Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

We commented in November that growing levels of new issuance suggested that there were cracks in the ice in credit markets. This trend has rapidly accelerated. In the first quarter of this year, there was over €115bn of new issuance from corporates, almost twice as big as the previous record from 2001 and only slightly less than the €133bn figure for the whole of 2008.

Why has there been so much issuance? Part of the reason is that there was a backlog of refinancing that needed to be done in September and October 2008. But a bigger reason for the surge in issuance is that banks are not able or willing to lend, and if corporates are not able to raise finance (or refinance) with banks then they have to seek alternatives. And the only alternatives are issuing bonds to (ie borrowing from) people like us, or by tapping the equity markets via rights issues.

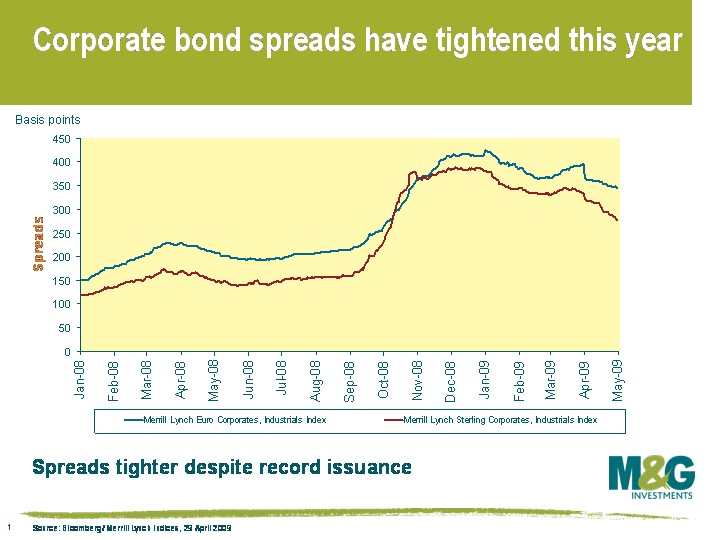

Just as an increase in government bond issuance doesn’t necessarily mean falling government bond prices (see previous blog here), surging corporate bond issuance doesn’t mean falling corporate bond prices. Taking Merrill Lynch indices, euro denominated investment grade industrials returned +4.1 in Q1%, 3.4% ahead of German government bond returns. Sterling industrials returned +4.2% in Q1,which was 5% higher than the return from gilts.

This chart shows how spreads in industrials (i.e. anything that’s not a financial or utility) have tightened over the past three months – euro industrials spreads are at least 100bps tighter than the wides hit in mid December, while sterling spreads are about 70bps tighter. (Note that at the end of May 2007, Euro industrial spreads were just 50bps over government bonds, and sterling 80bps). Spreads remain very attractive in a historical context, and spreads on new issues also continue to be attractive versus spreads in the secondary market.

We expect this flood of supply to continue through this year as companies refinance and banks continue to curb lending. However, we do expect it to fall back later this year and next year. Debt buybacks are already happening, where some companies have been patching up their balance sheets by issuing equity to buy back debt, and we expect this to increase. Many companies simply don’t have efficient capital structures for today’s markets, now that the cost of borrowing is so much higher than it was. Debt buybacks are good news for bond holders, but not necessarily good for equity holders. As companies buy back debt and new issuance falls, credit spreads should tighten fairly rapidly.

