Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

Thank you for all the entries – we had twice as many as last year’s bumper haul, and the average mark is creeping up too. The answers are shown below. Here are the winners – there’s an extra runners-up prize so everybody who scored 18 or better gets something.

First prize: Tom Lees with the only full house, 20/20

Runners-up: Lisa Taylor of ICAP (19), Nick Tudball of BNP Paribas (19), Mike Schmidt of Tricorn Partners (18), Alex Wall of Lloyds Banking (18), and Eirian Jones of Lord North (18).

Best M&G staff entry: Dominic Harlow, Marketing (17).

Have a great Christmas everybody, and congratulations to the winners. You’ll hear from us shortly.

1) There are five European capital cities that are home to Champions League/European Cup winning football teams. What are they?

Madrid, Lisbon, Amsterdam, Bucharest, Belgrade. Glasgow is not the capital of anything by the way.

2) An ounce of gold currently costs approximately $1150. What price per ounce did Gordon Brown get for the first tranche of the UK’s 125 tonnes of gold reserves when it was auctioned in July 1999?

$261.20

3) What is defying its name and stops being circular this month?

The Circle Line on the London Underground now spirals from Hammersmith, through the City, and back west to Edgware Road, rather than being the loop around the centre that it used to be.

4) Moore 64, Picasso 73, Warhol 75, and Haring 88. What was 77?

The Queen and the Queen Mother. This refers to labels on bottles of Chateau Mouton Rothschild. Each year a famous artist produces a painting for the label, but in 1977 there was a special label to commemorate the visit of the Queen and Queen Mother to the chateau.

5) Bud Light used to be the biggest selling beer in the world, but in 2008 it was overtaken by which brand?

Snow, the Chinese beer brand.

6) Finding what would explain how particles with no mass can make up matter which has mass?

The Higgs boson.

7) If this was a joke, what’s the difference between bird flu and swine flu?

One requires tweetment, the other requires oinkment.

8) BA001 used to take half the time of a standard flight to get from London to New York. It now takes over 2 hours longer – why?

This used to be the supersonic British Airways Concorde flight, but this year BA resurrected the flight number for its London City to JFK flight, which, because of a short runway at City Airport, has to stop for fuel in Shannon, Ireland, hence the longer than usual flight time. You had to get both parts of the question right to get the point (i.e. why was it shorter, and why is it now longer).

9) In November this year, what became the biggest grossing entertainment release of all time, with a worldwide gross of over $500 million in under a week?

Call of Duty: Modern Warfare 2, the console game. Lots of people said New Moon, which might well be true of its cinema take, but the video game outsold it.

10) Which artist wowed crowds this autumn with a show that included the regular firing of a red wax shell from a cannon at the gallery walls?

Anish Kapoor.

11) What topped the NME’s “best album of the last ten years” list?

“Is This It” by The Strokes.

Optional bonus question – was there a better album, and if so what is it? Suggestions will go to the kangaroo court and may be awarded an extra point if we go,” you know what, that WAS a better album”.

No bonus marks were awarded. Perhaps the nearest I came to it was with the suggestion of the Arctic Monkeys first album, but I also nearly removed marks in a fury when I read some of the drossy suggestions, so count yourselves lucky.

12) Covered bonds and Residential Mortgage Backed Securities are both fixed interest instruments secured on home mortgages. What is the significant difference between the two?

Banks issuing Covered Bonds keep the residential mortgages on their balance sheet, whereas RMBS see the mortgages removed from their balance sheet completely.

13) So far in 2009 which artist’s painting has sold for the highest amount at auction (and although it’s a high number, it’s only 50% of 2008’s most expensive work of art)?

Henri Matisse (Les Couscous, Tapis Bleu et Rose, 1911) $46.5mn. We had a small panic with a handful of people who suggested Titian’s “Diana and Actaeon” which was bought by the National Gallery of Scotland and National Gallery in London, for about £50 million at the start of the year – but the question does ask for auction results, and the Titian sale was part of a more complicated deal (not an auction), and the money will be paid in instalments over three years. Also, Raphael’s Head of a Muse recently became the most expensive drawing of all time, selling for $47.9 million in December. But we asked for a painting, and this isn’t one.

14) “A great vampire squid wrapped around the face of humanity, relentlessly jamming its blood funnel into anything that smells like money”. What?

Goldman Sachs, according to Rolling Stone magazine.

