Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

According to many market commentators, the UK debt market is looking sick and is at a critical juncture. It is amongst the most unloved government markets in the developed world, which is understandable given the British inability to save in the boom times. Now there is justifiable scepticism that markets will not be able to absorb the forthcoming huge government debt issuance once the Bank of England stops providing life support to the gilt market when it ends the quantitative easing program.

This consensus view is typified in PIMCO’s monthly investment outlook in which the UK bond market is singled out as a market that must be avoided. In their opinion, the gilt market is resting on a bed of nitroglycerin. PIMCO point to the UK’s relatively high level of government debt, potential for sterling to fall and domestic accounting standards that have driven real yields on long dated inflation linked bonds to exceptionally low levels.

We agree these are issues that face the UK economy and have commented on these points previously. However, like any consensus, it makes sense to investigate if this is correct, priced in, and when it might come to an end.

Firstly, the IMF forecasts that for 2009 that the UK government will have a relatively large annual deficit of -11.5% of GDP, which is below that of the USA (-12.5%) but almost triple Germany’s government deficit (-4.2%). However the UK’s total outstanding gross debt stands at 68.7% of GDP, which compares favourably with the USA (84.8%) and Germany (78.7%). The UK government has responded in aggressive Keynesian fashion to the downturn, if this medicine works then the action will be short term in its nature and will not leave the UK with a permanent debt burden, or the increase in debt could alternately be curtailed by the arrival of a more fiscally stringent government in this year’s election. The UK has very little foreign debt and has been prudent by having the longest maturity debt profile in the G7. Outstanding debt and re-financing needs would therefore appear relatively manageable on an international basis. Not all outcomes will be bad.

Secondly, with regard to fears that our exchange rate could fall, the exchange rate has already collapsed by 22% on a trade weighted basis since 31 July 07. So a lot of the necessary adjustment has already taken place. This adjustment process is very beneficial for an open economy such as the UK, especially when many of our trading partners are locked into using the relatively strong Euro currency. By having a flexible currency and control over domestic interest rates, the UK is arguably in as good a position as anyone to grow our way out of our debt problem.

Finally, accounting standards have indeed distorted gilt yields as we have previously mentioned here. However, this accounting standard is designed to improve company accounts in terms of disclosing assets and liabilities of company pension schemes and this is surely a good accounting standard that should be adopted by many other regulators. The fact that better pension regulation in the UK results in lower long term rates makes long dated bonds – especially UK linkers – look dear internationally. But this dampening influence on gilt yields is a distortion that is likely to persist unless the regulation and the accounting oversight of this significant employee benefit are changed.

The view that the UK gilt market is one to avoid has some punch in the short term, but the consensus is exaggerating the risks the UK gilt market faces. Even if one agrees with the consensus, it is important to see if this view is priced into markets and when this will eventually come to an end. I agree with the direction of the consensus, absorbing that much new supply will be negative for gilts in the short term. However in the longer term the UK has the chance to adjust to the crisis through fiscal stimulus, financial reform and a falling exchange rate that might well provide the medicine required. The consensus that a bed of nitroglycerin is a dangerous place to rest like any consensus view should be challenged. Don’t forget, a bed of nitroglycerin could be exactly what the sick UK economy needs as it is one of the oldest and most useful drugs for restoring patients with heart disease back to good health!

Guest contributor – Jeff Spencer (Financial Institutions Credit Analyst, M&G Credit Analysis team)

In an attempt to reduce risk-taking at financial institutions, yesterday President Obama announced a proposal to bar banks from engaging in proprietary trading activity that was unrelated to customer business. He also advocated that banks be stopped from owning or investing in hedge funds or private equity funds. This address was met with concern from investors, with highly-rated government bonds benefiting from their safe haven status and global equities and commodities falling over the course of the trading day. Investors are wary about the potential implementation and impacts on the banks profitability of the so-called “Volcker Rule” – named after the former Federal Reserve chairman who has advocated the move for months.

