Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

With only four more days of moustache shame left to endure, the M&G team is up to around £6000 raised for The Prostate Cancer Charity. With some offline donations and a generous contribution from M&G still to be added on, we should be nearing £9000 by Monday when this horror comes to an end. Thank you very much your kind sponsorship, it’s very much appreciated.

From left to right: Ben Lord, Stefan Isaacs, Gordon Harding, Richard Woolnough, Rob Burrows, Mike Riddell, Anthony Doyle, Jim Leaviss.

A couple of weeks ago I went on an incredibly useful trip to Frankfurt, where I met with some key policy makers from the European Central Bank and the Bundesbank, and discussed a range of issues including the timing of exit strategies and rate hikes, the inflation outlook, and the state of the banking sector.

This video was recorded in early November, and it’s interesting that many of the things I discuss have since become hot news, particularly regarding the timing of rate hikes (central bankers have repeatedly said they’ll stay low for ages) and the state of the European & German banking sectors (eg earlier this week, Dominique Strauss-Kahn, the managing director of the IMF, said that banks have only revealed about half of their losses).

PS The soundtrack is a bit more ‘eurotrance’ than usual – ideally we’d have had 99 Luftballons, which would have been apt, but unfortunately the copyright was too much!

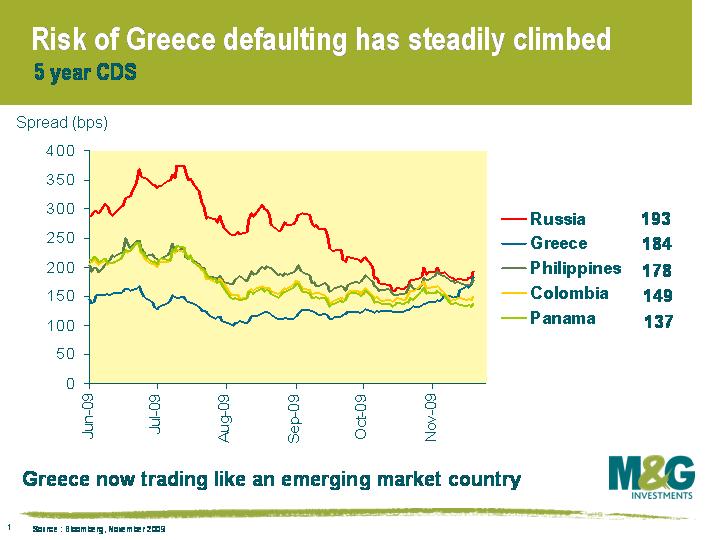

The original ‘Bond Vigilantes’ were the bond investors who reacted to authorities’ loose monetary or fiscal policies by forcing sovereign bond yields higher, thus punishing central banks or governments by increasing the cost of issuing further debt. Right now, the Bond Vigilantes are hunting around the world like a pack of wolves. Japan was the prey a few weeks ago (see recent blog comment here), but the winds have changed slightly and the wolves have caught a new scent. As the chart shows, the credit derivative market is implying that the risk of a Greek default in the next five years is about the same as the risk of a Russian default, and Greece is now deemed a higher risk credit than the Philippines (BB-), Colombia (BB+) or Panama (BB+). In fact this data is as at yesterday’s close, and Greek 5y CDS has today widened further to 182-87. At the beginning of November, 10 year Greek government bonds had an excess yield of 1.4% over German government bonds, and they now have an excess yield of over 1.7%.

It’s been known for a while that Greece has structural fiscal problems and unreliable statistics (in Trichet’s own words, there is a “problem with credibility”). The main issue facing Greece, however, is that neither the Greek authorities nor the Greek population seem prepared to do much about it. A new Greek government was voted in after the previous government lost the election that it itself called in an effort to win a mandate for its proposed package. In January this year, the Greek deficit was projected to be – 3.7%, but it’s been steadily revised upwards, to the point that the new government projects a 12.7% budget deficit for this year and 9.4% next year. The EC projects a more realistic deficit of 12.4% for 2010. (You may recall that a 3% budget deficit was originally an entry condition to join the Eurozone – it seems Greece has been fudging its budgets for a while).

