Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

It’s been quite some time since we have seen a new public issue in the UK RMBS market. In fact, it’s probably been closed for new deals since the beginning of the crisis. As property prices plummeted, and as everyone fled risk assets for cash and gilts, RMBS bonds saw large price falls. Liquidity in these bonds actually suffered almost as much as subordinated bank bonds, because unlike corporate bonds where you generally know the company you are buying into and the terms on which you are agreeing to invest in them, with RMBS you have to know about all the structural idiosyncrasies of the bond, including its ranking, which assets it is secured against, what the triggers of the structure are (that can sometimes protect you as an investor, and sometimes impede you), and so on. Given these additional layers of complexity in contrast to a traditional corporate bond, and given that they are largely secured upon financial assets, which everyone hated during the onset of the crisis, liquidity fell off a cliff.

Last week, though, we saw the issue of Permanent Master Trust 2009-1, the RMBS issuing platform of Halifax Bank of Scotland (now owned by Lloyds TSB). The government, having provided all the support it has to prop up the entire banking system (including capital injections, debt guarantees, liquidity facilities, and asset purchase schemes (almost!)), was keen that the banks in return offer to make new loans to its voters. So banks on the one hand had to de-lever urgently, but on the other now owed their very existence to the government who were telling them to keep lending. In fact, even, to increase lending over 2007 levels!

Whilst banks have not been able, let alone willing, to originate many new loans of any type, even secured, they have clearly made some, and have built up meaningful balances of mortgages and other loans that are sitting on balance sheet, or being financed on repurchase agreements with the Bank of England or the European Central Bank. It felt that the old master trust system had well and truly broken. Until Wednesday.

In order to get the investment community interested once more in the UK RMBS space, the Permanent deal had to come with an array of structural concessions in favour of the buyer. Whilst there are too many protections built in to mention here, there are a couple that are worth mentioning. The first was that traditionally you bought a master trust RMBS bond that had two maturity dates, the first being an expected maturity date, and the later being a legal final maturity date. The difference between these was that in the event that everything was working fine, your bond would pay out at expected maturity as cash flows from all the mortgages started to be trapped to build up your expected principal. But if there was some kind of problem with the market, the master trust, or the bank, and the principal couldn’t be built up within the master trust, then you knew you had the risk of extension of your bond to legal final maturity date. This new bond, though, came with a new put option at the expected maturity date, which means that after 5 years if the master trust hasn’t been able to trap the cash to pay our principal out (at expected final), we as investors can put the bonds to Lloyds and get our principal back. So the new RMBS deal has eradicated extension risk, and is now essentially a bullet bond. The other new feature of this issue was that Lloyds-HBOS replenished the master trust’s reserve fund, which is the most subordinated part of the trust, from c.2% to c.8%. In other words, the issuing banks felt they needed to improve the credit enhancement of the trust to get a new deal done.

Well, these improvements to the old structures worked. The deal was upsized (ie they issued more than planned) given the high interest, and even after increasing the size of the deal, the books were 2 times oversubscribed (orders for 2 bonds for every one being issued). Lloyds-HBOS issued euro and sterling denominated tranches, both coming at around Libor + 1.8%. The deals have performed extremely well in the last couple of days, and are now quoted at spreads of around Libor +1.3%, meaning the bond is priced almost 2 points higher in only 2 days!

Our feeling is that at this level of funding for new mortgages (somewhere close to 1.5% over Libor), the banks are once more, and after a considerable period of time, economically able to finance mortgage loans. We thus anticipate more deals to come from other master trust issuers in the coming weeks. Ultimately, if this genuinely represents the reopening of the RMBS market, and doesn’t turn out to be just a fillip, then mortgage availability to all of us is about to improve dramatically, and that just can’t be a bad thing.

