Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

We wrote about our January research visit to the States in our recent Letter from New York, but whilst we were there we also took along a £75 video camera and shot a few clips.

Bond Vigilantes – New York research trip – January 2009

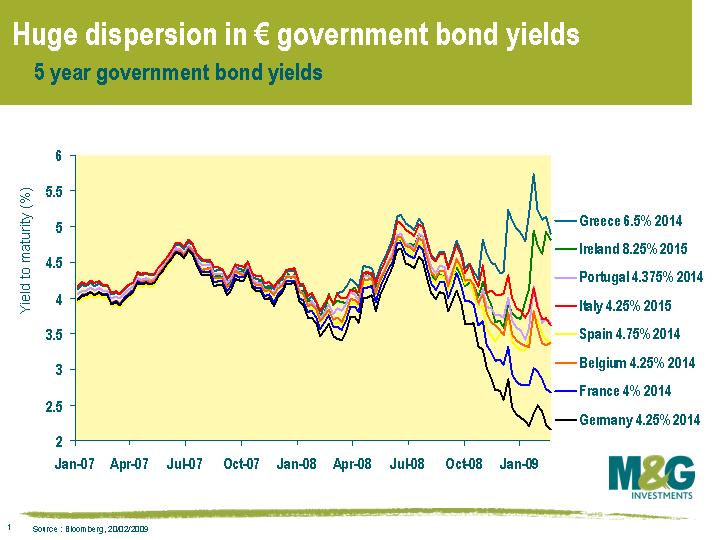

We first talked about cracks appearing in Euroland in June, and expanded this to include emerging market government bonds in October. Over the past few months, the trend of rising sovereign default risk has accelerated, and particularly in Europe where we’ve seen downgrades to the sovereign debt of Greece, Portugal and Spain. It’s probably a matter of time until the UK follows. In today’s environment, what can you define as ‘risk free’?

The attached chart shows the yields on a selection of euro denominated government bonds. At the beginning of 2007, a Greek government bond maturing in 2014 yielded only 0.15% more than a German government bond with a similar maturity. Now, the German bond yields a shade over 2%, while the Greek bond yields almost 5%. Bearing in mind that even German government bonds have an element of credit risk, perhaps as much two thirds of the Greek government bond yield is compensating you for the risk of default.

It’s slightly harder working out how much credit risk there is on a 5 year gilt, because it’s obviously not issued in euros. But if you look at the credit derivative market, the 5 year CDS on UK government bonds is about 165 basis point (so, if you wanted to insure £100,000 of gilts for 5 years, you’d earn £1,650 per year). According to the credit derivative market, there is a slightly higher risk of the UK government defaulting than for Belgium (rated AA+), Spain (rated AA+) and Portugal (rated AA-), though not quite as high as the default risk of Italy (rated AA-). Cash bond yields often don’t quite tally with the default risk implied by derivative markets, although yesterday Portugal issued a government bond where the two did match up. If you assume that the credit risk implied by the CDS market is correct for UK gilts, then of the 2.6% yield you can get on a five year gilt today, more than half of this yield is now credit risk.

Could we get to a situation where corporate bond yields are lower than government bond yields for the better quality corporate issuers ? This is already happening in the case of Greek government bonds – investors now need to analyse Greek government bonds and ask whether they should lend money to the Greek government for 5 years, or for a very similar yield and a maturity, should they buy euro denominated bond issues from Vodafone, Carrefour, BHP Billiton, Deutsche Telekom or Diageo? If the UK economy deteriorates much further then there is no reason that the same thing can’t happen in the UK. It could even happen in the US, Germany or France, particularly if you consider the ugly technical picture that could result from the huge amount of government bond issuance that will be necessary over the coming years.

Bond investors and citizens typically consider their respective governments to be their safe haven. However, within the Eurozone investors are confronted with a choice of safe harbours beyond their national borders. Therefore risk averse capital will tend to flow into the perceived safest harbours at the expense of others. This understandable reaction in difficult times begins to become self fulfilling as a flow of cash from one to the other makes it relatively safer.

Recent months, not entirely unexpectedly, have seen increasing speculation that the Euro may see one or more member states depart for a variety of reasons. This in itself deserves a separate blog and I’ll do my best to pen something in the near future. For now, lets just say that although it isn’t our core scenario, such an outcome shouldn’t be discounted.

The team has just watched I.O.U.S.A., the film about the future American disaster brought about by unbalanced government budgets (Dick Cheney: “Reagan proved deficits don’t matter”) and, in particular, unfunded Medicare and Social Security liabilities.