Things have all properly kicked off in the last week couple of weeks. The European Commission highlighted that there has been a “lack of effective action” in Greece in sorting out its public finances, a statement that was probably a reaction to the less than credible budget put forward by the new government (increases in health, education and welfare spending, with little in the way of tax rises and spending cuts). Then last week it was rumoured that the Bank of Greece had advised Greek banks to sell part of their government bond holdings (officially denied), though it seems that they have asked Greek banks to be prudent and try to find alternative ways to fund themselves, as some of the extraordinary stimulus measures are being wound down. Investors are also concerned that Greek banks may find that Greek government bonds could become more expensive as collateral if further rating downgrades occur (the ECB has said that a haircut add-on will be applied to all assets rated below A-, which is where Greece is rated by Fitch and S&P, and Fitch has Greece on negative outlook). You can add into the mix the fact that the Greek economy is struggling versus its peers – unlike the Eurozone, which is out of recession, Greece is still in recession – and it becomes clear that the country is potentially facing a crisis.

If Greece doesn’t come up with effective measures in the next month, it will be given notice to take measures to remedy the situation under the Excessive Deficit Procedure (Maastricht Treaty). If it continues to misbehave, then it may face sanctions and the EC may require a non-interest bearing deposit (I’m not sure how effective these measures would be – will it help Greece’s problems if it starts getting fined as well?). Ultimately, though, it will be the bond vigilantes who move in for the kill, rather than the European authorities. This was echoed by the ECB’s Gonazales-Paramo last week, when he said that the debt markets will punish countries which don’t control fiscal deficits. And ‘punish’ is what the bond vigilantes are currently doing.

The following is a long piece, but we feel it has potentially dramatic implications for the bank bond market.

Last week saw the much anticipated capital raisings from Lloyds-HBOS and RBS. Lloyds has managed to raise £13.5 billion in new shares with HMT’s holdings remaining at 43%, whilst RBS has raised £25.5 billion from the Treasury, and a further £8 billion from the Treasury in the form of contingent capital notes. This sees the taxpayer’s economic interest in RBS rise to 84%. Lloyds is also raising between £7.5 billion and £9 billion from the exchange of old subordinated bonds (upper tier 2, tier 1 and preference shares) into new contingent capital notes.

Lloyds’ total capital raising sees it avoid the Government Asset Protection Scheme, wherein HMT guarantees 90% of losses incurred on a book of toxic assets, although it will have to pay £2.5 billion in break-up fee for the confidence boosting that the implicit support provided by the scheme has given to the company over the last 9 months or so. RBS, though, has not managed to avoid entrance into this scheme, but managed to reduce the amount of assets going into the protection scheme from £325 billion to £282 billion. As a sign of the toxicity of these assets, though, RBS’ first loss piece was increased by £20 billion to £60 billion.

But there is a cost to both these companies for their needing substantial government support, and for, indeed, almost bringing down the UK economy. Indeed, last week’s actions clearly indicate that RBS remains entirely reliant on the government money for its survival. The EC has ordered Lloyds to shed 4.6% of its current account market share, and 19% of its UK mortgage market share, by 2013, with a clear drive to try to reduce concentration in the banking system and to avoid banks being ‘too big to fail’. RBS once again comes off worse from this part of the restructuring: RBS will be forced to sell its insurance businesses, arguably the most attractive part of the group at the moment, as well as large numbers of branches in the UK, its payment processing business and its interest in a commodity trading arm. Ultimately, we feel that it is in some way right that Lloyds is given the chance to make a clean break from the APS, given that it bailed out HBOS at the height of the UK banking sector’s woes and at the same time decimated its theretofore strong franchise. RBS, in contrast, was not so much a solution as a large part of the problem, and in some way has been and will continue to be treated as the UK banking sector’s whipping boy.

But the most relevant part of all this to us as bondholders, aside from the clear and much-needed improvements in the equity positions of the two banks, is the liability management exercise being undertaken by Lloyds to generate £7.5 billion in contingent capital from exchanging existing subordinated noteholders. On top of ordering the two banks to sell parts of the businesses, the EC has also ordered that the two banks cease payments of all discretionary coupons on subordinated debt (to not pay coupons on senior debt or lower tier 2 is, currently, an event of default) from January 2010 to January 2012. This is a very substantial development, and one that we have been expecting to be imposed on problematic banks for quite some time. It appears that large numbers of deeply subordinated bank bonds are going to become non-coupon paying for the next two years, and there will be no calls over that period either. We are a step nearer to zero coupon paying perpetuals!