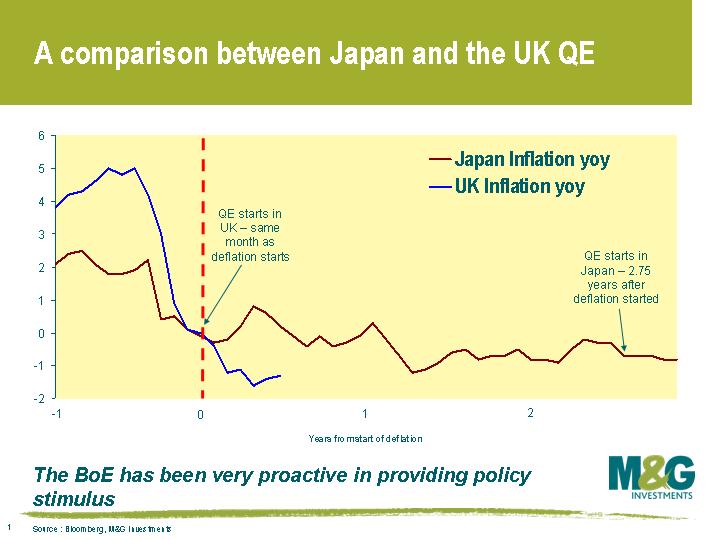

We’ve had a huge rally in risky assets since we wrote a comment about Turning Japanese almost a year ago, and while diminished, the risk of a ‘lost decade’ is still very real. I thought it would be worth another look. Now I am not out to compare and contrast the prevailing conditions that led to deflation and QE between Japan and the UK, but what I want to do is ask whether deflation, which led to QE in both countries, necessarily means stubbornly low and flat government bond yield curves, as it did in Japan?

As a brief reminder, the Japanese experience began with the property and equity bubble bursting in 1989, followed by weak growth and deflation through most of the 1990s. As people know, the Japanese response was much slower that what we’ve seen.

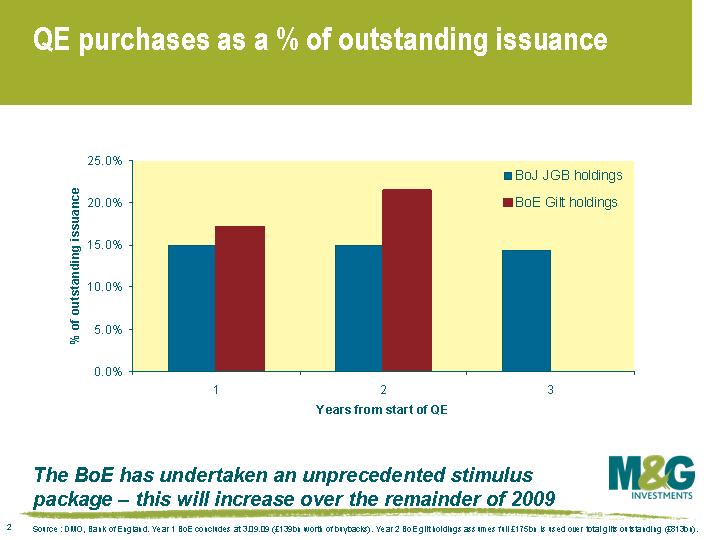

The Bank of Japan (BoJ) hiked rates to 6% half a year before the economy entered recession in March 1991, and cut incrementally towards zero over the next 4 years, well into the country’s contraction. The BoJ waited almost 3 years after entering deflation before beginning QE. And, as a comparison, the Bank of England has bought back a bigger percentage of the gilt market in only six months than the BoJ did at any stage, and has approval to do even more.

As we have discussed in previous blogs, deflation is a dire scenario for central bankers and policymakers, destroying the efficacy of monetary policy. But when the deflationary psychology sets in to an economy and its agents, it could also have horrific consequences for the economy through consumer spending (which represents about 70% of our economy’s output), as people cease spending. Why would we buy a new fridge, say, today, if we know that in 1 year’s time it will be cheaper? It is really with these fears in mind that authorities in the US and UK in particular have reacted so quickly and substantially, and why we are repeatedly told they would “rather do too much, than too little”.

