Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

I went to the excellent Barclays Capital Inflation Conference a couple of weeks ago – although titled “inflation”, a lot of the conference’s content concerned the growing fears about the solvency of western governments. In particular, whilst the US Treasury market is currently seeing a massive flight-to-quality bid (10 year yields are now down below 3%) I came away worrying that it’s difficult to see that the US has any plan to avoid medium term bankruptcy other than some hopeful reliance on the American Dream to magic it all better.

Ken Rogoff (Professor of Economics at Harvard, and co-author of This Time Is Different) accused the US Treasury of “playing the yield curve”. With yield curves still extremely steep by historical standards, the authorities have skewed issuance to short maturities with the lowest interest rates (even though long dated maturity bonds would have historically low coupons despite the steep yield curve). Around half of all US debt will mature in the next three years – a tactic which keeps the US’s interest payment burden down in the short term, but which is a “classic way” of triggering a financial crisis when rates start to rise. This is the shortest debt maturity profile for the US since the 1960s. A huge burden of debt refinancing, coupled with higher interest payments was the trigger for Greece’s recent debt crisis. It’s another reason why we disagreed with Bill Gross’s “nitroglycerin” comments regarding the UK – the average maturity of the gilt market is around 14 years, compared with under 5 years for the US and 6 and 7 years for Germany and France. A “buyers’ strike” should be a little less problematic for the UK than it would be for the other nations.

Rogoff also talked about the prospects for financial repression as a method for governments to create a buyer for their debt when the natural, economically motivated, buyer has disappeared. Financial repression is the process of making people own assets they don’t want to hold – and the financial regulator is the important driver of this. In particular banks are encouraged (or forced) to hold more of their assets in less risky assets – i.e. government bonds – but also pension funds and individuals might find themselves being nudged into government bonds (in Japan individuals have most of their savings in the Japanese Post Office, which invests those savings in JGBs). Once domestic buyers are handcuffed, it becomes much easier to use inflation as a tool to reduce the real debt burden, especially in an economy like the US which has been steadily reducing the amount of inflation-linked debt it has outstanding as a percentage of the overall debt mix (although see comments below about the other inflation-linked government liabilities which stop inflation being the magic bullet policy tool).

Finally Rogoff said he’d be astounded if many Eastern European governments (and Greece) did not default, even with the IMF helping them. He pointed out that an IMF rescue package doesn’t always mean an economy is saved; in fact in 1/3rd of the IMF programmes since the 1970s default has ensued (including Argentina, Indonesia, the Dominican Republic and Turkey).

If you were nervous about the US keeping its creditworthiness after Ken Rogoff, a speech by Ajay Rajadhyaksha (Barclays Capital’s Head of US Fixed Income Research) piled on the anxiety. First the good news – the role of the US dollar as the primary reserve currency allows it to run excessive deficits far in excess of its economic rivals. Barclays have modelled the US’s AAA credit rating with an overlay based on the percentage of the world’s reserves kept in US dollars. On a stand alone basis, the US should have a AA credit rating, like Spain – but currently the US$ makes up 60% of global currency reserves, and this would allow them to run a 200% Debt/GDP ratio without losing their AAA rating, compared with the estimated 90% Debt/GDP level now. If the US$ became a bigger portion of global reserves (65%) then a 250% Debt/GDP ratio could be sustainable. Under current projections, only a fall in the dollar’s share of reserves to 50% would trigger the downgrade to AA. Even with continued diversification away from the dollar by foreign investors, this looks a long way off. However, once it happens the acceleration is severe – when Japan lost its AAA rating the yen fell significantly as a percentage of foreign portfolios, perhaps helping to trigger Japan’s further ratings downgrades.

That was pretty much it for the good news. Even at current low levels of interest rates, the US’s debt servicing costs take a step upwards in coming years, as the Debt/GDP ratio rises to 95% by 2020. If yields were to rise by 2% across the yield curve the percentage of US government revenues spent on debt service would rise from a troubling 17% now to around 33%! And inflating away that debt burden doesn’t work very well, as so much of the government’s outlays are indexed to inflation (although I guess you can always do what George Osborne did in last week’s UK Budget and change the inflation measure used to index benefits to one that is structurally lower, CPI rather than RPI). Radadhyaksha was also nervous about the US government’s contingent liabilities – losses on mortgages held by the GSEs (e.g. Freddie and Fannie) could be in the realms of $300 bn+. But the biggest contingent liabilities are the entitlements due to the US populations – and predominantly Medicare costs. After 2020, for every $2 trillion of taxes raised, spending will be $3.5 trillion. How do you close that gap without triggering a popular revolt, especially in an economy where median household incomes are only at the same level that they were back in 1998/99? Senator Judd Gregg, who some expect will run for the Republican Vice Presidential nomination next time round and sits on the Senate Budget Committee, suggested that the answer was to slash entitlements and cut taxes – this combination will encourage entrepreneurial spirits and reduce the deficit. It’s one possible outcome I suppose. (Earlier Ken Rogoff suggested that the Federal tax take needs to go up by a massive 25% to put a dent in the deficit.)