For me, it is important to delve deeper into President Obama’s announcement. In the accompanying White House fact sheet, President Obama, echoing a small portion of the Group of Thirty document released on January 15, referred to “hedge funds, private equity funds and proprietary trading operations for [banks’] own profit”, not “investment banks” or “investment banking” – an important distinction to bear in mind.

The equity market’s panic reaction to the speech indicates that financial institution shareholders understand that trading activity has at least partially underwritten huge losses in consumer loan books in 2009, and may ultimately be more indicative of a fear that the days of banks’ trading on the back of easy Fed money are numbered (shares of banks without sizeable trading operations were generally flat or up). Fed rules already prevent depository institutions from providing liquidity to non-bank entities within a group, but on September 23, 2008, the Fed allowed exemptions for banks to fund activities that are typically funded in the repo market. This exemption was extended on January 30, 2009 but expired on October 30, 2009. New limitations on the scope of trading by regulated banks appear intended to complement these regulations.

Credit investors may or may not have new worries as a result of whatever new rules ultimately come out of Congress, but it is fairly clear that there will be some confluence of 1) higher capital charges for trading/markets activities (neutral to positive for bank unsecured bondholders) and 2) more emphasis, for regulated entities, on lower-margin trading activities, as banks appear likely to be forced to demonstrate to regulators that any trading they are doing supports customers and is not “proprietary”. We do not think at this point that this means that investment banking divisions of large US banks (or, for that matter, non-US banks that own significant US broker-dealers) will be forced to be spun off. It could, on the other hand, mean that non-bank financial institutions may have to close or sell their insured depository institutions. Whatever emerges in the financial sector reform legislation, it may not be the blunt instrument that the market evidently fears.

The limit on bank size is potentially the more problematic new rule to enforce, but only because it is so unclear how it will be determined that a bank is too big to fail, and what the consequences of this will be once it has been made. Again, the President’s remarks need to be understood correctly: he said that he wanted to “prevent the further consolidation of our financial system”, not that he wanted to break up existing banks. As with trading activities, existing rules already address this topic with a ceiling on nationwide deposits at one institution; the question is what additional measures any new limit will actually target.

These two prospective additions to the House bill (HR 4173, which has passed) and to whatever Senate bill emerges from the Banking Committee have not yet been outlined in anything like detail, so anyone who claims to know what their precise implications will be, probably doesn’t.

Today we have seen the preliminary release of M4 money supply (so-called ‘ broad money’), and it could potentially be a very important piece of economic data. December saw a 1.1% drop in the money supply, the largest monthly fall since records began in 1982. Expectations were for a 1% increase. Year-on-year, expectations were for an 8.9% increase, but this came in at a meagre 6.4%. M4 money supply includes cash in circulation, retail deposits and wholesale deposits at banks and building societies and certificates of deposit.

M4 became a key piece of economic data post the economic crash, since it’s a primary concern of monetary policy decision makers if the supply of money ceases and contracts. Trust and credit disintegrate, and monetary policy becomes utterly ineffective. Ultimately, this can lead to drastic deflation post a financial crash, which in a heavily indebted economy, can spell disaster (see here for a blog from early 2008 on the importance of money supply). One of the key motivations behind the Bank of England’s decision to implement exceptional monetary policy measures, and in particular Quantitative Easing, was to prevent such a collapse in the supply of money, and so to prevent serious disinflation or deflation. As Mervyn King said in his speech earlier this week, “the unprecedented actions of the Monetary Policy Committee to inject £200bn directly into the economy…have averted a potentially disastrous monetary squeeze”.

Mike wrote earlier this week about the rising inflation numbers in the UK. And whilst we feel that most of the cause of this spike was due to base effects, policymakers are likely to find it incredibly difficult to justify a further round of printing money through QE (as Anthony mentioned last month here). Following the higher than expected inflation numbers, there is now a very strong consensus that there will be no QE extension next month, although there is a considerably weaker consensus around whether we could see more QE in the future.

