Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

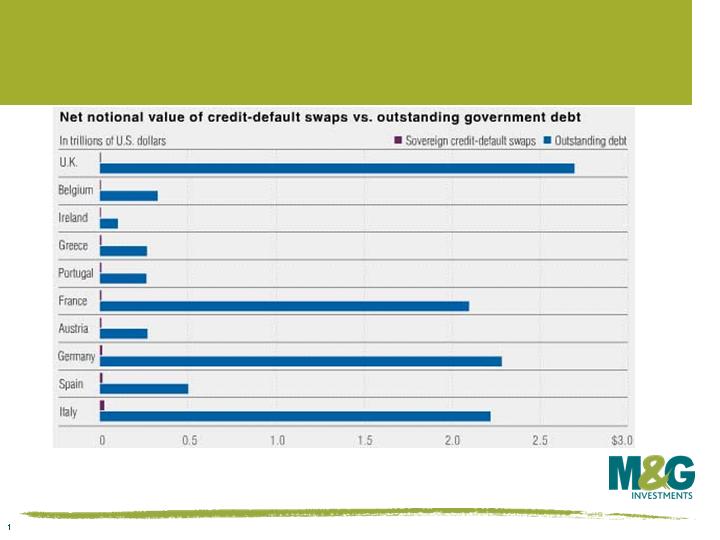

Following on from Jim’s Sovereign CDS Q&A blog (see here) I came across this chart at zerohedge.com. Whilst I can’t vouch for its accuracy, the chart shows that the actual net amount of outstanding sovereign CDS contracts, relative to outstanding government debts, are actually very small. That would seem to add weight to Jim’s argument that the pressures faced by governments are borne ‘of fiscal imprudence and a lack of will to resolve this,’ rather than the sole work of evil speculators.

Following on from Jim’s Sovereign CDS Q&A blog (see here) I came across this chart at zerohedge.com. Whilst I can’t vouch for its accuracy, the chart shows that the actual net amount of outstanding sovereign CDS contracts, relative to outstanding government debts, are actually very small. That would seem to add weight to Jim’s argument that the pressures faced by governments are borne ‘of fiscal imprudence and a lack of will to resolve this,’ rather than the sole work of evil speculators.

The risk free rate is a concept beloved of micro-economists and bond math geeks. It’s the building block of Modern Portfolio Theory and an input into option pricing models. It’s supposed to represent the interest rate available in the market that is without credit risk and as such is the lowest interest rate in the market. The complete absence of risk has always been more observable in theory than in practice but in the last month or so, swap rates have fallen below gilt yields – can it be right that the lowest interest rate in the market is lower than the traditional risk free rate? Are government bonds still the right instrument with which to observe the risk free rate?

Interest rate swaps are a means of turning a floating rate cashflow into a fixed rate cashflow for a set period of time, or vice versa. If you decided to receive fixed rate payments for ten years, you would agree to pay Libor (reflecting the cost of short term money) and receive the fixed payment for the life of the contract from the bank with which you’d traded. Historically the fixed rate payment would be more than you could get by buying a gilt from Her Majesty’s government. On average over the past decade it was around 0.5% more than the ten year gilt yield. This seems to make sense, as there is a risk that the bank counterparty that you have traded with disappears and can no longer service the contract, so the premium over gilts reflected credit risk.

