Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

The EM story is a strong one – in sharp contrast to the developed world, EM counties tend to have favourable sovereign/consumer debt dynamics, current account surpluses, high savings rates (implying scope for a pick up in consumer demand) and strong demographics. Continued globalisation and liberalisation should be to the advantage of these counties. Reflecting these opportunities, US mutual fund flows into EM debt have seen the sharpest increase of any asset class year to date versus this time last year, and I suspect it’s a similar story for EM equity. However you rarely hear about the risks in EM, only the opportunities, so I thought I’d try to present the other side of the argument.

The first thing I’d like to highlight is the risk posed by the sheer size of the flows themselves. Like the rest of the desk here, I’m a confirmed Reinhart and Rogoffian, and it’s easiest to just quote the authors;

“Countries experiencing sudden large capital inflows are at a high risk of having a debt crisis. The preliminary evidence here suggests the same to be true over a much broader sweep of history, with surges in capital inflows often preceding external debt crises at the country, regional, and global level since 1800 if not before.”…

“Emerging market borrowing tends to be extremely pro-cyclical. Favorable trends in countries’ terms of trade (meaning typically, high prices for primary commodities) typically lead to a ramp-up of borrowing that collapses into defaults when prices drop.”…

“The problem is that crisis-prone countries, particularly serial defaulters, tend to over-borrow in good times, leaving them vulnerable during the inevitable downturns. The pervasive view that “this time is different” is precisely why it usually isn’t different, and catastrophe eventually strikes again.”…

“There is a view today that both countries and creditors have learned from their mistakes. Thanks to better-informed macroeconomic policies and more discriminating lending practices, it is argued, the world is not likely to again see a major wave of defaults. Indeed, an often-cited reason these days why “this time it’s different” for the emerging markets is that governments there are relying more on domestic debt financing. Such celebration may be premature. Capital flow/default cycles have been around since at least 1800—if not before. Technology has changed, the height of humans has changed, and fashions have changed. Yet the ability of governments and investors to delude themselves, giving rise to periodic bouts of euphoria that usually end in tears, seems to have remained a constant.”

So, large capital inflows result in tighter credit spreads on external debt and lower yields on domestic debt, which eventually incentivise EM governments or corporates to issue more debt, and once the hot money goes into reverse the EM countries suddenly find themselves facing liquidity and/or solvency problems. There are a few early warning signs of this occurring, for example in just the past week, three Indian banks have taken advantage of strong EM investor demand for anything with a pulse and a yield to issue USD paper, while at the sovereign level, countries such as Korea do indeed appear to be taking advantage of cheaper financing conditions to increase local currency issuance. Others, particularly in Eastern Europe, are relying on capital inflows to finance budget deficits.

But EM debt levels are currently very low so there’s nothing to worry about, right? Well EM sovereign debt levels are lower than developed country debt levels, and the IMF estimate that this difference is likely to increase over time (see chart), but this is assuming that this time it really is different and EM countries don’t go on a debt binge. Also, it’s important to note that a comparison of developed and EM countries is potentially misleading. EM countries have a much lower tolerance for debt than developed countries for a number of reasons, including investors having greater confidence in the strength and independence of institutions, developed countries having greater credibility with investors (owing to a history of honouring their debts), developed debt markets offering superior depth and liquidity (allowing debt to be more easily rolled over), developed markets demonstrating a history of greater macroeconomic stability and tax revenues in developed countries typically being much higher as a percentage of GDP. All these things mean that bond yields (and hence interest payments) tend to be lower in developed countries, allowing higher sustainable debt levels as a percentage of GDP.

But EM debt levels are currently very low so there’s nothing to worry about, right? Well EM sovereign debt levels are lower than developed country debt levels, and the IMF estimate that this difference is likely to increase over time (see chart), but this is assuming that this time it really is different and EM countries don’t go on a debt binge. Also, it’s important to note that a comparison of developed and EM countries is potentially misleading. EM countries have a much lower tolerance for debt than developed countries for a number of reasons, including investors having greater confidence in the strength and independence of institutions, developed countries having greater credibility with investors (owing to a history of honouring their debts), developed debt markets offering superior depth and liquidity (allowing debt to be more easily rolled over), developed markets demonstrating a history of greater macroeconomic stability and tax revenues in developed countries typically being much higher as a percentage of GDP. All these things mean that bond yields (and hence interest payments) tend to be lower in developed countries, allowing higher sustainable debt levels as a percentage of GDP.