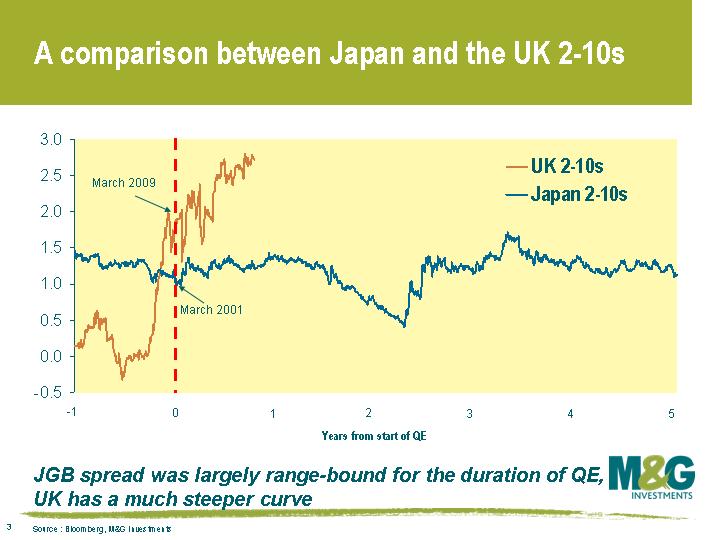

Looking at the difference between 10 and 2 year government bond yields in the UK and Japan when QE started, we can clearly see that the UK curve is substantially steeper than Japan’s yield curve. This suggests that the markets are as yet not expecting the curve to flatten a la Japan. Why might this be? Well, firstly, it may be because unlike Japan, the Bank of England has been quick to react to deflation and has been aggressive in its response. So the markets have perhaps interpreted the level of stimulus as being sufficient to stave off anything like a lost decade of growth due to a fall in aggregate demand leading to a deflationary spiral. In other words, QE may have done enough to reignite inflation.

However, I think a significant reason is to do with the constitution of the two markets, namely the proportion of government borrowings owned by foreign investors. In Japan at the time of QE, approximately 3.4% of JGBs were held by foreigners. This is a sharp contrast to the government bond markets the US and UK. Today, 36% of outstanding gilts are owned by foreigners. This is a huge difference, and it adds to my hunch that deflation, even if it were to persist in the UK, would not necessitate very low and flat yield curves. With only 3.4% of JGBs owned by overseas investors, Japan could proceed with an inflationary stimulus programme and not worry about an exodus of foreign demand for their bonds, or about an influential foreign buyer network demanding higher JGB yields for the (perceived rising) risks.

Japan could print money, thereby putting negative pressure on the Yen without overdue concern about not being able to borrow the requisite funds. Contrastingly, the US and UK are constrained in regards to inflating out of a large debt burden and devaluing the currency, since foreign owners fleeing government bonds would put huge upwards pressure on government bond yields. This is a big issue for the US at the moment, with China owning over $800bn of US Treasuries (see here for full list).

Painful adjustments undoubtedly lie ahead as government expenditure is cut, as taxes rise, and as the nation’s balance sheet is rationalised and delevered. And if this is done sufficiently and appropriately, there is no reason foreign holders will flee the currency or the government bond markets. And we actually take our hats off to the authorities for recognising the dangers of a deflationary spiral that could so easily come from the complete shut-down of the credit mechanism in an economy. Now for the second, and every bit as important part: withdrawing the stimulus at the right time so as to avoid hyperinflation and a collapsing currency.

There has been a lot of talk about M&A activity, fuelled by Kraft’s attempt to buy Cadbury. Judging by where corporate bond yields are, this talk is entirely justified. The credit rally we’ve had, coupled with the fact that government bond yields are still very low historically, means that right now non-financial investment grade companies are able to borrow from debt markets at almost the cheapest levels ever. The attached chart shows the yield for the average single-A rated industrial company – citing specific examples of A rated companies,  McDonald’s can borrow in euros for five years at 3.6%pa, while GlaxoSmithKline can tap markets at about 3.5%pa for five year paper, and IBM at 3.3%pa. GlaxoSmithKline’s estimated P/E ratio is 12, which means that its equity earnings yield (ie the inverse of the P/E) is 8.3%, so it makes sense to lever up the balance sheet, either through share buybacks or takeovers.

McDonald’s can borrow in euros for five years at 3.6%pa, while GlaxoSmithKline can tap markets at about 3.5%pa for five year paper, and IBM at 3.3%pa. GlaxoSmithKline’s estimated P/E ratio is 12, which means that its equity earnings yield (ie the inverse of the P/E) is 8.3%, so it makes sense to lever up the balance sheet, either through share buybacks or takeovers.

Now it’s very important to stress that corporate bond yields around historical lows doesn’t mean that corporate bonds look expensive. As argued recently here, credit spreads are still at levels that you’d normally associate with a bad recession, and are at similar levels to the most distressed points seen in 2002. A bigger concern on our desk is that government bond yields are likely to rise (and portfolios are positioned accordingly), but that said, government bond yields do deserve to be lower than average – economic growth around the world is still very weak and will probably be anaemic for a while, deflation is still a major risk, and central banks’ policies should prevent government bond yields rising rapidly in the short to medium term.