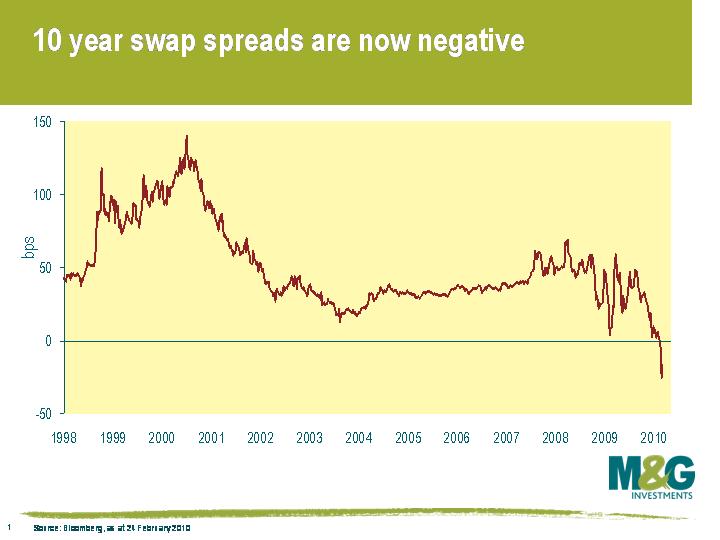

As this chart shows however, this swap spread (the difference between the swap rate and the gilt yield) has fallen substantially since the start of 2009, and in the first couple of months of this year it has turned negative. The ten year swap spread is now -0.18%. In other words you get a lower rate of interest in receiving a fixed payment from a bank than you would from a AAA rated (still!) government bond. Does this make sense? After all, if you are a UK investor that swap might well be with a government owned bank anyway, so isn’t the credit risk the same? There are two reasons why you might want to receive fixed via an interest rate swap rather than buying a gilt. Firstly, if there was a UK sovereign default you would probably lose capital if you owned a physical gilt, whereas your downside in a swap default would be limited to having to replace the counterparty at a potentially less advantageous rate of interest. More significantly though, the markets are reflecting not just the increased risk of a UK default (which in our view is much less likely than is priced into the CDS market, at about 9% over the next 5 years) but more importantly the relative supply of swaps and government bonds. Gilt issuance will be running at around a £200 billion rate for the next couple of years, but without the market’s biggest investor – the Bank of England has ended its Quantitative Easing programme (although not irrevocably).

As this chart shows however, this swap spread (the difference between the swap rate and the gilt yield) has fallen substantially since the start of 2009, and in the first couple of months of this year it has turned negative. The ten year swap spread is now -0.18%. In other words you get a lower rate of interest in receiving a fixed payment from a bank than you would from a AAA rated (still!) government bond. Does this make sense? After all, if you are a UK investor that swap might well be with a government owned bank anyway, so isn’t the credit risk the same? There are two reasons why you might want to receive fixed via an interest rate swap rather than buying a gilt. Firstly, if there was a UK sovereign default you would probably lose capital if you owned a physical gilt, whereas your downside in a swap default would be limited to having to replace the counterparty at a potentially less advantageous rate of interest. More significantly though, the markets are reflecting not just the increased risk of a UK default (which in our view is much less likely than is priced into the CDS market, at about 9% over the next 5 years) but more importantly the relative supply of swaps and government bonds. Gilt issuance will be running at around a £200 billion rate for the next couple of years, but without the market’s biggest investor – the Bank of England has ended its Quantitative Easing programme (although not irrevocably).

So with an implied default rate of nearly 10%, the gilt market cannot seriously be regarded as “risk free” any more, even if we do think that probability is nutty given the UK’s access to the printing presses of mass destruction if we ever did get stuck for a few bob to repay our bond debts. But once the gilt supply glut is out of the way in a couple of years time (we hope), expect swap spreads to move steadily higher. The swap market has become an increasingly important yardstick for valuations however, and maybe the UK corporate bond market will begin to price in relation to swaps rather than gilts – the European corporate bond market has already been doing this for years, as has the UK population whenever we’ve considered a fixed rate mortgage.

The market in sovereign credit default swaps has sprung to life over the past year as worries about the health of nations, rather than corporates, have multiplied. Problems in Dubai in December, and Greece right now, on top of a general deterioration of the developed economies’ budgetary positions have seen sovereign CDS making headlines. Here’s a chart of some of the latest CDS spreads on the major economies showing that fear of sovereign defaults is growing. This article is in the form of a Q&A and aims to answer some of the main questions that our clients are asking us about the sovereign CDS market.

Q: What are Sovereign CDS?

A: Credit Default Swaps (CDS) are contracts made by two market participants to either increase or reduce credit exposure to an entity – in this case a sovereign nation rather than a company. Quoted in basis points per year, a CDS price indicates the cost per year to either buy or sell exposure to the possibility of a sovereign defaulting or restructuring. Selling protection means you receive the premium every year of the contract but bear the risk of capital losses in the event of default; buying protection means that you pay the premium but will receive a payment equivalent to the losses suffered by bond holders in the event of default or restructuring. In other words sovereign CDS behave a little like insurance contracts – you can take the role of the insurer, or be insured.