Maybe EM debt levels aren’t so low after all. In the recent paper ‘Growth in a Time of Debt‘, Reinhart and Rogoff find that economic growth has historically deteriorated markedly for a country with a public debt ratio above 90%, and for an EM economy with an external debt/GDP ratio of greater than 60%. Some EM countries are approaching (and a few in Eastern Europe are exceeding) these levels. Also, note that in ‘Debt Intolerance’, another paper that Reinhart and Rogoff wrote with Miguel Savastano in 2003, the authors find that 50 percent of sovereign defaults or restructurings since 1970 took place with external debt-to-GNP levels below 60 percent. Mexico defaulted in 1982 with a debt/GNP ratio of 47%, Argentina in 2001 with a ratio of just above 50%.

Inflation poses a significant risk to the EM story. Food and energy tend to be a much bigger part of the consumer basket for an emerging market than a developed market, so for example in Turkey (where CPI inflation in the year to February was 10.1%) food and energy forms about 30% of the inflation basket, while in India (where the Urban CPI rose 16.9% in the year to January) food prices are between 46 and 69% of CPI, depending upon which index you look at. If you believe in the EM story, you’re likely to believe in the commodity story too. Yet further commodity and food price rises risk destabilising many EM countries and could even risk derailing the global economic recovery in general. We could see the return of public unrest and tariffs (and with this the risk of more inflationary pressure), threatening a repeat of the experiences of many emerging markets in 2007 (see one of Richard’s old blogs here).

What about other risks? Each EM country obviously faces specific risks, so it may be worth very briefly focusing on each of the BRICs in turn.

Short term, Brazil faces uncertainty around the election and upwards inflationary pressure (with a series of rate hikes likely), but a far bigger medium and long term problem is the huge infrastructure spend necessary. A senior analyst at S&P told us that Brazil needs to spend an enormous US$500bn on all its infrastructure projects in the next five years, which includes things like the 2014 FIFA World Cup, 2016 Olympic Games as well massive oil project expenditure. S&P suggested that US$500bn is actually a conservative estimate and only gets infrastructure to ‘Brazilian standards’, as opposed to ‘Western standards’. The Brazilian government is looking at project finance initiatives to pay for this but it won’t be easy, and Brazil’s net public debt/GDP is already around 50%.

Russia is essentially an oil play – its budget is based around $59 per barrel, above this and it’s fine (in fact it’s more than fine), below this and the country and its fragile banks could easily unravel. I’ve already mentioned India briefly above, but as well as facing a potential inflation problem, India also has high deficits and high debt levels for an EM county (70% debt/GDP), making it potentially vulnerable. And finally there’s China, where the rate of credit growth looks like bubble-esque, and as we know, bubbles usually go pop rather than deflate in an orderly unwind. Then there’s the brewing trade spat with the US regarding China’s currency pegging policy, and probably most importantly of all, like any other country with limited political liberties, a negative economic shock can easily spiral into political upheaval.

Looking at emerging market debt specifically, it doesn’t look like markets are factoring in these risks, particularly in relation to hard currency debt. For example, long dated Indonesian USD denominated bonds yield 6.5%, which is only 1.7% more than US Treasuries, and arguably that’s not enough for a country that’s still rated junk. Ten year Lebanon USD denominated debt yields 6.3%, or 2.4% more than US Treasuries – is that a big enough yield premium for something rated B, which is only five notches above D for Default? I had a large investment bank tell me earlier this week that the 7.7% yield on some bonds issued by the Development Bank of Kazakhstan bonds was “the best risk adjusted thing out there”. They may well be right, but if so, it doesn’t say much about value in the rest of the market! Local currency EM debt still offers some opportunities, but many currencies have already come a long way.

In sum, I still stand by what I said in November – the rally in risky assets we’ve seen is largely liquidity driven, and due to deep concerns about the sustainability of the recovery, the authorities are only withdrawing the extraordinary stimulus measures very gradually. Until we see a speeding up of fiscal tightening and the beginning of monetary policy tightening, the risk rally will most likely continue over the short term, and this would be expected to continue to support emerging markets. But it doesn’t seem that the risks facing EM are getting sufficient coverage, and there are potentially significant medium and long term issues to be aware that don’t appear to be getting priced in.