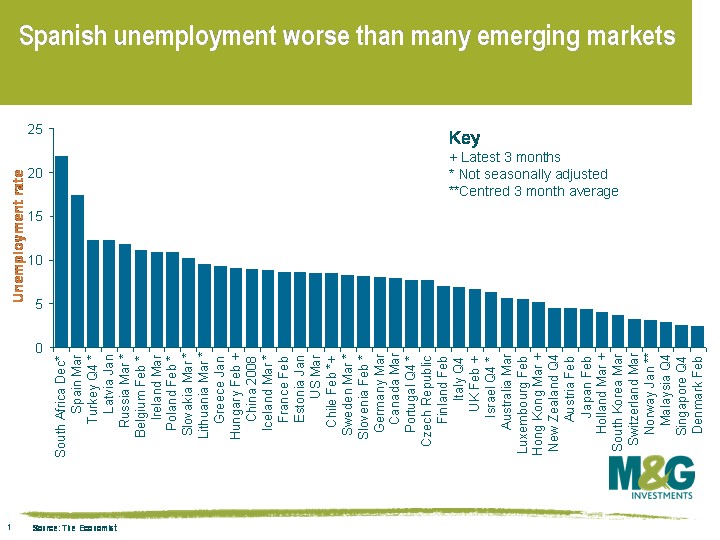

Spain is already in deflation, and this morning it released some horrible unemployment numbers. Spanish unemployment soared to 17.4% in Q1, from 13.9% in Q4. This is the first time unemployment has risen above 17% since 1998, and is further evidence of the alarming deterioration in the European economy.

Also this morning it was announced that UK GDP was -1.9% in Q1, taking the year on year rate to -4.1% (equalling the annual rate recorded in Q4 1980, which was itself the worst year on year fall since records began in 1956).

Then Bundesbank president Max Weber this afternoon said that the German economy may have contracted at least 3% in Q1 alone, which would be the worst quarter since records began in 1970. The German unemployment rate is likely to exceed 10% later this year, and the Eurozone unemployment rate is already 8.5%.

The chart puts the Spanish unemployment data into an international context. Unemployment measures do vary across countries, but the Spanish unemployment rate is considerably higher than any developed country, and is worse than a large number of developing countries (although note that emerging market data is a little old). The higher the unemployment rate rises, the greater the national discontent and the more likely there will be a severe political crisis (and the more pressure there will be for some European countries to leave the euro).

UK prime minister Gordon Brown must be jealous that his Spanish counterpart José Luis Rodríguez Zapatero had his election in March 2008, before the global economy began to really fall apart.

This is a question that numerous clients and members of the press have asked us so I thought it would be worth writing a brief comment here.

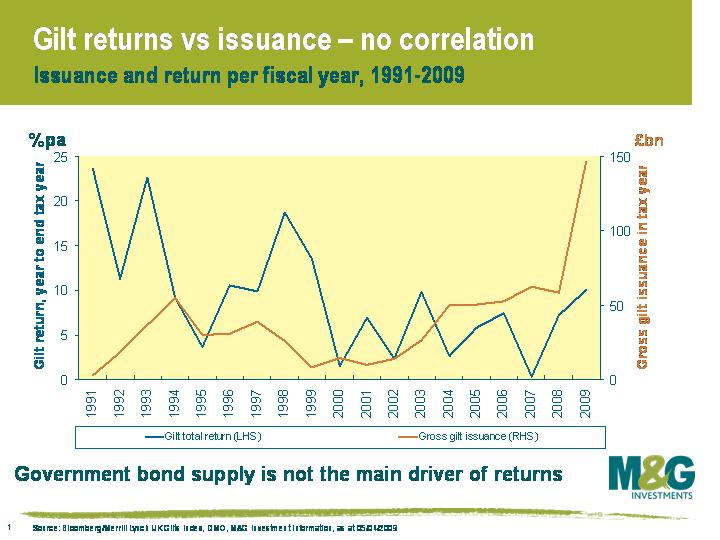

Focusing on the UK, in yesterday’s budget, chancellor Alistair Darling said that gross gilt issuance will be £220bn this financial year, which is easily a record. There is much speculation as to whether the market is able to digest this much issuance. If there is a lack of demand, or ‘indigestion’, then prices will have to fall and yields to rise until appetite for gilts returns.

The chart shows the relationship between gross gilt issuance in each fiscal year since 1991 against the total return from gilts in that period. There is no relationship. It’s also a similar story if you measure gilt issuance as a percentage of GDP, or look at net gilt issuance rather than gross gilt issuance.

