Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

The euro area unemployment rate rose to 10.1% today, a level not seen since July 1998. But does the market place too much emphasis on this number?

Of course it is always important to keep a close eye on unemployment rates. Strong consumer demand is less likely to be inflationary if the unemployment rate is well above the non-accelerating inflation rate of unemployment (NAIRU) rather than close to it.

However, because of the way the unemployment rate is calculated, countries like Ireland and Spain have made a disproportionate contribution to this deterioration in the unemployment rate relative to the size of their economies in the region over the past couple of years.

In order to calculate labour market statistics for the euro area, Eurostat simply sum the series of the member states. For example, the labour force is the total number of people employed and unemployed in an economy. The unemployment rate equals the amount of unemployed persons divided by the labour force.

This differs from how Eurostat calculate the Harmonised Index of Consumer Prices (HICP), which have an element of weighting involved in the calculations. For example, the country weight of Germany in the HICP is 26% whereas Ireland has a weighting of only 1.5%.

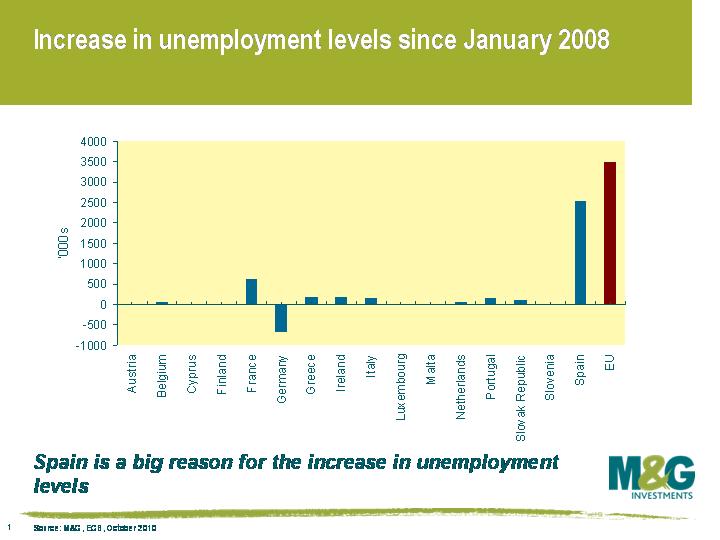

Since the beginning of 2008, the number of unemployed persons in Spain has risen by a massive 2.5 million people. Unemployment in the euro area has risen by 3.5 million people in total over this period. As a result, Spain represents 73% of the total increase in unemployment in the euro area. This is much larger than the size of the Spanish economy relative to the size of the European economy. Spain accounts for around 13% of the European economy on a purchasing power parity basis.

Doing a few back of the envelope calculations produces some surprising results. Excluding “peripheral” Europe, unemployment in Europe has risen by 416,000 people since 2008. This suggests an unemployment rate closer to 7% than 10%. Peripheral Europe accounts for almost 90% of the increase in the number of unemployed persons in the EU since the start of 2008. A very large impact given that as a percentage of EU GDP, the peripheral countries make up only around 20%.

Mervyn King has regularly referred to the great moderation as the NICE era: Non-Inflationary Consistently Expansionary period. Obviously, those days are well gone as we are over three years into the credit crunch, a vast array of stimulus measures have been applied, and their effects are waning (see mike’s blog). So, if we are no longer in the NICE era, where are we? Well, growth and inflation will be low and people will feel pretty poor for a considerable period of time. How do you describe a period where we could experience Deflation, Unemployment, and, No Growth? DUNG!

Richard has written over the last couple of weeks about how QE is turning the world topsy turvy with potentially the higher inflation economies experiencing the lowest bond yields, how central banks and their printing presses are killing the bond vigilantes, and how the currency vigilantes are rising up in the bond vigilantes’ place.