We’re giving away our copy of the DVD. To win it, send your answer to the following question to bondvigilantes@mandg.co.uk. The first correct answer we receive gets the film.

What happened when Dick Cheney went quail hunting in February 2006?

On the day that the Bank of England started its Quantitative Easing (QE) regime with the purchase of £340 million of commercial paper under the Asset Purchase Facility, it’s worth remembering why our blog is called Bond Vigilantes, and ask ourselves whether we need to be baring our teeth a little more.

The term Bond Vigilantes dates from the bond market’s aggressive response to President Clinton’s attempt to increase the US budget deficit in the 1990s. The Treasury Bond market selloff (leading to rising financing costs for the US) helped to persuade the administration to balance the budget. Clinton’s political adviser at the time, James Carville noted “I used to think that if there was reincarnation, I wanted to come back as the president or the pope or as a .400 baseball hitter*. But now I would like to come back as the bond market. You can intimidate everybody”.

I would want to come back as Brad Pitt.

Well, with the collapse of the global economy, budget deficits everywhere in the world have been allowed to expand to almost unheard of levels. Government borrowing in the UK will be about 8% of GDP in the next year, the highest in recent history (it hit 7.7% in 1993-94) and our debt to GDP level is quickly heading north of 50%. The Office of National Statistics has declared that the liabilities of the nationalised and part-nationalised UK banks will have to be added to the UK’s balance sheet, so we could be nearing 100% pretty imminently. At the same time, the Bank of England is starting to print money and central banks everywhere have added to the government’s fiscal stimulus packages with a huge amount of monetary easing (zero interest rate policies). All of this should, on the face of it, be really bad news for investors in government bonds. Fears of a never-ending supply of government bonds, and stories that hyperinflation is on its way, have made many bond investors fearful.

So a good bond vigilante really needs to take a step back from the consensus view that we are going to see a year of weak inflation (perhaps with a period of mild deflation) and then there’s a chance that it’s Zimbabwe here we come. So what are the theoretical drivers of inflation, and is it possible that the consensus could be very wrong this time?

Are you a monetarist or a Keynesian? Monetarist Milton Friedman popularised what is known as the Quantity Theory of Money. In short, the theory simply reflects the idea that if you print more money, the value of that money is reduced proportionately to the amount of money printed. The equation he used was MV = PQ, where M is the amount of money in circulation, V is the velocity of money, P is the price level and Q is the total number of items purchased with the money in circulation. The important thing to note is that there is more than one determinant in the generation of inflation in the economy – the quantity of money is very important, but a rise in this quantity can be offset by a fall in the velocity of money. If money stops moving around the economy (because individuals, banks, and companies are hoarding it) then printing the stuff won’t generate inflation. This spreadsheet here allows you to plug in some numbers of your own to estimate what might happen going forwards – I’m using column C, which allows you to input all factors other than inflation. Thinking about the last year, let’s say that the broad money supply grew by 17.5% (M4), the velocity of money remained unchanged, and the quantity of goods sold rose by 4.3% (volume of retail sales). This results in annual inflation of 12.66%, but UK CPI in 2008 ended at 3.1%. What change in the velocity of money would therefore result in the actual inflation rate? The answer is that a fall in the velocity of money from 5 to 4.575 results in inflation of 3.1%. This is a slowing in the speed of money going around the economy of 8.5%. Assuming that the other factors remained the same, a decline in the velocity of money of 11% would have lead to zero inflation, and anything greater to outright deflation. It therefore follows that even printing money, and doing Ben Bernanke style helicopter drops of dollar bills over the population can’t generate inflation unless we go and do something with that cash.

For the Keynesians, I present the output gap theory. The output gap is the difference between the potential growth in an economy (based on factors like demographic growth in the labour market and productivity improvements) and the actual growth. When an economy is growing below trend, it is difficult to generate inflation – too many out of work employees are chasing too few vacancies, and wage growth is stifled. Unused factory capacity, high stocks of inventories, going out of business sales and empty buildings also keep the lid on inflation. Our favourite economist, Paul Krugman published his analysis of the US output gap and its impact on inflation on his NY Times blog a couple of weeks ago. For every 1% that actual growth falls below potential growth, the inflation rate is reduced by 0.5%. The US Congressional Budget Office is saying that the output gap will be 6.8% over the next two years, which means that the US is staring at a period of deflation, even if you assume that President Obama’s fiscal stimulus fills in a third to half of that growth shortfall.

Finally, thinking back to the UK’s last period of fiscal indiscipline – the 1993 budget deficit of 7.7% – did the gilt market collapse? Well no. 10 year gilt yields fell from 9.7% to 6.1% – a gigantic rally. A selloff did come, but not until the next year, when the Fed hiked rates – something clearly (and explicitly) not on the cards for some time to come. Vigilant yes, panicked, no.