A lack of correlation is not to say that it doesn’t matter if the supply of government bonds is huge – clearly it does matter. The law of economics says that if the supply of something increases, then all else being equal, the price will fall. But with regards to government bond issuance, all else does not remain equal. When governments issue lots of bonds, it generally means that the economy is in trouble. And if the economy is in trouble, it means that spare capacity is probably being created because unemployment is going up and wages are stagnant (or perhaps even falling). These things all put downward pressure on inflation. If inflation falls and interest rates are low or falling, then locking into a high fixed interest rate (at least ‘high’ relative to cash interest rates) is very attractive, and demand for government bonds increases. Yields therefore fall and prices rise. This is exactly what happened last year in the UK – 2008 was the biggest year for gilt issuance but was still a very good year for gilt returns.

What will cause demand for gilts to rise over the next year to equal or exceed the supply of gilts? It depends on what happens to inflation and economic growth. In terms of inflation, Alistair Darling projects CPI to fall to 1% this year, and RPI to fall to -3% in September before rising to zero next year. In terms of growth, he expects -3.5% for 2009, +1.25% for 2010 and 3.5% for 2011.

Slightly ironically, gilt investors should be hoping that the chancellor has overestimated his growth forecasts, even though this will inevitably result in the budget’s numbers not adding up and even more gilts being issued than projected. Gilt investors should hope Alistair Darling is wrong because if the chancellor is correct about +3.5% growth in 2011, the economy will be booming at its strongest pace since 1999 and you can be pretty confident that government bond yields will be quite a bit higher.

Much can happen between now and 2011, and his growth projection is certainly possible, but at the moment our view is that it is unlikely that UK growth will be this strong. If UK economic growth does indeed fall short of his projections, then it’s also likely that inflation will fall short too. And if your core scenario is that sterling won’t collapse (which would put upwards pressure on inflation), then gilt yields are very capable of going lower.

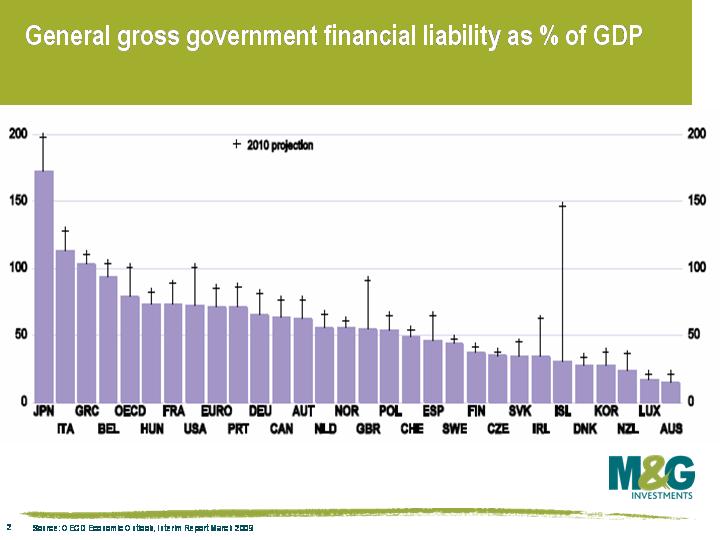

Finally, as we’ve mentioned previously on this blog, don’t forget what happened to Japan. There are of course many differences between the UK and Japanese economies, but an important lesson is that large issuance doesn’t mean government bond yields must rise. The OECD expects Japan’s ratio of public debt to GDP to rise to 197% next year, more than two times as much as for France, Germany and the UK (see chart). Japanese government debt has tripled since 1996. And yet today, 10 year Japanese government bonds yield 1.4%, and got as low as 0.4% in 2003.

With first quarter results out of Wells Fargo, JP Morgan and Citigroup this week in the US, and Barclays over here, you might be forgiven for starting to think that the financial crisis is well along the bumpy transition to the next phase, ie a global ‘real economy’ crisis. To some extent, I think we’d have to agree. We have come a long way from the week that Lehman went, when it felt like AIG would go the very next day. But we also firmly believe that the transition will not be smooth. And I would also like to point out a substantial risk that current measures are likely to meet further down the road.