Q: Why would you use Sovereign CDS?

A: You can use CDS to hedge an existing government bond position against losses it might suffer as sovereign credit worthiness deteriorates, or to take exposure to sovereign risk and receive yield in exchange for that credit risk. Like all derivatives they can be used to hedge trading positions and efficiently manage portfolios, or to take speculative or naked positions on the underlying markets. Because the instruments are mark to market, profits and losses from movements in the CDS levels occur constantly – you do not need to see an event of default to either make or lose money, just a movement in the market’s perception of the risk of that default. These are OTC (over the counter) derivatives, so participants need to have legal documentation in place with counterparties, and collateral moves from one counterparty to the other to reflect movements in the profit and loss – this reduces counterparty risk.

Q: What triggers a payment?

A: The Sovereign CDS contract is triggered when a credit event occurs. There are three credit events for sovereign CDS, and they differ from corporate CDS in that “bankruptcy” is not one of them (that’s a concept that only legally applies to a corporation). The credit events are:

1) Failure to pay a coupon or principal on a bond or loan.

2) Moratorium – the announcement of the intention to suspend payments of debt obligations.

3) Restructuring – changing the terms of a debt obligation in a way that disadvantages investors, for example by extending the maturity date, cutting the coupon, or changing the currency of denomination to that of a non-G7 or AAA rated OECD member.

Sometimes credit events are not clear-cut. For example, what about the UK’s War Loan example that we talked about recently? Bond investors voted overwhelmingly to accept the reduced coupon payments (from 5% to 3.5%) – but was there really an alternative? So although this was a voluntary restructuring, nowadays this would probably trigger a CDS credit event. A committee of market participants sometimes has to decide whether such an event has taken place or not – obviously this is not as “clean” as you might like, and there is obviously potential for conflicts of interest to occur.

Q: What happens after a credit event has taken place?

A: The investor who has bought protection through a CDS contract needs to receive a payment equivalent to the face value of the contract that they have entered into, less any recovery on the bond. So, let’s assume that Country X misses a bond coupon, and its bonds fall to 20 cents in the dollar. There are two ways of settling the contract – physically or simply as an exchange of cash. In physical settlement, I give the counterparty who sold me protection $100 nominal value of bonds for every $100 which I have insured. The counterparty gives me $100 in exchange. Thus if I own the bonds and have hedged them with CDS then although my bonds have fallen by 80%, I get my full face value back. If I have simply been speculating, then I can buy the distressed bonds in the market for 20, and sell them for 100 to my counterparty. Contracts will typically cash settle however – in this case there is an auction to set an observed market price for the distressed bonds and thus determine their recovery value. Instead of bonds changing hands, the counterpart simply transfers the difference in value between the nominal value of the bonds and their distressed price to the buyer of protection. This is neater, but there are again some issues about the fairness of the price determined at auction if participants were conflicted – in a large, liquid government bond market this is less likely to be a problem than in an auction for illiquid high yield issues.

Q: Are all bonds deliverable into the CDS contract?

A: No. The contract determines which bonds are deliverable – only bonds in major currencies are allowed, and bonds must be under 30 years to maturity. The concept of the cheapest-to-deliver (CTD) bond is important. The buyer of protection will want to deliver the lowest cash priced bond to the seller of protection, in order to maximise their payment. All other things being equal, this would be a long dated, low coupon bond – although in a full blown default where no coupons are being paid all bonds will tend to trade at similar cash prices in any case. Other issues to consider include whether agency bonds are deliverable into the CDS contract – some believe that KfW bonds are deliverable into a German sovereign CDS contract, while Railtrack bonds are not deliverable into a UK contract, even though both are AAA rated and government guaranteed. Lawyers love credit default swaps.

Q: What are sovereign recovery rates likely to be?

A: There has only been one example of the auction process being used to determine the recovery rate for sovereign CDS. After the last Ecuadorian default, the auction settled at a recovery rate of 31.4%. In recent sovereign defaults in the days before CDS, the observed recovery rates ranged from 6% (Russia in 1998) to 90% (Dominican Republic in 1990). The average according to Credit Suisse was 39%. Long term recovery rates may of course differ from those used in the auction process. Recoveries will tend to be based on willingness to settle, rather than asset coverage. In a corporate default, debt investors can seize physical assets or contracts from a company; with the exception of overseas embassies and property it is much more difficult to seize sovereign assets.

