Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

Over the weekend Ardagh Glass announced a transformative acquisition of another well known packaging name in Impress Cooperative U.A. The deal left me with mixed emotions and came as something of a surprise because an IPO had been considered the most likely exit for sponsor Doughty Hanson.

The purchase of Impress sees the departure of a European high yield market stalwart. The company’s inaugural transaction back in May 1997 saw it raise DEM 200m paying a coupon of 9.875%. That was followed by a further €150m raised in 2003, paying a coupon of 10.5% until both bonds were called by the company in July 2006, the former at face value, the latter at a small premium, netting investors annual returns of 10%, give or take. Those obligations were replaced with the current debt stock, set to be retired again either at face value or a premium depending on the exact bond in question.

The sale to Ardagh Glass raises a couple of interesting points:

Firstly the IPO exit that never materialised. The ongoing volatility in equity markets, the scarcity of capital and the level of suspicion levelled at private equity from the public markets has resulted in fewer IPOs in recent times than many had imagined. Without a significant change in any of these conditions, the much touted IPO exit will give way to tertiary and secondary LBOs, likely accompanied by lower multiples and weaker IRRs.

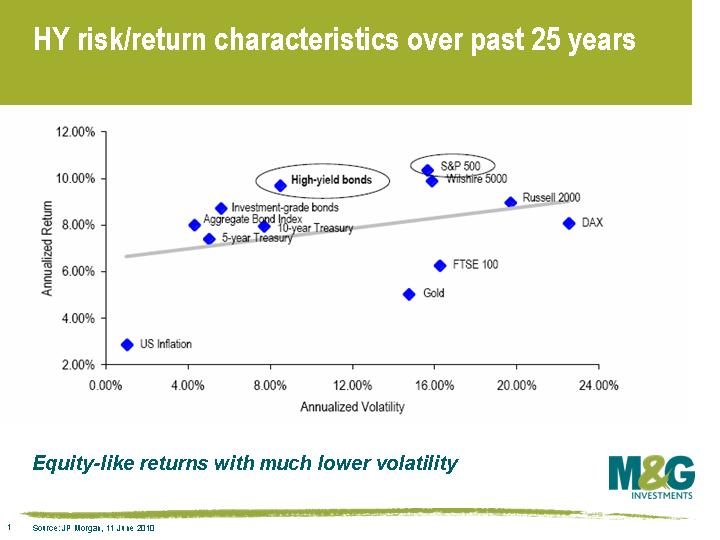

Secondly, the Impress story clearly demonstrates the attraction of high yield as an asset class. While it’s obviously disappointing to lose a conservatively run business (it’s all relative), with defensive and stable cash flows historically paying around 10% annually for its unsecured debt, it does highlight the importance of income and its ability to smooth volatility. In fact, comparing the US high yield market and the S&P 500, the two markets have realised similar annual returns over the past 25 years, yet the high yield market has done so with nearly half the volatility.

It is the time of year when the geese begin their long flight south to avoid the hellish northern European climate. In markets we are always on the look out for flocking and herd mentality. Sometimes as an investor you want to run with the herd and sometimes you want to observe the herd mentality from afar.

And it’s not just the geese who are looking for a change of scenery. Over the last few weeks some of the biggest names at British banks have announced they will be standing aside. John Varley (CEO of Barclays), Stephen Green (Chairman of HSBC) and Eric Daniels (CEO of Lloyds) have all decided to fly the coop. This has got me thinking; do these gaggle of astute top bankers, like the geese, know some inclement weather is on the way and are getting out while the going is still relatively good?

Hybrid bond issuance has started to grab headlines again. The last month has seen a few companies start to issue the centaurs of the bond world again. But are they a good investment?

We wrote about hybrid bonds back in April, suggesting that they could potentially be a good source of alpha if investors do their homework. Hybrid securities have features of both equities and bonds, and like equity they don’t mature (although some do have call features) but pay a coupon like a bond. The legal language, bond covenants, incentives for the company to call the hybrid and rights of the bondholder in the event of a default can differ considerably from issue to issue.

Hybrid bonds are treated as debt for tax purposes, and depending on the individual structure can be treated as equity by credit rating agencies. Because the rating agencies give credit to hybrid deals for their equity features, they do not put downward pressure on a company’s credit rating like all-debt deals can. Ratings agencies like them because should a company get into financial difficulty, it could choose to simply not call the debt or stop paying coupons to hybrid bondholders. This is attractive for the issuer but if the coupon gets deferred what investor would want to hold a zero coupon bond in perpetuity?

