Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

Back in April, Mike wrote about the US entering deflation for the first time in half a century, noting a number of other countries that were also in deflation (see here). Since then, we’ve seen several more follow – the list now reads Ireland, Thailand, Malaysia, Taiwan, US, Japan, China, Belgium, Portugal, Hong Kong, Spain, Switzerland, Morocco, Canada, Sweden, Cyprus, France, Estonia, Finland, Slovenia, Germany, Singapore and Austria (in fact the Eurozone as a whole is in deflation).

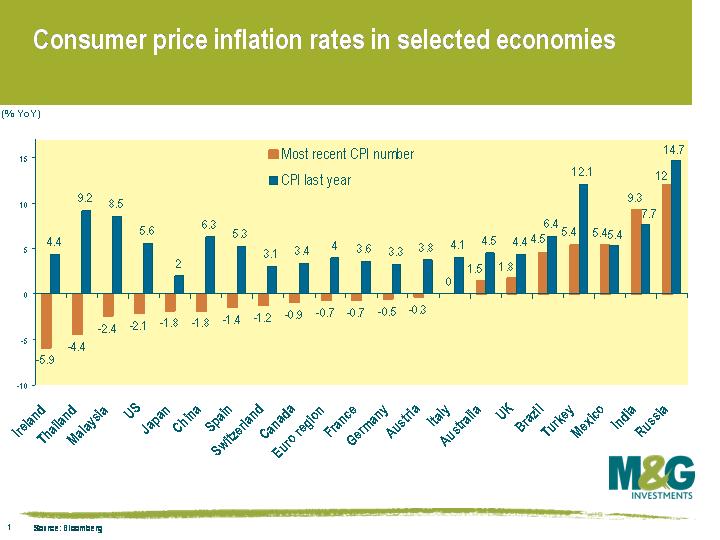

The accompanying chart shows the latest CPI inflation rates in a selection of countries, along with the rate for the same time last year. It’s clear just how large some of the downward movements in CPI have been. This is partly due to base effects, such as the decline in oil prices from last summer’s highs, but also because of the amount of spare capacity that has been created in the global economy as a result of huge falls in economic output. ‘Highlights’ from the chart include Ireland, where prices are falling at nearly 6 percent a year (perhaps we may soon see the Northern Irish heading south to shop instead of the other way around), and France and Germany, which are in deflation despite recently printing positive Q2 GDP numbers.

The accompanying chart shows the latest CPI inflation rates in a selection of countries, along with the rate for the same time last year. It’s clear just how large some of the downward movements in CPI have been. This is partly due to base effects, such as the decline in oil prices from last summer’s highs, but also because of the amount of spare capacity that has been created in the global economy as a result of huge falls in economic output. ‘Highlights’ from the chart include Ireland, where prices are falling at nearly 6 percent a year (perhaps we may soon see the Northern Irish heading south to shop instead of the other way around), and France and Germany, which are in deflation despite recently printing positive Q2 GDP numbers.

It’s also interesting to note that US CPI is lower than Japanese CPI.

Having recently recovered from my amateur stunt man escapades I thought I’d pen a short note on the recent court sanctioned debt restructuring by IMO Carwash.

Why do investors outside of IMO care ? Well, it’s the first time that the English courts have been asked to rule on the issue of valuation in the case of a company restructuring, and it has implications for senior & junior lenders in both the high yield and leverage loan markets, particularly in light of the rising default rate.

The case recently ended up in court after the LBO ran into trouble and the proposed restructuring left no value for the mezzanine lenders. Mezzanine finance is usually the most junior debt a company will issue, senior only to the equity. The original plan was for the senior lenders to have their debt swapped for virtually all the equity in a new company, cutting the junior lenders out. The senior lenders argued in court that the mezzanine lenders had no economic interest given that the value of the assets was less than the value of the senior debt. The mezzanine lenders countered that this was an unfairly good deal for the senior lenders, arguing that the deal was being struck at trough valuations. Ultimately the judge ruled in favour of the senior lenders, dismissing the arguments of economic interest made by the mezzanine lenders.

