Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

We’ve talked about new issuance a few times recently on this blog (see Matthew’s blog from December here and my more recent comment about the record issuance in Q1 here). But the focus has been firmly on issuance in the investment grade market, until now.

The European public high yield primary market was essentially closed for 18 months, with no new issues at all from August 2007 until January this year. This is perhaps not surprising since a lack of risk appetite, combined with forced selling led to a huge blowout in high yield spreads, with the spread on the Merrill Lynch Euro High Yield Constrained Index peaking at 2298 bps over government bonds on 18th December. This therefore meant a massive increase in the cost of borrowing for sub-investment grade companies, which had been spoiled for many years with extremely low financing costs.

But spreads have tightened considerably so far this year and a handful of companies have taken advantage of the improved sentiment to return to the debt market. German medical company Fresenius was the first, issuing new bonds maturing in 2015 with a 8.75% coupon back in January, and in the past couple of weeks paper company Stora Enso and Dutch cable operator UPC have tapped existing issues (both coming on the back of reverse enquiries from existing bondholders). On top of this, yesterday saw a new five year issue from drinks company Pernod Ricard, which priced to yield approximately 400 bps over government bonds, and today Virgin Media is issuing bonds with euro and dollar tranches, slated to yield around 10.25%, in order to prepay some of its outstanding secured loans.

This is obviously good news for the high yield market, which has been pretty illiquid for some time. We’re not getting carried away though. So far we have only seen new issues from the higher rated end of the credit spectrum (Pernod is rated BB+ by S&P for example), and from names that the market is pretty comfortable lending to. Many of the more aggressive high yield companies are unwilling or frankly unable to raise capital in either the bond or equity markets. Restructurings and defaults are still the likely order of the day for many of these businesses despite the improving risk sentiment.

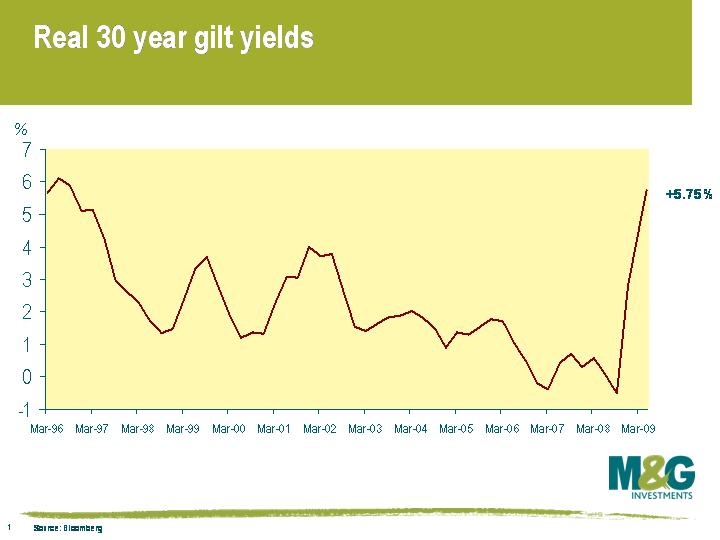

Right now the most commonly submitted question to this blog is about the impact of QE, high budget deficits and zero rates on inflation. Most people are inclined to think that after a brief period of deflation, largely as a result of lower year on year energy prices, we’re heading into hyperinflation. I guess my cop out answer to that question is that we just don’t know – it is uncharted territory, and of course, as good bond vigilantes, we are very nervous in particular about the levels of government borrowing (even though the relationship between high deficits and low bond prices is poor) and also about the way in which central banks will manage to exit QE (do gilts tank on the day that the BoE says it’s ending, or reducing, its repurchase programme?). As a result we have small short duration (i.e. bearish) positions on in our portfolios. But it isn’t a strong conviction position, and with the recent selloff in government bonds, real yields are as high as they’ve been since 1997 and perhaps we should be buying government bonds again. The real yield (the bond yield adjusted for inflation) of the 30 year gilt is now 5.75%, having been at minus 0.5% in 2008.