A panel session with Adam Posen of the UK’s MPC, and Former Fed Governor Larry Meyer asked whether Central Banks’ independence is under threat from concepts like Quantitative Easing (buying government bonds as part of the monetary policy, but also incidently (?) keeping yields down at times of budgetary pressure – not unlike the trigger for the Weimar Germany inflation experience), and some increasing commentary about Central Bank inflation targets being too low (including from the IMF’s research director Olivier Blanchard who thinks that 4% would be more like it). Posen believed that as long as a government is unable to fire the Central Bank Governor, and that the Bank is not made to buy government bonds in the primary market then independence is safe (although I didn’t get why there should be a difference between the primary market and secondary market). Most importantly, independence is not about legislation, but about a “buy in” from society – for example, the Bank of England was able to be made independent in 1997 because it had gained anti-inflation credibility in the preceding years, rather than prices subsequently falling because it was made independent. Meyer did, however, worry that the US Federal Reserve was more vulnerable to political interference than in the past – there was currently extraordinary hostility to the Fed from Congress as the result of the Fed’s bailout of the banking sector, and its new lending powers. Further more as fiscal deficits become unsustainable, could the Fed really hike rates in a world where the US needs to rollover half its debt every three years without triggering a downgrade or default?

Now for a word on the inflation measures that we use. I’ve lost track of the times that people have told me that the RPI, CPI or some other measure systematically under-report inflation – or that these measures are useless for pensioners, who don’t buy iPads, Blue Ray discs and SuperDry T-Shirts (sub-editors – please check that these things exist). Dean Maki (Barclays Chief US economist) and John Greenlees of the US Bureau of Labor Statistics put paid to a few of these inflation myths, and in particular pointed to the famous Boskin Commission Report of 1996 which concluded that in fact the US CPI measure was actually overstating inflation by something like 1.1% to 1.3%. The reasons why inflation measures tend to overstate actual inflation include substitution bias (the basket of goods doesn’t change to reflect the fact that if the price of something rises, consumers will switch to a cheaper alternative), outlet substitution (not capturing the lower prices charged by a new Aldi store in the data for example), quality change (more reliable goods with higher specifications) and new product bias (price deflation is often seen in new technology for example, but it may take a while for that new technology to enter the inflation basket). Another big complaint people have about CPI measures is the treatment of housing, and especially the US concept of Owners’ Equivalent Rent (OER), which is supposed to reflect the implicit costs of owner occupancy (“if someone were to rent your home today, how much do you think it would rent for monthly, unfurnished and without utilities?”). Recently OER has depressed inflation, causing critics to claim that this is somehow fiddling people with incomes linked to CPI. However, over the past 20 years or so, OER has actually boosted the CPI in most periods. The US does have an experimental measure of inflation supposed to better reflect the basket of goods for a pensioner (CPI-E), but it is only very marginally higher than the ordinary CPI. In fact there are no serious studies to show that western governments have suppressed the inflation measure to save money on inflation linked outlays (Argentina is a very different story however!) – the widely used inflation measures usually overstate inflation, which means both that inflation-linked bonds are good hedges for experienced inflation, and that there is a bias towards pensioners and other recipients of inflation-linked incomes being overcompensated.

If the CPI measure is so robust why does the Federal Reserve like to use the PCE deflator (personal consumption expenditures price index) as its preferred measure of inflation? Firstly it is chain-weighted, so it’s more flexible in changing its composition weights to reflect cost-conscious goods substitutions, and secondly, unlike the CPI measure the PCE deflator can be revised historically along with the GDP numbers as fuller data is received. Because the CPI is used to calculate things like bond coupon payments, once released it never changes. The real cynic would additionally say that it is because the PCE deflator is usually lower than the CPI!

Finally, a senior sovereign analyst from one of the major ratings agencies was asked whether there has been any pressure on him from AAA sovereign issuers imploring him to leave their ratings unchanged. The terse reply was “There has been absolutely no pressure from the US or UK authorities”. I wonder who has been calling?

I went to the excellent Barclays Inflation Conference a couple of weeks ago – although titled “inflation”, a lot of the conference’s content concerned the growing fears about the solvency of western governments. In particular, whilst the US Treasury market is currently seeing a massive flight-to-quality bid (10 year yields are now down below 3%) I came away worrying that it’s difficult to see that the US has any plan to avoid medium term bankruptcy other than some hopeful reliance on the American Dream to magic it all better.

Ken Rogoff (Professor of Economics at Harvard, and co-author of This Time Is Different) accused the US Treasury of “playing the yield curve”. With yield curves still extremely steep by historical standards, the authorities have skewed issuance to short maturities with the lowest interest rates (even though long dated maturity bonds would have historically low coupons despite the steep yield curve). Around half of all US debt will mature in the next three years – a tactic which keeps the US’s interest payment burden down in the short term, but which is a “classic way” of triggering a financial crisis when rates start to rise. This is the shortest debt maturity profile for the US since the 1960s. A huge burden of debt refinancing, coupled with higher interest payments was the trigger for Greece’s recent debt crisis. It’s another reason why we disagreed with Bill Gross’s “nitroglycerin” comments regarding the UK – the average maturity of the gilt market is around 14 years, compared with under 5 years for the US and 6 and 7 years for Germany and France. A “buyers’ strike” should be a little less problematic for the UK than it would be for the other nations.