* Note for non-US readers, I believe that .400 is a good batting average in a version of the game that we know as rounders.

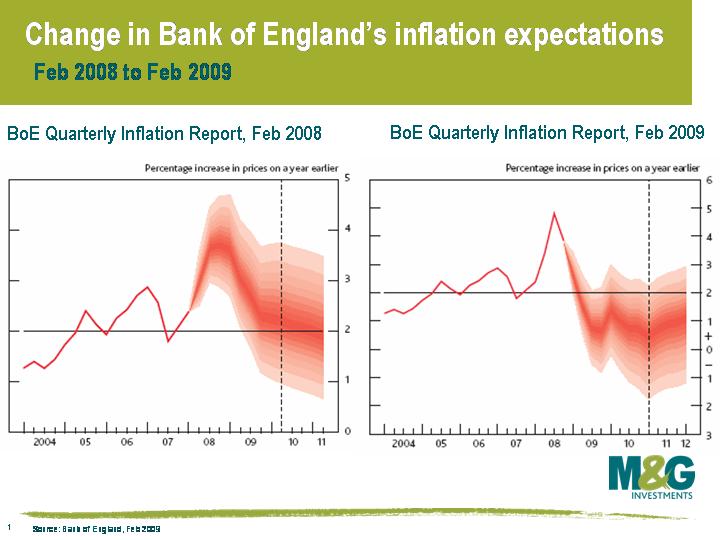

Most of the press coverage of the Bank of England’s inflation report centred around Mervyn King’s comments that the UK was in a ‘deep recession’. That’s hardly controversial any more – for me, more interesting was the fan chart depicting the Monetary Policy Committee’s best collective judgement of where inflation is heading in the next three years.

The attached chart shows how the BoE’s inflation expectations have changed from a year ago. Inflation expectations are displayed as a fan, where the MPC has 90% confidence that inflation will fall within the band. In February 2008, its central forecasts were for UK inflation to remain slightly above 2% target two years later, given the market’s interest rate expectations at the time (which was for UK interest rates to fall to about 4.5%). The MPC believed that there was a 5-10% chance that UK inflation would fall below its 1% lower limit by 2010.

Since the summer, the BoE has been steadily adjusting its inflation expectations downwards. While its core scenario is still for CPI inflation to remain above zero, it estimates that there is about a 1 in 5 chance of deflation in the UK – not just this year, but at the end of 2011. And this is taking the market’s current interest rate expectations, which are for UK rates to stay close to 1% for the next three years.

The MPC’s models have come in for some criticism lately, from three former MPC members no less (see here), but when the guys who actually set interest rates think there’s a very real risk of entrenched deflation (which is something that we’ve been arguing for over a year on this blog), you ‘d be foolish not to take note.

The MPC’s models have come in for some criticism lately, from three former MPC members no less (see here), but when the guys who actually set interest rates think there’s a very real risk of entrenched deflation (which is something that we’ve been arguing for over a year on this blog), you ‘d be foolish not to take note.

It’s been a very long while since the leveraged loans team last did anything on the blog, so here’s an update of where we see the market.

The first thing to point out is that while high yield bonds have started the year with a 10% rally (perhaps making up for the lack of a ‘January effect’ last year!), loan returns have been broadly flat. For the past 18 months, the loans market has been dominated by technicals (ie forced selling) rather than fundamentals, although a clear sectoral bifurcation is emerging – the more cyclical, economically-sensitive areas such as industrials, building materials and chemicals have underperformed those such as cable, healthcare and telco. A credit is doubly favoured by the market if it also happens to be liquid, carries a high coupon and has a high rating. If it ticks all these boxes, then it is seen as attractive to structured credit buyers such as CLOs, and will generally be trading at a 20-point premium to the rest of the market.

Investors’ preference for earnings visibility is unsurprising given the number of credit shocks and other unforeseen outcomes over the last two months. It is unarguable that the long anticipated default cycle is starting, with the US in the vanguard. By value, 4.9% of the US loan market has defaulted in the last year, but the pace has accelerated sharply. In December and January, 3.2% of loans defaulted, the highest two-month period on record, beating the 3.1% posted in May-June 2002.

Thirteen European issuers (five in December, eight in January), representing approximately €9 billion of debt, have defaulted or gone into restructuring. Some were anticipated – UK homebuilder McCarthy & Stone, for instance, while others – eg Italian yacht maker, Ferretti – were more of a shock. German auto parts manufacturers have suffered particularly heavily as it appears that their balance sheets have been strained to breaking point by working capital outflows. So we expect that 2009 will see low levels of new business and high volumes of restructuring as the scarcity of credit and global economic slowdown feed on each other.