Whether ’tis nobler in the mind to suffer

The slings and arrows of outrageous inflation,

Or to take arms against a sea of inflation expectations,

And by opposing end them?

Never has Shakespeare been so crudely adapted, but I am going somewhere with this so bear with me. There is an interesting debate currently taking place amongst economists regarding the subject of inflation. On one side we have the intellectual heavyweights of Olivier Blanchard (The Chief Economist at the IMF), Paul Krugman (winner of the Nobel Prize in economics) and Ken Rogoff (Harvard University Professor, former IMF chief economist and chess Grandmaster). On the other side we have the men in charge of monetary policy.

We are now all familiar with the actions that governments and central banks had to undertake in the aftermath of the financial crisis. Record low interest rates, huge fiscal stimulus (and hence deficits) and extraordinary policy measures such as quantitative easing have been the medicine that economies like the US, Europe and the UK have needed to support their respective financial systems. Ironically, the financial market investors that took excessive risk and had to be saved by governments are now punishing those governments that bailed them out.

There is now a considerable divide in opinion about what should be done to address the deficits and general debt levels that many nations now face. In Rogoff’s view as shown in The Guardian, “it is time for the world’s major central banks to acknowledge that a sudden burst of moderate inflation would be extremely helpful in unwinding today’s epic morass” (a morass is an area of low-lying, soggy ground – I had to look it up). On the large amount of debt that governments have, Rogoff noted that “Moderate inflation in the short run – say, 6% for two years – would not clear the books. But it would significantly ameliorate the problems, making other steps less costly and more effective.”

Rogoff is probably the punchiest in the ‘we should be targeting higher inflation outcomes’ debate. But Olivier Blanchard isn’t far behind, especially considering where he is currently employed. Blanchard says that the financial and economic crisis has “exposed flaws in the pre-crisis policy framework” and “forces us to think about the architecture of post-crisis macroeconomic policy”. He notes that “If we had had more margin to play with on interest rates, we would probably have had to use fiscal policy less [in the recession]”. He believes that higher inflation and higher interest rates in normal times would have costs, but this may be a price worth paying because it would make monetary policy more effective during crisis periods.

Not to be outdone, Krugman believes “even in the long run, it’s really, really hard to cut nominal wages. Yet when you have very low inflation, getting relative wages right would require that a significant number of workers take wage cuts. So having a somewhat higher inflation rate would lead to lower unemployment, not just temporarily, but on a sustained basis.”

And what do the central bankers think of all this? Certainly they are not too pleased, after spending the large majority of their careers attempting to gain credibility for a low inflation targeting monetary policy regime. This was Trichet’s response in the recent Q&A on monetary policy to a question on Blanchard’s IMF paper suggesting an inflation rate target of 4% may be more appropriate than the current 2 % target:

“I would say that it is plain wrong. That is my opinion and I believe it is the opinion of all central banks I know… I think it is totally counterproductive in the present period, when we have to cope with a difficult situation, to contribute to unanchoring inflation expectations….it is extremely dangerous…”

Inflation targets are unlikely to be changed for now and the debate at this stage appears to be purely academic. However that doesn’t mean that inflation targets can’t or won’t be changed in future. Economics is an evolving discipline – it was as recently as the 1980s that the UK targeted the money supply, but this was abandoned when it became clear that the policy didn’t really work and led to unsatisfactorily high levels of inflation. Inflation targeting has gained traction internationally since the early 1990s, and had – until recently – been deemed a success pretty much universally. It’s dawned on people that maybe a low and steady inflation rate wasn’t due to targeting, but was simply due to the opening up of China and globalisation generally, which helped improve technology and led to productivity gains. Arguably the natural state for the world in the past two decades was deflation, but deflation of a good kind – falling prices due to better productivity, as experienced in the US in the late 19th century. Trying to hit an inflation target meant running unnaturally loose monetary policy, which helped contribute to the bubbles we saw in the noughties.