The final M4 figure will be released on 1st February, when we’ll get an idea of the breakdown and therefore why the M4 figure was so weak. In addition, it’s worth highlighting that the Bank of England prefers to strip out the deposits of ‘intermediate other financial corporations’, which excludes things like counterparties and SPVs. Nevertheless, today’s release is still alarming, because it suggests that QE’s efficacy as a tool to increase the supply of money is perhaps not what we thought it was.

It is also potentially alarming that there is less money supply chasing the same number of goods and services, and yet inflation is still quickly rising. It’s not our core view, but there’s a risk that inflation could be more persistent than first thought, ie imagine what will happen to inflation if or when the money supply starts rising quickly again. This number will also be a concern to policy makers because it suggests an emergence of a monetary policy dilemma : the higher inflation number suggested that QE had served an important part of its purpose, the avoidance of deflation. But concomitantly, now, it appears that it has had less impact than expected on the supply of broad money – the money supply data would argue for an increase in monetary policy stimulus.

So which one of the two measures will policymakers give primacy to in February? Our belief is that the members of the MPC will still struggle to justify an increase in QE with inflation where it is now, but this M4 figure has just presented them with a much harder decision. Mervyn King also spoke of this lack of clarity in his speech;

The headline in the Racing Post of 29 December said it all: “Quantitativeasing Maintains Perfect Record”. Its Newbury correspondent reported that “Quantitativeasing started as a red-hot favourite and had little trouble maintaining his unbeaten record. Ridden with plenty of confidence his task was made easier when Tail of the Bank came to grief at the second last. His trainer said ‘I was delighted with the way he went through that testing ground’”. Rather like the MPC, the owners of Quantitativeasing, winner of all three of his races in 2009, have yet to decide how many outings he will have in 2010. They are waiting for race conditions to become clearer.

We do appear to be living in a two-tier world. One part of this world (banks and investors) is awash with cash as a result of £200 billion of QE, and some of this cash for gilts is being invested in other, higher risk assets, which is bringing significant asset price appreciation and, perhaps, inflation. The other part of this world, the real economy, is in a very different position, and today’s money supply data suggests that the cash that has been given to banks and investors is not permeating down into new loans and new credit to the real economy. Worryingly, at some point these two worlds will have to come back into line.

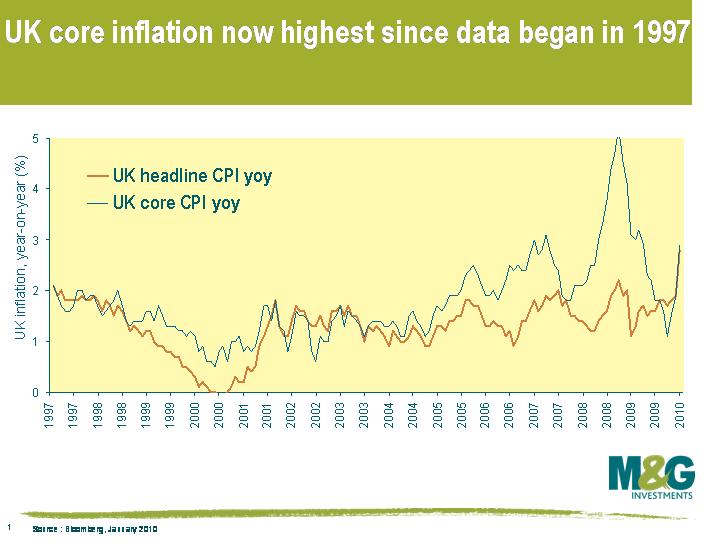

Expectations had been for a big jump going into this morning’s release of December UK inflation statistics, however expectations still weren’t high enough. The year-on-year CPI inflation rate surged from +1.9% to +2.9%, eclipsing the average forecast of 2.6% (economic forecasts varied from as low as +1.9% to +2.8%). This marked the biggest jump in UK CPI since April 1991.

