Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

Over the past week or so we have seen an interesting development in bank bonds as around a dozen institutions across the UK and Europe have announced that they are tendering for their subordinated debt. Essentially this means they are offering to buy their bonds back from investors. Bank sub debt is usually issued with call dates (typically after 10 years) when the issuer can either repay the bonds, or extend their life and suffer an increase in the coupon rate. Banks have historically been expected to call their bonds at the first call date and there was a huge outcry in the market when Deutsche neglected to call a Lower Tier 2 bond back in December (as Jim documented here). The other extremely important feature of this type of debt is that the issuer can choose to skip coupon payments if they’re not paying an equity dividend, and this does not count as a default as it would with any other type of bond. So, firstly, tendering for the bonds makes sense from the issuers’ perspectives because it means they avoid having to decide whether to call the bond or to skip coupon payments. Although it might make sense from an economic perspective to not call the bond, and to skip interest payments, such action could potentially be very damaging to their reputation and ability to raise finance in the future. Secondly, tendering for the bonds also means they no longer have to pay out to service the debt. These two concerns are the main short-term drivers for wanting to buy back bonds with these options in them.

But what is really going on is this. Bank subordinated debt has been languishing for some time now. Banks can buy back 100p worth of their subordinated bonds at a premium to their current price to persuade investors to let them go, and yet generally only have to pay 40p to 50p in the pound (because they have been priced at 20p to 40p). And what this means in accounting terms is that, for example, cash has fallen by 40p for the bonds they buy back, and liabilities have fallen by 100p. The net result of this on capital is that the bank has a 60p ‘gain’, which goes straight into core equity, into the retained earnings account. And this is the highest quality form of capital. So investors make a small and quick profit, and the bank gets a very big boost to core capital. A further positive is that the banks can buy back Tier 1, Upper Tier 2 and Lower Tier 2, which are all different types of ‘hybrid’ capital, and get an accounting boost to core capital, which these days is the only type of capital that anyone cares about.

For the past few months there has been virtually no liquidity at all in subordinated debt. The only bonds changing hands were the cheapest, because for 10p you could buy 100p of bonds…it was basically option value. Now, though, there is at least some liquidity, and to that extent these buybacks are a positive for everyone. The news has led to a small rally in subordinated bank debt , but is not significant taken in the context of the past six months or so, during which period deeply subordinated debt has returned around -60%.

So at what prices are they offering to buy these bonds back? Well, prices vary from instrument to instrument but in all cases are significantly below par value, so those taking up the offer will be locking in substantial losses if they bought at anything other than distressed levels. By accepting 40p or 50p for their subordinated bank investments, investors are giving the banks equity (as explained above), and, although it may be happening in a different guise, this is a clear equitisation of bank capital securities, something that we recently argued was highly likely (as I wrote here). Investors seem to be willingly crystallising principal losses on their bank debt to exit the investments. From the banks’ points of view, these exchanges are the direct equivalent of buying back subordinated bonds for 40p in cash, plus the remaining 60p in equity. But in these exchanges, investors don’t even get the upside potential from the equity. Many have long been arguing Tier 1 is really worth 100p in the pound. We still don’t think it is.

Investors have been buying corporate bonds as a savings vehicle for a number of years in the UK, however yesterday they were joined by the oldest lady of them all – the Bank of England. The BoE yesterday commenced its investment programme by buying £85.5 million of sterling corporate bonds.

The reasons why she is doing this are (1) to improve liquidity in the UK corporate bond market; (2) to reduce the cost of borrowing for companies with significant business interests in the UK; and (3) to supplement the quantitative easing they are doing through gilt purchases.

This is obviously going to be beneficial for corporate bonds, at least in the short term, because increased liquidity and buying of the asset class should help its performance. Within the corporate bond sector, they are aiming their firepower at better quality, non-bank issuers. These bonds are obviously going to benefit most from this buying programme.