I think fiddling with the inflation target may be the wrong debate to be having right now. Certainly in the current environment, securing a self-sustaining recovery whilst maintaining low and stable inflation expectations is the thing that is of most importance to politicians and central bankers alike. And let’s not forget, it’s the politicians that set the appropriate target for the central bankers. Perhaps implementing in the UK and Europe a US style ‘dual mandate’ – targeting full employment and price stability – is more appropriate in the current environment.

Never get too gloomy about the prospects for mankind. We’re good at stuff. Whilst most of us were wasting our lives in economics lectures and going to Happy Mondays concerts, the geeks were out there saving the future. Of course we’re going to run out of fossil fuels at some stage this century (the Peak Oil theory suggests that we’ve already gone past the hump of maximum production of oil) but the internet is getting excited about recent developments in fusion energy.

Previous attempts to create fusion energy have relied on extreme high temperature and pressure to force atomic nuclei together, thus releasing energy (cleanly, there is no harmful waste in contrast with fission); and in addition the end result has not been net gain – the output from the reaction is only 65% of the energy required to create the fusion. Recent developments (funded by the US Navy) of what is known as a polywell, which does not require extreme heat and pressure, look really promising. The developers are currently in Phase 2 – the final phase which could end in 4 or so years time is Phase 3. In the words of a fusion research charity, EMC2: “successful Phase 3 marks the end of fossil fuels”!

We can’t get too excited, but it does feel that we humans are not too far away from virtually free, unlimited energy. Obviously the US Navy will want to develop a giant killing ray with it, and will get first dibs, but after that, the implications for everything from transport, food production, inflation and global warming are incredible, and the industrialised nations will no longer have to rely on energy supply from unstable regions of the Earth.

With the latest Beckham injury hitting both the front and back pages of our national newspapers, the FIFA Football World Cup will soon rival talk of elections and budgets for headlines. We are about to be bombarded with messages from numerous corporations eager to use the tournament to expand their profile within the consumer psyche.

Apart from the usual car, razor and fast food companies vying for attention, financial institutions will also use some astute advertorial and promotional techniques in order to court new customers. For example the Spanish bank, Banesto, is using the World Cup in South Africa to push three new financial products; Firstly, a mortgage which offers €1,500 worth of appliances from another corporate partner of the Spanish football side. Secondly, a credit card that gives you a Spanish scarf and T-shirt to support the national team after an initial spend. And finally, Banesto are offering a deposit account with a 3% interest rate that will jump to 4% should Spain win the World Cup.

Interestingly, renowned investor Warren Buffett has recently let it slip that he will be hoping France doesn’t win. It turns out that an insurance company that Buffett has an interest in underwrote a large bet on the French side. To quote – “If France wins the World Cup, I think we’re going to lose about 30 million bucks or something like that”.

In addition to looking at what a World Cup can offer the individual investor it is worth noting how an event of this magnitude may impact the local economy and also that of the countries participating.

The South African treasury estimate that GDP will be boosted by 0.5 per cent as fans follow their teams to the country for the world’s most watched tournament. South Africa has spent 33 billion rand (almost £3 billion) and more than 130,000 jobs have been created between 2007 and 2010. At the previous world cup in 2006 the German Government estimated over €3 billion was added to the economy with €400 million pumped into the country during the month of the world cup . It is estimated that this boosted German GDP by around 0.4%, the direct result of a large increase in consumption.

The impacts of the world cup are not only felt in the host nation. Studies by the Centre for Economic and Business Research estimated that the cost of England missing the European Football Championships in 2008 was around £1 billion. ABN AMRO economists estimate that winning a world cup can add 0.7% to a country’s economic growth. They note that “good performances on the soccer field often go hand in hand with performances in the stock market and economy”. Additionally, after the last three tournaments the winning finalist’s stock market has outperformed the losing finalist’s. Has Thierry Henry’s handball cost not only Ireland’s place at the World Cup but also it’s chances of an early exit out of recession?

And who does the IMF think will be the best performer of the 32 finalists? As we can see in the chart, the IMF estimates that Ghana will grow by 5 per cent in 2010 closely followed by Nigeria.

I suppose this adds a little more pressure on those penalty kicks!