Rogoff also talked about the prospects for financial repression as a method for governments to create a buyer for their debt when the natural, economically motivated, buyer has disappeared. Financial repression is the process of making people own assets they don’t want to hold – and the financial regulator is the important driver of this. In particular banks are encouraged (or forced) to hold more of their assets in less risky assets – i.e. government bonds – but also pension funds and individuals might find themselves being nudged into government bonds (in Japan individuals have most of their savings in the Japanese Post Office, which invests those savings in JGBs). Once domestic buyers are handcuffed, it becomes much easier to use inflation as a tool to reduce the real debt burden, especially in an economy like the US which has been steadily reducing the amount of inflation-linked debt it has outstanding as a percentage of the overall debt mix (although see comments below about the other inflation-linked government liabilities which stop inflation being the magic bullet policy tool).

Finally Rogoff said he’d be astounded if many Eastern European governments (and Greece) did not default, even with the IMF helping them. He pointed out that an IMF rescue package doesn’t always mean an economy is saved; in fact in 1/3rd of the IMF programmes since the 1970s default has ensued (including Argentina, Indonesia, the Dominican Republic and Turkey).

If you were nervous about the US keeping it’s creditworthiness after Ken Rogoff, a speech by Ajay Rajadhyaksha (Barclays Capital’s Head of US Fixed Income) piled on the anxiety. First the good news – the role of the US dollar as the primary reserve currency allows it to run excessive deficits far in excess of its economic rivals. Barclays have modelled the US’s AAA credit rating with an overlay based on the percentage of the world’s reserves kept in US dollars. On a stand alone basis, the US should have a AA credit rating, like Spain – but currently the US$ makes up 60% of global currency reserves, and this would allow them to run a 200% Debt/GDP ratio without losing their AAA rating, compared with the estimated 90% Debt/GDP level now. If the US$ became a bigger portion of global reserves (65%) then a 250% Debt/GDP ratio could be sustainable. Under current projections, only a fall in the dollar’s share of reserves to 50% would trigger the downgrade to AA. Even with continued diversification away from the dollar by foreign investors, this looks a long way off. However, once it happens the acceleration is severe – when Japan lost its AAA rating the yen fell significantly as a percentage of foreign portfolios, perhaps helping to trigger Japan’s further ratings downgrades.

That was pretty much it for the good news. Even at current low levels of interest rates, the US’s debt servicing costs take a step upwards in coming years, as the Debt/GDP ratio rises to 95% by 2020. If yields were to rise by 2% across the yield curve the percentage of US government revenues spent on debt service would rise from a troubling 17% now to around 33%! And inflating away that debt burden doesn’t work very well, as so much of the government’s outlays are indexed to inflation (although I guess you can always do what George Osborne did in last week’s UK Budget and change the inflation measure used to index benefits to one that is structurally lower, CPI rather than RPI). Radadhyaksha was also nervous about the US government’s contingent liabilities – losses on mortgages held by the GSEs (e.g. Freddie and Fannie) could be in the realms of $300 bn+. But the biggest contingent liabilities are the entitlements due to the US populations – and predominantly Medicare costs. After 2020, for every $2 trillion of taxes raised, spending will be $3.5 trillion. How do you close that gap without triggering a popular revolt, especially in an economy where median household incomes are only at the same level that they were back in 1998/99? Senator Judd Gregg, who some expect will run for the Republican Vice Presidential nomination next time round and sits on the Senate Budget Committee, suggested that the answer was to slash entitlements and cut taxes – this combination will encourage entrepreneurial spirits and reduce the deficit. It’s one possible outcome I suppose. (Earlier Ken Rogoff suggested that the Federal tax take needs to go up by a massive 25% to put a dent in the deficit.)

A panel session with Adam Posen of the UK’s MPC, and Former Fed Governor Larry Meyer asked whether Central Banks’ independence is under threat from concepts like Quantitative Easing (buying government bonds as part of the monetary policy, but also incidently (?) keeping yields down at times of budgetary pressure – not unlike the trigger for the Weimar Germany inflation experience), and some increasing commentary about Central Bank inflation targets being too low (including from the IMF’s research director Olivier Blanchard who thinks that 4% would be more like it). Posen believed that as long as a government is unable to fire the Central Bank Governor, and that the Bank is not made to buy government bonds in the primary market then independence is safe (although I didn’t get why there should be a difference between the primary market and secondary market). Most importantly, independence is not about legislation, but about a “buy in” from society – for example, the Bank of England was able to be made independent in 1997 because it had gained anti-inflation credibility in the preceding years, rather than prices subsequently falling because it was made independent. Meyer did, however, worry that the US Federal Reserve was more vulnerable to political interference than in the past – there was currently extraordinary hostility to the Fed from Congress as the result of the Fed’s bailout of the banking sector, and its new lending powers. Further more as fiscal deficits become unsustainable, could the Fed really hike rates in a world where the US needs to rollover half its debt every three years without triggering a downgrade or default?