Regulatory forbearance is a term that gained currency during the savings and loan crisis in the US of the 1980s and early 1990s, and a variant of it was also used during the Japanese banking crisis. It is essentially the relaxation of accounting rules and regulations applied to banks in regards to recognition of losses on bad assets. The idea is that relaxation enables banks to delay recognising losses, which in turn provides the banks with the time and flexibility to return to profitability. This enables banks to start increasing internally generated capital through retained earnings, which enables them to better cope with the latent losses they have on their balance sheets. The recent relaxation of fair value accounting methods by FASB in the US is a form of just this policy.

But this time round, I think we can coin a new phrase for the forbearance of bad assets: monetary forbearance. Interest rates across the western world are at historically low levels, and our view is that rates are likely to stay at or near zero for quite some time yet, given our deflationary outlook. Financial crises simply are hugely deflationary. The direct consequence of this is that yield curves are steep, particularly in economies where quantitative easing programs are underway, because the market’s expectation is that yields will eventually rise when the bonds are sold back to the market, and because QE should, all else equal, be inflationary. Banks borrow short term and lend long term, so with policy rates being so low and yield curves reasonably steep, they are able to post very decent profits. Wells Fargo’s results best demonstrated just this fact.

Another advantage banks gain from low rates is that loan defaults are minimised for those borrowers who have variable rate debts. So the banks get a double-whammy: an excellent net interest income portion of their income statements from low rates and the yield curve, as well as the added benefit of borrowers finding it easier to pay. That is monetary forbearance, here defined. Banks are getting the opportunity to start to earn their way out of the crisis, and low rates mean fewer loans are going bad.

But rates will not stay low forever. Indeed, for investors who believe that QE will be very inflationary, then rates will have to rise, and rise aggressively to control price increases. In the US, where the majority of the mortgage market is on fixed rates, this inflation will be a welcome development, since inflation dramatically increases the affordability of long-term fixed rate obligations. But in the UK most of our borrowings are floating or variable. When inflation returns we can expect the MPC to hike rates aggressively if needed, and this could well spell doom for UK borrowers, whose cost of borrowing will rise along with interest rates. At this point, monetary forbearance will be a warm but distant memory for UK banks, because higher rates will be directly correlated with a rise in defaults on banks’ assets. And this could be a quite brutal period for the economy and the financial institutions. Perhaps, even, a double dip in the financial crisis?

Unfortunately, it seems unlikely that this kind of outcome only comes in the event of severe inflation, and the resulting aggressive tightening of monetary policy. Disposable income is plummeting right now as jobs are being lost and bonuses are shrinking or disappearing. Enforced pay-cuts are likely to spread. Furthermore, an enormous part of the mortgage market was financed during the heady days of 2003 to 2007, which means the average size of existing loans is too large, as property was severely overvalued. This means that all the people who borrowed in this period are particularly sensitive to the size of their interest payments, and therefore particularly sensitive to rising interest rates. So, small rises in rates, along with fewer employed people and less disposable income, could have dramatic effects on people’s ability to pay their debts. This is bad for the consumer, and bad for banks.

How can we avoid this outcome, now we are engaged in QE? Well, if you want to assume an inflationary outcome to all this, the best way would be to move quickly towards the US mortgage market model of fixed interest rates. I don’t see this happening any time soon. The availability of credit at affordable terms has gone: where you could once get a mortgage for more than 100% of the value of the property,you now need around a minimum deposit of about 25%. But huge swathes of homeowners are now in negative equity, so these people are unlikely to have that kind of deposit available to them. If you instead assume that inflation is harder to regenerate, even with QE, then this solution would be a nightmare scenario because fixed rate obligations in deflation become more and more expensive to the borrower.

The outcome to all of this is so unclear as to make this mere conjecture. But it seems that, on all the cases considered above, the outcome is likely to be unpleasant for borrowers and for banks. And it is hard to see how banks’ large reported ‘accounting’ profits can be continued over the medium term.