The Bank of England is trying to boost the number of £5 notes in circulation – their chief cashier Andrew Bailey (whose signature is on every new banknote) said “our evidence suggests that the public wants more £5 notes”. The general public are demanding more of the lowest denomination banknote? On our desk we have some Reserve Bank of Zimbabwe One Hundred Billion Dollar notes, and, from a trip less than a year later some One Hundred Trillion Dollar notes (100,000,000,000,000). In an inflationary environment, the public demands higher and higher denominations of banknote. In the UK we want the lowest possible denomination. This looks like a deflationary sign.

Yesterday the UK’s FSA came out with a Liquidity Calibration statement. We’d thought that the authorities might try to kill two birds with one stone, and force banks to hold more in quality, liquid assets – the banks would then be more liquid in case of market turbulence, and the government would find a new, big source of demand for its never ending supply of gilts. This statement has delayed that – “the FSA believes that it would be premature to increase liquidity requirements across the industry at the current time”. Given the weakness of the economic recovery, the FSA doesn’t want banks to be forced sellers of risky assets (including loans to the private sector) – but this is clearly bad news for the UK’s ability to find buyers for its gilt issuance.

Journalist Andrew Rawnsley put the boot into David Cameron in his Channel 4 Dispatches documentary last night, concluding that if the Conservative leader in opposition doesn’t have any real guiding principles now, he will struggle badly if elected to government. The public seem to feel this way too, and additionally undecided voters in vulnerable jobs (especially in the public sector) fear the threat of higher Tory cutbacks post the election. This explains the collapse in the Tory poll lead – down to something like 2-5%, with some polls showing Labour and the Conservatives neck and neck in even the marginals, despite non-dom Lord Ashcroft’s windfalls for Conservative candidates’ campaigns. So a hung parliament looks more and more likely. I’m not sure it would be the end of the world however; a coalition might find it easier to sort out the public finances, as it would have safety in numbers and not have to take sole responsibility for a period of high unemployment and cuts to public services. Also, past examples of coalitions have not necessarily been disastrous – the UK’s greatest moment of national crisis, World War 2, was fought under a coalition government. A paper from the Hansard Society looks at the history of such coalitions, and concludes that a hung parliament might be a great opportunity. “Parliament would be strengthened because parliamentary votes would be less predictable and therefore crucial”. Buy the pound and sterling assets whatever the election result is?

If you thought Greece was bad, have you seen California lately? It’s a good comparison, because both are credit-challenged nations within a single currency area. At least Greece is not terribly systemic at 2% of EU GDP, whereas California is 14% of the US economy (France is 16% of EU GDP). Too big to fail? California was badly hit by the crash in subprime housing, and tax revenues have fallen sharply. S&P just downgraded its debt to A- (Moody’s is at Baa1) and its 5 year CDS trades at 250 bps versus Greece at 280 bps, and the US as a whole at 35 bps. Things have got so bad for California that it started to print its own currency last year – in July it issued IOUs to individuals and businesses who were owed tax refunds. Effectively it is trying to bypass the single currency area, by issuing parallel money – but one dollar of Californian IOU is not worth a proper dollar in any free market. Especially if you call them “revenue anticipation notes” – come on, at least a doubloon or groat would sound like proper pretend money? Some crunch dates coming up for the Californian budget – sovereign worries in Europe have faded a little in the last week or so, might the spotlight head to the US next?

And finally, a great article about Come Dine With Me, the TV competition where amateurs take it in turn to cook for each other and then are rated by their fellow competitors to try to win £1000. Economists spend a lot of time and money trying to create experiments like this (OK they just bribe some undergrads with a couple of those rare UK blue fivers). Come Dine With Me provides a closed environment where you can see that the rational economic man, beloved of all economic models, does not exist. The rational score to give your rivals is zero – that never happens. Read the article for that, and other micro-economic insights (“Regret – if Rachel had known how big an arse Stuart was she would not have scored him so highly”).

Inflation rates, at least in the non-emerging markets, remain low. US core inflation (CPI less food and energy) was negative in January, the first month on month decline since December 1982. Preliminary German CPI in February was +0.3% year on year. Japan hasn’t recorded a positive year on year inflation rate since January 2009.

Things seem different in the UK. The annual UK inflation rate jumped to 3.5% in January, prompting Mervyn King to write yet another letter to Alistair Darling explaining why CPI had breached the upper limit of 3%, and prompting Darling to write yet another response.