Now for a word on the inflation measures that we use. I’ve lost track of the times that people have told me that the RPI, CPI or some other measure systematically under-report inflation – or that these measures are useless for pensioners, who don’t buy iPads, Blue Ray discs and SuperDry T-Shirts (sub-editors – please check that these things exist). Dean Maki (Barclays Chief US economist) and John Greenlees of the US Bureau of Labor Statistics put paid to a few of these inflation myths, and in particular pointed to the famous Boskin Commission Report of 1996 which concluded that in fact the US CPI measure was actually overstating inflation by something like 1.1% to 1.3%. The reasons why inflation measures tend to overstate actual inflation include substitution bias (the basket of goods doesn’t change to reflect the fact that if the price of something rises, consumers will switch to a cheaper alternative), outlet substitution (not capturing the lower prices charged by a new Aldi store in the data for example), quality change (more reliable goods with higher specifications) and new product bias (price deflation is often seen in new technology for example, but it may take a while for that new technology to enter the inflation basket). Another big complaint people have about CPI measures is the treatment of housing, and especially the US concept of Owners’ Equivalent Rent (OER), which is supposed to reflect the implicit costs of owner occupancy (“if someone were to rent your home today, how much do you think it would rent for monthly, unfurnished and without utilities?”). Recently OER has depressed inflation, causing critics to claim that this is somehow fiddling people with incomes linked to CPI. However, over the past 20 years or so, OER has actually boosted the CPI in most periods. The US does have an experimental measure of inflation supposed to better reflect the basket of goods for a pensioner (CPI-E), but it is only very marginally higher than the ordinary CPI. In fact there are no serious studies to show that western governments have suppressed the inflation measure to save money on inflation linked outlays (Argentina is a very different story however!) – the widely used inflation measures usually overstate inflation, which means both that inflation-linked bonds are good hedges for experienced inflation, and that there is a bias towards pensioners and other recipients of inflation-linked incomes being overcompensated.

If the CPI measure is so robust why does the Federal Reserve like to use the PCE deflator (personal consumption expenditures price index) as its preferred measure of inflation? Firstly it is chain-weighted, so it’s more flexible in changing its composition weights to reflect cost-conscious goods substitutions, and secondly, unlike the CPI measure the PCE deflator can be revised historically along with the GDP numbers as fuller data is received. Because the CPI is used to calculate things like bond coupon payments, once released it never changes. The real cynic would additionally say that it is because the PCE deflator is usually lower than the CPI!

Finally, a senior sovereign analyst from one of the major ratings agencies was asked whether there has been any pressure on him from AAA sovereign issuers imploring him to leave their ratings unchanged. The terse reply was “There has been absolutely no pressure from the US or UK authorities”. I wonder who has been calling?

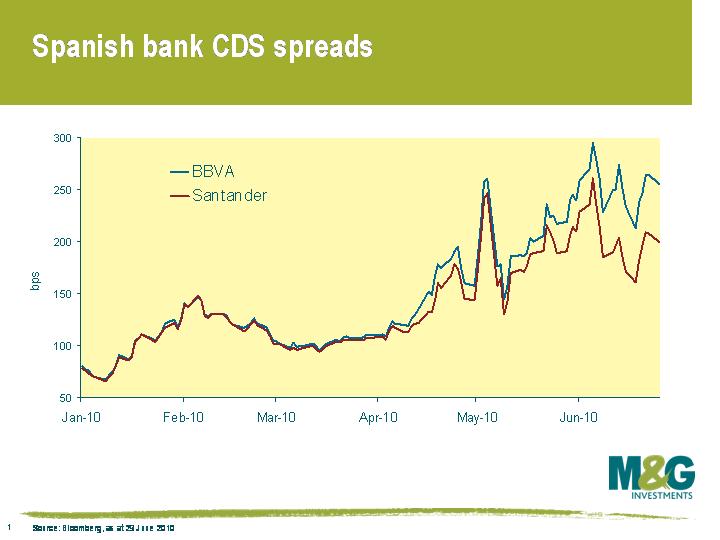

A report in the FT today highlights the lobbying of the ECB by Spanish banks to renew a one year funding facility known as the Long-Term Refinancing Operation (LTRO) that comes to an end this week. Banks borrowed €442bn from the ECB under the facility last year, at a time when borrowing in the market was either impossible or too expensive. When the facility closes, the banks that still need ECB funding will face two options – either roll into a 3 month facility, or into an even shorter 6 day facility. Banks worry that this shorter term facility will make their funding task more uncertain, and puts them subject to rollover risk when each facility matures.

