Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

A couple of short youtube clips from Australian satirists John Clarke and Bryan Dawe. We thought it might give you a chuckle before the long weekend.

For an explanation of how the financial system works, click here. To gain an insight into the European bail-out package, click here.

Enjoy!

I wrote a while back about the Spanish Bank Banesto offering a deposit account that jumped from 3% to 4% should Spain win the world cup. In the UK, Nationwide has followed suit and is offering a 4 Year Football Bond that increases from 4.15% to 4.65% should England emerge victorious at this summer’s tournament. The investors in this product will be hoping for the swift progress for the national side and successful qualification on the 23rd of June to the knock-out stages.

Chancellor George Osborne may be hoping that England’s final group game on the 23rd of June may take some attention away from his emergency budget on the 22nd. While welcome, the pre-announced £6.2 billion of spending cuts (dropping to £5.7 billion once £500 million of the cuts is reinvested in education) only results in a 1% reduction in government spending, taking the budget deficit from £156bn to £150bn. Removing consultants from the public sector and cutting the first-class travel allowances of civil servants will only go so far.

As the 22nd of June approaches, the cuts will need to be furnished with detail. Hits to core services and job cuts will need to be deliberated, and potential changes to VAT, capital gains and inheritance taxes will need to be negotiated. Neither party in the coalition will be keen on losing ground or face in this first real test of its co-operation. The impact difficult decisions could have on the public sentiment will be at the forefront of both party’s minds, with the temptation for each party to attribute popular cuts to their own invention whilst deflecting damaging decisions to the other side. This first budget could outline the initial fault lines between the two parties that may sculpt the political landscape for this coalition government and potentially the next election.

In yesterday’s speech, the Queen declared that this government’s “first priority” is the reduction of the UK’s deficit, increasing the pressure on both the Chancellor and Chief Secretary to deliver a robust and achievable budget in 28 days’ time. The requirement for this budget to deliver a more sustainable economic outlook for this nation is paramount and the fact that it will be a joint effort will only underline its importance. Come the 22nd of June, all eyes should be on this budget, and I doubt Capello’s boys will be able to do much to distract the attention.

It appears that developments have moved on quite dramatically since my last blog on the market describing the political dynamics between governments and capitalist investors (insert speculators here!). There are a number of key points in the latest round of sparring that I think should be highlighted.

Firstly, European governments have taken the kind of action speculators respect and can’t ignore. European authorities shocked markets last week by announcing a huge €750bn bailout fund for the eurozone . Additionally, the European Central Bank said that it was ready to purchase eurozone government and private debt to ensure depth and liquidity in markets. The ECB has noted that it will sterilise the bond purchases, meaning that it will not quantitatively expand the money supply like in the UK. After an initial bout of investor exuberance the enthusiasm of market participants has waned since the announcement. It has dawned on everyone that Europe still faces significant hurdles and there are growing fears that the situation could send the global economy back into recession.

Secondly, as Stefan wrote yesterday, the German authorities have decided to attack market disorder and valuations by banning naked short selling of European government bonds, credit default swaps, and some German financial securities. This is the type of action that speculators can not ignore, and will not respect. The move by the German authorities has caused confusion and uncertainty in markets. France was quick to say that it will not follow suit and said these measures could actually hamper market liquidity. The move raises more questions than answers. For example, how will it be applied? Who does it apply to? Which jurisdiction does it apply to? How will it be monitored? How will investors be prosecuted and fined if found guilty of short selling? I am sure you can think of even more.

These are serious questions for market participants. Unfortunately, markets do not close while we await the answers of the above. The effect will be to increase uncertainty, make markets less efficient, and could therefore possibly increase risk premiums. One would think that these results are the opposite of what the authorities are trying to achieve.

As I write, trying to understand the above new set of rules is vexing many market participants. I think the issue will be that if governments start to try to fix the price of markets at a set level through political and legal policy, the invisible hand of the markets could well be inefficiently bound. Increasing regulation in Europe will see investors increasingly look at other markets to invest in. I hope the European governments realise that they are still going to need to borrow in the coming months and years, and to do that they will need a big, deep, and liquid market.

At this stage the details are very limited but it appears that the German supervisory body BaFin has banned the “naked” short selling of Eurozone sovereign bonds, their credit default swaps, and the shares of ten leading German financial institutions. The ban was effective as of midnight last night.

This move by the German authorities has had the effect of spooking already fragile markets. As we have discussed before markets do not like a lack of transparency and these actions appear to be draconian and uncoordinated. The fact that the ban was announced after the European market closed and was implemented only a few hours later is nothing short of reckless and has the market speculating about larger, unknown problems.

The S&P 500 closed about 1.5% lower last night and European markets are currently seeing a flight to quality on their open.