As a result of this ruling, senior lenders are likely to gain more confidence in their ability to exclude junior creditors in future restructurings and perhaps increase their willingness to enforce their rights in certain circumstances. As investors in senior and subordinated debt, we have long recognised the increased security afforded to senior lenders.

The coming years will see further restructurings as a number of the aggressive leveraged finance transactions of previous years find themselves in difficulty. We’d expect the implications of this recent ruling to be felt by many more mezzanine lenders.

The Minutes from the Bank of England’s Monetary Policy Committee meeting of two weeks ago were released earlier today. They show that the motion to increase the Quantitative Easing program by £50bn was carried with a vote of six to three. Interestingly, Governor Mervyn King was one of the dissenters. Not too long ago one would have assumed that this would have been due to him worrying that inflation is about to pick up and that he would therefore be reluctant to increase the monetary stimulus further. In fact quite the opposite is true. King and the other two dissenters (Beasley and Miles) actually voted against the £50bn, as they wanted to increase it by £75bn (which would have taken the total programme to £200bn). This is a quite a departure from the previously hawkish Governor, who, it was reported in the New Statesman, opposed the 1.5% rate cuts of late last year. I guess it remains to be seen if once again he’s a little late to the party or he has now managed to get himself ahead of the curve. Bear in mind however that the increase in QE was announced before the unexpectedly sticky UK inflation data…

There’s a hidden restaurant, somewhere north of the Bethnal Green Road, called the Rochelle Canteen. And for some reason it has a figure of eight wooden cycling track in its garden, built by an artist at St Martin’s and looking like a haunted rollercoaster out of Scooby Doo. With the spirit of Team GB’s Beijing 2008 track triumphs still in our hearts, the Bond Vigilantes gave it their best shot. If you just want to skip to the pain and suffering, then 2 minutes 15 seconds is a good place to start.

Click here to watch on You Tube.

The rally in corporate bonds this year is reminiscent of Usain Bolt in full flight in the 100m dash at the Beijing Olympics. Historic. Unprecedented. Fast. So just how far have corporate bond spreads rallied?

After blowing out late 2008 and early 2009, corporate bonds spreads have rallied back to levels that were last seen before the Lehman Brothers collapse. And rightly so. Corporate bond spreads were pricing in a very pessimistic level of defaults, especially for investment grade corporates. If we believed what corporate bond markets were telling us, we should have been building shelters and waiting for the collapse of the world as we know it.

Fortunately this scenario didn’t eventuate. We have discussed the factors surrounding this rally here, and I have updated a couple of charts that we used back in May. Looking at BBB spreads, the current level of spreads suggests that the economic environment for corporate bonds is now a “typical” recession. From this, we can extract that the market is now expecting an increase in the level of defaults that is consistent with that experienced during a typical recession (the worst experienced default rate in Europe was 5.8% for BBB bonds over 5 years). Industrial spreads have rallied to such an extent they are now lower than the peaks seen back in 2002.

What is really interesting is the total (capital appreciation plus interest) returns that the various indices have generated for investors. Nick Burns from Deutsche Bank notes that from a starting point of July 31 2007 – a time when credit spreads were very low – BBB corporate bonds have returned close to 13% in Europe, 10% in the US and 4% in the UK. Corporate bond returns are now only slightly lagging government bond returns over this period. This is impressive considering that if an investor sold at the peak of credit spreads (let’s say around December 2008), he or she would be looking at a loss of -9% in the US, -6% in Europe and -15% in the UK. Over the same period, equities have not performed quite so well. Since end July 2007, the DJ Stoxx 600 is -36% lower and the S&P 500 has fallen by -29%. Basically, the financial crisis has had negligible impact on an investor’s IG corporate bond portfolio. This is amazing given the heart attack financial markets had last year.

Importantly, the good returns in corporate bond markets reflect the fact that credit markets are healing and are returning to normality. The first half of 2009 has seen a record amount of new corporate bond issuance by non-financial companies. Investors’ risk appetite is increasing and there has been a lot of demand for these new issues. The cash holdings that were hoarded by investors following the financial crisis are now being put back to work and IG credit continues to look cheap relative to forecasts for future economic growth.