This buyer is not however the usual little old lady. This one owns a magic purse containing many billions of pounds courtesy of her right to literally print money. On the first day the purchase programme she took out £85.5 million of bonds. The plan is for every Tuesday through to Friday of every week to repeat this exercise (not sure what’s wrong with Monday, maybe it’s washing day). Therefore one might expect buying of roughly £350 million a week. To put this in context, her investment grade bond fund at this rate will be over £4bn in size by the end of June, probably making it the largest corporate bond fund in the UK retail universe. In January, according to the Investment Management Association (IMA), retail investors put a net £1.4bn into sterling investment grade corporate bond funds, so in relation to current flows, this old lady will be roughly doubling demand.

As a corporate bond investor, this action is obviously going to have a significant influence on the market place. From the Bank of England’s point of view, we will have to see how successful she will be through this bond buying programme, though given her cost of finance is zero and she is buying bonds at attractive yields, it might turn out to be quite a profitable exercise if she is a long term investor.

Central bankers passionately love inflation-linked bonds. Firstly, they keep governments honest by discouraging them from generating inflation in order to reduce their debts, and secondly they provide real “put your money where your mouth is” information as to where the financial markets think inflation is heading. Unfortunately, the Bank of England’s new QE regime makes the information derived from index-linked gilts useless – and in a perverse way too.

Just at the time when everybody is worrying that QE is the first step on the road to the issuance of Zimbabwe style One Hundred Trillion Dollar notes (I have one in front of me as I type, the watermark is a picture of a buffalo’s backside), we’ve seen a collapse in the expected future level of inflation in the UK, according to the gilt market. In February, before the Bank’s QE announcement, the 10 year breakeven inflation rate was just below 2.5%. It subsequently halved to 1.25%. In other words the bond market expected half the level of inflation over the next ten years than it had before the Bank turned on the printing presses. As I said, perverse.

The problem is that the Bank’s QE programme only targets ordinary gilts (£75 billion of them). Index linked gilts are excluded (for liquidity reasons) and have therefore missed out on some of this big rally. Conventional gilt yields have therefore fallen further, and dragged down the breakeven inflation rate (the difference between nominal (conventional) and real (index linked) yields). This is probably an unintended consequence – but in so far as this “information” is used by wage setters and policy makers, might it in itself prove deflationary?

Since the height of the QE driven conventional market rally, linkers have caught up a little (the implied inflation rate has risen to 1.75%) – but the fact remains, if QE excludes linkers, then the information contained within their prices will become less valuable. Perhaps this is why the Bank has recently placed more emphasis on survey data (the Bank of England/GfK NOP Inflation Attitudes survey) when they talk about future inflation expectations?