Some interesting numbers came out of the US yesterday. US CPI was -0.1% in March, below expectations of +0.1%. This means that US CPI was -0.4% versus a year earlier, the first time there’s been a negative reading in over 50 years (see chart).

(It’s important to stress that I’m quoting the broad measure of CPI, which is including food and energy costs – the Federal Reserve, unlike the ECB and Bank of England, prefers to strip out the effects of food and energy from its inflation numbers. ‘Core CPI’ was +1.8% in the year to March. See an old blog from Richard here on whether central banks are targeting the correct inflation measures).

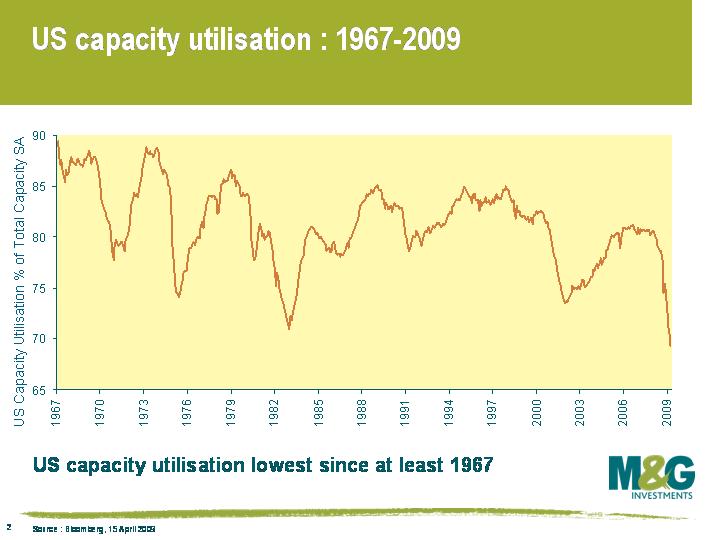

To understand why CPI has turned negative, and to understand why we think it’s likely that a number of other countries will experience deflation in the next few months, you need look no further than the ‘capacity utilisation rate’ for US, which was also released yesterday. A capacity utilisation rate of 69.3% for the end of March is the lowest figure recorded since the data series began in 1967 (see chart). See here for a comment that Jim wrote on relationship between the output gap and inflation.

So we now have US CPI negative on a year on year basis. In the UK, RPI is now zero year on year and likely to turn negative soon (although CPI is still at +3.2%). Spain, Portugal, Ireland, Switzerland, Japan, Thailand and Taiwan are already in deflation, while German and French inflation is only slightly above zero (the inflation rate for the Eurozone as a whole to the end of March was +1.2%).

The thing that all investors are trying to figure out is whether deflation proves temporary and relatively painless, or whether it develops into a deflationary debt spiral of death whereby investors delay making purchases as they can buy the same goods at a cheaper price in the future. Such behaviour would serve to exacerbate this already severe economic downturn.

It’s all getting rather interesting at the ECB. Facing a rapidly deteriorating economy and the prospect of deflation, the governing council are at odds on the best way to deal with the crisis.

Fighting out of the blue corner, the German duo of Axel Webber and Jurgen Stark argue that cutting rates further and/or embarking on quantitative easing (QE) in a US/UK style would have little positive impact. Yesterday, Webber said in a speech that he would be critical of lowering the key rate to below 1% and that “direct interventions in the capital markets should take a backseat”. Stark’s philosophy is more hawkish; in a speech he gave last month, he effectively ruled out involvement in the capital markets by stating “the health of the financial system cannot be made the ECB’s responsibility” (he didn’t offer any suggestions as to whose responsibility it is, but one assumes he is looking to individual governments). He also feels that cutting rates further could exacerbate the problem by weakening “the incentives for banks to clean up their balance sheets…and monitor their credit risk carefully”. The solution coming from these two seems to be to keep calm and carry on. They suggest continuing with the policy of offering banks unlimited loans, and Webber has also suggested lengthening the loans from the current six months to a year.