On Monday RWE – a German utility – issued a hybrid bond at B+322bps which is a yield of 4.7%. 5yr CDS for RWE (a rough proxy for what it would cost them to issue senior 5yr paper) was trading around the 65bps mark. Not a bad yield pick-up for an investor, and the credit rating companies are happy as well. This brings us onto the potential upside for the bond investor. If you pick the right company and the right hybrid bond, you may be rewarded with an attractive yield relative to senior bonds that have been issued by the company.

But perhaps hybrids aren’t quite the panacea they are made out to be. Are investors better off simply investing in a company’s equity and participating in potentially unlimited upside from the share price going up?

Traditionally it has been financial firms at the forefront of issuing hybrid bonds, but the uncertainty of the regulatory outlook at present has all but halted issuance from this part of the capital structure. On September 12th the Basel Committee announced that any newly issued hybrids will not receive any capital credit from financial regulators. As some of you may be aware, a rally in tier 1 and tier 2 securities has followed – the overriding sentiment in the market was that banks would start calling these instruments at the earliest possible opportunity.

So the centaurs are coming back – but be careful which horse you choose to ride as you may get bucked off.

Yesterday I attended a presentation by Greek officials and delegates from the IMF and EU as part of the London leg of a two day European trip. Considering this was a two day roadshow designed to reassure investors and rebuild confidence in Greece, and the speakers were Greeks and the guys who’ve lent them lots of money (and are likely to lend lots more), it was never going to be anything other than positive. Nevertheless, there were some useful and interesting snippets.

Greek finance minister Giorgos Papakonstantinou spoke at length on the ‘political economy’, focusing particularly on the misperception about Greece in the media. News reports of civil strife and TV images of burning trash cans on the streets are a wild exaggeration of reality. Obviously there have been issues, but last weekend’s major protests in the city of Thessaloniki (Greece’s second largest), which were designed to clash with a keynote economic speech by Prime Minister George Papandreou, saw only 20,000 protestors. Papakonstantinou couldn’t resist having a pop at ‘a central European country’ (France) that saw well over a million people protest against government plans to raise the retirement age from 60 to 62 – a change that pales in comparison to reform that the Greek government has implemented already this year. There is still significant political will behind the Greek government despite the austerity measures, as evidenced by the healthy lead in the polls.

In terms of fiscal consolidation, results have so far been impressive, prompting the IMF and EU to release a 2nd tranche (€9bn) of the €110bn total loan package which Greece received a few days ago. The budget deficit is on track to be cut from 13.6% to 8% by the end of year 1, with the deficit reaching 3% by year 3 of the package. Public sector wages have been cut 15%, pensions by 10% and operating expenses by 50%. Central government expenditure cuts have been successful, although control of local government finances has continued to be difficult (see here for a detailed IMF review of Greece’s progress).

Now the problems. The biggest issue for Greece has been implementing reform on the revenue side. Tax evasion is totally socially acceptable. This issue is being addressed (eg a tax bill was passed in April, which included the introduction of a presumptive taxation system) however tax revenues have underperformed the IMF’s expectations.

Longer term, as Giorgos Papakonstantinou explained, the key challenge for Greece is to improve the country’s competitiveness and hence its long term economic growth potential. Policies put forward include improving productivity of health and education, focusing on technologies such as green energy, and reform (reduction) of the large shadow economy. These are considerable challenges, but the depth of the problems also give rise to significant growth opportunities.

The overriding message was that it is not in anybody’s interest for Greece to restructure its debt, since this wouldn’t solve the main problems which are a lack of growth and a lack of competitiveness. Greek banks are in difficulties, but that’s not due to exposure to toxic assets or over-leverage, instead the problems stem from the weakness of the sovereign. So in Greece, perhaps in contrast to many other countries in the past few years, sovereign issues have brought down the banks rather than the other way around. A debt restructuring would cause huge problems for Greek banks, and would rapidly become an issue for countries and banking systems outside of Greece.