So rather than answer that question in detail, here is a link to a piece by the New York Times columnist Paul Krugman called The Big Inflation Scare, which debates these issues. It concludes that we are still very much in a deflationary world as output gaps increase, that the current forms of QE are having no inflationary impact, and finally that governments can cope with elevated levels of debt without having to resort to inflating it away. Krugman quotes economist Ralph Hawtrey’s comment about those who fretted about inflation during the Great Depression: “Fantastic fears of inflation were expressed. That was to cry, Fire, Fire in Noah’s Flood”.

So rather than answer that question in detail, here is a link to a piece by the New York Times columnist Paul Krugman called The Big Inflation Scare, which debates these issues. It concludes that we are still very much in a deflationary world as output gaps increase, that the current forms of QE are having no inflationary impact, and finally that governments can cope with elevated levels of debt without having to resort to inflating it away. Krugman quotes economist Ralph Hawtrey’s comment about those who fretted about inflation during the Great Depression: “Fantastic fears of inflation were expressed. That was to cry, Fire, Fire in Noah’s Flood”.

And could the recent sell off in government bond markets itself trigger a new wave downwards in economic activity, and an even bigger output gap? Yesterday in the US, Freddie Mac announced that the 30 year mortgage rate had hit 4.91%, a leap of over 75 bps in a handful of trading sessions. This means that millions of US homeowners will no longer find it possible to refinance their existing mortgages at attractive levels, and could cap any recovery in consumer spending. It’s also bad news for a banking sector that still owns billions of dollars of mortgage bonds. Risky assets have rallied hard as hopes of a V shaped recovery have multiplied – but it might be time to pause for breath.

We’ve had a question from a reader of this blog about yesterday’s announcement that Bradford & Bingley will be skipping coupon payments on some of its bonds and whether this constitutes an event of default.

Actually it doesn’t, and why not? Well, because HMT says so…

Back in February the government made changes to the terms of its nationalisation of B&B, using power it gave itself under the new Banking Act. HMT amended the Transfer Order through which B&B was nationalised to explicitly allow non-payment of coupons on B&B’s Lower Tier 2 (LT2) dated subordinated debt, and to rank it pari passu with preference shares in liquidation.

This meant that from that day onwards B&B LT2 instruments had NO event of default (neither coupon non-payment nor non-repayment of principal count as events of default), making them effectively Upper Tier 2 (UT2) instruments in every way (it was always the case that banks could defer interest payments on UT2 debt in certain cases), except that they now expressly ranked pari passu with preference shares in liquidation.

B&B had already said it would only make payments until the end of May, and after that would submit a restructuring plan that was unlikely to see any payments being made to subordinated debt holders. So yesterday’s announcement that it won’t be paying coupons on three of its Tier 2 securities (one lower T2 and two UT2 bonds with a nominal value of around £325m), which have coupon dates in July, came as no surprise.

The only continuing confusion is whether this triggers an event of default on subordinated bond Credit Default Swap (CDS) contracts, and if so, whether this credit event would also apply to the senior CDS as well. Trader speculation is rife, with varying interpretations, but no clarity yet from the trade body ISDA. The CDS market remains an immature one, and stressed events like this nationalisation show that participants need to be very cautious about the protections that they think they’ve bought or sold.

This morning S&P announced that the outlook on UK’s long term sovereign credit rating was put on negative outlook. It’s important to stress that a change in rating outlook does not mean that a downgrade to AA is inevitable, but obviously the risk has increased (S&P say the chance is “one in three”). The primary reason for the change was that the “UK’s net general government debt may approach 100% of GDP and remain near that level in the medium term”. 10 year gilt yields initially spiked 13 basis points on the news, but have since recovered most of the lost ground.

In truth it’s a bit of a surprise that people were surprised. Firstly, it’s been clear for some time that the UK’s government debt is approaching 100% of GDP. Indeed the OECD were saying this back in March, as can be seen in the second chart in a recent comment on this blog (see here).