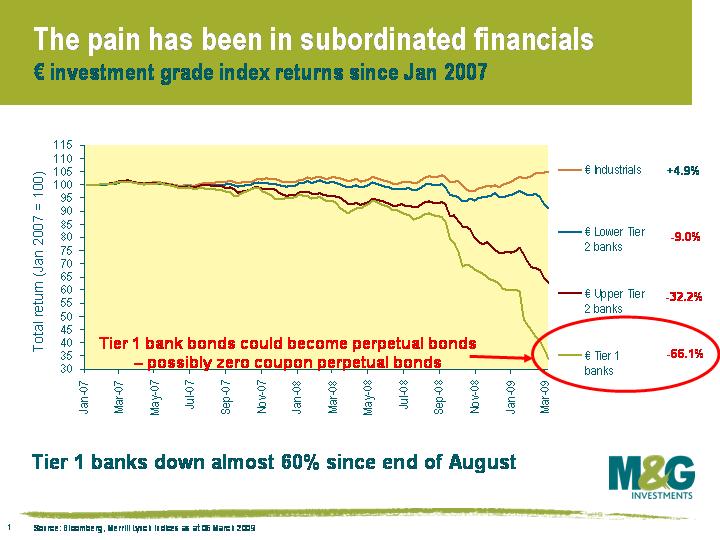

The somewhat bizarre title owes to the fact that euro and sterling bank tier one securities (the most subordinated and equity-like ones) are now priced roughly between 18 cents in the euro, or 18p and 30p in the pound! We have discussed these bonds at length in previous blogs (see the most recent comment from Jim here) and have outlined the reasons for their being a very high risk way of taking exposure to banks. Nonetheless, the decline in the valuation of these subordinated bonds has been both fast and brutal, accelerating further this year so far (see graph). I thought I’d take a moment to briefly draw attention to a few of the relevant events that have taken place in recent weeks and that relate to bank bonds.

The somewhat bizarre title owes to the fact that euro and sterling bank tier one securities (the most subordinated and equity-like ones) are now priced roughly between 18 cents in the euro, or 18p and 30p in the pound! We have discussed these bonds at length in previous blogs (see the most recent comment from Jim here) and have outlined the reasons for their being a very high risk way of taking exposure to banks. Nonetheless, the decline in the valuation of these subordinated bonds has been both fast and brutal, accelerating further this year so far (see graph). I thought I’d take a moment to briefly draw attention to a few of the relevant events that have taken place in recent weeks and that relate to bank bonds.

The End of Contract Law?

The first hammer blow to the industry took place recently when Her Majesty’s Treasury announced that Bradford & Bingley’s lower tier two bonds (a senior-ish type of capital security that should pay you interest and principal in all circumstances other than wind-down, in which case you probably get nothing) could now defer interest and defer principal. Or in other words, it can default, without actually being an event of default. HMT had in effect torn up the rule book and subordinated the lower tier 2 bonds to the ranking of preference shares. The markets, quite predictably, took this to mean that the contracts that exist between issuers of bonds and investors, and that form the basis for the investment in the first place, were now not worth the paper they were written on. All bank capital notes, and especially lower tier 2, which had thus far held up relatively well, went into freefall again.

And then some urgent back-peddling!

6 days later, with the lower tier 2 market still frozen, and with tier 1 securities shacked up in the 18-30 territory, Lord Myners released a letter of intent stating that the Bradford & Bingley action had only come as a result of its being a ‘special case’ – ie being in wind-down. He explicitly stated that going forward, and in regards to banks that remain ‘going concerns’, banking powers “do not provide for the modification of the terms of contracts (including subordinated debt instruments) of a banking institution”. The significant and widespread negative reaction to the original change of ranking had warranted an urgent response to quash market fears. And market sentiment improved, but recovered only part of the ground lost on the above news. So, thankfully, the sanctity of contract law remains in place in the UK. For now. At least for banks that remain ‘sufficiently’ free from government control. Our belief and fear is that we may not yet have heard the end of this issue.

Dresdner tier 1 principal loss participation

Bank tier 1 notes in Germany generally have loss participation clauses in them. These state that in the event of erosion of balance sheet reserves and a balance sheet ‘loss’ (which is loosely defined within each bond’s prospectus but is roughly a loss for the year), then the tier 1 securities can have their principal written down. Tier 1 bond investors therefore share in the losses that equity holders will also have borne. The actual figure for the writedown of the value of Dresdner’s tier 1 bonds has not yet been released, and will be determined between regulators and some overly-complex formula, but this announcement and realisation gave the markets another cause for alarm. It is worth remembering that in the tier 1 market every domicile, every issuer and every individual bond has extremely important differences. Buyer beware! In the bull market it felt like the engineers of these capital products had achieved the remarkable feat of getting regulatory capital for banks whilst giving the bond holders a bond product. As we work through this bear market, though, it feels more and more as though the engineers have manufactured a product that could be sold as a bond, but which in actual fact is equity.