Why the big jump? Well we already knew that inflation would rise sharply, which was simply due to base effects (as we mentioned here). The inflation rate in December 2008 has just dropped out of the year on year number, and this deflationary month was important since it was when VAT was cut from 17.5 to 15%, and was also a month of heavy discounting by retailers. In addition, the high year on year numbers are reflecting the fact that energy prices were at their most depressed at the beginning of 2009 (oil prices alone added almost 0.3% to today’s CPI number), although this inflationary impact will gradually unwind over the coming months.

The bad news is that the VAT increase isn’t yet in the data. This month’s increase in VAT from 15% back to 17.5% doesn’t appear in the data until the inflation rate for this month is released in one month’s time, so it now looks very likely that Mervyn will soon have to start writing letters to Alastair Darling explaining why UK CPI has exceeded the upper limit of 3%.

Further bad news came in the form of core CPI, which rose from 1.9% to 2.8%,the highest rate since data began in 1997. Core inflation is a less volatile measure since it excludes energy, food, alcohol and tobacco, although it is clearly still affected by base effects, the weakness of sterling and changes in VAT (see a critique that Richard wrote of core vs headline back in 2007 here).

Does this therefore mean that the inflation genie is out of the bottle? Very unlikely. Spare capacity in the UK economy is still huge, bank lending is weak, and money supply growth remains feeble, in spite of the Bank of England’s best efforts at creating money (note that this doesn’t mean that QE hasn’t worked – we have no idea what the growth or inflation rate would be right now if we’d never had QE). It’s difficult to see how inflation can be generated, unless energy and food prices skyrocket over the remainder of this year or sterling collapses (sterling has actually strengthened today on the inflation news today rather than weakened). We expect inflation to fall back again from the middle of this year once the base effects fall out of year on year numbers. The MPC will also be looking through today’s data release, and I can’t see this upside inflation surprise kickstarting any rate hikes – remember that the bank rate is set with a 2-3 year view of where inflation is likely to be, not a 2-3 month view.

Finally, it’s worth highlighting something I mentioned a few months back regarding inflation-linked gilts (see here). Inflation-linked gilts are becoming a popular investment for people who are seeking to protect their portfolios against the risk of rising inflation, but some investors fail to realise that the return profile on these bonds isn’t just driven by what happens to the inflation rate, but also what happens to the ‘real yield’. The real yield is driven by things like pension fund demand and supply, and is also driven by what happens to conventional gilt yields.

The further out along the yield curve you go, the more duration you have. So the further out along the yield curve you go, the more the return profile on index-linked gilts is driven by what the real yield is doing, and the less the return profile is driven by where inflation goes over this year and next. Today, conventional gilts have predictably sold off on the inflation print – at the time of writing, 10 year gilt yields are 8 basis points higher (equivalent to about a 0.6% price fall), while 30 year gilt yields are 4 basis points higher (which is also equivalent to about a 0.6% price fall, owing to longer dated gilt prices being more sensitive to changes in yields, ie longer duration). As you’d expect, inflation-linked gilts have outperformed conventional gilts today as inflation expectations have risen slightly, but the UKTI 2.5% 2020 and UKTI 1.125% 2037 have still both fallen in price by around 0.3%.

There has been a lot of anguish and complaints from bankers about Obama’s tax on banks, and complaining why they have been singled out. Some of this is the usual self interested financial posturing (they are bankers!), some of it is in response to unfair political criticism, typified by last week’s focused grilling of Lloyd Blankfein, a successful CEO of a successful bank (Goldman Sachs). Ignoring the emotional sides of the argument what about the tax itself?