So the response from Lloyds? Astonishingly, the bond exchange has been designed to take out some of the bonds that the EC would have enforced non-payment on, swapping instead into a must-pay security. But the EC’s push to enforce non-payment of coupons was presumably justified by the need to preserve cash within the business rather than leaving it? So either you hold your old Lloyds hybrid notes and take a 2 year payment and call holiday, or you exchange into the new contingent capital, or CoCo, bonds, that must pay coupons unless converted to shares. And in our view, from the banks’, regulators’ and the taxpayers’ perspectives, the new capital notes are a very good idea. Simply put, you get a bond that must pay coupons each year, and that have a definite maturity of 10 to 20 years (like a senior bank bond or a corporate bond). But: if the bank gets into trouble, and its core capital falls below a certain level (5%), then your bond gets automatically converted to common stock. We here think that this is the future of the hybrid capital note market. In times of trouble these subordinated bonds will actually convert to equity (just when banks need it most!). We got into this banking crisis thinking the banks were ‘well capitalised’, and we soon found out that most of their capital was more bond-like than equity-like, which wasn’t much of a help at all to a severely under-capitalised banking system. These CoCo’s would correct that. Good.

But there is a plethora of problems and inconsistencies with these new bonds. Regulators have agreed to allow these CoCos to be mandatory pay securities, so cash will continue to exit the business to pay coupons, which is exactly what the EC wanted to stop. Furthermore, to entice old bondholders to exchange into the new notes, and to reflect the increased risk of a mandatory conversion to common equity, Lloyds is offering coupons on the CoCos that are 1% to 2% higher than the old subordinated bonds. So even more cash will be leaving the business than before! Moreover, the bonds have been classified as lower tier 2 for purposes of seniority of payment and in liquidation, but regulators will consider them at the same time as contingent core tier 1 capital: isn’t that a contradiction in terms? It seems to us that regulators are being overly accommodative to get this deal done, and to help recapitalise Lloyds, and to open this new CoCo market. We do expect other banks to explore the feasibility of similar issuances once the market has got used to this one. From bond investors’ points of view, though, these look like bonds until distress, in which case you are automatically converted to common stock (unlike convertible bonds, where it is generally your right, not obligation, to convert). So they don’t naturally fit into the fixed income universe. At the point of conversion, given distress, the shares will be worth very very little. And the risk of Lloyds-HBOS’ core capital falling to or below 5% is non-negligible, in our view, especially in the next 3 years. Finally, given how high the coupons are going to be, isn’t a management team or regulator at some point going to be incentivised to manipulate their capital levels to force conversion of this expensive debt into cheap equity?

We don’t think that these bonds naturally fit into the fixed income space, although the yields do look attractive. Thus, if other, stronger banks bring similar deals, where there is a premium paid for potential equity conversion over existing tier 1 yields, and where we feel the risk of exchange to equity is sufficiently remote, we will consider them carefully. However, there are still several potentially large issues for these notes, nicely exemplified by a certain index provider’s excluding them from the index on Tuesday, then re-including them, and then yesterday re-excluding them. This shows how difficult is it to know whether they should be classified as fixed income or equity. And that would suggest that the powers that be are worried about who exactly will buy these new CoCo The Clown notes. Are these clowns happy, or are they sad? Are they bonds or are they shares?

The M&G Bond Vigilantes are growing some very fine moustaches in aid of the Prostate Cancer Charity. We’re less than two weeks into Movember and already the bond desk looks like the Hulk Hogan Appreciation Society crossed with the Village People. We’ll post links to our progress as the month progresses (and maybe even photos), and you’ll be able to rate our efforts from the 15th Movember. If any of you would like to make a donation to this excellent charity, we’d be very grateful. All of our retail fund managers and blog contributors are taking part and you can donate to individuals, or to the whole team, via the link below.