15) Which James Bond film has the longest title?

On Her Majesty’s Secret Service.

16) Which Arabic word meaning legal instrument or deed is used to describe bonds structured in order to comply with the Islamic prohibition on charging interest?

Sukuk.

17) Which headline-grabbing celebrity’s real name is Eldrick?

Tiger Woods.

18) Which cocktail is made from lemon juice, 1 shot of gin, 2 shots of cherry brandy, soda water, and ice?

A Singapore Sling. Not that it impacted the final results, but we also gave marks for the Eton Highball, which looks pretty similar (although possibly has less cherry brandy in it?).

19) What’s the proper name of the instrument made famous by George Formby?

The Banjolele (or variations on banjo-ukulele). No marks for the ordinary ukulele.

20) For which charity did the M&G Bond Vigilantes grow moustaches last month?

The Prostate Cancer Charity. The final amount raised was £14,345.

As BA goes to court to try to stop the 12 Days of Christmas strike by its UNITE cabin crew members, I dug out the paper mentioned in the Times yesterday about the impact of striking on workers’ pay. The paper is called Do strikes pay? by Metcalf, Wadsworth and Ingram, and you can read it here (scroll down to section 9 on page 179). Having done a comprehensive analysis of strikes in the UK in the 1980s, the authors concluded that going on strike boosted workers wages by just 0.3%, and that given the average strike length was 11 days, “the ‘average’ strike is unlikely to be a good investment (for the strikers)”. They do caveat their findings – the mere threat of strikes, without there actually being one, might elevate pay levels, and having to follow through with the threat periodically is necessary to show the employer that the threats are credible. In addition, striking by some workers might lead to the small gains being won even by non-striking workers (even in related industries, or at competitor firms) increasing the overall benefit to workers. Finally, non-wage gains might be realised which are not included in the analysis. However, even with these caveats, losing around 4.5% of an annual wage (11 days out of 250 working days) to gain 0.3% per year doesn’t look compelling.

As for BA, we rate it as a BB high yield company. Its 5 year CDS spread is currently at 500, implying an annual 7% default probability on average over the next 5 years (assuming a 30% recovery rate). Its 1 year CDS is only 200 however, which suggests that the market doesn’t believe that this strike will prove to be terminal for the airline. The good news for BA is that it does have a lot of cash on its balance sheet, and also that there has been a return of passengers to the premium cabins on its expensive London to New York routes. The bad news is its £3.7 bn pension fund deficit and a rising trend in fuel costs. We don’t own any of their debt.

Lastly, a final call for all Christmas Quiz entries. Gates will be closing at 5pm on Friday. Frequent Fliers are reminded of the “one entry per person” rule. I’m looking at you Lisa Taylor.

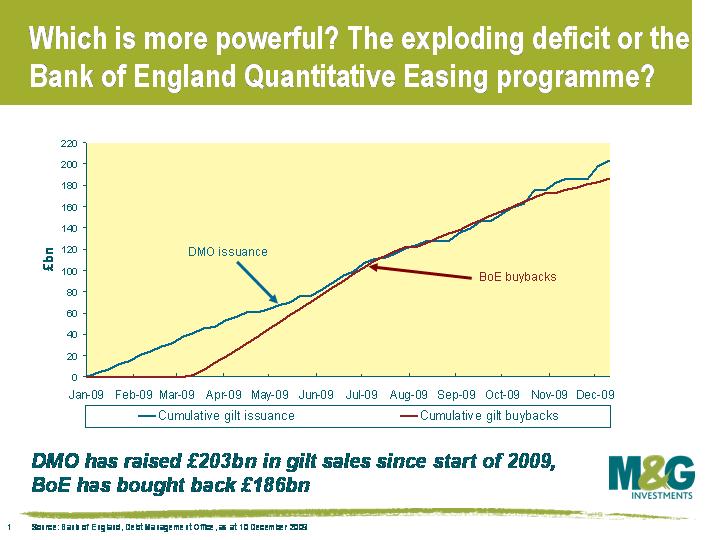

In last week’s Pre-Budget report, UK Chancellor Alistair Darling announced that gilt issuance for the current financial year would total £225.1bn – a shocking and record figure, although not far off the £220bn that was originally planned in this year’s Budget. But while on one side we’ve had this huge volume of supply from the DMO, we’ve also had the unusual situation of the BoE busily mopping up gilts at a frantic pace. In fact as this chart shows, in Q2 and Q3 of this year, the BoE was actually buying gilts back faster than the DMO could issue them. This massive demand for gilts has kept a lid on gilt yields – 10 year gilt yields today are where they were at the beginning of June.