It is clear that corporate bonds have been the star performer in financial markets this year. We continue to believe that credit spreads are overcompensating for the risk of default, but it is almost impossible for corporate bonds to continue rallying at this 100m pace for more than another three months on credit spread tightening alone – if they do, then credit spreads will be at all time record lows.

It seems the Bank of England has been acting as the Grand Old Duke of York – gilt yields had been marched fairly close to the top of the hill a week or two ago, with 10 year gilt yields getting close to 4% (back to levels seen in November) and 30 year gilt yields reaching 4.6% (about the same as in July 2007). Now they’ve just marched some of the way down again. 10 year gilt yields initially tumbled 0.16% lower yesterday (a 1.2% price gain), and 30 year gilt yields dropped 0.25% lower ( a 3% price return), although gilts have since given back a small amount of these gains.

The reason for this sharp rally is that the 10000 or so men and women who closely follow the Bank of England’s every move thought that it would pause its asset purchase scheme, or at least not extend it by much. The decision announced yesterday that it would purchase an additional £50bn of government and corporate debt therefore came as a surprise to most.

Why did the BoE extend the programme? You can see the full release here, but the reasons cited were that the UK “recession appears deeper than previously thought”, “slack in the economy is likely to grow for some while yet”, “financial conditions remain fragile”, and “lending to business has fallen and spreads on bank loans remain elevated”.

But at the same time, “there have been increasing signs that output in the UK’s main export markets is stabilising”, “financial market strains have eased and banks’ funding conditions have improved a little”, “the pace of contraction has moderated”, “business surveys suggest that the trough in output is close at hand” and “credit conditions may have started to ease”. So make of that what you will.

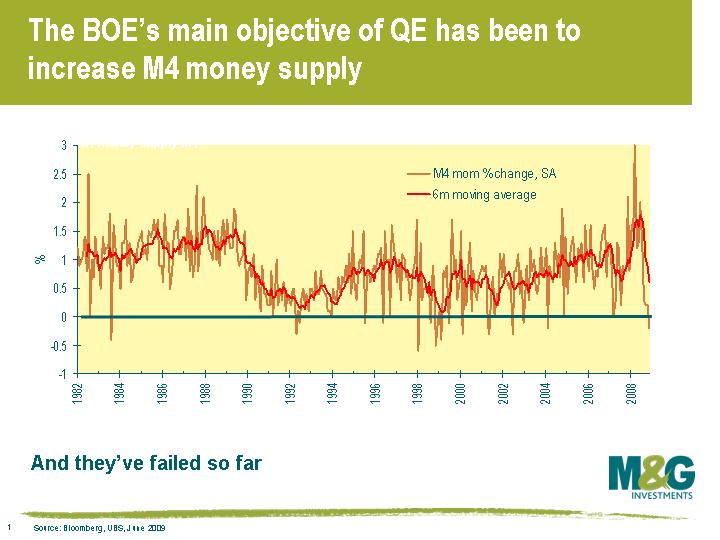

Not everyone’s been anticipating the end of QE, and among the people who deserve a hat tip is UBS’ Roger Brown, who showed us the chart below on Tuesday. He pointed out that the Bank of England’s main aim has been to increase M4 money supply. When the BOE initially got permission to begin QE, M4 money supply stood at £2trillion. The BoE is targeting money supply growth of 7.5%, and that’s why the BOE originally sought permission to buy £150bn of assets. However, M4 money supply growth has in fact been dropping rapidly in the past few months, and was negative in June. On this measure, therefore, QE has been a failure, and Roger Brown therefore argued that more QE is likely (although he stressed that this didn’t make him a long term bull for gilts – QE extension would just delay the enormous gilt market puke that is surely going to happen at some point). Why hasn’t QE worked? There’s a bit of a clue in Lloyds’ recent results – end December 2008, it had £7.5bn of ‘cash and balances at central banks’, and by the end of June 2009 it had over £60bn.

In fairness to the BoE, though, everything they said in the release above is entirely true. The UK and global economy remains in a very fragile state. The BoE is walking a tightrope – do too much QE and the result will be growth in the short to medium term, but accompanied with runaway inflation, which will be very bad for longer term growth as rates are hiked and government bond yields soar. Do too little QE, or implement the exit strategy too soon, and the result would be an acceleration of the downturn and further pressure on the vulnerable banking sector.