Secondly, as we wrote in October last year and more recently this February, the credit derivatives market has long been saying that the risk of default on the UK is broadly in line with an AA rated sovereign rather than an AAA rated one. This chart (data as at the end of yesterday) shows the 5 year CDS on a range of European sovereigns, and as you can see the premium for insuring against the risk of default on Germany and France (both rated AAA) has been considerably lower than the premium for the UK for quite a while. Since the end of last year, the implied risk of default on the UK has been more in line with AA rated issuers such as Belgium, Portugal and Spain. (Note that if the credit derivative market is anything to go by, Switzerland and particularly Austria may soon find their AAA rating under threat too).

Secondly, as we wrote in October last year and more recently this February, the credit derivatives market has long been saying that the risk of default on the UK is broadly in line with an AA rated sovereign rather than an AAA rated one. This chart (data as at the end of yesterday) shows the 5 year CDS on a range of European sovereigns, and as you can see the premium for insuring against the risk of default on Germany and France (both rated AAA) has been considerably lower than the premium for the UK for quite a while. Since the end of last year, the implied risk of default on the UK has been more in line with AA rated issuers such as Belgium, Portugal and Spain. (Note that if the credit derivative market is anything to go by, Switzerland and particularly Austria may soon find their AAA rating under threat too).

So does it matter if the UK does eventually get downgraded to AA? Judging by this morning’s very successful UK government bond issue, not much. The UK’s Debt Management Office issued £5bn of UK gilts maturing in 2014, and the issue attracted bids for 2.6 times the amount offered. This was impressive considering that, as RBC have pointed out, it was the biggest ever nominal amount of bonds sold in a single operation. Also, a credit rating downgrade doesn’t necessarily mean government bond yields will rise – Moody’s downgraded Japan to A2 in June 2002, which was lower than the credit rating of Botswana at the time, and that didn’t stop 10 year Japanese government bond yields getting to 0.4% in May 2003. And lastly, what do the credit rating agencies know anyway – as we’ve previously documented on this blog (see here), Moody’s rated Iceland Aaa until May 2008.

In the worst of the Great Depression, US BBB spreads peaked at 724 basis points (see chart). Then in Q4 last year, extreme risk aversion and a huge number of distressed sellers meant that credit markets collapsed. On December 16 2008, soon after we last produced the chart on this blog (see here), US BBB spreads peaked at a 76 year record of 804 basis points.

This year has seen a big bounce in corporate bonds. A combination of a more positive economic outlook and a tailing off of hedge fund blow-ups has resulted in the pressures on the corporate bond market easing. While US Treasuries returned -3.0% from the beginning of the year to last Friday, US BBB corporate bonds were up an astonishing +10.2%. European BBB corporates have returned +9.7%, although UK BBBs have lagged with a +1.6% return so far this year, which is due to the UK index having a much larger weighting in subordinated financials at the turn of the year.

Are credit spreads still attractive? On the face of it, yes. If you exclude four months in 1932, US BBB spreads have never been wider prior to this cycle. But wide credit spreads do not necessarily mean that the asset class is attractive. Credit spreads definitely deserve to be wide right now, reflecting both the severe recession that we are currently experiencing, and the risk that the recession may last longer or be deeper than the market currently anticipates.

Another thing to bear in mind is that these charts of nice high credit spreads that investors are probably now familiar with are painting a slightly misleading picture. This is because of the way in which yields are quoted on subordinated financials. In the chart above, UK BBB spreads are significantly wider than in the US or Europe, which is a direct consequence of financials being only 12% of the US BBB index and 13% of the European BBB index, but 23% of the UK BBB index.

To understand why yields on subordinated financials are overstated and to understand the scale of this problem, take the Barclays 6.3688% 2019 as an example. This is a sterling denominated Tier 1 Barclays bond, with a total issue size of £500m. It currently has a price of 57 pence in the pound. Its yield is quoted as 13.9%, which is assuming that the bond is called in 2019. This is a shaky assumption. Barclays may never call the bond, because Tier 1 and Upper Tier 2 bonds do not have official maturity dates – they are perpetual. If Barclays decides not to call the bond in 2019 – a decision that may make economic sense given that the bond would then turn into a floating rate bond paying 170 basis point above LIBOR – then the yield on the bond today is actually a far less impressive 8.9%. Taking prices on Bloomberg, while the yield to call implies a spread of 1030 basis points on the bond, the ‘yield to worst’ (which assumes the bond isn’t called) implies a far less attractive spread of 450 basis points.