In last week’s Pre-Budget report, UK Chancellor Alistair Darling announced that gilt issuance for the current financial year would total £225.1bn – a shocking and record figure, although not far off the £220bn that was originally planned in this year’s Budget. But while on one side we’ve had this huge volume of supply from the DMO, we’ve also had the unusual situation of the BoE busily mopping up gilts at a frantic pace. In fact as this chart shows, in Q2 and Q3 of this year, the BoE was actually buying gilts back faster than the DMO could issue them. This massive demand for gilts has kept a lid on gilt yields – 10 year gilt yields today are where they were at the beginning of June.

However, the demand/supply dynamic is changing and is set to change further. Looking at demand, the pace of buybacks has recently slowed considerably, as pointed out by Richard here. In November, the BoE ‘only’ increased the scale of QE by £25bn versus a £50bn increase previously, and year to date gilt issuance has once again overtaken the volume of BoE buybacks. In terms of supply, we still have around £50bn of mainly conventional gilt issuance to come over the remainder of this financial year, followed by another £174bn in the pipeline for 2021/12 and probably a similar amount the following year.

The quantitative easing pressure cooker has clearly kept gilt yields lower than they would have been in its absence, but the worry is what will happen once the lid is eventually taken off. Who’s going to buy the gilts? Will the gilt market bubble over and make a big mess?

You shouldn’t underestimate the power of the authorities to find new ways of generating domestic demand to keep sovereign debt yields yields suppressed, as the Japanese experience of the past decade has shown, and in the UK we’ll see that a significant part of next year’s gilt supply will find its way onto banks’ balance sheets. But in our view there’s a greater risk that gilt yields will rise from here rather than fall, and the prospect of a hung parliament and the potential for a UK credit rating downgrade increase the risks.

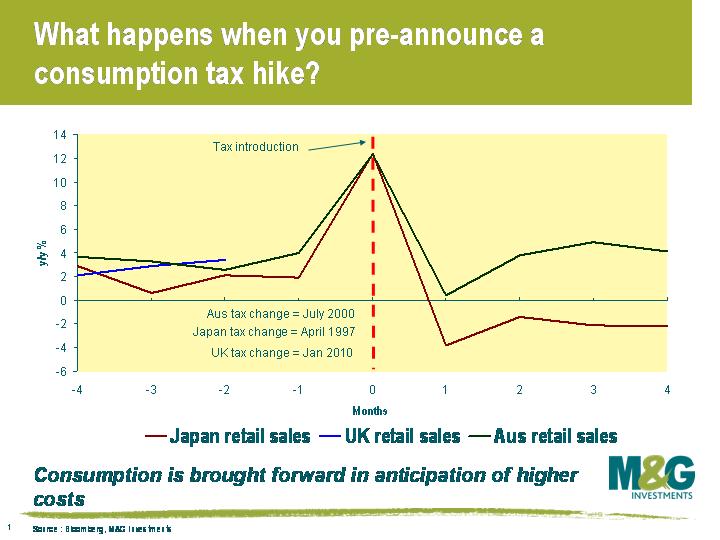

In under a month’s time, the UK’s emergency VAT reduction from 17.5% to 15% will be reversed. This will not only cause a blip upwards in inflation rates (most of the CPI basket apart from food attracts the tax) but might also derail the recovery of the UK economy. Because this VAT hike is pre-announced, is it possible that we will see lots of frontloading of consumption in December, and a big fall back in 2010? After an understandably weak 2008 and first half of 2009, it looks like retail sales have started to pick up. The British Retail Consortium reported yesterday that November hadn’t been as strong as expected, partly due to a big fall in food inflation, but like-for like sales in non-food items were up 3.3% from last year.

This chart shows what happened in other countries around the time of a pre-announced increase in consumption taxes. Perhaps the most famous example came in Japan in 1997. Although it had formally come out of recession, annual growth had not convincingly risen above 2% for 3 years, compared with an average of nearly 5% in the boom years of the 1980s. Yet because, like the UK, the fiscal position was poor, consumption taxes were hiked from 3% to 5%. As you can see, in the month before the tax hike came into effect, retail sales were up by around 12% year on year.