Two further observations. Firstly, I was bemused by the initial reaction to the good but fairly obvious first question from the audience regarding what would happen at the end of the three year rescue package (when the Greek public debt/GDP ratio is expected to peak at over 140%). The IMF and EU delegates whispered animatedly for a good 20 seconds (had they not considered the answer to this rather important question previously?!) before finally answering the question by suggesting that if Greece stuck to its targets and progressed as hoped then this could be extended.

Secondly, I was impressed by Giorgos Papakonstantinou – clearly you don’t get to become a finance minister of a country such as Greece without being smart, but the media portrayal of Greek government officials as being a bunch of wallies is far from the truth. You need only look at the biographies of Giorgos Papakonstantinou or Prime Minister George Papandreou to realise that Greece has among the smartest, most capable people of any government in the world at its helm. But brains may not be enough. Even ignoring the short and medium term implementation risks (not to mention global economic risks), the only escape for Greece is to return to strong, sustained growth in the long term. That may not be possible with such high debt levels and associated high interest costs. Sure, Greek banks are able to refinance with the ECB, which means that Greece has a big advantage relative to emerging market countries that have historically experienced sovereign debt crises. With the help of the IMF and EU, Greece’s life support system can therefore last for a very long time, and arguably for longer than the bond market is currently pricing in (we’ve recently started nibbling at Greek debt). But if the patient is terminally ill then there is little you can do.

The global investment community is having a collective head scratch about why sovereign bond yields are so low. As I argued here, if you take the rule of thumb that nominal government bond yields are roughly equal to expectations of the real growth rate plus the inflation rate (i.e. nominal growth), then developed sovereign bond yields of sub 3% are suggesting that we’re turning Japanese.

But maybe the conventional wisdom that bond markets are pricing in something never seen before outside Japan is wrong. Maybe, in actual fact, we’ve been gradually ‘turning Japanese’ for quite a while, but bond markets have been very slow to notice.

Rather than thinking about the 10 year government bond yield as representing expectations of the nominal growth rate, consider that the ten year Treasury yield should be broadly equal to expectations of the average fed funds rate over the next decade.

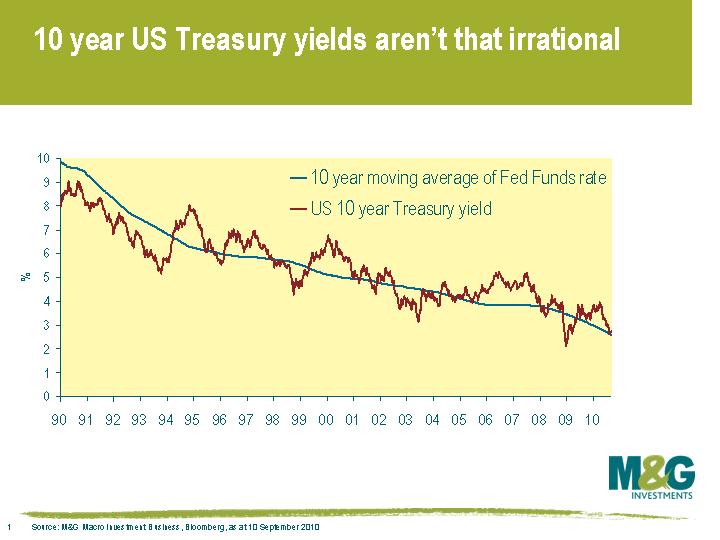

The macro hedge fund team here at M&G uses this concept to get a feel for what’s priced into government bond markets, and look at (among other things) the rolling 10 year average of the Fed funds rate against the current ten year US Treasury yield (see chart). So, when the 10 year Treasury yield is above the 10 year rolling average of the Fed funds rate, then markets are anticipating a higher interest rate environment over the next decade (and presumably therefore are pricing in a higher nominal growth rate over the next decade too). Conversely, if the 10 year Treasury yield is below the Fed funds rate seen over the past decade, then the market is pricing in a lower bank rate environment than that seen in the past decade.

There are two interesting conclusions from this chart. The first is that it seems that the market’s best collective guess of where the Fed funds rate is going to be over the next decade (i.e. the 10 year Treasury yield) is simply to look at where it’s been over the last decade and assume a repeat. The market tends to be slow to react to ‘regime change’, which in the past couple of decades was namely globalisation, and with it, greater competition, lower prices, and the reduced bargaining power of workers in developed countries.