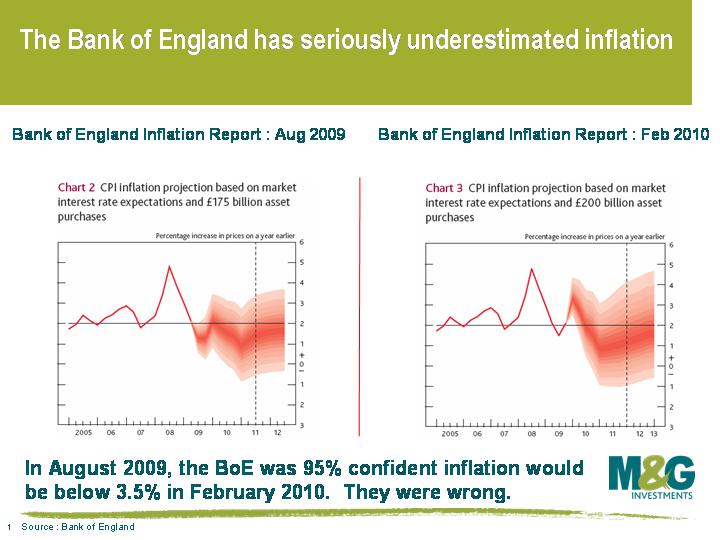

The BoE is confident inflation will fall, and has been busy telling people to relax, it’s just temporary, nothing to worry about, we said it would fall last time it was a bit high and we were right. But in August 2009, the BoE was about 95% confident that inflation would be below 3.5% in January 2010. They were wrong (see below). An ex-member of the MPC recently described the BoE’s fan charts to me as being “rivers of blood”, and the FT announced that it was not going to publish the fan charts any more. The market is getting worried about the accuracy of the BoE’s inflation forecasts.

Why is the UK inflation rate worryingly high and what’s likely to happen in future? ‘Base effects’ are usually given as the main reason inflation has picked up – inflation is a year on year number, the oil price was below $50 a barrel at the beginning of 2009, it’s now $80, and petrol prices have therefore risen. The good news is that base effects should prove temporary, unless the prices of things like oil continue rising rapidly or we see second round effects (eg higher wages). But is this the reason the BoE has significantly underestimated the UK inflation rate? I don’t think so – in August 2009, the Bank of England knew what had happened to energy prices in the first half of 2009 and would have factored this into their inflation projections. Since August, energy prices (which are admittedly a small part of the CPI basket) have barely moved, and besides, other countries don’t seem to have experienced base effects to anything like the same extent as the UK. So there’s clearly something else going on.

Government policies have definitely had an effect, particularly changes in VAT. The jump in UK CPI from 2.9% to 3.5% last month was partly due to the year on year numbers reflecting January’s increase in VAT from 15% to 17.5%. This effect will continue to be felt through to the end of this year when the VAT increase works its way out of the annual inflation numbers. We’ll probably therefore see elevated inflation levels until then, and again, this effect should be temporary. But, I think VAT is very likely to be increased to the EU average of 20% after the election, AND we may see a number of items that are not taxed (eg most food, children’s clothes, gambling, lottery tickets, museum tickets, antiques, water supplied to households, funeral services, incontinence products, freight, postage, newspapers, loans) start to get taxed. We may also see an increase in the tax rate on items that carry a reduced VAT rate (eg energy, some construction). Additional VAT increases this summer would put further upwards pressure on inflation, keeping inflation elevated until at least the second half of next year.

The third commonly cited reason for higher UK inflation is the weakness of sterling. This does not mean that sterling has been weak over the past twelve months – in the year to the end of January (the period covering the last annual CPI release), sterling actually appreciated about 10% against the US dollar and was up 4% on a trade weighted basis. What matters more, as explained in Mervyn King’s letter, is that we are still feeling the lagged effects of sterling weakness in 2007 and 2008. I think this lag effect is a very important point, and probably goes a long way to explaining why economists and probably the Bank of England themselves have underestimated inflation over the past year. Things like companies currency hedging, retailers setting prices months in advance and wage settlements being based on the previous year’s prices mean that there’s a significant lag effect between a currency rapidly depreciating (which increases the cost of imports) and these import price increases being passed onto consumers. Import price inflation peaked at more than 13% in December 2008, the highest rate since our data series began at the beginning of 1981. Michael Saunders of Citigroup has estimated that import prices lead consumer goods prices by a massive 30 months, and if this correlation between import prices and consumer good prices holds, then we could well see further upwards pressure on UK inflation through the remainder of this year and into the beginning of next year.