Q: Can I estimate probabilities of sovereign default from CDS prices?

A: Yes, with the caveat that like all financial instruments, prices are driven by fear and greed and may not reflect the fundamentals. You need to have an assumption for a recovery rate – let’s use 39% as the average. So if Greek 5 year CDS is trading at 400 bps per year, this means that in any one year you anticipate a pre-default spread of (4% x 100/(100-39)) = 6.56%, which given markets are efficient (!) must equate with the expected one year default rate. So on the back of an envelope, ignoring the impact of compounding and the expected timing of a default, the cumulative expected default rate for Greece over the next 5 years is 5 x 6.56%, or over 30%.

On today’s CDS levels, the following default probabilities can be calculated:

| 5 year CDS, bps | 5 year implied cumulative default at 39% recovery | |

| Germany | 45 | 3.7% |

| USA | 47 | 3.8% |

| France | 63 | 5.1% |

| UK | 91 | 7.5% |

| Italy | 135 | 11.1% |

| Portugal | 186 | 15.2% |

| Greece | 400 | 32.8% |

Q: If I buy protection on my gilts from a UK bank, what happens if the UK defaults?

A: It wouldn’t be a good idea, and luckily it’s not allowed. UK banks don’t trade UK sovereign CDS (and US banks similarly don’t trade US CDS). If you trade UK sovereign CDS the most liquid contract is in US dollars; you can’t trade the contract in £ – this is because in the event of a sovereign default there is also likely to be a currency crisis which would significantly distort the recovery value in non-£ currencies. Because the UK only has £ obligations (there is no foreign currency debt) the recovery value will therefore be determined by auction and there will be cash settlement. This distortion of the knock-on currency devaluation is the big difference between sovereign CDS and corporate CDS (there is no currency impact in a typical corporate bond default), and a reason why the two instruments cannot be directly compared (ie. you can’t automatically conclude necessarily that because an index of corporate CDS is trading at a lower spread than the UK sovereign then the corporate credit risk is lower).

Q: What is the “basis”?

A: The basis is the difference between the spread over the risk free rate on a bond issued by a government and corporate and the CDS spread. As a simple example, Greek 5 year bonds yield 440 bps over similar maturity German government bonds (risk free, hopefully), and the CDS is at 400 bps. This difference of 40 bps is the basis – it’s common for the CDS level to be below the bond spread (a negative basis). The difference should be arbitragable, but issues such as liquidity, different investor preferences and uncertainty over the cheapest to deliver mean that the differences can persist. It is worth mentioning that given most assets contain an element of sovereign risk, the desire to hedge this out, especially amongst banks, has had a huge technical impact on what is still a fairly illiquid market thus distorting prices. It is not unknown in the credit markets for CDS spreads and corporate bond spreads to move in opposite directions – this can be a real pain trade for those who thought they had hedged an exposure.

Q: Are sovereign CDS evil?

A: Some people think so, and there have been rumours in the past few days that the European Commission is considering a ban of some sort as speculators have been blamed for the current Greek woes. Certainly CDS provide a method of reflecting bearish views on a nation in a way that was difficult to do historically (most investors cannot physically short government bonds), and it’s a method that produces a highly visible bellwether of a country’s perceived risk. But Greece, and the other weak sovereigns, would be in trouble even if the CDS market did not exist – the problem is one of fiscal imprudence and lack of will to resolve this, and the market reflects the fundamentals rather than drives them. There is a wider, and perhaps more valid issue with CDS though, and that’s the issue of moral hazard. I can’t buy insurance on somebody else’s house that pays out if it burns down – if I did it might produce perverse incentives for me, and even if I didn’t turn into an arsonist, it might make me think twice about calling 999 if I saw smoke. Does buying protection on a company or a nation create perverse incentives to hinder a possible recovery for that entity? Is it morally right to hope for bankruptcy, or default, when it might mean hardship for employees, or indeed a whole nation?