The second interesting conclusion is that the 10 year Treasury yield today is almost exactly in line with the average Fed funds rate of the last decade. So it doesn’t appear that the bond market is pricing in a ‘new normal’ at all, it is simply pricing in a repeat of the experience of the past decade. Given that the 10 year Treasury yield is at 2.8% today, which is where the Fed funds rate has been for the last decade, you should be very bullish on the direction of US government bond prices if you believe that the US is about to enter a ‘new normal’.

It’s that time of year once again – school holidays are over and the children are going back to work. This feels very much the same in the grown up (?) world of investment. This year’s questions and tests look as though they are going to be trickier than usual. After all, the financial headmaster Ben Bernanke has just warned that conditions are unusually uncertain.

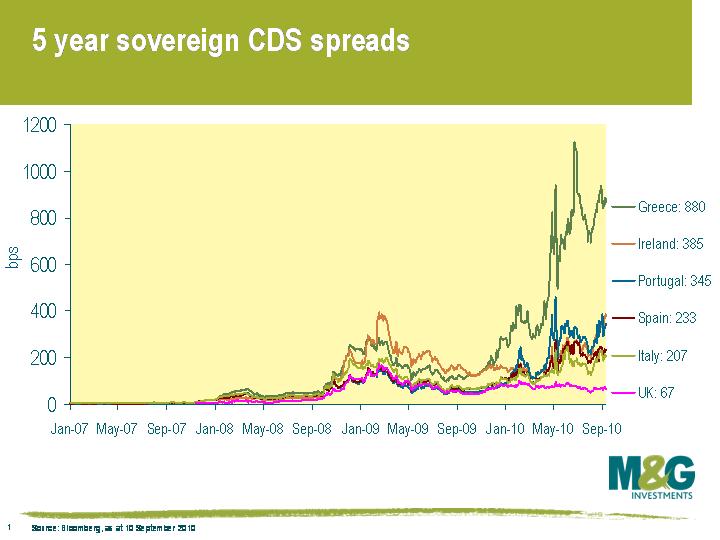

The move from the summer lull to the rigours of testing examination is no more acute than the pressure that has been reapplied to sovereign credits in Europe. The European authorities have generally responded to these challenges by a series of increasingly significant policy measures, but this chart shows they have still not solved the problem. Let’s go back to the economics class and study why their unprecedented actions have failed to soothe the markets.

When I first started studying economics as a 13 year old I didn’t have a professor Ben Bernanke. I had a “professor” Cec Thompson. He was not a real professor, but had acquired the nickname when educating himself while playing professional rugby league, where he reached the heights of playing internationally for Great Britain. Unlike Doctor Greenspan, his autobiography is a very good read. The first economic lesson I can remember that he gave was based on the price discovery and market clearing process in a simple economic example called the hog cycle. This introduced me to the concept of relative price change and market pricing, teaching us the principle of the invisible hand.

The current problems of the European periphery appear to centre on the concept of a single currency zone. By moving to a single currency 10 years ago, a simple and effective method of price discovery and market adjustments was removed from the labour and capital markets. Looking back this seems to have resulted in too much capital at too low a rate being deployed in the European tiger economies – boom and bust on a grand scale. How are we to solve this problem?

In order to make labour and capital markets efficient again, the simple option would be to reintroduce national currencies. The mechanism for doing this is non-existent, and their reintroduction and failure of the euro in this scenario is seen as worse than the current problems we face. The solution is to find a way to reintroduce national currencies, and the invisible hand, in the least damaging way possible. I have talked about this before at length, where the introduction of a new euro (the “Neuro”) would have to be done in a planned way and with a share of the shock born by savers and lenders. In the short term this would still be painful. But the long term alternative of an increasingly pressurised Eurozone, with the peripheral economies unable to adjust due to a lack of efficient market mechanisms, will turn out to be a chronic rather than a temporary problem in my opinion.

In a modern society, labour and capital should be allocated by a combination of governments and the free markets. Removing the efficient, invisible hand provided by national currencies and replacing it with political decision making as occurred with the euro was a big step. The result was political rather than economic responses to the stresses within the Eurozone, as typified by a Jean-Claude Trichet interview in today’s Financial Times, where he argues that in order to get markets to work we need to think about further strengthening the political framework.

Education is not only about doing things right, but learning from mistakes. Let’s hope that the experiment of the euro – which is just getting past its infancy – develops into a successful means of developing the economic fortunes of the Eurozone, and not a dysfunctional teenager in the years ahead.

