Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

This collapse in growth should not turn into a slowdown as severe as The Great Depression. The scale and pace of the authorities’ response has been astounding, and brilliant. We have done more in the last 6 months than the Japanese did in the first 6 years of their downturn, and we have avoided making the mistakes of 1929 when bank depositors lost their life savings, where taxes were hiked, rates kept high, and where fiscal contraction was preferred over Keynesian expansion. As David Smith of the Sunday Times put it, this is now a battle between King Kong and Godzilla – not a one-sided fight.

However, one thing still worries me, and might tilt that fight in the direction of Depression. Protectionism. In mid 1930, there were some tentative signs that the US economy was stabilising – but then the Smoot-Hawley Tariff Act became law. Going against both a huge consensus of economists (1028 of them signed a petition against the Act), and against the wishes of the President, two Republicans, Smoot and Hawley had huge grassroots support and managed to pass the bill imposing significant tarif hikes on imports to the US. According to Selwyn Parker’s excellent book The Great Crash, global trade effectively came to a standstill at that point and the global growth collapse resumed. Could the US be about to make the same mistake again?

The American Steel First Act would mean that only US manufactured steel could be used for any government project – a clear protectionist measure. On top of this, new US Treasury Secretary Geithner recently came out with this statement: “President Obama – backed by the conclusions of a broad range of economists – believes that China is manipulating its currency”. This could lead to US companies being able to seek import duties on Chinese goods. Could we be approaching our generation’s own Smoot-Hawley moment?

Let me start by restating our opposition to index investing when it comes to corporate bonds (we would say that, wouldn’t we). An equity index is an index of success – as the company prospers and its market capitalisation rises, its weighting in the index increases. Bond indices are buckets of failure. The more a company borrows, the greater its weighting in the bond index. If you follow a bond index, and a company within it doubles its leverage, making its failure more likely, you will have to increase your exposure to that company. Companies like Ford and General Motors were at one stage 23% of the European high yield market – today GM bonds trade at between 15 and 30 cents in the dollar. There is no more depressing sight in the world than a bond fund manager rejoicing in the default of a company because he or she was “underweight” the benchmark. If you don’t like a company, or even a whole sector, don’t invest in it. The index issue might soon become very important for high yield investors, as bank bonds continue to tumble.

We have been very clear on our views on Tier 1 bank bonds over the course of this credit crisis. These bonds just had their worst week ever, with prices down on average around 20%. A new Lloyds 13% Perpetual Tier 1 was issued at a price of 100 on Monday, briefly traded at a 2 point premium, before falling by 50 points by the end of the week, as nationalisation fears accelerated. One broker held a competition to see if this was the worst performance from a corporate bond ever (the “winner” though was a high yield deal issued in the last cycle where the issuing company had a major accounting fraud discovered on the weekend after issue, although at least in this case the sponsoring investment bank made investors whole, taking the loss themselves).

RBS has just had its T1 bonds downgraded to sub-investment grade (BB+ or below). This means that they will enter the high yield bond indices in February, and, when the rating agencies catch up with our internal ratings, there are likely to be many more bank bonds entering the high yield universe.

The European Tier 1 market has a value of Eur 40.7 billion, compared with the European High Yield market which is Eur 49.5 billion in size. On a worst case scenario, Tier 1 could therefore become 45% of the high yield market. This raises a lot of questions – not least, do high yield investors have the skills and appetite to invest in financial bonds (a very different animal to the usual LBO industrial and media names that are the mainstay of high yield investing). Also, will downgrades from investment grade provoke heavy selling from funds which are not allowed to hold high yield?

So more bad news for Tier 1 – but perhaps one crumb of comfort. The prices have fallen to such levels that for some bonds, the bank needs only to keep paying for 2 more coupons before an investor has seen a full return of capital. Whilst full nationalisation of some banks is a step nearer, governments are making it up as they go along, and there is obviously some option value to owning subordinated bank bonds at extremely distressed levels. Full wipe outs can still occur, but the risks are at least a bit more symmetrical at these super-distressed levels.

Dear Mervyn

I see from your speech last night that you might start buying corporate bonds. Now that the Bank of England and the authorities have entered the prime broking industry through (a) repoing securities with banks (b) buying equity stakes in banks, and (c) writing insurance on debt, this is the next step in the Nation State’s aggressive move into financial services.

In my experience, when buying corporate bonds, the most important thing is to do your due diligence. Obviously you have better information than anybody else on the state of the UK economy, but I would not rely only on the rating agencies for their credit views (you can see what a mess they have done rating UK banks).

With regard to your timing, I think it is very good. As you explained in your speech, corporate bond spreads are exceptionally wide on an historical basis (see previous blog here). Risk premia are at excessive levels, and all central bankers and their governments are taking appropriate action via lower base rates and traditional fiscal spending measures. The market is pricing in that you cannot save the day, but I think your and the government’s actions will successfully moderate the extent of the slowdown we are in.