Back in January at our Annual Investment Forum I focussed on the changing face of the European Leveraged Finance markets – those companies financed with significant levels of debt. My belief is that the current, somewhat forced reinvention, will ultimately result in an increasingly deep and liquid European High Yield market (EHY), more akin to that of the USHY market.

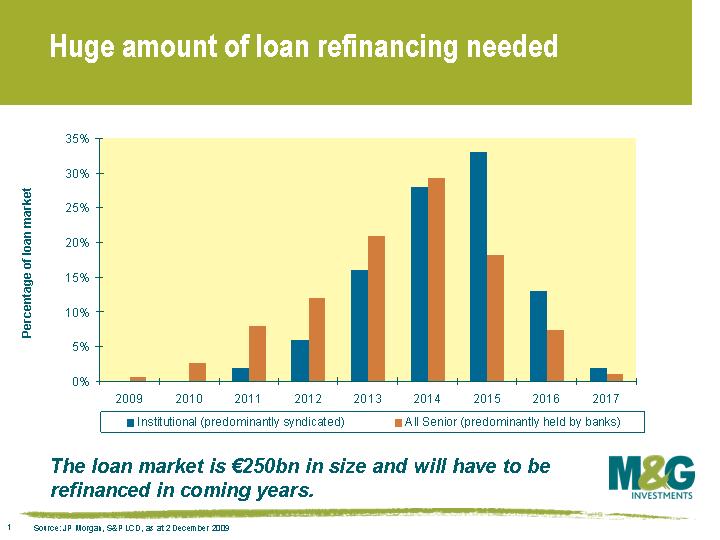

This change, which is already well underway is being predominantly driven by three factors. Firstly, a need within the European leveraged loan market to re-finance a huge wall of debts maturing between 2012 & 2015 (see graph). Secondly, we have witnessed a significant rise in the number of fallen angels issuers; those high yield companies who have lost their investment grade status, the likes of Fiat and ITV. Thirdly the now significant sub financial component of the high yield universe is changing the nature of the market. Subordinate debt issued by the likes of Lloyds, RBS and ING currently comprise around 13% of the EHY universe.

On my first point, the consensus has held that a mixture of trade sales, secondary LBOs, IPOs, restructuring and re-financings will offer a solution to the circa €200 bn worth of European leverage loans coming due. However, the recent decision to abandon attempts to IPO Travelport, and delay those for New Look and Merlin, has brought the spotlight firmly on the IPO market asking questions of its willingness to participate in future.

The European equity market has arguably learnt some harsh lessons over the last few years. The relisting of Debenhams back in 2006 was followed by three profit warnings in quick succession with its stock price predictably suffering. (See Times article here) Gartmore and Smurfitt Kappa’s IPOs are other examples of sponsor owned businesses that come to mind whose stock prices have underperformed the market since relisting. Had much, if not all of the low hanging fruit already been extracted by the sponsor?

In today’s volatile environment the ability of private equity to hit their IRR targets may be hampered by the scepticism pervading the European equity markets. The reality is that there will always be an equity market interest in backing companies with good prospects and strong track records, sensible debt levels and an alignment of sponsor/equity market interests. But the lack of willingness to underwrite the IPO’s of highly levered, cyclical businesses poses further questions for the European leveraged finance market. If the European equity market is unwilling to play its part in re-financing the excesses of previous years, then the implications are likely negative for both private equity returns and certain European leveraged finance investments.

On Tuesday morning, I attended a breakfast with Joseph Stiglitz that was both fascinating and gloomy. Stiglitz, who was formerly the senior adviser to Bill Clinton, Chief Economist at the World Bank, and was awarded the Nobel prize for Economics in 2001, shared his views on the state of the US and global economy and discussed some of the key themes in his new book Freefall. Stiglitz’s views are mentioned in brief below.

Consumption forms the majority of economic growth in the US, and a sustainable recovery needs consumers to spend. However consumers can’t consume if they’re saddled with too much debt. There are three solutions to this:

1) Bankruptcy. Defaulting on outstanding debts would reduce the burden, thus allowing spending to rise. However banks clearly don’t want that, and most certainly can’t afford it.