Rising leverage has a longer term implication for credit markets, in that it is bad for credit quality. However while credit markets are ripe for an increase in leverage (at least in non-financial investment grade companies), it’ll probably take a while for the M&A boom to really kick in. A number of CEOs will have been scarred by being over-leveraged going into the downturn and won’t want a repeat. Plus a lot of the credit bubble of 2004-07 came from banks and private equity. Banks won’t be allowed to leverage up to anything like the same extent, and we’re quite a long way from another private equity/LBO boom (in fact the two groups are closely related – a friend in a relatively small private equity firm tells me that while banks have re-entered the market in the past three months, banks are having to club together on any deal over £20m, leverage multiples are almost half what they were a few years ago and the banks’ arrangement fees are double what they were in the boom times).

A final observation is that maybe the monetary transmission mechanism isn’t quite as broken as some think. As the global economy was heading for recession last year, central banks slashed interest rates and government bond yields tumbled. Central banks were desperate to contain the financial crisis within financial companies, and prevent the worst of the effects spilling over to non-financial companies. On this measure at least, the policy responses seem to have worked – many companies have gone from facing crippling refinancing costs at the end of last year, to enjoying the cheapest refinancing levels they’ve ever experienced. The leverage cycle normally follows the traditional business cycle, taking 8-10 years, but the authorities have been giving this cycle a serious dose of amphetamines.

Yesterday the MPC meeting was a non-event since there wasn’t a change in anything. However a few of us on the team had a bit of a ‘coo’ after we had a much more interesting meeting with David ‘Danny’ Blanchflower, who left the MPC in May of this year with his credibility sufficiently enhanced as one of the very few people who saw chunks of the financial crisis coming. Having served his three months of silence on Bank of England and MPC matters, he is now very busy revealing all. Some of the topics discussed appeared in his sensational article in the New Statesman, which is well worth a read. On top of this we got the following impressions from our alternative monetary policy meeting.

The economic recovery will be anaemic, and a big reason why is that the MPC is struggling to create demand for credit in the economy. Quantitative Easing should (in his view) be increased since the monetary policy mechanism is broken. The man who got it right over the last few years is still very dovish, and if he was still on the MPC, he’d clearly be pushing for an extension of QE. From what he was saying, interest rates could remain low for ages.

An under-appreciated reason why we’re in for a period of sustained weak growth is that unemployment is spiking, particularly among the highest propensity to consume sector, the young, just as a demographic time bomb is going off (I talked a bit about this on our blog in June here). It’s today’s jobless youth who are going to have to pay for us when we eventually retire, and we need to address this issue or we could expect significant social unrest. We need to err on the dovish side for the good of society, and governments may need to err on the dovish side for the good of popularity.

It was very interesting discussing the workings and influencing of a committee-based process. The New Statesman article linked above got a lot of press coverage, and the main sensationalist focus was on what appeared to focus on the workings of the committee, and the rift between Danny and Mervyn King. Yes, the article is scathing in places, but the coverage seems to have missed the point – Danny clearly has a lot of respect for Mervyn, and having been a hawk, Mervyn is in fact now dovish like Danny. Mervyn seems to take a very pragmatic approach to understanding economic signals, and is prepared to be sceptical of the Bank of England’s economic models (which is similar to Danny, who calls himself an empiricist and firmly believes in the economics of walking about). This is quite different to some other members of the MPC – the ‘plodders’ – who seem to focus more significantly on the models. And that’s a very big problem right now – the Bank of England’s models could not have been perfectly programmed for the seismic shock we have had to the financial system, and have been primarily tailored to work via examining changes in the price of money (bank rate) rather than the quantity of money. Yet monetary policy is currently been conducted in the realm of quantity, not price, via quantitative easing. The outcome from this quantitative easing is a big unknown for everyone, which is something that we have referred to in a previous blog here.

Not only is it difficult to reach a consensual view on policy in a committee, it is also hard to put the message across, so in the recent press conference following the release of the inflation report, Danny believed Mervyn was deeply uncomfortable since he was representing the MPC’s consensual view not his own. When interpreting the messages coming out of the Bank of England, it’s very important to realise that sometimes even when Mervyn King speaks it’s sometimes Mervyn’s own view, and other times he’s representing the MPC’s view (I commented on some of the recent confusing messages here).