Thank you for supporting the bond market’s best moustaches

Whilst scanning the local news website in Sydney for the Melbourne Cup winner (it was Shocking for those antipodeans that are interested), I stumbled across an interesting article that features an ex-colleague of mine. Rory Robertson, an interest rate strategist at Macquarie Group, bet University of Western Sydney associate professor of economics and finance Steven Keen that Australian house prices would not fall 40 per cent within a year. The loser of the bet had the fun task of walking over 200km from Canberra to Mount Kosciuszko (Australia’s tallest mountain) wearing a t-shirt that says “I was hopelessly wrong on house prices! Ask me how.”

Dr Keen (or the “Merchant of Doom”) will be starting his trek in April. His reasons for forecasting the massive fall in house prices were a large build up in debt by the average Australian homeowner, an increase that he believed was similar to the Japanese experience between 1991-2006. Dr Keen expected that many homeowners would have to default on their home loans in an environment of weakening demand and rising unemployment. This scenario has not eventuated and house prices in Australia have in fact risen over the last year.

I have written before on the strength of the Australian economy. China’s insatiable demand for commodities has boosted mineral exports and provided a fillip for the Australian economy when most other developed economies have struggled to return to growth. Australia has now raised interest rates twice and the market is pricing in a good chance of a third hike in December, which has contributed to the Australian dollar being the best performing currency this year. The positive outlook for the Australian economy has led us to increase exposure to Australian assets and we have bought both Australian corporate and government debt.

The scenario that Dr Keen forecast has in fact played out on the other side of the world, in Ireland. Builders in Ireland are now selling homes for less than they cost to build. With no currency to devalue, no control over monetary policy and relatively high wages, Ireland has found it difficult to regain its international competitiveness. It is hard to see what will drive growth in Ireland over the short to medium term and result in a return to positive growth. Earlier this week, Fitch cut Ireland’s sovereign rating from AA+ to AA-, citing the severity of the decline in nominal GDP and the exceptional rise in government liabilities. In terms of the housing market, eventually house prices should get so cheap that prices will stabilise and demand returns. But until Ireland works off the extra supply of homes that were built during the boom years, prices will continue to fall. And that will take time.

Earlier today the Bank of England announced that along with keeping the bank rate at 0.5% it is to increase the QE program by a further £25bn over the next 3 months. Whilst an increase was somewhat expected by the market gilts have sold off, the yield on the 3 3/4 2019 rose to 4% earlier as it seems to have expected a larger commitment. Even though we had a GDP print of -0.4% recently it seems the Bank is laying the groundwork for stepping away from the bond purchases. Considering they have bought back £175bn worth of gilts since March and now they are planning to do £25bn over the next 3 months it definitely feels like they are turning down the dial. By my basic calculations the rate of increase has reduced by roughly 70% (originally they were buying £25bn per month and now that has fallen to £8bn per month). Hopefully this reduction will strike the right balance between helping the economy get back on its feet and allowing the Bank to hit its inflation target. We should get further colour on their thinking when the quarterly inflation report is released on the 11th.

We had a number of correct entries to our QE prediction competition so in the interest of fairness we have drawn a name out of a hat. The winner is Peter Lowe at Smith & Williamson. Congratulations and we hope you enjoy the book.

Earlier today the Bank of England announced that along with keeping the bank rate at 0.5% it is to increase the QE program by a further £25bn over the next 3 months. Whilst an increase was somewhat expected by the market gilts have sold off, the yield on the 3 3/4 2019 rose to 4% earlier as it seems to have expected a larger commitment. Even though we had a GDP print of -0.4% recently it seems the Bank is laying the groundwork for stepping away from the bond purchases. Considering they have bought back £175bn worth of gilts since March and now they are planning to do £25bn over the next 3 months it definitely feels like they are turning down the dial. By my basic calculations the rate of increase has reduced by roughly 70% (originally they were buying £25bn per month and now that has fallen to £8bn per month). Hopefully this reduction will strike the right balance between helping the economy get back on its feet and allowing the Bank to hit its inflation target. We should get further colour on their thinking when the quarterly inflation report is released on the 11th.