And in the Red corner, representing Greece, Cyprus, Italy and Austria we have Provopoulos, Orphanides, Smaghi and Nowotny. Provopoulos has indicated that he may support a rate lower than 1% if necessary, and would also be in favour of involvement in the capital markets. Orphanides went further in January, saying it is “dangerous” to take the view that monetary policy becomes ineffective as rates approach zero. Smaghi is a little less dovish, favouring an interest rate of zero if it’s justified, but would prefer the ECB committing to maintain a low rate of interest for a “prolonged period of time”. Nowotny agrees with the Germans to an extent as he thinks lengthening the maturities of the bank loans is the fastest option but has also recently said that “the purchase of commercial paper, corporate bonds and similar things” would be “sensible”.

The referee for the fight will be Jean-Claude Trichet. He has been non-committal as ever on “non standard measures”, although he did signal that the rate is likely to be cut to 1% at next week’s ECB meeting. None of the QE advocates have yet described how the process of purchasing government bonds (let alone corporate bonds) would work. This will be a major hurdle to intervening in capital markets, as the process will inevitably become extremely politicised. Hopefully next week both parties will add more colour to their arguments. I for one would like to have a ringside seat.

If you’re interested in watching how the fight unfolds, you can read ECB speeches as they occur here.

In a speech this morning, the Shadow Chancellor George Osborne hinted that he might change the UK’s inflation target if the Tories form the next Government (and it’s difficult to see how they can muck it up from here). Currently the Bank of England must set monetary policy to keep CPI inflation within the band 1% to 3%, and must write a letter to the Chancellor in the event of "missing". With the benefit of a bit of hindsight, commentators are saying how stupid it was not to also target house price inflation (and to be fair to Mervyn King he had publicly criticized the CPI measure on that basis as long ago as 2006), and that by ignoring them, rates were kept too low for too long, and the property bubble resulted.

It’s hard to predict what a Conservative inflation target would look like, but let’s assume they are elected in May 2010, and that they include some measure of house price inflation (HPI) in their target. Let’s also assume that this house price crash is as long and severe as the last one from mid 1989 to mid 1995 (chart here). If that were the case, then although we’ve seen the steepest falls in prices, we might not see a rising trend in prices until 2012 or 2013. On this simple, and highly speculative analysis then, including house prices in the Bank’s inflation target could cause them to keep interest rates lower than under the current regime for the next few years (the electorate won’t complain about that). We could eventually therefore see higher levels of core inflation for a given level of interest rates. The bond markets won’t like that. It is also possible that if housing prices did boom again, that the Bank would have to live with negative core inflation rates (deflation) until house prices stabilised again. The appropriate weighting of asset prices within an inflation target is going to be the topic of a very interesting debate.

The ECB cut rates from 1.5% to 1.25% last week, taking the main rate to the lowest level since the ECB took control of monetary policy in 1999. Markets had been expecting a rate cut to 1%, and rightly so.

Everything seems to be deteriorating in Europe, almost without exception. The euro is close to the strongest it has ever been versus a basket of foreign currencies, and this is killing exports (in January for example, German exports to non-EU countries were down 24.5% on a year earlier). Euro-zone Q4 GDP was revised down to -1.6% today, meaning that the economic slump in Q4 was just as bad for the region as for the US and the UK. Unemployment was 8.5% in February and is expected to exceed 10% quite soon. Consumer confidence fell to a record low in March. The reluctance of Europe’s leaders to provide additional fiscal stimulus is doing little to improve things.

Meanwhile, on the money side, inflation has fallen to 1.2% and is very likely to fall further (Spanish consumer prices are already falling). The rate of lending growth is dropping sharply – loan growth to households and companies was the weakest in 14 years in the year to February. Worryingly (see why here), the growth of money supply has fallen to 6% year on year, about half the rate at the beginning of 2008.