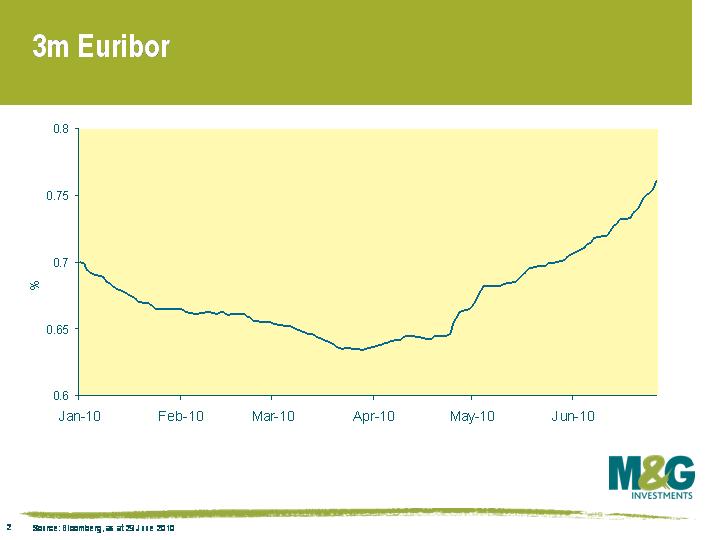

This highlights two issues. The first is the difficulty that Spanish banks (amongst others) are currently facing in accessing the capital markets (see first chart). It will be very interesting to see just how much of the €442bn gets rolled because it will give us an indication of the reliance of European banks on the lender of last resort – on the FT blog they show the market’s expectation of the roll, and the implications of this as an indicator of banking system health (the more that gets rolled, the more worried we need be). To what extent are banks able to fund themselves in the open market at all? This second chart shows that strains in the European interbank market have intensified in recent days, with 3 month money market rates up from around 0.65% at the start of May to 0.76% now.

The second and perhaps larger issue is the risk to the anaemic European recovery that the ECB is taking. I’ve been critical of the ECB in the past, such as when it raised rates in summer 2008, and its obsession over fighting inflation. Now it wants to withdraw term financing from the market when arguably it is most needed. Shouldn’t they be cutting rates? Where’s the European inflation risk?

Whilst President Obama warns of the dangers of tightening fiscal policy too early in the recovery, Europe (and the UK) is backing austerity. The austerity measures that are being implemented across Europe may act as a drag on growth for some time to come. Who knows which is the right approach, but the tightening of liquidity by the ECB seems to be premature and misplaced. The European banking system remains on life support. Whilst European banks can continue to access 3 month unlimited tenders, the message from the ECB is that it is uncomfortable being the lender of last resort and that inflation remains the enemy. Unless the market’s perception of the ECB changes I fear European banks will continue to struggle on their path to recapitalisation.

The ECB recently published a paper on its website detailing its preliminary proposals to reinforce economic governance in the euro area. The paper was split into three main sections. (1) Strengthening surveillance and greater prevention/correction of excessive deficits and debts. (2) Improving the surveillance framework and the correction of economic imbalances, and (3) a framework for crisis management in the euro area. It makes for interesting reading, and there are three main points to draw out in more depth.

Firstly, the most significant proposal is the creation of an independent fiscal surveillance agency. This will effectively be a government watchdog much like the UK’s recently created Office for Budget Responsibility. This body will be tasked with monitoring and assessing euro area countries’ fiscal policies. Once a country is deemed to have breached the ceiling of a debt to GDP ratio of 60% and/or has a deficit in excess of 3% they will be eligible to face an array of sanctions, ranging from purely financial penalties to loss of voting rights. Hopefully these penalties will be more strictly enforced than is currently the case. Remember, under the Maastricht treaty the EC already has powers to fine countries that break the stability pact (those running a deficit of more than 3%). Clearly a desire to create a larger eurozone dominated the perceived need for fiscal probity in the past, allowing countries like Greece to join the EMU that otherwise wouldn’t have met the requirements.

Secondly, the level and depth of monitoring will be directly proportional to the perceived risk of an individual countries fiscal policies. The idea behind this is that it will allow policy makers to focus on the areas that need attention while applying a lighter touch to those countries with sounder fiscal positions. All well and good, but what happens when more than a handful of countries experience difficulties simultaneously?

Finally, the ECB outline a crisis management body with control of a special purpose reserve fund. This will be used to bail out failing states (one already exists) either by offering direct loans or purchasing government bonds in the market (already been done). There is also talk of minimising moral hazard. This appears like a noble but futile exercise to me as the mere existence of central banks creates moral hazard – It’s what they do. Once a lender of last resort is introduced into an economy the behaviour of borrowers and lenders is influenced so as to create more risk in the economy than there otherwise would have been.

These preliminary proposals are wide-ranging and could potentially have a massive impact on European fiscal policy. One can see how the implementation of strict requirements and monitoring of fiscal policy could lead to European governments running extremely similar fiscal policies. There can not be too much of a disparity between taxes, borrowing and spending across countries if they all have the same targets for debt to GDP ratios and fiscal deficits in mind.

The idea that we won’t have an effective European monetary union without a political one is the prevailing view in the market. I agree. Fiscal policy by committee is probably not the ideal way to strengthen the Euro but perhaps it is the least controversial means of getting there.