This chart shows what happened in other countries around the time of a pre-announced increase in consumption taxes. Perhaps the most famous example came in Japan in 1997. Although it had formally come out of recession, annual growth had not convincingly risen above 2% for 3 years, compared with an average of nearly 5% in the boom years of the 1980s. Yet because, like the UK, the fiscal position was poor, consumption taxes were hiked from 3% to 5%. As you can see, in the month before the tax hike came into effect, retail sales were up by around 12% year on year.

The following month, post the consumption tax increase, retail sales plummeted, and in Japan’s case retail sales remained extremely weak for months afterwards. It looks therefore that the impact of the tax hike was to bring forward consumers’ purchasing decisions in order to mitigate the impact of that tax, an entirely rational thing to do. I would guess therefore that in the run-up to Christmas the UK will see bumper sales – especially of big ticket, non-food items. But the impact of the VAT hike in 2010 will be to slow things down dramatically – with the caveat that the first half of 2009 was so weak, that the year-on-year numbers might look respectable without it necessarily being a cause for celebration from the retailers.

But there might be worse to come. If the Conservatives are elected to government in May or June, they would call an emergency Budget. They haven’t announced any plans to do so, but many expect a further rise in the VAT rate to 20% (Vince Cable of the LibDems said that the Tories would hike to 25%!).

We’ve also shown the Australian example on the chart above. In contrast to the UK and Japanese examples, Australian economic growth was strong in the run up to the consumption tax hike in July 2000. As a result, whilst retail sales did spike up ahead of the tax introduction, they didn’t fall back so aggressively the following month, and indeed by the next month they were back to normal levels. It’s much less messy to tighten fiscal policy when the economy is in good health, than when it’s not – obviously. But it does make you worry that the UK’s VAT hike might provoke a double-dip in a nation where consumption remains nearly 2/3rds of the economy. Post the April 1997 Japanese tax rise, the economy slipped back into recession with average quarterly negative growth of around 0.3% for the next 2 1/2 years!

And from a purely selfish viewpoint, I’m sure I’ve told you about my mental block about buying a new television. My current one is over ten years old, is deeper than it is wide, and the on/off button broke in 2004, so since then it has to be turned on or off from the plug socket. I still maintain that it has a better picture than the flashy, but poor quality, 50" flatscreen sets that the youngsters on the desk got jobbed into in Dixons a couple of years ago – but technology has moved on, and it’s probably time to buy a new one. Do I buy now, and achieve a guaranteed 2.5% discount relative to January’s higher VAT prices, or do I wait until the New Year, when VAT is higher, but where the retailers are much, much more desperate to sell me one?

Here is this year’s Christmas Quiz. Please email us your entries by 5pm on Friday 18 December. First prize is £100 of Amazon vouchers and there are 4 copies of “Too Big To Fail” by Andrew Ross Sorkin (in which Hank Paulson accuses Alistair Darling of doing something too rude to repeat in this blog) for runners-up. As usual the competition is open to all of our readers, clients or not, and as usual you probably won’t need a full house to win the prizes.

1) There are five European capital cities that are home to Champions League/European Cup winning football teams. What are they?

2) An ounce of gold currently costs approximately $1150. What price per ounce did Gordon Brown get for the first tranche of the UK’s 125 tonnes of gold reserves when it was auctioned in July 1999?

3) What is defying its name and stops being circular this month?

4) Moore 64, Picasso 73, Warhol 75, and Haring 88. What was 77?

5) Bud Light used to be the biggest selling beer in the world, but in 2008 it was overtaken by which brand?

6) Finding what would explain how particles with no mass can make up matter which has mass?

7) If this was a joke, what’s the difference between bird flu and swine flu?

8) BA001 used to take half the time of a standard flight to get from London to New York. It now takes over 2 hours longer – why?

9) In November this year, what became the biggest grossing entertainment release of all time, with a worldwide gross of over $500 million in under a week?

10) Which artist wowed crowds this autumn with a show that included the regular firing of a red wax shell from a cannon at the gallery walls?

11) What topped the NME’s “best album of the last ten years” list?

Optional bonus question – was there a better album, and if so what is it? Suggestions will go to the kangaroo court and may be awarded an extra point if we go,” you know what, that WAS a better album”.