2) Inflation. This is also not likely, as central banks won’t allow it. Plus, in practice, inflating your way out of debt problems doesn’t really work – countries typically have a lot of short term debt, and as soon as markets get a whiff of an inflationary policy, short term bond yields will rise, thus making the cost of debt more expensive. In fact the worst thing for central banks is if markets believe that there’s a risk of inflation even if the central bank has no desire to inflate its way out of a debt problem, since this results in the cost of debt rising without the accompanying benefit of inflation (no wonder, therefore, that US policy makers continue to stress the downside risk to inflation, whether they actually believe it or not)

3) Muddle through. This is the most likely outcome, is what the authorities seem to be doing now, and the implications are a low growth rate for a prolonged period.

In his view, the US unemployment rate is likely to remain elevated. The budget office doesn’t expect unemployment to return to normal levels until at least the middle of this decade, and that’s based on what some might argue is an overly optimistic real growth rate of 3% per annum. In addition, the official unemployment rate is underestimating the ‘true’ figure – if you add in all the Americans who actually want a job but can’t get one, the number is almost 20%. Furthermore, about 40% of people in the US have been unemployed for more than six months, which is something that Europe’s used to, but hasn’t been experienced in the US in modern times. The effects of the labour market crisis are likely to be exacerbated and long lasting because this financial crisis has come at a time when US labour is at a particularly vulnerable phase. Just as in the Great Depression, when the US economy was transitioning from one based on agriculture to one based on manufacturing, this crisis has hit as the US economy is transforming from one based on manufacturing to one based on the service industry.

Labour market aside, he believes that the US economy is facing two huge underlying macroeconomic problems, the first being a weakness in global aggregate demand brought about by a very high saving rate in the emerging countries, and the second being mounting inequality between the rich and the poor. The apparent solution to the latter problem was to encourage people on low incomes to spend more and save less, resulting in an unsustainable savings rate of zero, and which has clearly now backfired.

Stiglitz also touched on exit strategies. Something that’s very important but hasn’t yet received sufficient attention is the effect of Federal Reserve ending its purchase of mortgages. The Fed’s balance sheet has swelled from $800bn to about $2tn, and it has bought almost all mortgages issued in the US over the past year. The Fed will go from buying almost the whole market to buying none, and surely this will result in mortgage rates rising, which is clearly bad news for the housing market and for the already depressed commercial real estate market. The most likely outcome for the US economy is a ‘double dip’ – not necessarily one that returns the economy to recession outright, but a slowdown in US growth.

There were numerous additional pieces of information that warrant a mention. I wasn’t aware that (according to Stiglitz) Paul Volcker was fired by Ronald Reagan. Despite Volcker’s excellent track record in bringing inflation under control in the 1980s, the bankers wanted someone to repeal Glass-Steagall and ultimately the bankers had their way. Reagan turned to Alan Greenspan as someone who strongly believed in deregulation. Greenspan succeeded in controlling inflation, although in Stiglitz’s view it wasn’t particularly due to Greenspan’s policies – the main credit goes to China. Greenspan has been blamed for a lot of what has happened over the past couple of years, but it’s not solely Greenspan’s fault – if it hadn’t been Alan Greenspan, it would have been anyone else who believed in deregulation to meet the political will at the time when Greenspan was appointed.

Stiglitz also discussed a favourite topic of his, on how a lack of regulation led to inappropriate incentive structures in banks, which led to bad behaviour. The banks’ job is to efficiently allocate capital, manage risk, and reduce transaction costs, thus resulting in higher productivity. But 40% of corporate profits went to banks at a time when real wage growth was flat for a whole decade – banks stopped being the ‘means’, and became the ‘end’. Banks were allowed to become not only too big to fail, but too correlated to fail. Saving the banks has been a social cost, but a private gain. This isn’t acceptable – the cost should be carried by the financial sector.

So radical reforms are necessary, and greater stimulus is needed, not least to support the labour market. If you are keen to read more of Joseph Stiglitz’s thoughts, then I have a signed copy of his book Freefall. The person who is closest to guessing where Greece 5y CDS is at the close of Monday 15th February wins (we’re taking the GCDS page on Bloomberg). To give you a guide, it started this year at 283, mounting credit concerns meant that it closed at 426bps on Monday this week, before rumours of a bail out saw it close at 375 on Tuesday 9th February.