There was some big news over the weekend, with the People’s Bank of China announcing that it was going to allow some flexibility in its exchange rate. The statement from the BoC points to the global economic recovery and domestic growth as the background to pursue further exchange rate flexibility. Markets have reacted positively to the announcement, with corporate bond indices opening up tighter this morning.

This signals the end of a de facto peg to the USD that started in mid-July 2008. From July 2005 to July 2008, the Chinese authorities very gradually allowed the Chinese renminbi (yuan) to appreciate by around 21% against the USD. Any appreciation of the yuan this time around is likely to be similar to the period between 2005-2008 i.e. modest and consistent. We should highlight that there is still some uncertainty around the timing, nature and potential scope of the new flexibility in the yuan at this early stage.

For us there are a number of main implications of this move worth highlighting.

Firstly, by keeping the yuan pegged to the dollar, Chinese exports are cheaper than they would be if the currency was allowed to float. There are many critics, particularly in the US, that believe China should be penalised for keeping its currency artificially weak. These penalties would likely take the form of trade protectionist measures. By allowing greater flexibility in its currency, the Chinese are reducing the likelihood that other countries start to introduce trade barriers in an effort to protect local industries. On this point, the timing of the announcement is interesting given there is a G-20 meeting this week.

Secondly, any move to see the yuan appreciate in value versus the USD is likely to be bearish for US treasuries at the margin resulting in higher yields. The exact nature of the impact on US treasuries is difficult to analyse. If the yuan appreciates in value then China will have less USD to invest into US treasuries, suggesting a weakening in demand. That said, given the appreciation in the yuan is likely to be measured it is unlikely that this is going to have a huge impact in the demand for US Treasuries in the short-term.

Thirdly, there will be upward pressure on global inflation rates if Chinese goods become more expensive due to the rising currency. Import prices for developed economies are likely to increase, suggesting higher producer and consumer prices. Analysing the allocation of items in the UK CPI basket for instance, we can see that many of the CPI divisions use Chinese goods as an input for the final product. This is similar for the inflation divisions in Europe and the US. Additionally, have a think about how many goods you own are manufactured in China. We can now see how a rise in the yuan can lead to higher costs for inputs which may lead to higher consumer prices. Given inflation is already above target in the UK this is something the Bank of England will have to keep a close eye on.

Fourthly, if the yuan appreciates versus other currencies, the purchasing power of Chinese businesses and households is going to improve. This could provide a boost to growth for countries that export goods to China and something that would be highly positive for global growth.

Ultimately, the announcement by the Chinese authorities is a positive step. A more flexible yuan will allow some correction of the imbalances that have developed in the global economy in recent decades. Given that China is such a large economy it is likely that the appreciation of the yuan will have many more impacts on global trade and finance than those listed above. We believe that any currency move will likely be gradual, thereby avoiding the large disruptions that a one-off revaluation would have on the global economic recovery. Watch this space.

Being the intellectuals that you are, we thought you might find some of the upcoming events being held at the London School of Economics (LSE) of interest. On the 30th of June they have Andrew Ross Sorkin discussing the development of the financial crisis since the publication of his book Too Big to Fail, and what he thinks the future may hold. We’ve mentioned his book numerous times on the blog – it’s very well written, engaging and thought provoking. On the 14th of July there is a talk from Alan Beattie (the Financial Times world trade editor) on why Greece should default (we here think some form of restructuring is inevitable by the way). The LSE runs these free lectures throughout the year on various topics in the social sciences and I’ve enjoyed the ones I’ve listened to previously. If you can’t make the actual events you can download podcasts a day or so later – they tend to keep me entertained while I’m ironing my shirts on a Sunday evening (Editor’s note – you iron your shirts? Who’d have known?). I’m not sure if it’s by design but neither of these talks clash with the World Cup. Sorkin’s lecture is on a rest day before the quarter finals and the final is on the 11th July. For those England fans among you some news just in: Robert Green trained on Thursday for 3 hours and had 400 shots taken at him without conceding a single goal. Today he and Heskey will train with the rest of the squad.

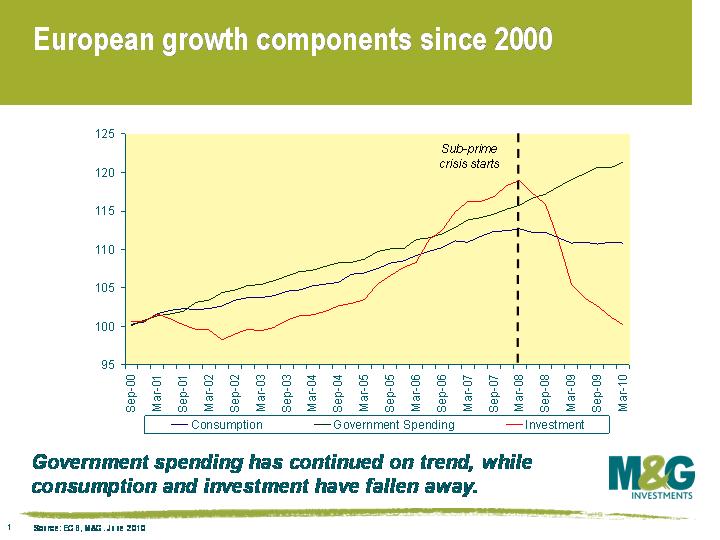

Much has been made of the fact that the European economy (since the creation of the European Economic and Monetary Union or EMU) has exited the worst recession in its existence. Many have pointed to the early actions of politicians and government officials as a reason Europe avoided a depression-like scenario. You might not know it or be able to feel it, but Europe is actually growing again. We will see that this growth has been led by government spending and a build up in inventories. With bond markets now demanding fiscal cuts and austerity measures, this type of growth will not be able to continue much longer.