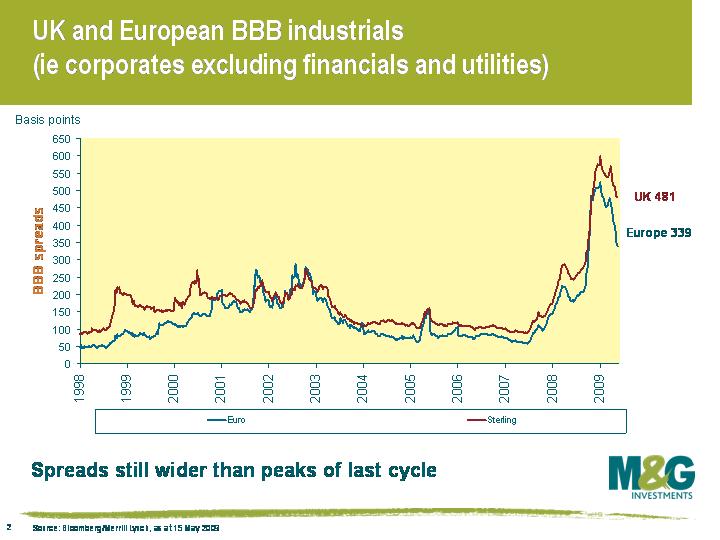

This chart is therefore a better measure of whether there is still value in corporate bonds. It focuses on European and UK Industrial BBB spreads, where an ‘industrial’ is anything that is not a financial or a utility. Industrial spreads are still wider than the peaks seen in 2002, and we do still believe that investment grade corporate bonds are overcompensating investors for the risk of default. But if BBB credit spreads were to fall to perhaps 200 basis points and we hadn’t seen further signs of improvement in the economy, then our positive view would likely change.

This chart is therefore a better measure of whether there is still value in corporate bonds. It focuses on European and UK Industrial BBB spreads, where an ‘industrial’ is anything that is not a financial or a utility. Industrial spreads are still wider than the peaks seen in 2002, and we do still believe that investment grade corporate bonds are overcompensating investors for the risk of default. But if BBB credit spreads were to fall to perhaps 200 basis points and we hadn’t seen further signs of improvement in the economy, then our positive view would likely change.

Whether you want to call it quantitative easing, credit easing, printing money or “enhanced credit support” as Jean Claude Trichet prefers, the ECB yesterday took a step in that direction. At the post rate decision press conference, Trichet announced that they had agreed in principle to purchase up to €60bn of euro-denominated covered bonds, which is roughly 10% of the public market. He said that they had decided on covered bonds as that market has been particularly badly affected by the “financial turbulence”. The announcement is good news for banks in Germany, France and Spain as they are the heaviest users of these instruments (a blog with a bit more detail on covered bonds is on its way). Regardless of how you label it, a foray into the credit markets is a clear signal that the opinions of the doves are becoming increasingly influential.

Trichet also announced a 25bp cut in the key rate to 1% and emphasised that it had not been decided that 1% was their floor. We were told that the current 6 month maturity on the loans offered to banks would be increased to a year and that the European Investment Bank (EIB) would be permitted to participate in the ECB’s re-financing operations from the 8th July. I find this a particularly clever manoeuvre as it potentially transfers the decision of which firms to lend to from the ECB to the EIB, and any criticism that may come with further interventions in debt markets.

Trichet made clear that all the decisions were made unanimously, a step no doubt designed as a show of unity after the recent bickering which came to a head with him asking members not to comment publicly on non-standard measures (see previous blog). Even though the argument appears to be swinging a little in favour of the doves it is clear the hawks are still strongly defending their corner. The weak first quarter economic data may have led one to think that more substantial policy may have been announced, I’m sure if the economy continues to weaken we will be seeing the doves in the ascendance and the hawks marginalised.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.