12) Covered bonds and Residential Mortgage Backed Securities are both fixed interest instruments secured on home mortgages. What is the significant difference between the two?

13) So far in 2009 which artist’s painting has sold for the highest amount at auction (and although it’s a high number, it’s only 50% of 2008’s most expensive work of art)?

14) “A great vampire squid wrapped around the face of humanity, relentlessly jamming its blood funnel into anything that smells like money”. What?

15) Which James Bond film has the longest title?

16) Which Arabic word meaning legal instrument or deed is used to describe bonds structured in order to comply with the Islamic prohibition on charging interest?

17) Which headline-grabbing celebrity’s real name is Eldrick?

18) Which cocktail is made from lemon juice, 1 shot of gin, 2 shots of cherry brandy, soda water, and ice?

19) What’s the proper name of the instrument made famous by George Formby?

20) For which charity did the M&G Bond Vigilantes grow moustaches last month?

Click here to email your entry. Click here to read terms and conditions. The information we collect from you is solely used to contact you in the event that you have won a prize. This competition is closed.

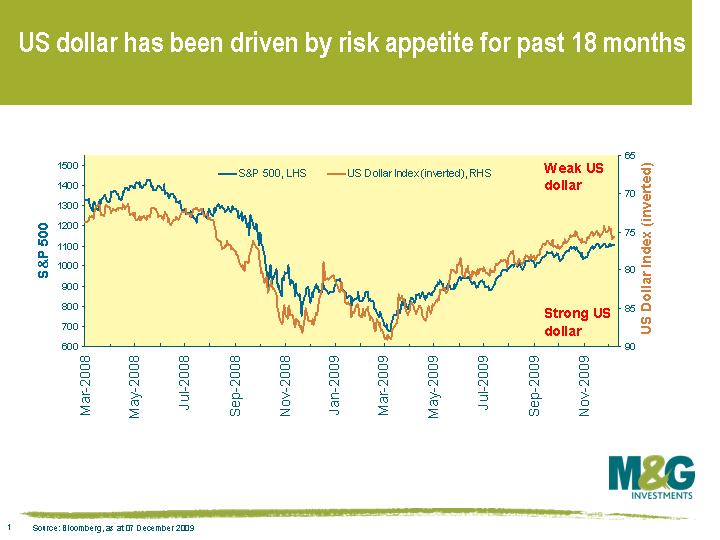

The behaviour of the US Dollar over the past few days has left investors a bit stumped, and the FT have been asking the same question in today’s Short View column. Friday of last week saw the biggest rally in the US Dollar since January as an unexpected drop in the unemployment rate led to speculation that the Federal Reserve will lift interest rates by the middle of next year. Yesterday the dollar continued to gain against the euro, which has been attributed to Bernanke’s comments that the US economy faces “significant headwinds” and inflation could move lower. Surely weak growth and subdued inflation suggests no pressure to raise US rates, so the thing that apparently drove the US dollar yesterday was the opposite of what influenced the US dollar on Friday.

People try to attribute all sorts of things to the performance of the US dollar, but the reality is that for the last 18 months, or until last Friday anyway, the performance of the US dollar has been almost entirely due to whether the world’s investors were in a mood for risk taking or risk aversion on any given day. This can be seen in the attached chart, which plots the S&P 500 versus the US Dollar Index, where the Dollar Index measures the US dollar against a basket of six major currencies. The two indices have tracked each other particularly closely over the past six months, with a correlation of -0.94.

The close negative correlation between the US dollar and risky assets can be explained by the currency carry trade. The carry trade rapidly unwound post Bear Stearns ‘s rescue in March 2008, resulting in lower yielding, lower risk currencies such as the US Dollar and Japanese Yen outperforming. This year, the carry trade is back, as risk seeking investors have taken advantage of low US interest rates to borrow in US dollars at a cost of next to nothing, and have used the proceeds to invest in higher yielding currencies such as the Australian Dollar or Brazilian Real.

Last Friday, US non-farm payroll data caused the correlation to wobble. While the payrolls figure was still negative, data came in much stronger than expected as US employers cut the fewest jobs last month since the recession began. The US unemployment rate unexpectedly fell from 10.2% to 10.0%. European equity markets jumped 1.5% on the news and government bonds sold off reasonably sharply. You’d normally expect to see the US dollar weaken in this environment of risk appetite, however the US dollar actually rallied more than 1% against the Aussie Dollar and Norwegian Krone, and rallied 1.5% against the euro and more than 2% against the Japanese Yen.