This announcement appears to be largely symbolic and arguably politically driven. The vast majority of derivative trading that Germany has banned actually takes place outside of Germany. The German authority simply does not have the legal jurisdiction to implement the ban in major financial centres like London and New York in respect of non-German domiciled institutions. It is a question for the lawyers whether this ban extends to German domiciled financial institutions trading in different jurisdictions, either through branches of the German domiciled parent or through foreign domiciled subsidiaries.

I wouldn’t be surprised if domestic German institutions are able to find a way around the legislation. The unintended consequences may see ‘speculators’ merely reset their positions in markets that fall outside of the scope of the ban. Will investors express their negative view on Europe by further selling the Euro currency?

As with the recent $1 trillion package to support the Eurozone the short selling ban is an effort to buy time and take pressure off the EU economies. The fact is that neither of these actions address the long term solvency of a number of Europe economies and is likely to further set the cat amongst the pigeons.

Mervyn King introduced himself to George Osborne last night by writing him a letter, not to wish him luck in his new and frankly unenviable role, nor to advise him on just how much austerity is needed on 22nd June to keep the markets supportive of gilts, but instead to explain why he has again overseen a rate of inflation of more than 1% above the target rate of 2%. The letter states that the Governor should:

1. Explain why inflation has moved significantly away from the target.

2. State the period within which the Governor anticipates inflation to return to target.

3. State the policy action that is being taken to deal with it.

1. The CPI index rose to 3.7% year over year in April, up from a 3.4% rise in consumer prices the previous month, and not insignificantly 0.2% above the market’s expectations for where today’s number would be. The Governor blames oil prices, the VAT increase and the fall in sterling for the inflation miss (no mention of higher duty on cigarettes and alcohol!). He believes these three factors are temporarily boosting the inflation rate and expects that inflation will fall back over time to its desired level of 2% due to the output gap. We are sympathetic with the Bank’s argument that there is a significant amount of spare capacity in the economy at present and that this will likely see inflation fall in the future.

2. Mervyn King believes that it is likely that inflation will fall back to target “absent further price level surprises…..within a year”. What a nice performance target for the year, if you are an inflation forecaster (which, thankfully, Mervyn is not): he will hit his forecast unless he is wrong.

3. The Bank of England took unprecedented action in response to the huge contraction in demand at the onset of the financial crisis with the aim of keeping inflation near target in the medium term, by which I am referring to quantitative easing and near zero interest rates. The Governor today states that in this meeting the Committee felt it appropriate to maintain the current level of stimulus in the economy, citing an appropriate balance between downside risks (spare capacity) and upside risks (commodity prices, amongst others) to inflation.

So Mervyn’s seventh letter (now to his third different chancellor) once again explains that whilst inflation is substantially higher than where he and the MPC expected it to be at this time, and whilst inflation continues to come in higher than the market’s expectations, he and the Committee are happy for the extraordinary level of stimulus to remain in the economy for now, for fear of the fall-out that would result were stimulus to be removed too soon. This is a view we here have huge sympathy with. One only has to look at the panic in the Eurozone in recent weeks to realise that the current recovery is extremely fragile. On top of this, our new government has already announced an emergency budget for 22nd June, which will surely see fiscal tightening dampening some of the inflationary effects of monetary stimulus currently in the system.

So whilst there is sure to be some heavy criticism coming from the media and other commentators about the apparent ineptitude of the MPC to correctly forecast near term inflation, spare a thought for Mervyn. First of all, whilst the MPC has got near term inflation wrong (underestimating) for the best part of the last year, its remit is to manage medium term inflation, for which it has a strong record since its independence. My interpretation of the Governor’s citing the fragile balance between ‘upside’ and ‘downside’ risks to inflation is that it is actually a balancing of near term and medium term inflation, with the former on the one hand being boosted by extraordinary policy measures and the resulting global recovery, and the latter being justified by concerns about the recovery’s persistence and strength. Perhaps he realised that the MPC was too focused on short term inflation rather than medium term inflation when it left rates too low after the dot.com crash and then had them too high from 2007 as we approached the financial crash? This is a criticism that is surely all the more cogent when directed at the ECB?

Most importantly, though, give him credit for what he has achieved. Faced with collapsing global demand, a financial system in disarray, and a freezing and contraction in the velocity and quantity of money in the economy, extreme monetary and fiscal stimulus were a necessity. The fiscal stimulus and growth of the state that resulted from the crash has meant the UK’s and most of the western world’s levels of indebtedness have risen hugely too. And the very worst case scenario in a highly leveraged world is a deflationary spiral where prices for everything are falling whilst debts still have to be repaid in full. The lesser of two evils in this case is definitely some controlled or temporary inflation to reduce the real cost of a large debt burden (not to mention that the avoidance of deflation also enables monetary policy to maintain its efficacy). And on these terms, with positive growth, positive inflation, and a recovering housing market, perhaps it is time to praise, not criticise, the MPC for its decision to embark on quantitative easing? The range of decisions we face today as an economy are inestimably preferable to the ones we could have been facing now had we seen monetary policy inaction during the crisis. Well done Mervyn, inflation above a short-term target is a result.