So what is the ECB waiting for? Did they go for a 0.25% rate cut because of some sort of compromise? Perhaps they’re hoping for extra stimulus elsewhere. It does seem likely, though, that they’re going to begin quantitative easing after Trichet referred to the need for “unconventional measures”. What this will look like in Europe is difficult to predict though – whose government bonds should the ECB buy? Will they focus just on buying corporate bonds, and if so, which bonds? If they do buy corporate bonds, will it really make that much difference given that European companies are less reliant on issuing bonds, and more reliant on bank lending?

We’ll probably get some idea next month, although there’s likely to be a lot of disagreement between members on the best course of action. Whatever happens next, the ECB’s inactivity so far demonstrates the problems of attempting to arrive at an economic decision via group political consensus, where different countries have different desires.

Yesterday the Financial Accounting Standards Board (FASB) has voted to ‘relax’ fair-value or mark-to-market accounting rules. This is, in our view, a big step in the wrong direction. We believe that it has done this under huge pressure from politicians, lawmakers, and, particularly, financial institutions. In essence, the reversal means that companies will no longer have to value their assets at available market prices (real prices), but will be able to use some amount of ‘judgement’ in their valuation. Why do we have a problem with this? Quite simply and quite clearly, if you have a company valuing its own assets, there’s a clear incentive to value assets for management’s purposes. And this is when assets are valued incorrectly.

Since 1993, with FAS 115, financial statements have been put together with certain large components of companies’ balance sheets reported at market, executable, fair values. But not all assets have to be valued in this manner. If you can argue successfully to your independent auditors and your audit committee that you are likely to hold a security to maturity, then there are other methods of valuation which do not require current market prices, and so which avoid volatility in earnings and capital.

However, companies (especially financial institutions) will be able to value many more assets than hitherto at other-than-fair-values. These are values that depend on ‘judgement’ from management, and perhaps some black-box computer model for illiquid securities. And if the financial sector is rallying, as it is, and companies are trying to reinforce confidence in them by posting profits, then there is a clear incentive for these companies to use ‘judgement’ in valuing their assets.

Rather than reflecting market illiquidity in pricing their assets, as you would expect in times of crisis, and so marking assets down in value, we now expect banks to avoid doing this by recategorising these investments as held to maturity, and so value them at a depressed, stale value, and only recognise a loss or a gain when the asset actually defaults or pays you back. So effectively this accounting change will present the banks with a means to draw a floor value level below large swathes of assets. We are losing the transparency that FASB as well as IFRS worked so hard to gain.

We have now seen $1.3 trillion of realised losses at financial institutions around the world this cycle. According to some we are closer to the end than the beginning. According to others we are closer to half way through. Whichever camp you sit in, yesterday’s event will mean we won’t know who is right for a lot longer than we would have done had this change not been made. After all, how many assets that default had a market value of par the day before they default? None. In almost all cases, the day before an asset defaults, its value would have been at a steep discount to par. So we are losing a very important piece of information. Sure, banks can’t avoid recognising losses on the assets that default, but they can avoid having to recognise large movements in value if the markets take another deep turn down.

This accounting change would not have prevented the $1.3 trillion of realised losses that financial institutions around the world have taken so far. But if these banks want to own so many securities, then the market values of those securities should be recognised in the accounts for all to see. It gives an indication of risk appetite and risk management, two key measures of bank strength at all times. And just as banks lending to us want to have all information on their borrowers as is possible, so do we as their clients and investors want to have some up-to-date, real, current information on them. Yesterday’s action is a blatant double-standard in this regard. We really hope that this US action does not gain global traction. It’s remarkable how the banks managed to get themselves mark-to-market accounting through the boom years, and so were able to recognise huge gains to asset values on the way up, and now in a downturn are allowed to relax these rules so as to avoid downward valuations. What is desirable above all at this moment is a regulatory system which ensures that banks are capitalised adequately for all markets: if the banks were capitalised appropriately, then we wouldn’t have seen this change today.