To understand why this is the case, we need to understand how the bean-counters calculate GDP. For those of you that are unfamiliar with the inner working of calculating the GDP of an economy, I’d like to introduce you to the expenditure approach of calculating GDP. This approach tells us that:

GDP = private consumption + gross investment + government spending + (exports minus imports)

Looking at the chart, we can see the growth in real terms of the main components of European GDP since 2000. This data confirms many of the trends that we have been highlighting on this blog. Investment has fallen off a cliff because banks have had to replenish the amount of capital on their balance sheets. As a result, banks have reduced their lending to businesses. Governments – forced to step in to secure the economic recovery – have continued to borrow from capital markets and spend. Whilst the European economy is out of recession, it is a recovery led by inventory stockpiling and government spending. This is not yet a sustainable recovery.

The health of the household sector or the ‘private consumption’ component of GDP is crucial to generating any sort of self-sustaining economic recovery. And at this stage it appears to us that growth in the household sector will be positive but remain below trend. This is important because in Europe, the household sector is about 60% of the economy, meaning it is almost 3 times larger than the government or investment components of GDP. The European economy needs consumers to start spending again and governments need a strong household sector so they can start raising more tax revenue. In order to generate solid growth we need to see the labour market start to improve. Of course consumers can draw on savings that they have built up through investments and pensions but the events of recent years have left many feeling poorer.

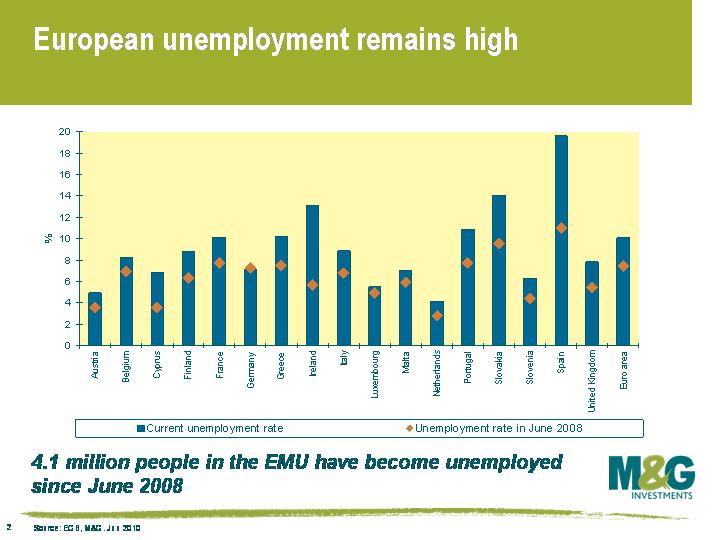

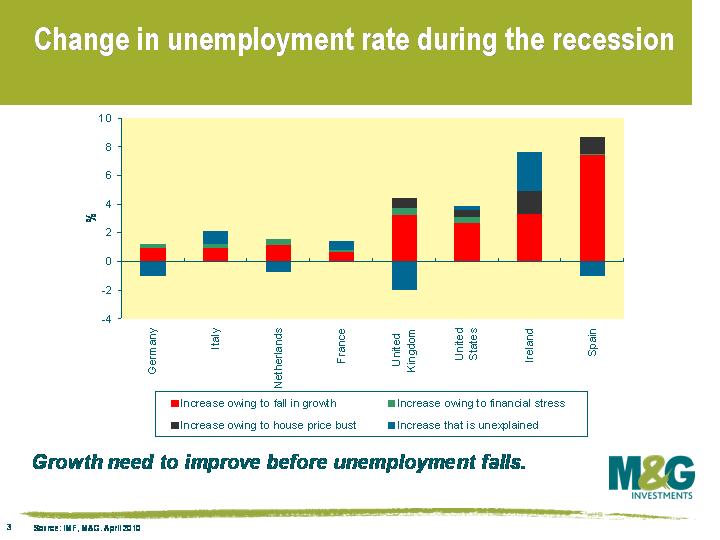

Turning to the labour market, the chart shows the deterioration in official European unemployment rates since June 2008. The unemployment rate has risen from 7.4% to 10.0%. This equates to an extra 4.1 million people out of work (equivalent to the population of Ireland). In Europe, almost 16 million people are now out of work. If we include those who would like to work more (the underemployed) these numbers are much higher. A quick analysis of why unemployment has risen might help us determine when we can reasonably assume to see labour markets improve again.