As Jim explained in a recent teleconference, the Federal Reserve has not traditionally started hiking rates until unemployment has been falling for a while. Strong unemployment figures therefore increase the risk that the Fed will start hiking rates next year. If the Federal Reserve does start to hike rates, it has the potential to dramatically alter the way the US Dollar behaves. For proof of this, you need look no further than what happened between March 2004 (when the markets began pricing in a series of Fed rate hikes) and the end of 2005 (when the ECB started hiking rates too) – in an environment of rising risk appetite, the US dollar appreciated almost 12% versus the Yen, 7% against sterling, and 4% against the euro and the Australian Dollar, all this despite the US dollar’s status as a ‘safe haven’.

Now it’s quite easy to read too much into last Friday’s strong unemployment number, ie one data point does not a trend make, although one data point is more likely to be the start of a trend than no data point at all. Bernanke’s comments yesterday suggest it’s probably still too early to get excited about rate hikes happening any sooner than the second half of 2010. But the case for a steadily weakening US dollar is now a little less compelling.

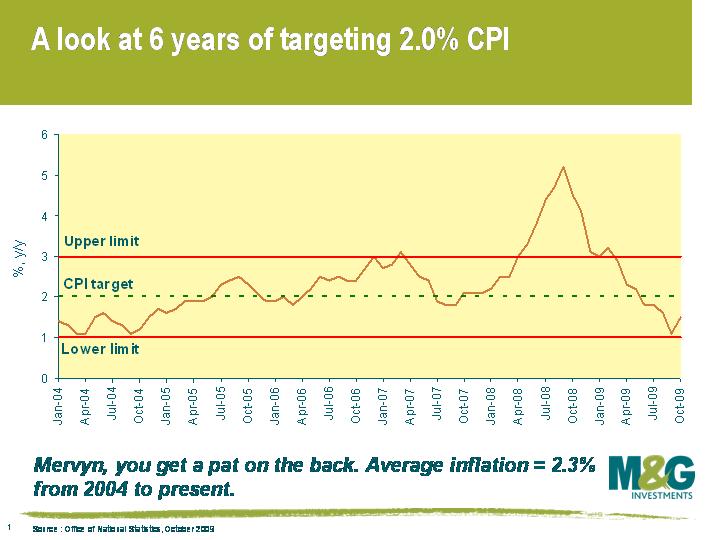

Six years ago this month, Gordon Brown, who was Chancellor of the Exchequer at the time, set the Monetary Policy Committee (MPC) an inflation target of 2.0% for the Consumer Prices Index (CPI). Additionally, if the inflation target is missed by more than 1 percentage point on either side – in other words, if the annual rate of CPI is more than 3.0% or less than 1.0% – the Governor of the Bank, as Chairman of the MPC, has to write an open letter to the Chancellor explaining the reasons why inflation has increased or fallen to such an extent and what the Bank proposes to do to ensure inflation comes back to the target.

With such a clear and transparent policy objective, I thought it might be useful to have a look at how the Bank of England has performed in achieving this target and how well it may do in the future.

The announcement in 2003 that the MPC was to target the CPI was not a radical development, as monetary policy had been targeting various levels and measures of inflation since 1992. This was simply the adoption of a new inflation measure, a new target rate of inflation and is the objective that the MPC still has today. And that’s the yardstick that I am going to use to rate his performance.

Since 2003, the average annual rate of CPI has been 2.3%. Governor King has had to dip his pen into his inkwell on 5 different occasions to explain to the Chancellor why the inflation target was missed. CPI inflation on all of these occasions was more than 1 percentage point above the 2% target. Of the 70 monthly observations of the CPI since January 2004, CPI has been or exceeded 3.0% on 12 occasions and never fallen below 1.0%. If you consider that we’ve had an environment of rising commodity prices, a housing boom and relatively low unemployment (and more recently a sharp reversal of all these things), only missing the inflation target by 0.3 percentage points suggests that the MPC and Mervyn King have done a reasonable job.