Yesterday Jim blogged that M&G was launching two new innovative corporate bond funds – the M&G UK Inflation Linked Corporate Bond Fund and the M&G European Inflation Linked Corporate Bond Fund. For those that are interested in hearing further details about the funds straight from the horse’s mouth, click here for a short video interview Jim did yesterday with Charlie Parker from Citywire (video no longer available).

We’ve announced today that we are launching two corporate bond funds which aim to deliver returns ahead of inflation in the medium to long term. We believe that these are the world’s first inflation-linked corporate bond funds for retail investors. These funds will hopefully capture the systematic overcompensation for credit risk that you get from investing in corporate bonds, as well as the inflation-linking obtained in assets where the coupon and final principal repayment rise in line with retail prices.

Is this the right time to launch an inflation-linked bond fund? As we’ve said before, we remain more worried about disinflationary pressures than inflationary pressures – the still growing reserve army of the unemployed should keep a lid on wage growth for the foreseeable future, and manufacturing capacity is also still high. However, we know that many of our clients and blog readers disagree with us on this. We also worry that whilst in the short term price pressures remain subdued, longer term we might not fully understand the impact of the huge Quantitative Easing programmes in the western economies. To quote from the out of print Dying of Money: Lessons of the Great German and American Inflations, “each big inflation – whether the early 1920s in Germany, or the Korean and Vietnam wars in the US – starts with a passive expansion of the quantity of money. This sits inert for a surprisingly long time. Asset prices may go up, but the latent price inflation is disguised. The effect is much like lighter fuel on a camp fire before the match is struck”.

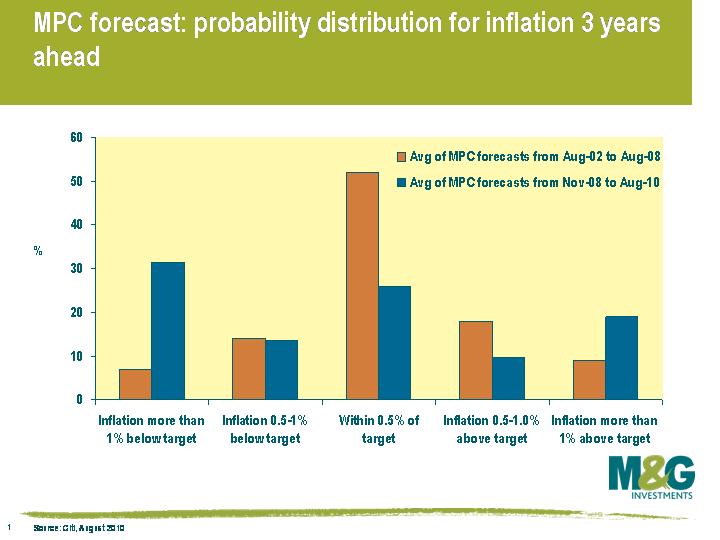

As we’ve said before, perhaps we’re Japan, and concerted action from the authorities can’t dislodge deflationary pressures from the economy, or perhaps we’re Zimbabwe and the turning on of the printing presses will bring about hyperinflation. Certainly the growth of such tail risks and the end of predictable inflation (and the end of faith in Central Banks to control inflation in either direction) makes investment decisions in any asset class much more difficult. This chart derived from the Bank of England’s Inflation Reports over the past 8 years shows that their expectations for inflation have moved from a normal distribution curve, with only a 15% chance of inflation being more than 1% above or below target 3 years into the future (taken from the Inflation Reports from 2002 to 2008), to a more than 50% chance of future inflation being more than 1% above or below target in the next 3 years in the most recent Inflation Report. This Abnormal Distribution Curve accords with our own view – we’d put more emphasis on the deflation risks, but we can’t ignore the inflation risks either.

So we don’t think you necessarily need these funds right now, but we’ve decided to build the fire engine before the fire breaks out, rather than waiting until it’s burning out of control. We’ll probably blog a bit more about the small (£11 billion in the UK) but interesting corporate inflation-linked bond market in due course.

It feels a little like the first half of 2008 again to me. People are asking who has it right? The bond market or the equity market? Government bond yields in the UK, US and Germany are the lowest they’ve been in recent history. Yields this low, the argument goes, imply that the bond market is expecting the dreaded double dip. The equity markets on the other hand – after a fairly positive earnings season – are trading back where they were in the mid 2000’s.