With sovereign and political issues taking centre stage in markets recently, macroeconomic indicators have taken a back-seat in many market participants’ minds. But how have the advanced economies been recovering, absent these risks? Today I’d like to focus on some research on labour markets that was recently published by the International Monetary Fund (IMF) in their World Economic Outlook and the implications this might have on central bank interest rates.

Unemployment is a big problem at the moment and is a key challenge for policymakers globally. Strong labour markets generally result in higher consumption and wealth effects, generating higher standards of living and stronger GDP growth. Given this context, the IMF has sensibly asked: how long before employment recovers?

Sadly the employment reports to come out of the US, Europe and the UK have not made for comforting reading. In the US, the unemployment rate jumped to 9.9%, despite the fact that more jobs were created than in April than in any month in the past four years. In Europe, there are 23.1 million people out of work, and unemployment is still rising in 26 out of the 27 member states (the unemployment rate has fallen in Germany however, showing the unsynchronised nature of the economies within the Eurozone). Finally, the UK has 2.51 million people looking for a job – the highest level since December 1994. The UK unemployment rate, at 8 per cent, is at a level that has not been seen for sixteen years.

To help us assess the current state of labour markets in an historical context, the IMF has analysed unemployment developments in recessions and recoveries over the past 30 years in a number of advanced economies. Being economists, they have a rule to assist them in organising their analysis called Okun’s law. It’s basically the relationship between the unemployment rate and GDP. If the unemployment rate rises in a country, then its GDP will fall. If unemployment falls, GDP goes up. Pretty simple really. According to Andrew Abel and Ben Bernanke (Chairman of the U.S. Federal Reserve), estimates based on data from more recent years give about a 2% decrease in output for every 1% increase in unemployment.

The IMF has found that ‘the responsiveness of the unemployment rate to changes in output has increased over time for several advanced economies, due to less strict employment protection and greater use of temporary employment contracts’. The IMF suggests that Okun’s law – the responsiveness of the unemployment rate to changes in output – has increased over time. Labour markets are now suffering more in a downturn leading to higher unemployment levels, but in the upturn phase of the business cycle labour markets can improve quicker than they used to.

It’s an interesting analysis but the key findings for me are as follows. If we look at the chart by the IMF on the experience of the last 30 years the unemployment rate peaks 5 quarters after a “standard” recession, 6 quarters after a recession caused by a financial crisis, and 5.5 quarters after a recession caused by a house price bust. Employment tends to trough before unemployment peaks except during recessions caused by financial crises. In these recessions employment troughs and unemployment peaks 6 quarters after the economy returns to positive growth.

The recent readings in unemployment and employment are consistent in these findings. Taking the US as an example, we saw a large number of jobs created in April yet the unemployment rate increased. Why was this the case? It is because the participation rate increased, meaning that more people were actively seeking work. This is what economists call the “encouraged worker effect” – people outside the workforce seeing the economy improve and deciding to actively look for a job.

The IMF analysis is important, as we now know that the US and Europe exited their respective recessions in Q3 2009; and the UK registered positive growth in Q4 2009. Based on the IMF conclusions we can reasonably assume that unemployment rates in the US, Europe and the UK are unlikely to peak until around Q1 or Q2 2011, suggesting a deteriorating labour market and high unemployment rates for the remainder of 2010. Additionally, as we know from our discussion of Okun’s law, the unemployment rate responds to positive growth. With current unemployment rates ranging from 8 to 10 per cent Okun’s law suggests that we need to see a 2% increase in output above trend growth (trend growth is estimated to be around 2-3% for the major economies) to see a 1% fall in the unemployment rate. Is this really going to happen anytime soon?

If we turn now to an analysis of when the Federal Reserve raises interest rates after a loosening phase of monetary policy, we can see in this chart that the Federal Reserve tends to hike interest rates around 8 months after a peak in the unemployment rate. Using this as a rough guide as to when the Federal Reserve might start to raise interest rates from their historical low levels, an interest rate hike by the Fed is now moved out to around Q4 2011. Current market pricing is for a rate hike from the Fed in 6 months time in around Q4 2010. This looks like it could be too early given the IMF and our own analysis of past recessions. What are the implications for global interest rates if the central bank of the United States doesn’t hike rates until Q4 2011?