Fund managers have to persuade investors to give them capital to invest on their behalf. You, however, can presumably finance your portfolio by issuing gilts or printing notes – wow ! Therefore not only can you invest in attractive corporate bonds offering excessive risk premia, but you can finance it easily, creaming off the extra yield while you wait for markets to normalise. This could prove to be a highly profitable exercise, as well as helping you to unblock the financial system by getting funds direct to the corporate sector.

By issuing gilts and buying corporate bonds, you would be both increasing the supply of gilts and increasing the demand for corporate debt (ceterus paribus). This will mean that corporate bond yields should fall relative to gilt yields, thus providing windfall gains to holders of corporate debt, who are prepared to take credit risk versus the more conservative holders of gilts. This is obviously a positive development for corporate bonds.

We look forward to seeing how you invest, and wish you luck in your day job of stabilising the economy and inflation. And I wish you every success as a fund manager.

Moody’s this week released their expectations for their global speculative grade default rate. Their default model is now (rather belatedly) indicating that there is to be a surge in defaults through this year, with the global speculative grade (ie ‘high yield’) default rate peaking at 15.4% in November 2009. Moody’s use a 12 month trailing default rate, so what they are saying is that 15.4% of the global high yield market will default in the year to the end of November 2009.

The thing that caught our eyes was the jump in Moody’s expected default rate. Only one month previously, Moody’s expected a peak of 10%. It’s worth adding, though, that November’s forecast appeared far too low, especially if you consider that as at the end of November, euro high yield bonds yielded almost 22% more than government bonds, and US high yield bonds yielded 20% more than Treasuries (both figures already implying roughly an annual default rate of 16-17%, and that’s assuming a zero recovery rate). In fact, the market doesn’t seem too bothered by Moody’s updated forecast – high yield spreads have actually tightened a bit since the end of November (the respective figures were 19% for euro HY and 17% for US$ HY as at yesterday)

How does a 15% annual default rate compare to the Great Depression? This chart shows Moody’s speculative grade default rate going back to 1920. The annual default rate peaked at 16.3% at the end of 1933, so not quite as bad. But the figures aren’t really directly comparable. The high yield market didn’t exist as such in the 1930s – companies that were rated sub investment grade were ‘fallen angels’, ie companies that were formerly investment grade. Junk companies only started issuing bonds en masse during the Milken years of the 1980s, and the European high yield market didn’t start developing until the mid 1990s. A better comparison would be the default rate seen in the early 1990s and particularly 2001-02. We concur with Moody’s that default rates should exceed those levels.

But remember, high yield spreads are massively wider than they were in the 1990s and the early ‘noughties’. The high market is already pricing in a default rate significantly higher than Moody’s is expecting. We are seeing some attractive valuations in the high yield market, and are chipping away at the better quality end where mandates allow. However we do expect defaults to surge, and particularly from the end of 2009 when a lot of high yield names need to refinance. We also expect defaults to be concentrated in companies that were LBOd in 2006-07 and in cyclical names, and defaults will be very heavy in the poorer rated names (so CCC rated bonds are still basically a no go area for us).

Finally it was interesting to note the Chapter 11 filing of Nortel this week, which was an event that bond markets had priced in since November. Nortel is a company that survived the 2001-02 tech wreck, but hasn’t made it this time. This is a good example of why we aren’t piling into high yield right now. We remain very bearish on the global economy, with the recession/depression likely to be worse than the early 1990s and obviously much worse than the non-recession of 2001-02. The high yield market hasn’t ever been tested by a 1981-82 recession or a 1974, nor even a 1932. So maybe two thirds of the high yield market really could go bust in the next five years (which is about what the bond market’s actually pricing in). That said, if you can avoid the companies that do default, then the potential returns are clearly considerable.