Posing this question as a simple disagreement between bond and equity investors is a touch disingenuous. Rather than being in opposition to one another maybe the two markets are actually singing the same song. One should bear in mind that – unlike Vegas – what happens in the credit markets doesn’t stay in the credit markets.

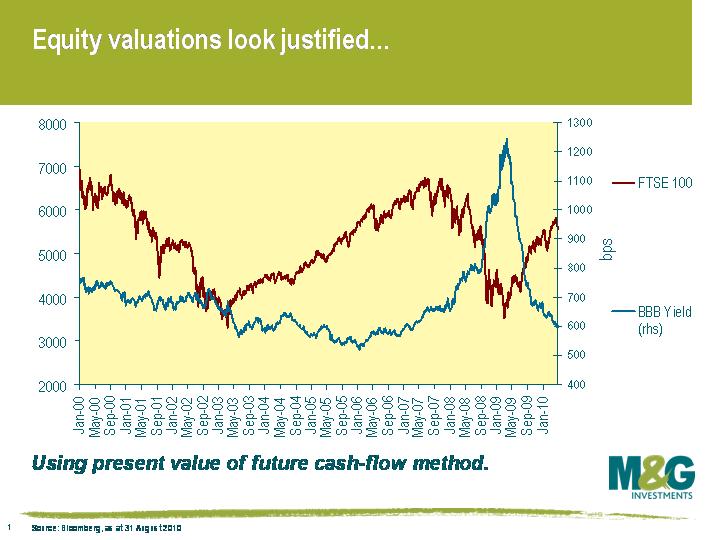

Rudimentary corporate finance theory will tell you that the optimal capital structure of a firm is one which contains an element of debt (due to the tax shield). In practice most firms do finance themselves with a combination of debt and equity. Therefore when valuing a company you should take into consideration the cost of both financing options.

There are many ways to value a firm but, if you use one of the variations on the present value of future dividend methods the cost of capital plays a huge role. Simply put, one discounts the future dividends by the cost of capital. The higher the cost of capital, the lower the value of the firm and vice versa. Here is a short worked example to show the impact of changes in the weighted average cost of capital (WACC). For simplicity I have assumed a growth rate of 0.5% and that firms in the FTSE raise their capital in equal proportions from equity and debt.

Basic Dividend Discount model;

V= D*1+g V: Equity value

WACC-g D: Dividend

g: Growth rate

We can then take the following data and plug it into the model:

| Mar-09 | Aug-10 | |

| BBB Yield (Cost of Debt) | 12% | 5.50% |

| FTSE 100 Forward looking Div Yield (Cost of Equity)* | 4.87% | 3.80% |

| FTSE 100 | 3926 | 5225 |

| Implied Dividend | 191 | 199 |

| Growth rate | 0.50% | 0.50% |

| Debt:Equity | 50:50 | 50:50 |

| WACC ([cost of debt+ cost of equity]/2) | 8.44% | 4.65% |

*Kindly provided by our friends at Evolution Securities

August 2010 – with current WACC

199*1.005 = 4,819

0.0465 – 0.005

August 2010 – with March 2009 WACC

199*1.005 = 2,519

0.0844 – 0.005

The values the model spits out are not that close to actual market levels but I think it demonstrates the sensitivity of these types of models to the cost of capital quite well.

I must admit I have no sense of the number of investors who actually take this approach to valuing equities, its pure text book theory. So let’s look at what has happened in practice. Back in 2008 when yields rose dramatically equity valuations began to drop, as you can see below. Today with yields on BBB’s (including financials) and equity prices back to where they were in the early part of the last decade one could argue valuations look somewhat justified.

Clearly these are absolute yields, they have been driven lower not by increased credit quality, but by near zero base rates and low growth/inflation assumptions. This has the effect of driving down yields on the govvies over which the corporates are benchmarked. Spreads on BBB’s are still in the 200bp region if you exclude financials, which is where they have been for a year or so now. It seems to me that we can’t necessarily take extremely low gilt yields as a sign pointing to an immediate dip in the equity market, they may actually be the reason for its buoyancy. Spreads are the real barometer of the credit markets not yields. As these haven’t changed much over the last year it’s hard to say the bond and equity markets are in opposition. It’s when credit investors disagree with equity holders that the real fun starts.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.