Fortunately for us, the IMF recently analysed labour markets in great depth in its World Economic Outlook. The IMF chart decomposes the change in the unemployment rate during the recession and explains why the unemployment rate has risen. We can see that the rise in unemployment rates globally can largely be explained by the fall in growth. House price busts and the financial crisis have also had a large impact on unemployment rates. These impacts have been higher in countries like Spain and Ireland that had an overheated housing market leading into the crisis – the result of easy credit and lending standards for mortgages. These bad loans are not only coming back to bite the banks, but also the countries in which these banks operate in. By nationalising these bad debts, governments have put their own finances in peril, resulting in skyrocketing debt/GDP ratios and the sovereign crisis we have seen this year.

We know that the main driver of the unemployment rate is economic growth. Thus, given the main driver of growth is consumption, we are likely to see persistently high European unemployment rates over the next couple of years. In an environment such as this, the ECB has been right to reduce interest rates to historic lows. European governments have been right to expand fiscal policy. The IMF conclude that “in countries where unemployment rates remain high and the economy is operating below potential, policy stimulus remains warranted”. But with markets demanding that governments implement harsh austerity measures and budget cuts in coming years, expansionary fiscal policy will no longer be accepted. It looks like Europe is going to have to get used to a period of high unemployment, sub-trend consumption and weak economic growth.

Now that the new UK government is bedding in and getting ready to unleash austerity upon us, I thought I’d quickly look back at the last Labour government and tell you something that you won’t want to hear: the last Chancellor Alistair Darling did a very good job.

There were three significant tests given to him during his 3 year Chancellorship. Of those, I think that two were passed with flying colours, and on the final test we’ll probably never know whether he was right or wrong. The first test was the run on Northern Rock in September 2007. This was the UK’s first bank run in 150 years (since Overend Gurney crashed in the 1860s causing 300 companies to fail) – and at the time both the Bank of England, obsessed with the concept of moral hazard, and the Conservative party, would have let the bank fail. It’s sobering to look back at how close we came to a full scale run on the UK’s banking system at that time – and perhaps how close we would have come to civil meltdown had the ATMs stopped working. Alistair Darling’s decision to support Northern Rock (and later the other major high street banks) was a game changer, and set a global precedent for the correct response to a run on a retail bank.

The second big game changer came a year later. US Treasury Secretary Hank Paulson was desperate to find a buyer for Lehman Brothers, the failing US investment bank. None of its US competitors would buy it without significant government support. In Andrew Sorkin’s brilliant account of those times, Too Big To Fail (a must read) he recounts how Barclays were on the brink of buying Lehman – before a phone call from Alistair Darling made it clear that that would not be allowed to happen. Andrew Sorkin claims that a furious Paulson said that “the British have grin-f*cked us” – and Lehman filed for bankruptcy by the end of the weekend. We’ll never know whether Barclays buying Lehman Brothers would have lead to its downfall, and systemic implications for the UK banking system – but we do know that Barclays was subsequently able to buy the best bits of Lehmans out of bankruptcy for a song, without exposure to the toxic parts of the business. If the US government was the seller, yet no US bank was a buyer despite having had unprecedented access to the Lehman books, it should have raised a lot of warning flags. Again, a big call, and one that turned out to be the right one.

The final test was the decision to maintain fiscal stimulus for the UK throughout 2010, despite the widening budget deficits. Thanks to the General Election result we’ll never know whether that would have been the right thing to do – certainly Keynesian economists like Paul Krugman are adamant that any contraction in government spending in the current fragile economic environment will be the trigger for a severe double-dip. David Cameron today announced “painful” cuts ahead that will affect “our whole way of life”. So the jury is out on this final big decision – Darling’s enemies will argue that the Labour government of which he was a key player was responsible for the exploding deficit in the first place. Whilst he didn’t become Chancellor until 2007 when things had started to go bad, the New Labour project did loosen fiscal policy when times were good (and befuddled current spending with “investment”) giving deficits nowhere to go but up when the economy turned. Much of this current deficit problem was baked in the cake thanks to our deteriorating demographics, or results from the correct decision to bail out the banks – but Labour’s pro-cyclical fiscal expansion must also take a share of the blame.

I wonder how we’ll judge George Osborne’s Chancellorship when it comes to an end? Whilst Nick Clegg has claimed there will be no return “to the savage cuts of the Thatcher years”, it’s interesting to note that apparently our “folk memory” of the Thatcher cuts is defective (according to a Stumbling and Mumbling blog post here). Apparently the Thatcher government only cut public spending in one year, and froze it in another. The blog’s author Chris Dillow suggests that the reason we all imagine there was a huge spending contraction in that Conservative government is because public spending grew at a slower rate than under the previous Labour government. It’s certainly interesting that the incoming Conservative government will be far more aggressive with the spending axe than Thatcher ever was – and perhaps Mervyn King’s reported comments about the incoming government being out of power for a generation as a result of the austerity that they would implement isn’t far from the truth. We’ll find out in 5 years’ time – if not sooner.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.