Click here to email your entry. Click here to read and print off competition terms and conditions. All entries to be received by midnight Sunday 14th February 2010.

This competition is now closed.

The information we collect from you is used solely to contact you in the event that you have won and the winners name may be publicised.

Britain has run debt to income ratios way in excess of current levels at several points in its history. Around the times of the Napoleonic War, and both the First and Second World Wars the debt to income level exceeded 200% – levels that today would be regarded as crippling and would lead the markets to expect imminent default. Yet there has never been a formal default, and much was made about the UK paying off the last of 50 instalments of World War 2 debt to the US and Canada in 2006.

But it cannot be said to be true that the UK’s credit record is unblemished. In their brilliant book, This Time Is Different (we’ve plugged it before), Reinhart and Rogoff do not have Britain in their very short list of six nations that have never defaulted (New Zealand, Australia, Thailand, Denmark, Canada and the USA). There are (at least?) two instances of the UK defaulting. In 1932, in the grip of the Great Depression, Britain (and France) defaulted on First World War debt to the United States – the so-called inter-allied debt. Britain had linked its ending of paying of these debts to the premature end of German reparation payments earlier in the year – academics therefore have termed this an “excusable default” where Germany was the real defaulter. The Americans didn’t seem to be especially cross about it in any case, although it was done without consent.

Another event that I would classify as a default was the changing coupon on the gilt known as War Loan. Issued in 1917 (“If you cannot fight, you can help your country by investing all you can in 5 percent Exchequer bonds. Unlike the soldier, the investor runs no risk”, the adverts said), the bond’s coupon was reduced from 5% to 3.5% in 1932. You can read Chancellor Neville Chamberlain’s speech announcing his plan in Hansard, here. This was a voluntary conversion – you could have had your money back – but the moral screws were on. Chamberlain ends his speech saying “For the response we must trust, and I am certain we shall not trust in vain, to the good sense and patriotism of the 3,000,000 holders to whom we shall appeal”. 92% of holders accepted the new, lower coupon (probably not just for patriotic reason, but because 3.5% was still a better rate of interest than was available elsewhere in those deflationary times). Today, we have seen the ratings agencies classify similar events as defaults, even if such disadvantageous changes were consensual.

Perhaps just as interesting is the question – why didn’t the UK default more often? A paper called Sustainability of High Public Debt: What the Historical Record Shows by Albrecht Ritschl suggests that it isn’t obvious why it didn’t. Post WW1, growth was disappointing, in contrast with expectations of a peace dividend. Yet even during the deflationary years between the wars (1926 to 1933) the conservative establishment view was to run budget surpluses, and to go onto the Gold Standard (until 1931), which didn’t allow a devaluation and thus help boost UK exports. Why the UK decided to beggar itself rather than default was in part due to the culture in the Treasury (the “treasury view” was hardline), and also due to the emergence of the United States as a rival economic power and financial centre. Post WW2, Ritschl argues that Marshall Aid was effectively a “rescue operation” that prevented a default. So reputation is extremely important in preventing default, the competitive threat from other financial centres matters, and having allies with deep-pockets (Germany or the IMF in the case of Greece?) can also prevent defaults. Remember the golden rule – willingness to pay is as important as ability to pay. Britain was willing to accept austerity in the 1930s to maintain its reputation; Ecuador has defaulted with a debt to GDP ratio of under 20%.

So to the present day. This weekend the papers were full of headlines about Conservative leader David Cameron postponing austerity for the UK. Today, in what looks like a different view, his Shadow Chancellor George Osborne has committed his party to maintain the UK’s AAA credit rating: “Judge us in the first few months of a Conservative government on whether we’re able to protect our credit rating”. I’d have thought that as a result, the UK’s 5 year CDS spread would have narrowed a little, but it’s stuck at 85 bps (we’ve written protection on Her Majesty’s Government because although fiscally we face a crisis, we don’t believe this will result in a default). Perhaps the market fears that the Conservatives are going to have a Devon Loch moment; the latest polls point to the forecast overall majority having slipped away, and a hung parliament is in prospect. With the UK economy at least growing again, albeit it only just, the chances of Osborne getting his chance to be Mr Austerity are slightly lower.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.