Two other trends are worthy of note. First, banks are clearly retreating from capital-intensive businesses like leveraged finance; second, in today’s volatile, non-par market place the practice of using leverage within structured vehicles is untenable. The vacuum from the traditional buyers of loans is being filled by allocations to credit from risk-tolerant, unleveraged investors with longer time horizons; anecdotal evidence suggests that the inflows we are seeing into loans are being replicated elsewhere in the fixed income world.

As always, for institutions looking to invest, the European loan market lacks transparency – there are few public ratings (the bank-dominated European market did not require them), information is generally non-public and insolvency regimes vary widely. But these concerns need to be balanced by the fact that average spreads to maturity are in excess of LIBOR plus 10%, which we believe overcompensate investors for the risks.

Yesterday the Bank of England cut rates by 0.5% to the new record low of 1%. The problem that the BoE now faces is that it’s reaching the end of its effective use of traditional policy. Theoretically rates could be set below zero at a negative rate, by charging banks to deposit their cash. However, faced with a negative rate on savings, banks and individuals would simply invest in a safe, and store their cash at no cost. To overcome this the BoE could (again, in theory) create bank notes that fall in value, or expire as legal tender on a set date. Theoretically possible, practically impossible.

So, if the appropriate policy rate is -1% rather than +1%, what can the BoE do? Firstly, if it thinks a negative rate is required the best it can do is cut rates quickly (which it has), and get them to the limits of its policy bands (lets say 0%.) Secondly, as it isn’t able to generate an appropriately negative rate for a short period of time to shock the economy and inflation back into life, it will have to compromise, by keeping rates low for longer. Not the perfect policy response, but the best it can do.

If the market doesn’t believe that the bank rate is going to be held low for longer, then the bank can work with the authorities to drive rates lower along the yield curve. It can do this by intervening in the money and government bond markets, thus providing a low risk free rate benchmark for months, and maybe years.

The next problem the bank faces is setting the real economy market rate that banks, corporates and individuals will actually lend to each other at (ie the non risk free rate). The BoE recognises that traditional policy isn’t working, and is proposing to act as a buyer of, for example corporate debt (see my blog from last month), while the government has provided equity and credit insurance to enable banks to borrow in these difficult real world conditions. These measures combined are being proposed to limit the damage caused by the credit crunch. If they work, fine. If not, more of the above will be attempted, and UK base rates will stay very very low, for very very long.

Perhaps we shouldn’t have expected to come away in anything but a deep depression from last week’s research trip to see strategists and economists at Wall Street’s investment houses, after all this is the epicentre of the job losses and zero bonuses. At times though, there was a real background hum of anxiety – about their own personal prospects, about the economy and about the future of banking. Somebody once pointed out that the plural of anecdote is not data (except in homeopathy) – but one of the strategists we talked to has bought a gun, in case things get really bad, and one of our flights from London to New York had just 38 people on it.

First then, the banks. Whilst we were there, equity markets had a burst of excitement over talk of the creation of a “bad bank”. But estimates of the size of the “bad” asset pool grow day by day. As one bank analyst put it, there’s $4 trillion of bad assets out there, before you even start thinking about commercial property – so the market’s going to tank if the bad bank is worth only a $1 trillion bailout. (And as a friend who works for a now partly state owned UK bank put it, “why do they want to set up a bad bank? We are the bad bank. They’ve already got one.”) There is a chance that subordinated bank bonds could be rescued by the authorities in the UK, as to allow them all to default could have systemic implications for pension funds and other institutional investors who have significant holdings of the instruments. In the US though, this is not the case – their subordinated bank bond investor base is more speculative in nature (hedge funds, distressed debt players). Bank common equity is now regarded as having only option value, and with no systemic risk, losses can be pushed right up the capital structure. The American public wants to see bank investors (and employees) get punished. The most likely mechanism for this would be through a series of debt exchanges – Upper Tier 2 bonds would be offered terms to convert into Tier 1, and Tier 1 would be offered terms to convert into common equity. Why would investors do this? Well the alternative might be immediate bankruptcy, and the pill would be sweetened with better than current market terms (if you are a distressed debt investor who bought a Tier 1 issue at a price of $45, and you get offered $55 worth of equity, you might well accept). This form of “voluntary” restructuring would not count as an event of default, or trigger CDS contracts, nor would it be seen as the state over-riding the law – President Obama lectured law at Harvard, and the market believes this means that he regards existing property and contractual rights as paramount.