The noises coming from MPC members in recent weeks have been occasionally confusing, but maybe the title of this blog is a little harsh. But better to be the Grand Old Duke of York than the Pied Piper, or we’re all in trouble.

Guest contributor – Tamara Burnell (Head of Financial Institutions, M&G Credit Analysis team)

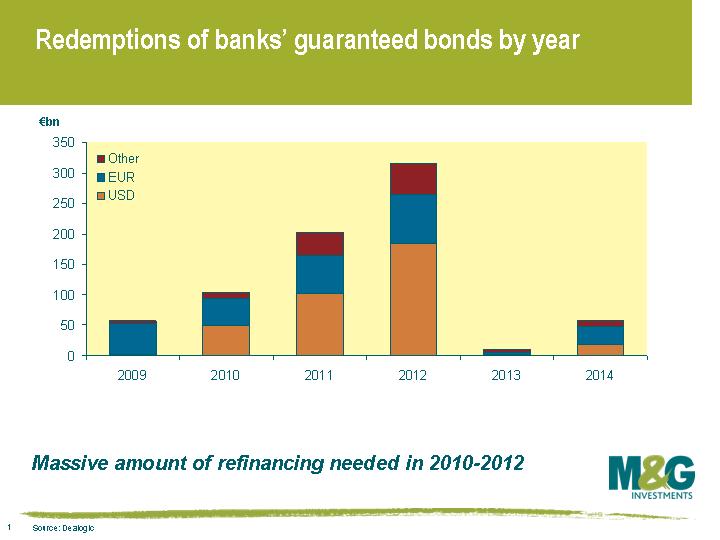

The Bank for International Settlements (BIS) has published a study of the ‘impacts’ of the bank rescue programmes used to date – see here for the full publication entitled ‘An assessment of financial sector rescue programmes’. It concludes, not surprisingly, that the schemes have so far failed to generate any perceptible easing of the supply of bank credit to the economy (which in fact continues to decline in the US, UK and EU). Moreover, the guarantee programmes have created some big refinancing risks of their own in 2010/2011/2012, as can be seen from the chart above. While there has been some tentative pick up in covered bond issuance in several countries, their cost remains prohibitive.

The Bank for International Settlements (BIS) has published a study of the ‘impacts’ of the bank rescue programmes used to date – see here for the full publication entitled ‘An assessment of financial sector rescue programmes’. It concludes, not surprisingly, that the schemes have so far failed to generate any perceptible easing of the supply of bank credit to the economy (which in fact continues to decline in the US, UK and EU). Moreover, the guarantee programmes have created some big refinancing risks of their own in 2010/2011/2012, as can be seen from the chart above. While there has been some tentative pick up in covered bond issuance in several countries, their cost remains prohibitive.

As well as the oft-discussed problem of crowding out of sovereign borrowing (especially in the UK), the data suggests that the guarantees are bailing out large complex/investment banks, rather than those banks most likely to lend to their domestic economies, so the subsidies are not reaching their intended beneficiaries. It also appears that the main investors in guaranteed bonds are a) other banks, ie investments in guaranteed bonds are crowding out bank lending, and b) more specifically, banks in the same country as the issuer – which in Europe is having the effect of breaking down the Euro area bond market back into its national constituents again and reducing liquidity.

With banks now addicted to government guaranteed issuance on both sides of the balance sheet (ie as issuer and investor), the BIS admits that “convincing the credit (risk seeker) investor base to resume investing in unsecured bank debt may turn out to be an expensive task, with potential adverse consequences for the real economy”.

However, some of their conclusions are flaky at best – eg they argue that weaker countries should be allowed to charge lower guarantee fees to the banks in their country, to give them access to bond markets on a level playing field with banks with higher rated sovereigns. [When you see that the report was prepared primarily by staff from the Bank of Italy, this starts to make sense!]. They also seem convinced that in order for governments to achieve a quick exit from the guarantee schemes, and wean banks and investors off these government guaranteed bonds, the solution is to recreate (ie subsidise) the securitisation market. However, they have no suggestions of how this could be done without releveraging the banks all over again and eating into the new capital cushions that have only just been injected by governments.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.