We had a number of correct entries to our QE prediction competition so in the interest of fairness we have drawn a name out of a hat. The winner is Peter Lowe at Smith & Williamson. Congratulations and we hope you enjoy the book.

It’s been quite a year to date for leveraged finance. Improving economic data, increased risk appetite and a supply/demand imbalance has driven valuations starkly higher. At the time of writing, the Merrill Lynch European High Yield Index is up a whopping 75%, the average bid for leveraged loans in Europe has risen by around 50% from its lows earlier in the year, and the high yield new issue market has reopened to all but the most speculative propositions printing approximately €20bn year to date.

Such a reversal in fortunes is bound to be met with raised eyebrows. Standard & Poors, in a report released last month asked ‘Is History Repeating Itself In The European High Yield Market?. The report identifies four areas where it claims the European high yield market is at risk of repeating past mistakes. I thought it would be worth taking a brief look at each.

The first area relates to pricing. ‘The lack of returns in money markets and investment grade bonds may be prompting new investors to enter the European high yield market, compressing spreads as volumes remain low’according to S&P. I have some sympathy with this notion. The lack of supply in the earlier part of the year combined with a near zero interest rate policy has undoubtedly forced less traditional investors to consider high yield risk. The huge oversubscriptions that new high yield transactions have garnered in recent months are, in part, testament to the idea. There is evidence that suggests that this interest has broadly targeted the stronger high yield credits and in itself has not been the major driver of lower spreads. An improving default outlook and economic backdrop has likely played a greater part.

The second area of concern relates to the recent non-rated issuance. ‘Anecdotal evidence suggests that much of the demand of unrated deals comes from private banks and other relatively new players’according to the report. I suppose we have to take this gripe with a pinch of salt. S&P are clearly incentivised to ensure the status quo of obtaining a rating prior to, or shortly after, coming to market. That said I don’t doubt that a number of investors have bought recent unrated transactions without the skills to fully analyse these investments.

The third area relates to the structuring of transactions. This and S&P’s final point are those with which I have the most sympathy. ‘Bond covenants have not been particularly strong for unsecured high yield debt’according to S&P. The ability of bondholders to protect their interests (and interests in the event of distress) will largely come down to the covenants that are put in place at the time a deal is structured. Indeed, a number of recent high yield transactions have come to market with the lack of covenant protection usually associated with investment grade rated transactions. This has been a major issue for us for a number of years (we have blogged on the subject on numerous occasions) and this has been one of the most important determinants when deciding on new transactions. Furthermore, we have long been advocates of a move to a US style approach of disclosing bank debt covenants. These covenants remain ‘private’ in Europe despite the dangers that this presents to investors.

The fourth and final area relates to disclosure. Historically high yield lenders receive detailed quarterly company reporting, whereas bank debt investors receive monthly updates. The more recent trend for certain high yield issuers has been for semi-annual reporting without an acceptable degree of detail.

Looking at the high risk end of the credit spectrum, it’s worth noting that CCC issuance has been notably absent so far this year. For example, a recent speculative transaction for Donington Park failed to get out of the pit-lane due to a lack of investor demand. Both are signs that we have yet to retest the heady heights of 2006 where credit was bountiful and there was a boon in speculative-grade bonds. That said, we are clearly trending back in that direction if spreads continue to compress for this type of debt. Such a trend will require close monitoring.

The year is 2020, and at the centre of the financial tsunami is Japan. Another decade of very low single digit growth has meant that debt to GDP has steadily climbed from 200% in 2010 to 300%, which is considerably higher than any other country. Another ‘lost decade’ has meant that the Japanese government has been unable to meaningfully cut back on spending or increase taxes, since such behaviour would have risked plunging the economy back into recession and deflation. Nominal tax revenue has been static for twenty years. Worsening demographics have meant that social security costs have skyrocketed – in 2010, 23% of the population was above 65 years old, but this has risen to 30% in 2020.

