6%). Last week the Home Office announced that the police would be getting just 2.6% per year for the next three years. On top of all of this, oil has halved in price from July this year, and it looks like food price inflation peaked out in August. We now suspect that Europe could print a negative year on year inflation rate in the second quarter of next year, with the UK not far behind.

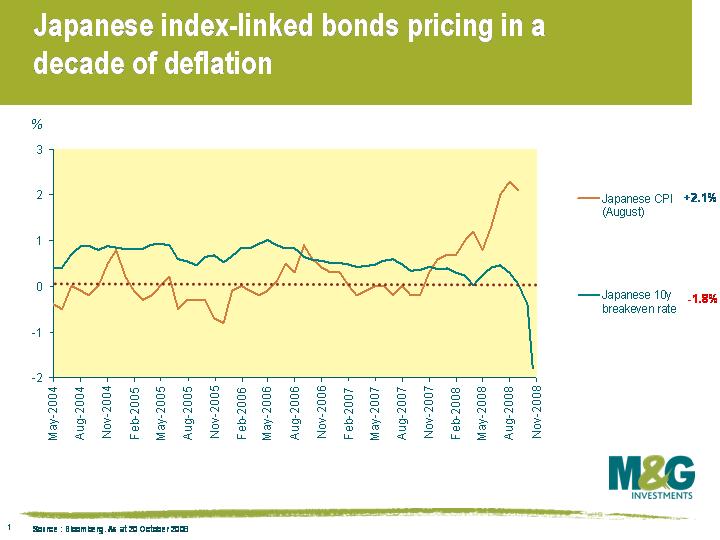

With this backdrop, it is easy to see why linkers have become unloved. However, the selloff has perhaps gone too far, especially in the Japanese market. Japan is no stranger to deflation (it only decisively broke out of falling prices at the start of this year after nearly a decade of negative inflation), but its relatively new JGBI inflation linked bond market is now discounting 10 years of 2% per year deflation (see chart). This is a real yield of 3.5%, the highest available real yield on any G7 government asset (we think – let us know if you find anything higher!). It’s an illiquid and immature market, but that’s sometimes where the best value can be found – UK index linked gilts were issued with real yields of over 4% when our market was brand new. The Japanese government has stopped issuing JGBIs for the foreseeable future as it thinks they are too cheap – we agree.

With this backdrop, it is easy to see why linkers have become unloved. However, the selloff has perhaps gone too far, especially in the Japanese market. Japan is no stranger to deflation (it only decisively broke out of falling prices at the start of this year after nearly a decade of negative inflation), but its relatively new JGBI inflation linked bond market is now discounting 10 years of 2% per year deflation (see chart). This is a real yield of 3.5%, the highest available real yield on any G7 government asset (we think – let us know if you find anything higher!). It’s an illiquid and immature market, but that’s sometimes where the best value can be found – UK index linked gilts were issued with real yields of over 4% when our market was brand new. The Japanese government has stopped issuing JGBIs for the foreseeable future as it thinks they are too cheap – we agree.

It’s always very hard trying to get a sense of historical perspective, particularly when you’re living through something that will be discussed and debated long after we’re all gone. I think this chart helps. It shows the S&P going back to January 1928, and I’ve used a logarithmic scale so that you can get an idea of how this crash compares to those that occurred in previous eras.

The 30% fall in the S&P since the end of August is considerably worse than the 1987 crash. It’s as big as the Wall Street Crash that took place over the month of October 1929 (although there’s a long way to go to match the horrendous bear market that accompanied the Great Depression in 1930-32).

The 30% fall in the S&P since the end of August is considerably worse than the 1987 crash. It’s as big as the Wall Street Crash that took place over the month of October 1929 (although there’s a long way to go to match the horrendous bear market that accompanied the Great Depression in 1930-32).

Readers of our blog in spring ’07 were probably a bit bemused as to why we were banging on about a little island over 1000 miles away from continental Europe, with a population the size of Sunderland/ Venezia/ Gelsenkirchen/ Cordoba/ Strasbourg/ Pittsburgh. It’s pretty clear now – Iceland is probably the world’s best example of the credit bubble, and the subsequent credit bust. Icelandic companies went on a debt fuelled binge, taking over a huge number of UK companies in particular (including, ironically, UK frozen food specialist Iceland, whose slogan forms half the title of this blog).

In February ’07, Stefan said that Moody’s decision to upgrade Iceland’s banks to AAA was “Codswallop” (see here). Moody’s thought that if any banks went under, then Iceland’s government would come to the rescue, and since Moody’s thought Iceland’s government was AAA rated then the banks were too. But as Stefan argued, it was debatable whether a country with Iceland’s population and an economy based around cod had the ability to support banks with liabilities many times the country’s GDP. Then in March ’07 (see here), Richard argued that a slowing economy would be very bad news for Iceland’s banks, and attached a chart from Merrill Lynch showing how Iceland’s deeply incestuous economy, with huge cross ownership, posed a substantial economic risk. Finally in March ’08, in “If it ain’t your cods, it pollocks” (see here) Stefan highlighted how Moody’s had backtracked and returned Iceland’s rating to A1. But even then, credit markets were already pricing Icelandic banks as junk (note that Iceland’s not the only place now closed for business – the restaurant Stefan mentioned has closed too as it smelt a bit too fishy for local residents).