Finally, is it not particularly striking that whilst banks are arguing strongly and successfully for an end to mark-to-market accounting on their assets, which are falling in value, these very same firms are exploiting market value accounting rules of their liabilities by buying their subordinated bonds at a discount to par and recognising a gain to equity? And does it not make a bit of a mockery of the Public Private Investment Program (PPIP) initiative, in that banks are clearly less likely to sell assets at distressed prices in order to cleanse their balance sheets when they have greater control over the levels they can mark their portfolios? It seems that what the banks want, the banks get.

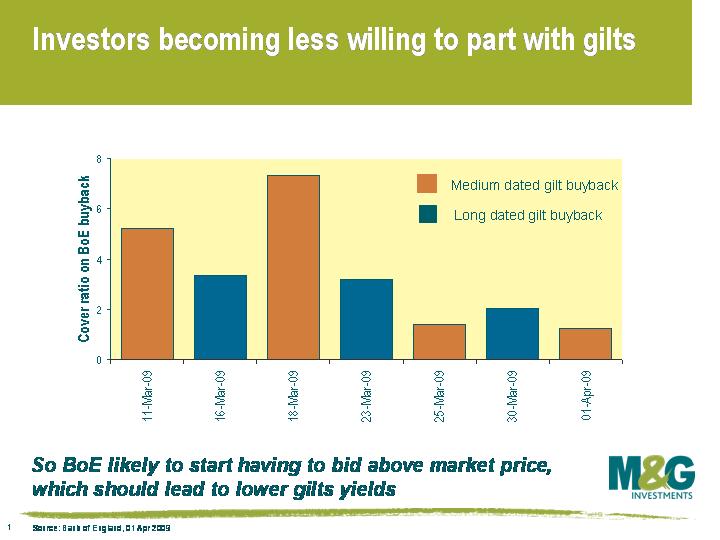

It’s still early days in the UK’s QE process, so the 7 data points we have from the gilt buyback programme to date are insufficient to draw too many conclusions from. However, this chart does seem to show that participation in the reverse auctions has been declining. The first 3 auctions had an average cover of 5.3 times – so for every gilt that the Bank bought back, there was over 5 times that amount offered. The last 3 auctions had an average cover of just 1.56 times. What’s more, the most recent buyback saw the Bank pay a healthy premium to the prevailing market prices.

It’s still early days in the UK’s QE process, so the 7 data points we have from the gilt buyback programme to date are insufficient to draw too many conclusions from. However, this chart does seem to show that participation in the reverse auctions has been declining. The first 3 auctions had an average cover of 5.3 times – so for every gilt that the Bank bought back, there was over 5 times that amount offered. The last 3 auctions had an average cover of just 1.56 times. What’s more, the most recent buyback saw the Bank pay a healthy premium to the prevailing market prices.

It’s possible that the "looser" holders of gilts (hedge funds, investment banks, market makers) have now got out of their positions, having made some profits by buying gilts ahead of, and immediately after, the Bank’s QE announcement. The next wave of gilts might prove to be harder to dislodge. These are the gilts owned by "real money" accounts, including pension funds and mutual funds. I run a gilt fund, what am I going to do if I sell my gilts to the Bank? I have to own the asset class. What’s more, isn’t QE the game that pays you not to play? The Bank wants to get gilt yields down substantially, so if I sell my gilts to them a little above the prevailing market, doesn’t the market move up to that level straight away, and then higher again at the next buyback? Paul Fisher of the Bank of England said that they are not price sensitive, and given that they are not even a third of the way through the first wave of buybacks (they will have bought back £25 bn of gilts by the end of next week), the next £50 billion of "sticky" gilts might come out at higher and higher levels.

A final thought – why have the £75 billion "quantity" target for purchases of gilts? Wouldn’t a statement that the Bank of England is going to buy gilts back in order to target 10 year gilt yields at, say 2% (they are currently 3.36%), cause the market to move there without the need for many purchases at all? And if they want to still pump the £75 bn into the market, both a quantity and level target might be a more powerful dual mechanism.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.