Our lunchtime meeting with the man who got it right on the committee was very interesting, intellectual, and challenging. Let us hope the spirit of that is not lost now he has left the committee. Thank you to John Wraith and the guys at RBC for organising and hosting the meeting.

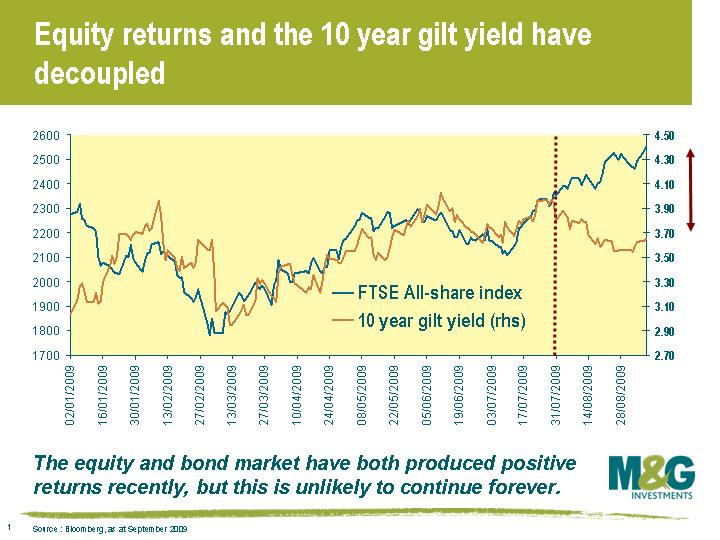

The month of August was an investor’s dream, with major asset classes like equities, government bonds, corporate bonds and property producing positive returns over the month. However, like two gunslingers in the American Old West, the equity and government bond markets are now currently staring each other down waiting for the other to flinch.

Taking the UK as an example, 10 year gilt yields and the FTSE All-Share Index are normally correlated, ie when the equity market goes up, gilt yields also go up and vice versa. As the chart on the left shows, up until the end of July this rough guide held true.

Taking the UK as an example, 10 year gilt yields and the FTSE All-Share Index are normally correlated, ie when the equity market goes up, gilt yields also go up and vice versa. As the chart on the left shows, up until the end of July this rough guide held true.

More recently, this relationship has broken down. And for our readers outside the UK, the relationship between equity returns and government bond yields has also broken down in Europe and in the US. The talking point in markets over recent weeks is the fact that equity markets have continued to rise while at the same time gilt yields have fallen. This has occurred very rarely in the past 5 years, so why is it happening now?

Part of the answer lies with the Bank of England’s Quantitative Easing programme. Bank of England Deputy Governor Charlie Bean has recently told markets that without the programme gilt yields would be around 50-75bp higher. And as the chart shows, a direct read of where gilt yields are relative to equity markets suggests the same.

Looking ahead, I’d expect that the usual relationship between gilt yields and equity market returns will reassert itself. But does this occur because equity markets fall or because gilt yields rise? That’s the interesting question here. In my view, the Bank of England will have to think long and hard about its QE exit strategy. Gilt yields are sure to rise if the Bank stops buying and the UK Debt Management Office keeps issuing.

Guest contributor – Jeff Spencer (Financial Institutions Credit Analyst, M&G Credit Analysis team)

Investors could be forgiven for thinking that the US banks are well on their way to recovery, with several big banks having redeemed the government preference shares and bought back the government warrants they received under the Capital Purchase Program (CPP) of the Troubled Asset Relief Program (TARP). Away from the office towers of Manhattan, Charlotte and San Francisco, however, the banking system’s troubles are getting rapidly worse, even if the larger banks’ situation has stabilised. Out of view of the bond markets, the Federal Deposit Insurance Corporation (FDIC), which insures US depositors, currently up to $250,000, is preparing for a wave of insolvencies among smaller banks, and is rapidly running out of reserves to absorb the losses those failures are likely to cause.

The FDIC deposit insurance fund dwindled to $10.4bn by the end of the second quarter, as reported on August 27, from $13bn at the end of the first quarter and from $45.2bn in 2Q08. This decline followed a special assessment approved in Q2, which was 5bp of each insured bank’s total assets net of Tier 1 capital (i.e., equity and retained earnings, preferred stock and some hybrid instruments). The FDIC does have a line of credit with the Treasury, which it can draw on if it needs to, but it announced recently that it was opening the door – just a crack – to private equity buyers by easing some of the conditions it had imposed on non-bank buyers of banks out of FDIC receivership; the unspoken hope is to increase the buyer base so that the deposit insurance fund sustains fewer losses.