The reason I have focussed on the US is because it arguably has the best economic growth outlook at the moment from a fundamental standpoint. Key leading indicators like business confidence, housing starts, consumer confidence and retail sales look like they are recovering and have largely been beating economists’ forecasts over the course of 2010. Given the US does not have the concerns that Europe currently does over sovereign risk or the political and budgetary concerns of the UK, it may be the case that the Federal Reserve leads the European Central Bank and the Bank of England in hiking interest rates from their current historically low levels.

I suspect that the central banks will want to make sure that the recovery is self-sustaining, as indicated by rising employment levels and falling unemployment rates. Central banks want to see labour markets improving before they risk killing off the economic recovery. Given below trend economic growth, the absence of wage pressures and the limited pricing power of corporations to pass through rising producer prices to consumers, it is unlikely that inflation will be an issue in the short-term. In this type of environment I think that the Fed, ECB, and BoE will keep interest rates lower for longer than the market and economists currently expect.

Strong earnings results, low inflation expectations and a view that the ECB will have to keep interest rates lower for longer to support the economic recovery has seen demand for European corporate bonds remain fairly robust.

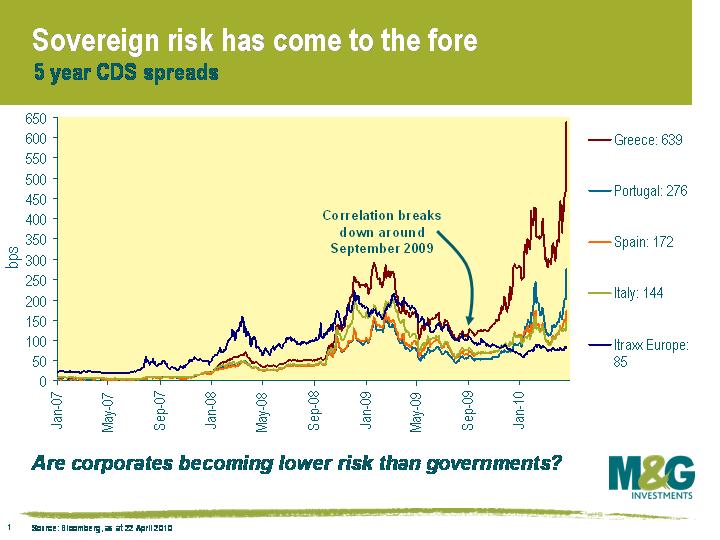

That is not to say that European corporate bond markets have been unaffected. Those credits that have been most impacted by the sovereign debt worries have unsurprisingly been domestic Greek and Portuguese corporations that have limited foreign earnings. It is clear to me that these corporations will continue to come under pressure from the market due to worries about lower earnings, higher taxes and continued speculation that some nations may leave the Euro. This is likely to be reflected in a higher spread for Greek and Portuguese corporate bonds over the equivalent risk-free government bond (which is currently German bunds). Some investors have sought the protection that is offered by credit default swaps (CDS) resulting in more pressure on cash bonds. CDS are seen as an early warning signal for bond markets, alerting investors to structural weaknesses before a crisis hits.

Interestingly, the once strong correlation between sovereign debt concerns and corporate bond markets appears to have now broken down. The iTraxx European index, a measure of creditworthiness of European investment grade credit, has tightened from September 2009. This is in contrast to countries that are located geographically on the periphery of Europe, where CDS spreads have had a tight correlation with Greek CDS. This phenomenon is highlighted in the attached chart. After the financial crisis of 2008 until September 2009, CDS spreads for investment grade credit and sovereign nations were highly correlated. Why is it that the risk of a sovereign crisis is not having the same impact on the European corporate bond market that it had from September 2008 to September 2009?

For me, there are a number of reasons. Firstly, unlike governments, companies have de-levered in the recession by cutting costs, unwinding or selling off assets, and have issued equity to retire debt. Secondly, unlike governments, companies have used favourable market conditions to extend their debt profiles. Thirdly, unlike governments, many companies are awash with cash. Fourthly, unlike governments, many high quality companies have not been affected by political uncertainties.

Given the above, I am not surprised that high-quality European corporate bonds have thus far remained insulated from the worries in sovereign markets. Corporations are operating from a strong starting position, with many having taken the necessary steps to improve their operating finances and balance sheets. Positively for the asset class, lending standards are improving and default rates may have peaked at levels that are much lower than the market expected. Corporate bond yields remain favourable, especially when compared to cash.

Peripheral European governments on the other hand are trying to stimulate weak economic growth, forcing them to borrow more and more. Rising government bond yields are making it difficult to borrow and causing debt servicing costs to increase markedly, as Greece has found out. Political tensions are rising, particularly in those countries where necessary austerity measures are required. Certainly, when economists from the Bank of International Settlements start writing things like “the aftermath of the financial crisis is poised to bring a simmering fiscal problem in industrial economies to boiling point” it is time to sit up and take notice.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.