Citigroup conversion

Citigroup released another set of ugly results last Friday, and has now lost somewhere in the region of $80 billion dollars so far this cycle (see WDCI screen on Bloomberg for a full list of bank losses). It announced that dividends will be ceased on common and preferred stock. Now at first this doesn’t sound too surprising, given the scale of losses. But we here at Bond Vigilantes just wonder if there may be the beginning of a trend somewhere in here. Banks don’t have enough capital for their leverage and their bad loans. Still. And confidence in the banking sector must have a very positive correlation with bank capital. So the first round of getting more capital was rights issues to existing shareholders; the second round was government injections of preference shares; and the third round is Citigroup (and RBS and Lloyds) having their government preference shares exchanged for common shares. Now, if the third round proves to be insufficient, what next? We wonder whether in certain particularly troubled names, certain classes of capital securities are exchanged for common shares. The Citigroup action last week suggests we are closer to this stage than one might have thought.

RBS and Lloyds Re(re-re) Capitalisation and Asset Protection Scheme

Along the same lines, Lloyds (or perhaps more accurately, HBOS) and RBS announced awful numbers. So the government is adding to its existing investment in part through converting the preference share investments and in larger part by injecting ‘near-common’ stock called class B shares. These shares were carefully invested below existing preference shares and above common stock so as to avoid another huge sell-off in bank capital securities: if the government had subordinated capital securities by investing above them, then the message would have been taken to mean that losses were even more likely than before on these subordinated classes of notes. The B shares have non-cumulative dividends of 7% and convert to ordinary stock when/if the share price has rallied above a certain price. Whilst this action can be taken as an immediate positive, since everything is being done to avoid nationalisation of the banks, it also clearly shows that the banks continue to have a sizeable shortfall in terms of required capital. The question now remains ‘do these recent injections of capital do enough?’. Our inclination is perhaps not, and that ultimately very junior debt holders may have to share in some of the losses thus far taken by shareholders and the government.

More importantly, though, was the announcement that both the above banking groups were able to remove hundreds of billions of pounds worth of bad assets from their balance sheets and into the Asset Protection Scheme. This is another clear effort to cleanse the banks’ balance sheets and to restore confidence in their businesses. The banks retain a first loss piece on assets placed with the scheme of 10%, and they must also pay a 6% fee for the assets placed within the structure. Our view on this new measure is that it is positive for the banks involved (and it seems as though Barclays may follow Lloyds and RBS into the APS). Ultimate losses on these assets could well exceed 16% (the fee and first loss piece), in which case we, the taxpayer, take the hit. Again, though, our concern remains that we may see these names having to top up their assets in the APS at a later date.

Today we get to see how the Bank of England’s Quantitative Easing process works. I will post again, in the comments section of this article, when we know the results of the Bank’s gilt buy back this afternoon (sometime after 2.45 pm). This is a £75 billion programme, with the first £2 billion of purchases being sought in gilts maturing from 2014 to 2018. These are as follows:

UKT 5% 2014

UKT 4 3/4% 2015

UKT 8% 2015

UKT 4% 2016

UKT 8 3/4% 2017

UKT 5% 2018

These bonds currently yield from 2.17% to 2.86%, and as Richard showed in yesterday’s blog, they have rallied aggressively since QE was announced alongside the last rate cut. The longest of these gilts has risen by nearly 4.5% in price since that announcement. The Bank will decide which stocks to buy, and in what proportions based on the highest yields submitted by market participants relative to where those gilts were trading before the reverse auction began. It’s therefore possible that the full £2 billion could come from as little as one gilt issue if that is where the “cheapest” offers come from. Other points to note: the Bank is not buying back sub 5 year paper as part of this programme, as that is where overseas Central Banks (big financers of the UK budget deficit) own gilts, and it could lead to a big reduction in the gilt market’s investor base and a possible knock on impact on the £ if overseas investors sold their gilts back to the authorities. Nor is the Bank buying gilts over 25 years in maturity, which would exacerbate the illiquidity in ultra long dated gilts, and possibly cause further problems for pension funds. The estimated UK deficit at the end of February according to the Pension Protection Fund (PPF) was £219 billion – but gilt market movements since then, even with no buy backs planned in ultra long gilts, could have increased this by £90 billion. The Bank also isn’t buying index linked gilts – but that’s worth a blog in its own right! Over the next 3 weeks, there will be a net reduction in the size of the 5 to 25 year gilt bucket of around 7%.