What lessons should be learnt from all of this? There are too many to write about here, but on a general level, the biggest lesson needs to be taught to the ratings agencies. The fall guys from Enron’s collapse were the accountants, namely Arthur Andersen. In the aftermath of Enron, the consultancy side and the audit side were largely separated and became better regulated. Before, the big accounting firms were effectively advising companies on how to ‘interpret’ accounting regulations. They were instrumental in providing guidance on things such as off-balance sheet financing. That’s a pretty big conflict of interest.

The fall guys from this banking collapse will be the credit ratings agencies. In some ways, auditors and ratings agencies are in the same boat – the financial industry relies on their independent judgement, but independence is open to abuse when companies pay for the service themselves. With the ratings agencies (where the consulting element is still intertwined with the rating entity), ratings agencies regularly provided guidance to the banks and brokers on what bonds could or could not be included within a structured deal in order for the deal to achieve the magic AAA rating. Ratings agencies need to be more accountable, and the industry needs to be opened up to much more competition.

Talking specifically about the Iceland debacle, people need to learn that there’s no such thing as a free lunch. In the world of corporate bonds, those bonds that have the highest yield are by definition the highest risk. Similarly, those banks that offer consumers the highest interest rate on their cash deposits are probably offering high rates for a reason – they’re desperate for your money. It’s one thing for the man or woman on the street to not appreciate these risks, but there are many people who should have known a lot better, and that includes people at local councils. Forbes Fenton, the head of our risk team, was telling me yesterday morning about how the Icelandic events remind him of the early 1990s (Forbes spent time in the Cayman Islands trying to unravel BCCI’s accounts). Depositors in the cases of both BCCI and the Icelandic banks were lured by the high interest rates on offer, and parked their money in what were effectively non-UK licensed banks. Prior to BCCI going under, 30 local councils had deposits or other exposure to BCCI. In Scotland, Western Isles council alone lost £23m. Lessons weren’t learnt last time around, and in the UK, that’s cost more than 100 local councils, police authorities and fire services almost £1bn this time around.

In light of the news of recapitalisation of the UK banking sector (which Ben alluded to in his blog yesterday afternoon here) and today’s coordinated global rate cuts, I thought it would be an appropriate time to see whereabouts we are on the road to recovery.

The route map we have been following has been laid out on this blog over the past 18 months, and is updated in this chart. The health of the financial system and the health of the UK citizen is intertwined by a common interest – the housing market. That common interest is based on the fact that homes generally have two owners, the consumer and the bank/building society. In order for the fortunes of these two players to turnaround, mortgage approvals must move up.

The route map we have been following has been laid out on this blog over the past 18 months, and is updated in this chart. The health of the financial system and the health of the UK citizen is intertwined by a common interest – the housing market. That common interest is based on the fact that homes generally have two owners, the consumer and the bank/building society. In order for the fortunes of these two players to turnaround, mortgage approvals must move up.

In order for mortgage approvals to rise, two problems need to be solved. First of all, the banks must have the capital and capacity to lend. The Treasury’s action today goes part of the way towards solving this. Secondly, consumers must want to buy a house, ie find housing to be cheap. The classic way to achieve this is via cutting the financing cost of purchasing a property. This is in the hands of the Bank of England.

To stop the freefalling UK housing market, the Bank of England should do its part by deploying its biggest parachute as quickly as possible. A half point cut today helps, but from my perspective rates need to be reduced a lot more than this. The lowest UK base rate in modern times was 3.5% from July to October 2003, the lowest since 1954. UK rates need to quickly go at least as low as this, and if a rate of 3.5% fails to stimulate the mortgage market, then it needs to be driven much lower.

One of our credit analysts came up to me on Friday and told me to pull my finger out and get something on the blog. So apologies for the lack of comments from mid-September. As you can imagine, things have been rather busy.

A lot has happened in the last few weeks and I thought I’d shed some light. The credit cycle has turned. Abundance of credit has given way to its utter scarcity. Companies – and people – that borrowed to grow and spend cannot ‘just refinance’ as they have done for years, but are now having to pay it back. Frequently, and increasingly, they can’t pay it back. In companies’ cases they can no longer issue new debt to repay old debt, so they have to sell assets. Depending on the nature of those assets, it could be terminal. People haven’t saved, and in a similar way to companies, those that relied on debt to keep going are not able to borrow any more.