All these things suggest that UK inflation rate may be a lot stickier than the Bank of England expects over the next 12-18 months However, it’s important to stress that these effects should be temporary, and there are a lot of deflationary pressures going on right now which should prove longer term in nature.

We’ve talked about these longer term influences many times before. Money supply remains extremely weak – M4 broad money supply was flat month on month in January, and only +0.9% year on year versus +3.5% in July 2009 – just think what it would have been without any QE! (Note that this figure is using the BoE’s policy of stripping out the deposits of ‘intermediate other financial corporations’, which excludes things like counterparties and SPVs). Spare capacity is still huge, and very importantly, the enormous trimming in the budget deficit and cut in government spending that is absolutely necessary and will definitely happen will have a major negative impact on growth, meaning that spare capacity is here to stay. Bank lending remains subdued, as evidenced by a dropping away of mortgage approvals in recent months from already pretty feeble levels – the authorities’ continued failure to generate meaningful demand for or supply of credit should keep inflation suppressed.

I wouldn’t put it quite as strongly as the MPC’s Adam Posen, who last month said that “any of you betting on high inflation in major economies, including the UK, will lose money” – there are certainly upside risks (eg sterling collapse, underestimation of the inflationary effects of QE) – but on balance there’s little to suggest that we’re going to have inflationary pressure beyond the next 18 months.

Having just returned from a couple of weeks in Australia for a friend’s wedding (all the best to the happy couple) I thought it might be worthwhile writing a note on what looks to me to be a bubble in the Australian property market.

On my first night out in Sydney I was fortunate enough to get chatting to a couple of the locals who were out celebrating, one of them having just completed the purchase of her second property. The other, who already has two, thought it totally normal that two girls in their mid 20s – one an interior designer, the other a shop assistant – should be able to do this.

A couple of mornings later, I was reminded of this conversation whilst reading an article that I felt I had seen many times before. The journalist was bemoaning the state of the market – house prices ballooning, first time buyers unable to get on the ladder, demand outstripping supply…..sound familiar?

After the wedding I headed up the coast to a small beach town for a change of scenery. The train journey was made interesting (if a little irritating) by an old lady at the other end of the carriage who must have forgotten to turn her hearing aid on that morning. She spent a good half hour telling a friend and the rest of us in the carriage about her grandson who was playing the property market. Apparently he has accepted an offer on his house and then pulled out in the hope of achieving a higher price twice already, and is considering doing the same again.

Once in my beach town (and gratefully out of earshot) I counted no less than seven estate agents/mortgage brokers in the parade of about 50 shops along the beach front. If I wasn’t already thinking “bubble?” I was now. So on a rare cloudy afternoon I popped into a few banks curious of what mortgages were on offer. Mostly I just picked up the standard leaflets but in the branch of one of Australia’s big 4 banks a very helpful member of staff offered me a seat so we could talk about my “options”. Once the disappointment of not being able to sign me up had passed, she told me how busy they had been and how the majority of people signing on for new deals were opting for variable rate mortgages.

With at least a 20% deposit on a property worth A$250,000 or more, the lowest variable rate one can achieve is 5.79% and 6.49% fixed for a year at this particular bank. Encouragingly there were no deals I could find that were offering an LTV of greater than 95%. However there was a decent amount of literature on re-financing existing deals and suggestions on how this cash could be used. Rather scarily one of these was to invest in the capital markets – and yes, you can trade on margin.

My helpful mortgage advisor also mentioned that a lot of re-financing took place last year when rates were at their lowest for some time. With every passing minute spent talking to her the bubble in my mind’s eye was growing larger.

Mortgage repayments increased by an average of 25% in Sydney in the 4th quarter of 2009, and if the experiences of this mortgage advisor are representative of Australia as a whole, last night’s rate rise from the RBA (of 0.25% to 4%) together with the further anticipated hikes that may be necessary to tame inflation could lead to tough times for mortgage holders further down the road.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.

{kind=link}