“Regulatory forbearance” is the phrase du jour. There is an argument that the problem isn’t the bad debt, it’s the recognition of bad debt. In a few years time we’ll be through this economic nightmare, and house prices will recover and toxic loans could well end up being money good (the Swedish state actually made money from such assets when it bailed out its bust banks). Why not then keep them marked at 100 on the portfolio, and only mark them down if they actually default rather than showing the low mark to market valuations which are due as much to forced sellers of risky assets as to credit fundamentals? That’s what the US banks did in the 1980s following the Latin American debt crisis, when they were, like now, insolvent. This would allow the banking sector to limp through the next few years, gradually repairing their balance sheets. But under this model they couldn’t start lending again and doing new business – the velocity of money would continue to fall even as the money supply rises, and a prolonged period of Japanese style deflation could ensue. Only “good”, well capitalised and properly solvent banks can facilitate a return to the normality of the lending of the past two decades (if you think that’s desirable). And in the meantime you have to bypass the banking system by putting taxpayer and Treasury Bond investor money directly into the hands of US consumers and businesses.

The Obama stimulus package was coming under a lot of scrutiny whilst we were there. Obama said yesterday that it would be a catastrophe if the Senate doesn’t pass the package quickly – it has has risen from $800 billion to $900 billion in the past week (and now totals 7% of GDP). The original bill had a strong focus on education and transport, and longer term infrastructure projects, but the Republicans want immediate tax cuts which they argue will act much more quickly in stimulating the economy. Away from the package, other ideas for bypassing the banks to get cash into the pocketbooks of Americans included a wholesale cutting of mortgage rates from (effectively state owned) Freddie Mac and Fannie Mae – by cutting mortgage rates from over 6% now, to under 4%, whilst being able to finance those loans by issuing government bonds (yielding around 3%) the government would be able to confer the benefits of the flight to safety in the bond market to homeowners.

Were there any rays of sunshine? Perhaps – at least a couple of economists (Larry Kantor of Barclays, and I see today that the historically very bearish David Rosenberg of Merrills has joined him) are predicting a significant US growth rebound in the second half of 2009. Partly this is due to some rebuilding of inventories after the expected violent destocking of Q1 and Q2, but also there is some expectation that the monetary and fiscal stimulus packages will have had an impact by then. There was also some excitement about the prospects for an early recovery in Asia – particularly in China which announced its own stimulus package (3.5% of GDP) and where direct state control of the banking sector means that lending volumes can be maintained.

We usually visit the Fed when we are in New York – and we did this time too, although we did it as tourists rather than investment managers. You can prearrange a free tour, which includes some exhibitions (including a display for kids which included a 4 page multicoloured book featuring cuddly animals and called “How the Federal Reserve Regulates Banks” which would have made a good photo had our cameras not been confiscated), the screening of an education film about banknote distribution (“Hi, I’m Troy McClure. You may remember me from such educational films as “Lead Paint: Delicious but Deadly” and “Here Comes the Metric System””), and best of all a trip down to the bedrock of Manhattan to see the gold vaults. There’s more gold there than at Fort Knox – $180 billion at today’s prices – but in a fairly small store room. I’m not convinced the stuff should have any value, other than for making trinkets.

Finally inflation. Deflationists hold sway, at least for the short term. There can be no return of inflation until credit demand returns, and we remain deeply in a world of deleveraging and recapitalisation, both on a personal and a corporate level. However, although we were only able to yell a hurried question to the barkeep from the window of our still moving cab back to JFK, it seems that a can of Pabst Blue Ribbon in Welcome to the Johnsons has risen to $1.75, from $1.50 in the autumn and $1 a year ago.

US auto sales for January came in below estimates at a seasonally adjusted annualised rate (SAAR) of 9.57m units. The figure, the lowest since 1982 was down from 15.4m last year and saw a dip below the psychologically important 10m reading. Whilst the European and Asian manufacturers were hurt; the US big three, GM, Ford & Chrysler were once again the notable underperformers witnessing their sales volumes fall by 51%, 43% & 56.5% on the same period last year.

The US manufacturers face huge challenges. Inventories remain high with consumers continuing to defer purchases of discretionary items. A poor product mix coupled with legacy healthcare and pension issues remain. Beyond that working capital requirements are consuming already decimated cash balances at record speeds and capital markets remain closed (long dated GM bonds trade around 15 cents in the dollar).

We remain deeply sceptical of most auto manufacturers with even the stronger European players now coming under ratings pressure. The development plans that the US manufacturers must present to politicians on Feb 17th will be one to watch.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.