The market was very wrong about some very important beliefs: banks and systemically important financial institutions can default. Not even investment banks that managed to survive events such as The Great Depression and the failure of Long-Term Capital Management are safe this time. A few weeks ago we had four independent broker dealers operating in the US; we now have none (since the only two "going concern" broker dealers are registered as bank holding companies). Even the larger regulated deposit-taking institutions can get into trouble and need protection for their depositors (WaMu, Bradford & Bingley). Some governments are coming out and putting their own names behind the entire banking liability structure (Ireland, Denmark). Oh, and as for any doubters about the globalisation or not of financial markets: big, systemic, deposit-taking institutions are failing or being bailed out all over the western world. The prognosis, for now at least, is that the disease is rapidly spreading: last week alone we saw the failures or rescues of more than 10 financial institutions.

The market was very wrong about another thing. There was a saying I heard long ago: "Banks don’t fail; they get cheap". If a bank started to perform badly, its valuation fell and the bank would be bought. Thus, equity holders might lose some value, and then exchange their old shares for ones in the new purchasing company. Creditors, both senior and subordinated, would just get consolidated into the new, bigger entity. Not any more. Barclays refused to resuscitate Lehman, and then bought its US operations for a bargain price the day after its failure. All senior and subordinated creditors got carried out. WaMu also showed that this ‘rescue model’ could also be applied to deposit taking institutions – all of WaMu’s group debt was left in a shell company containing none of the assets that previously supported that debt (they’ve all gone to JPMorgan). Bail-outs, though, as some used to think of them – equity holders lose and creditors are made good – do still take place: HBOS needed saving, and Lloyds was given huge regulatory and governmental support to take on all of the businesses of HBOS. But gone are the days when it was ‘safe’ to buy senior debt and to avoid subordinated debt and equity.

Lots of other things deserve comment, but one of the most violent events of the past couple of weeks was the equity and credit market sell off when it became clear that the much anticipated and much needed TARP program in the US had become embroiled in partisan issues. The markets very clearly needed this package to be passed, so the House worked around the clock to make sure it happened. The TARP was passed on Friday. And the markets relapsed. Perhaps the markets will only be happy once the banking system is nationalised with taxpayers’ injections of equity? $700bn in bail-out money is enough to buy the 10 biggest US banks at current market prices, but it is not the dose of medicine the market originally thought it would be.

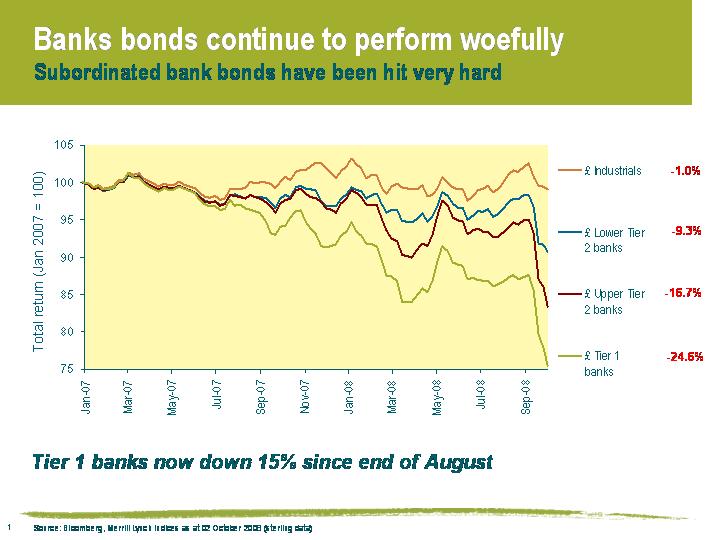

The original ‘supersub’ was the ginger scouser David Fairclough, famed for coming off the bench to rescue the mighty Liverpool FC. The financial markets themselves have returned to the 1970s with chants of stagflation and bank failures emanating from city players. Everyone is fully aware of sub prime, but as I explained in the FT today, corporate bond investors’ main concern should be about sub debt.

Ben argued at the end of August that Tier 1 bank bonds would feel more pain. ‘Pain’ was putting it mildly. As at yesterday, sterling Tier 1 bank bonds have returned -14.4% since the end of August, while euro Tier 1 banks have done even worse, returning -14.8%. We continue to believe that Tier 1 bank bonds are poor value, even at these levels. Given the huge illiquidity in subordinated bank bonds, any forced sellers of this debt (and there are many) are in serious trouble.

Finally, this article published in the New York Times in September 1999 is worth a look. “In moving, even tentatively, into this new [subprime] area of lending, Fannie Mae is taking on significantly more risk, which may not pose any difficulties during flush economic times. But the government-subsidized corporation may run into trouble in an economic downturn, prompting a government rescue similar to that of the savings and loan industry in the 1980’s.

The seeds of this crisis were sown a long, long time ago.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.