In principle it looks like a fair idea. If the government acts as a lender of last resort, financed by the tax payer, then the beneficiary of that guarantee, the banks’ shareholders, employees, and customers should share the fee. The difficulty of course is implementing the tax in a global financial system, and determining the appropriate fee. Fortunately for Obama, the threat of relocating your banking operations outside the biggest capital market in the world is not credible so implementation should be successful. Setting the level is a different matter, too low and the state effectively subsidises risk taking, too high and the state stops appropriate risk taking. However, this should not stop attempts to set an appropriate rate, as having no insurance indemnity will eventually distort markets.

A tax policy on its own is not the only answer to pricing risk correctly, you have that other government tool to help or interfere in the economy (depending on your political view): regulation. After all if you’re an insurance company providing insurance you tend to set out the terms and conditions to your customer to stop reckless behaviour. That’s one of the things that financial regulation sets out to achieve, and indeed if done successfully mitigates the need for setting an insurance premium. However insurers and regulators have to work closely in tandem, otherwise the risk takers will find ways round the regulations.

Given the chaos that has occurred following the run on Northern Rock, the bail out of major banks around the world, and the Icelandic bank failures, you would have expected the regulator, the lender of last resort, and the tax payer to have learnt a thing or two, and to stop the danger of free riding of bank shareholders, bank employees, and bank customers. However on reading the papers this weekend I came across an article about a one year sterling high yielding deposit account paying 4%. The catches to this offer referred to in the article included a lack of an https address and padlock symbol on the bank site, and an unproven customer service. On the other hand the article referred to the fact that account holders would be fully covered for £50,000 under the UK’s Financial Services Compensation Scheme. Pre October 2007, the compensation scheme used to extend to 100% of the first £2,000, and a further 90% would be guaranteed from £2,000 to £35,000 (so customers would take some degree of risk if a bank failed). On checking the website of the bank this morning to investigate further I was greeted with the comment that the website was being upgraded due to the unprecedented demand for its online deposit product. A rate of 4%, 8 times the official Bank Rate, where can you invest to get a relatively low risk free return on that type of cost of funding? Even Lloyd Blankfein and his team would have difficulties.

Isn’t there a danger that we have made no progress from where we were 2 years ago with Icesave, and the Icelandic banks paying up for deposits, lending them on to high yielding risky ventures? Don’t worry customer, the taxpayer will bail you out! Whether you’re right wing and dislike state subsidies, or left wing and hate distribution of tax revenues from the poor to the rich this does not look politically right. Things need to change, on the insurance front progress has been made, on the regulation front work still needs to be done, and sadly in the UK the incentive to take risk, with your deposits and tax payer money, has been increased.

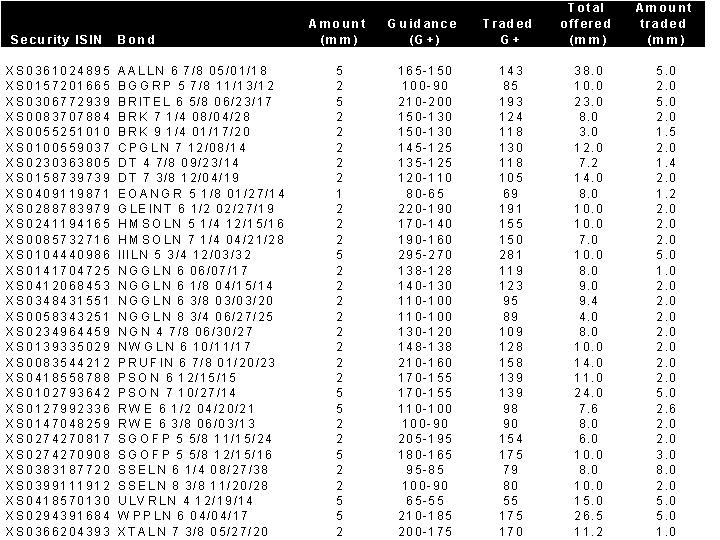

Last week’s BWIC list (bids wanted in competition) from the Bank of England gave further evidence, if it was needed, that the demand for Sterling corporate bonds remains very strong. The table below, kindly provided by HSBC, shows the bonds that were sold and that most traded through where the market was pricing them last Friday.