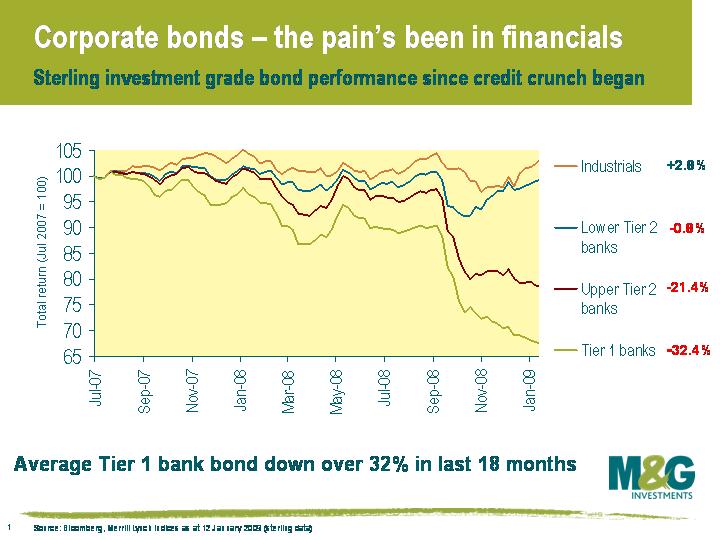

As our regular readers will know, we have been tracking Tier 1 (T1) capital’s fall from grace since last August. Unfortunately for these bank bond holders, the picture has not improved this week, with S&P and Fitch widening the notching between senior and hybrid debt on a number of European banks. This is because in their view (which has also been the long held view of our analysts) the risk/reward characteristics of these securities are becoming more akin to those of equity than debt. It feels as though the wider market is coming round to our way of thinking. This is significant because any further credit rating downgrades on T1 bank bonds will cause these bonds to drop out of investment grade indices, leading to more investors becoming forced sellers, and driving prices even lower.

Here is an update of the chart Richard used in his October 3rd blog. It shows that T1 has fallen even further since Deutsche Bank’s decision not to call a Lower Tier 2 bond in December; the average T1 bank bond is now down over 32% since July ’07. If more banks’ T1/UT2 ratings are cut things could get even gloomier.

If you would like more information on hybrid debt, or Deutsche not calling its LT2 bond, it is worth taking a look at last month’s blogs by Mike here and from Jim here.

Some pretty horrendous looking data came out of the Eurozone this morning. While the GDP and unemployment numbers were in line with expectations (Q3 GDP was confirmed at -0.2% and unemployment rose to a two year high of 7.8%), the business and consumer confidence numbers were horrific. Economic confidence fell to a record low and consumer confidence was the lowest since records began in 1985. Exports from Germany tumbled 10.6% in November, which was also the biggest drop since Germany was reunified in 1990. This data comes on top of yesterday’s economic data release showing that European producer prices in November fell the most since 1981, suggesting a severe risk of Eurozone inflation undershooting the ECB’s 2% target in the coming months.

The ECB suggested last month that it was going to adopt a ‘wait and see’ tactic, hinting that Eurozone interest rates would remain on hold at 2.5%. But data this week suggests that things are deteriorating faster than the ECB thought a month ago, and interest rates will have to fall further. Eurozone rates should be cut on Thursday next week, and rates should be cut further thereafter.

The start of another year is always a time to take stock, reflect on the last year and plan for the next. Last year was dramatic from an investment point of view, with equity markets having their biggest bear market since the great depression (and credit markets doing even worse) while government bond yields collapsed to post war lows.

All the way through this crisis we have focused on the strength of the housing market as a lead indicator of what is to come for financial markets and the broader economy. We have been joined in our observations by the policy makers, with the US Federal Reserve giving further detail last week over its plans to buy $500 billion of mortgage related debt by mid 2009. This is designed to drive the cost of mortgage debt down, so helping the US housing market. A similar response is being sought in the UK, where base rates have never been lower since the Bank of England was founded in 1694 (and rates are set to go lower still).

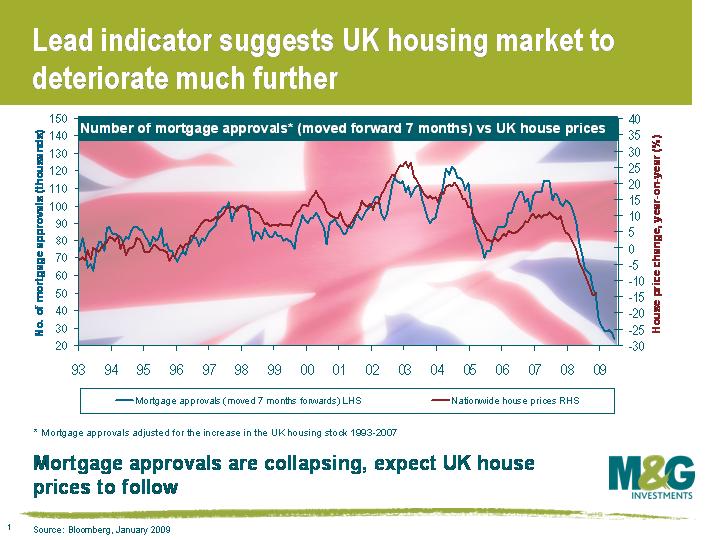

In the UK the lead indicator we have focused on has been the level of new mortgage approvals (see previous comment here), which indicates the upcoming buying power entering the UK property market. The latest numbers were released on the 2nd January, and the record low number continues to point to further weakness, as illustrated in the chart.

So the crisis has unfolded, a policy response is in place, but when will the economic animal spirits come back to the fore, watch this space…

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.