Since 2003, the average annual rate of CPI has been 2.3%. Governor King has had to dip his pen into his inkwell on 5 different occasions to explain to the Chancellor why the inflation target was missed. CPI inflation on all of these occasions was more than 1 percentage point above the 2% target. Of the 70 monthly observations of the CPI since January 2004, CPI has been or exceeded 3.0% on 12 occasions and never fallen below 1.0%. If you consider that we’ve had an environment of rising commodity prices, a housing boom and relatively low unemployment (and more recently a sharp reversal of all these things), only missing the inflation target by 0.3 percentage points suggests that the MPC and Mervyn King have done a reasonable job.

The Bank of England targets inflation because inflation distorts resource allocation, reduces economic growth, hurts the poor, creates social and political instability and is painful to reduce once it becomes entrenched in an economy. And the Bank of England’s inflation target is important for bond vigilantes because inflation targeting by an independent central bank creates inflation credibility. Central banks seek to meet their inflation targets by setting an interest rate (the Bank Rate) that is appropriate for meeting these targets. You can argue that inflation targeting has its shortcomings, and when the bank rate falls towards zero then central banks have to look to other measures to reach the inflation target over the medium term (such as Quantitative Easing).

Looking forward, things are likely to get much more difficult in 2010 and beyond. It appears that Mervyn would do well to have his pen at the ready because he could be writing a few more letters to the Chancellor. By the BoE’s own admission, inflation is likely to rise above 3.0% in the coming months, reflecting year-on-year effects (so called ‘base effects’), driven by higher petrol price inflation and the reversal of last year’s reduction in VAT.

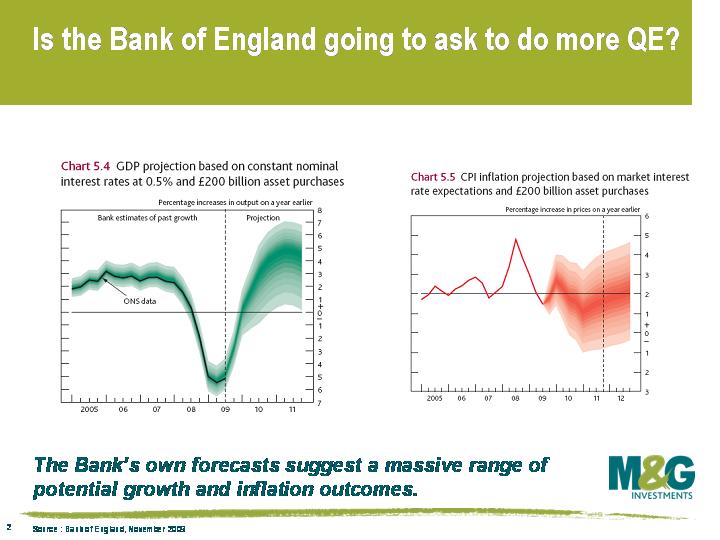

Does this mean no more QE then? There are reasonable grounds to extend QE further, since the UK economy is still (officially) in recession, money supply growth is feeble, and unemployment has showed no signs to date of improving. But will the Governor be writing to the Chancellor to explain why inflation has risen over 3.0% at the same time he is asking for another increase in quantitative easing beyond the £200 billion that the Bank has already done?

Politically, it appears only possible to extend QE while inflation is breaching the 3% upper limit if the BoE has great confidence that inflation will later fall back to target. The Bank of England currently believes this spike should prove temporary, but as can be seen from the fan charts depicting the BoE’s inflation and growth projections in last month’s Quarterly Inflation Report, it doesn’t have great confidence in either its growth or its inflation projections, so I think we’ll most likely have a pause in QE in February.

Politically, it appears only possible to extend QE while inflation is breaching the 3% upper limit if the BoE has great confidence that inflation will later fall back to target. The Bank of England currently believes this spike should prove temporary, but as can be seen from the fan charts depicting the BoE’s inflation and growth projections in last month’s Quarterly Inflation Report, it doesn’t have great confidence in either its growth or its inflation projections, so I think we’ll most likely have a pause in QE in February.

Something else that will very likely be on Mervyns’ mind is that he is becoming less and less in control of his own performance. Central bankers only control monetary policy, and now the bank rate is at 0.5%,monetary policy is losing its effectiveness. Even more of a problem is that central bankers don’t have control of fiscal policy. Large budget deficits for a prolonged period of time will inevitably prove to be inflationary eventually, and everybody wants to avoid a situation whereby monetary policy is being tightened in an effort to counter loose fiscal policy, because that’s a sure way of creating a sovereign debt crisis.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.