The BOE took the opportunity to sell a selection of the corporates it purchased in its QE program of last year. Despite receiving bids for every bond on the list The Bank decided to sell a mere £83.7m worth, or one quarter of the £324m bonds that were on offer. Running a ruler over the levels achieved in the auction The Bank achieved new highs for many of the bonds that were sold.

A year ago Richard wished the BOE every success as corporate bond fund managers, so far so good. Analysts over at Evolution Securities have since calculated that the BOE has so far earned around £60 million on the £1.55 bn portfolio of bonds they currently own. Not a bad return considering the Bank’s ability to print money and therefore to finance at no cost. Coupled with evidence from previous banking crises such as the Swedish one back in 1992, The Old Lady of Threadneedle may well see a tidy profit from its actions.

List of Bonds

Happy New Year.

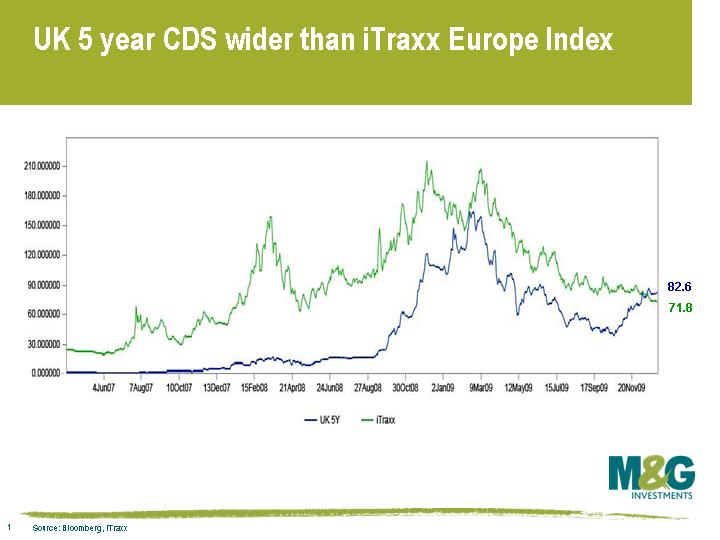

Over the past couple of weeks, the cost of buying protection to insure against a default by the UK government has risen to exceed the cost of insuring a basket of European investment grade companies. The chart below shows that 5 year Credit Default Swaps (CDS) for the UK sovereign are currently at 83bps per year, compared with 72 bps for the investment grade companies, which are all lower rated than Her Majesty’s government and unlike the UK, the last time I looked weren’t allowed to print bank notes to repay their debt. So it doesn’t look right. But noises about a downgrade of the UK continue, and the plans from both the government and the opposition to reduce the debt remain unconvincing.

Elsewhere we’ve had sovereign debt scares in Dubai and in Greece, and yesterday in Iceland the President exceptionally overruled the legislature and stopped a payment to the UK and the Netherlands of £3.4 billion to cover money lost by savers in the Icelandic banks. Fitch downgraded Iceland to BB+ yesterday, although the bigger agencies still have the country in investment grade, but only just. Iceland CDS now trades at 470 bps. The decision by the Icelandic people isn’t surprising, as the payment amounts to around £10,000 per person – a massive burden. I can’t imagine that UK voters would agree to make such a payment to a foreign government should the table be turned, and the Icelandic economy is in a worse state than ours. This article in today’s Irish Independent by David McWilliams is therefore a little worrying, as it probably does reflect the popular view that default is a better option that a strong credit rating or than having to wear a hair-shirt for a decade. Ireland has entered into significant austerity measures (including large pay cuts for civil servants) in order to restore the nation’s finances. McWilliams concludes “Iceland proves there is an alternative – are any (Irish) politicians, from the President down, prepared to listen?”. 2010 could be a year of angry populations and wobbly governments.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.