So how might today go? Perhaps the most important thing to note is that Paul Fisher, the new MPC member who is in charge of the Bank’s markets area (taking over from Paul Tucker who has been made Deputy Governor) has been intensively visiting market participants over the past few days. The explicit message to us is this: the Bank of England is not price sensitive. We will buy gilts at whatever level you want to sell them to us (because we want you to buy risky assets instead). This means that it is extremely dangerous to be short of the gilt market for the foreseeable future, and that far from being dear at 3% yields, ten year gilts could rally to 2%, or even lower (keep remembering that Japanese 10 year Government Bonds hit 0.5% yields in 2003). Incidently, the Wall Street Journal (subscribers only for the full article) is reporting today that the Fed has been impressed with the impact of the UK’s QE announcement and is ready to start buying back US Treasuries in a similar measure – Treasury Bond yields have marginally risen over the period that the UK gilt market has seen its mammoth rally.

Update to follow this afternoon, and we’ll let you know what we did, if anything, and whether it turned out to be a good idea.

The European Central Bank cut its main re-financing rate last week by 50 basis points to 1.50%. It is continuing to ease monetary policy into uncharted waters. Jean Claude Trichet conceded that the ECB staff’s projections for a recovery in 2009 were way too optimistic and now envisage only a “gradual recovery” – in fact, the ECB now expects flat growth in 2010 and a negative GDP print of somewhere between -3.2% & -2.2% in 2009. Inflation is also “expected to remain well below 2% over 2009 & 2010 ” and clearly leaves the door open for further rate cuts. These are all significant changes to what we were hearing from the ECB only a month or so ago.

I’ve been saying for some time (see here for a comment from September for example) that the ECB’s concerns about spiralling inflation were misplaced. The ECB now finds itself in a very difficult situation having stubbornly maintained a tight monetary policy; even absurdly hiking rates in July of last year. With consumer and business confidence remaining very weak, unemployment rising, lending slowing, a relatively strong currency & real concerns about a number of Eastern European economies, the ECB has its work cut out.

Not surprisingly JCT came under a lot of pressure to discuss quantitative easing (QE) during his Q&A session. Whilst he claimed that the ECB is already conducting “non-standard measures” and stated that the Governing Council are “discussing and studying possible new non-standard measures,” my sense was that we are unlikely to see large scale purchases of Eurozone government bonds in the near future. Clearly the ECB finds itself with less room to manoeuvre than the Bank of England and the Fed in this respect, but it may find its hand forced should the economy continue to deteriorate at the rate we are currently witnessing.

WOW. QE begins in earnest in the UK tomorrow, and is being done because conventional monetary policy has reached its limit (see previous blog article). QE involves swapping cash, issued by the Bank of England, for financial assets. The process of exchanging newly printed bank notes for assets that are then retained by the BoE forces excess sterling into the economy, and in theory, this increase in money supply will eventually be deposited with financial institutions who in turn lend it on. In theory, this process should stimulate the economy.

An important point is that QE differs from the straightforward printing of money and giving it away. This is because once the money has been created, it can be withdrawn by the selling of the acquired assets, which means the BoE is able to drain money out of the system at a later date when the fight against inflation becomes an issue again.

The BoE’s first target with the printed money is the gilt market. Gilts have been chosen as they are liquid, exist in significant quantity, and have traditionally been the least risky sterling asset from a credit risk perspective. Buying gilts therefore allows a swift and significant money expansion, and money destruction when the process is reversed. The purchase of gilts obviously drives their yields down and their prices up, bringing longer term interest rates down for the government. In driving down gilt yields, corporate bonds, which are priced off gilts, should also fall, thus reducing the cost of borrowing for corporates.