All the things that kept Japanese government bond yields so low through the 1990s and 2000s have begun to unwind. Demand from the postal savings and postal insurance systems, which held over 30% of all JGBs in 2010, has begun to wane due to the meagre returns on offer in domestic savings. The public pension fund, which held 12% of JGBs in 2009, is steadily redeeming its holdings, since JGBs no longer meet the fund’s required return, and the fund has had to sell assets to meet rising cash outflows. The average individual’s savings rate has steadily fallen, in line with the rapidly aging demographic (the propensity to consume for pensioners is about 120%). Japanese institutional and private investors have traditionally exhibited exceptionally strong home bias, holding over 90% of outstanding JGBs, but domestic demand has rapidly weakened as globalisation of financial markets and the lure of greater returns on overseas assets have resulted in domestic investors diversifying geographically.

Financial markets are getting deeply concerned that Japan will struggle to service its debts. Japanese investors are worried about the Japanese authorities attempting to inflate their way out of the problem and are increasing exposure to overseas markets. A wave of selling has meant that the Yen has weakened and Japanese government bond yields have started to rise sharply. The rise in yields means that the maturing low-coupon JGBs that were issued 10-20 years ago are having to be replaced by higher coupon bonds. Interest payments on sovereign debt are rapidly approaching tax revenues. The Yen is not a global reserve currency, and Japan can’t rely on capital inflows from abroad to fund its deficits. The country is on the brink of getting junked by the rating agencies. Financial markets are wondering what happens when one third of the world’s government bond market defaults in one go.

The year is 2009 again. Thankfully, the nightmare scenario above hasn’t happened, but how realistic is it? Rising sovereign indebtedness has been a very hot topic over the past 12 months (I wrote about it in June here), and having recently read an excellent research note from JP Morgan (which I’ve drawn from heavily above), it’s entirely plausible that Japan could be at the epicentre of a sovereign debt crisis.

A wave of sovereign defaults becomes all the more plausible if you read ‘This Time is Different : Eight Centuries of Financial Folly’, which is the recent publication from Carmen Reinhart and Ken Rogoff (Rogoff almost uncannily foresaw the collapse of Lehman Brothers – see here). The book is based on two highly influential academic papers published last year, (This Time is Different : A Panoramic View of Eight Centuries of Financial Crises and The Aftermath of Financial Crises), and is a ‘must read’ for any bond investor. Looking back over the centuries, they highlight that at the moment we’re in a typical lull in sovereign defaults, one or two decade lulls in defaults are not uncommon, and each lull has invariably been followed by a new wave of defaults. History tells us that there have been numerous periods where a high percentage of all countries are in a long period of default or restructuring.

I suppose that the goodish news is that if the terrible scenario described in the first three paragraphs above does occur, then it’s very unlikely to happen anytime soon. A high sovereign debt to GDP ratio does not mean that paying interest on the debt is necessarily that difficult – again citing JP Morgan, Japan’s debt service cost in 2008 was a very manageable 2.6% of nominal GDP, smaller than the US’s 2.9% and the Eurozone’s 3.0%. Sovereign debt levels are – for the next few years at least – easily sustainable in Japan and the rest of the developed world.

Another piece of good news is that default or restructuring is not inevitable. Canada is a good example of a country that lost its AAA rating in the 1990s, cleaned up its balance sheet, and is now one of the world’s strongest sovereigns (although Canada was arguably in a much stronger position in the mid 1990s than much of the world is in today).

The reaction of the authorities around the world to this crisis over the past year is, in my view, to be greatly admired. There have been mistakes and delays, but errors cannot be helped when such huge decisions need to be made in such a short period of time. The world has experienced much pain, but we can only guess at how many more times worse it could have been. There is no doubt, though, that some of the biggest challenges lie ahead, and as highlighted in the horror scenario above, if politicians fail to take brave and decisive actions over the coming years, then things will get much, much worse. These are issues that politicians are very aware of, but dealing with them is easier said than done (as an example, you can read about how Germany is trying to tackle the issue here).

Finally, we have a copy of Reinhart and Rogoff’s book mentioned above for our readers. The quantitative easing multiple choice question is this – on Thursday this week, how much will the UK’s MPC decide to extend asset purchases by – (a) nothing (b) £25bn, (c) £50bn or (d) other? The first correct answer drawn out of a hat later this week wins. To view the Terms and Conditions of the competition, please click here. Once you have read the T&Cs , please use the ‘get in touch’ function on this blog to enter.

This competition has now closed.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.