And it’s clear why this sort of move has become necessary. The number of banks on the FDIC’s “problem list” rose by 36% from the end of the first quarter, to 416 from 305, representing $220bn in assets. This is the largest number on the problem banks list since June 30, 1994, the FDIC says, when there were 434 banks on the list. $220bn is the largest amount of assets belonging to problem banks since December 31, 1993.

Does it really matter if many, all of or even more than the 416 institutions on the problem list fail? After all, few of the institutions have bonds issued into the market, and healthy banks can pick up branch networks and insured deposits cheaply, in smaller echoes of JPMorgan’s purchase of Washington Mutual’s banks out of receivership. But markets should still be concerned about the US banks. After all, further special assessments, to raise money for the deposit insurance fund, cannot be ruled out, and that imposes a cost on every insured bank – and by definition the absolute cost is higher the bigger the bank.

More importantly, though, is the daunting mountain of real estate assets and non-performing loans that the FDIC will soon be tasked with auctioning off. Given the disproportionate concentrations of commercial real estate loans (and to be clear, these are often low quality tertiary properties, not landmark ones) held by the smaller banks in the US, this is one asset class where downward pricing pressure may continue. US banks with $1bn to $10bn in assets have 30% of their loan books in construction and commercial real estate loans – compared with just 6.2% at the banks with assets over $100bn. In the nearby charts, we have plotted data from the FDIC’s website. The chart on the left shows that severe problems in residential property persist. It shows that prices achieved as a percentage of last appraised value, on properties sold are collapsing (to 66% compared with 160% at the height of the bubble), even with the relatively minor increase in the number of properties sold in 2008 (especially compared with the numbers sold during the Savings & Loan debacle). The pricing of non-performing corporate loans (chart on the right) has not declined markedly over the past couple of years, which may be a reflection of the relatively lowly levered balance sheets of the commercial and industrial sector (i.e., compared with the property sector), though it’s not immediately obvious that this pattern will hold.

This ominous news continues to seep out from the stratum of smaller US banks, and contrasts strongly with the positive tone hummed by the larger banks (whose recent profitability has a lot to do with their extensive investment banking and trading operations). It is certainly not a reason for investors to run for the hills, but it does indicate to us just exactly how much work lies ahead in repairing the developed world’s broken banking systems. Recall, too, that crucial decisions – first and foremost, what to do with the mortgage behemoths Fannie Mae and Freddie Mac – have yet to be considered, let alone made.

There are a couple of interesting things on TV this evening, both on More4. At 10pm it’s True Stories: The Shock Doctrine, a film based on Naomi Klein’s book which looks at the way far right economists have used disasters around the world to impose extreme free market “solutions” (Milton Friedman and the Chicago School of Economics) on society. After this at 11.45pm it’s Enron: The Smartest Guys In The Room about the 2001 fraud at the US energy giant. On the same theme, (and you’ll only get tickets on eBay now), Enron, the play by Lucy Prebble has had fantastic reviews, and opens in London at the Royal Court Theatre on 17th September. Tickets are still available however for David Hare’s new play, The Power of Yes at the National Theatre, a quickly written piece about the collapse of the banks, and how only the rich were bailed out.

Changing topics, you may remember that one of our favourite economists over the course of the past decade was David Rosenberg, who headed up Merrill Lynch’s US economics team. He called the deflation wave very well and, like Robert Peston, had a “good war” as the credit crisis developed. David has since left Merrill to head back to his native Canada where he’s Chief Economist at Gluskin Sheff; but the good news is that you can now sign up for his excellent daily emailed views on the US economy for free, here.

Finally, I present to you an emerging markets investment opportunity. You can make loans to sub-investment grade issuers in low income economies, and the average default rate experienced so far is below 2%, compared with around 10% currently for US high yield companies. The default rate I’ve experienced so far is even better, at 0%, although I’m starting to sweat on a $25 loan I made to an Azerbaijan farmers cooperative. The catch of course is that this is micro-finance lending through Kiva.org, a US not for profit organisation, and the interest rate is zero (the yield on the emerging market government bond index is about 9% at the moment). Have a look at the website – you can choose entrepreneurs from all over the world, in many different industries, and lend as little as $25 each time.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.