Like anything in economics, the effect this will have on gilt prices is a function of the size of the purchases (demand) versus the quantity of available assets (supply). The BoE’s announcement to buy £75 billion worth of gilts of between 5 and 25 years is tantamount to 25% of the existing stock of 5-25 year gilts, so it’s no surprise that gilts have rallied hard in the past week.

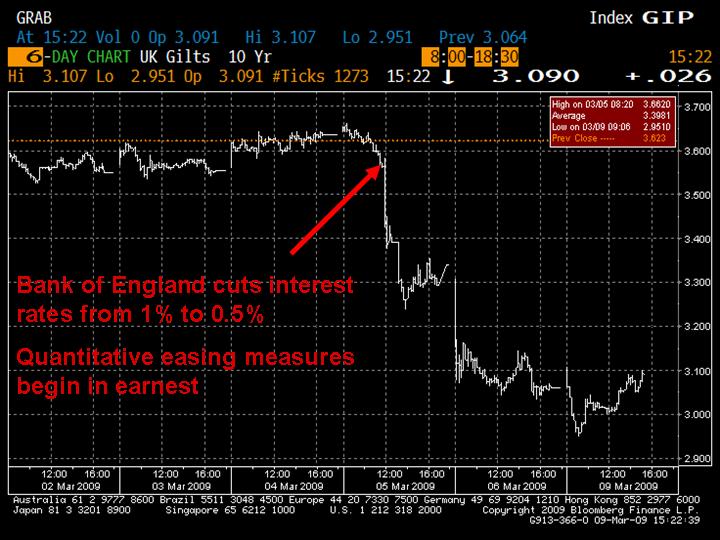

This chart shows the sharp fall in the 10 year gilt yield since last Thursday, with the benchmark 10 year gilt yield falling from 3.6% at the time of the announcement to below 3% earlier today, a record low. A 10 year gilt has a duration of just over 8 years, so a 0.6% fall in yield equates to a price return of about 4.8% in just a couple of days (0.6% x 8 years).

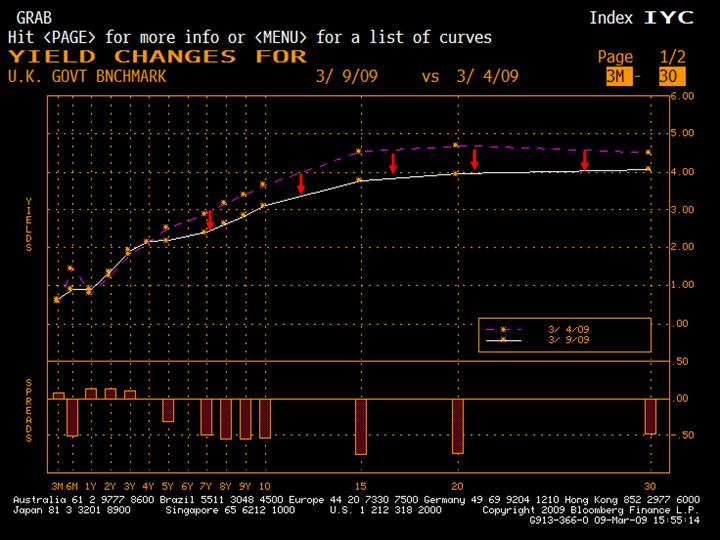

The second chart shows the change in the shape of the yield curve from the initial announcement to now. This dramatic move has been very positive for medium and longer dated gilts, and has had the desired effect of driving down long term interest rates now that short term rates have hit their lower limit. We will have to wait and look for signs for whether this works its way through the real economy as the academics predict – it may happen quickly, slowly, or not at all.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.