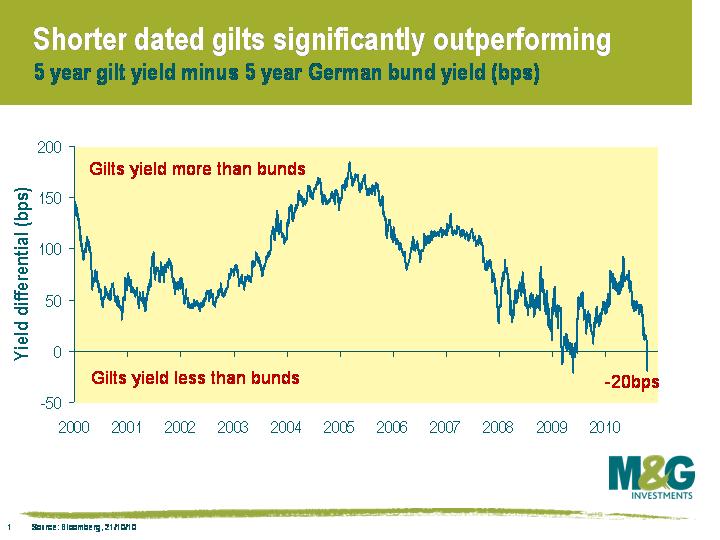

Well the currency vigilantes have certainly been pummelling the bond vigilantes today. As UK QE expectations grow on the back of a combination of very weak UK money supply data and a dovish speech from Mervyn King, five year gilt yields hit an all time record low yield of 1.44% this morning, which leaves them yielding 0.20% less than 5 year German bund yields (see chart). This is staggering if you consider that (a) Eurozone CPI is 1.8% vs UK CPI at 3.1% (and UK inflation is likely to remain elevated for another 15 months or so as VAT hikes work through the year on year numbers), and (b) German bunds have had a massive safe haven bid this year on the back of the European peripheral meltdown.

Meanwhile, on the currency front, so far today the British pound is down 0.6% against the US Dollar and 0.8% against the Euro. In fact, as the chart shows, sterling is the worst performing major currency in the world year to date, having fallen 2.5% against the US dollar. [Note that there’s still some distance to cover before sterling is the worst performing currency in the world YTD, though – you didn’t want to hold currencies such as the Venezuelan Bolivar (-50%), the Guinean Franc (-29%) or the Ethiopian Birr (-23%)].

Now that the new budget has been announced by George Osborne and spending review disseminated, the coalition is lauding its merits and the opposition is deflecting responsibility for the deficit and exposing flaws in the cuts. Today’s budget and public sector reforms will see billions cut from welfare spending, Whitehall budgets reduced, the retirement age raised, quangos culled and a permanent levy forced upon the banks. These austerity measures are taken with the intention of eliminating the structural deficit by 2015.

Many of these cuts implemented by the Chancellor were predicted / leaked and indeed austerity is believed to be the means to improving the UK’s balance sheet after quantitative easing and a decade of high spending. Although the political parties will debate exactly who was responsible for the deficit and what the correct action should be, the consensus opinion is that cuts were required and indeed were the only suitable remedy to the situation in which we find ourselves.

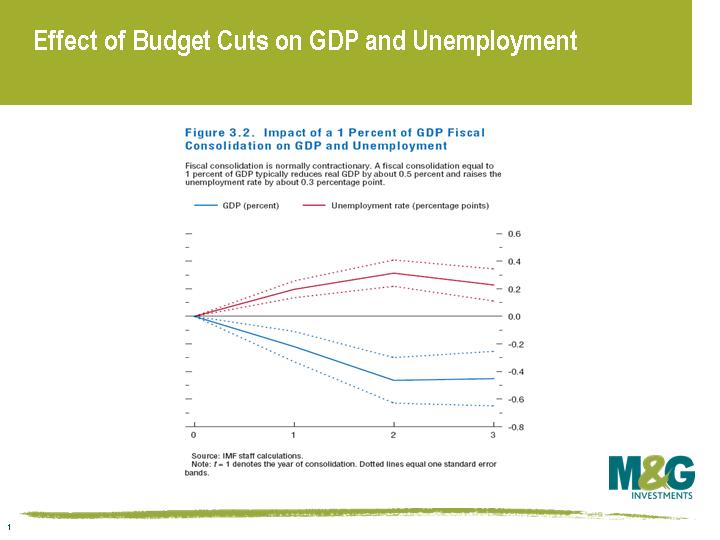

However a contrarian view is given by the IMF in their “World Economic Outlook” report they released this month. The data they have collated suggests that cuts do not necessarily lead to economic improvement, their data captured in this chart shows that a 1% fiscal cut in GDP typically reduces GDP by 0.5% and increases unemployment by 0.3% over 2 years. This would suggest the £81 billion (around 5.8% of GDP) of cuts announced today could lead to a 3% reduction in GDP and unemployment reaching 9% by 2012. It should be noted that the IMF’s empirical data does not take into account any potential for further monetary stimulus (QE) and its beneficial effects. It does, however, provide food for thought and suggests that although cuts may be in the interest of the UK’s long term balance sheet, they could have at least a short term negative impact on growth.

This is obviously going to mean that the UK economy is going to face a potentially dramatic onslaught of cutbacks reducing growth and increasing unemployment over the next year. George Osborne’s message is that this short term pain is essential for the long term health of the UK economy. We look forward to seeing if this medicine works. As Ozzy Osbourne once sang – See You On The Other Side.

Last week BBB rated Mexico issued a 100 year bond denominated in US dollars. It was originally supposed to be a $500m issue, but as is typical in any EM bond issue at the moment, the book soared to almost $3bn so the government decided to take advantage and make it a $1bn issue. It was issued at a price of 94.3, which meant it had a yield to maturity of 6.1%, or 2.35% more than a 30 year US Treasury. The bond’s price has since soared, and is now at a price of 101 (yield of 5.7%, excess yield over 30 year US Treasuries of 1.8%).

A ‘century bond’ is a good headline grabber, and most people’s instinct is to question why someone would want to lend money to a country whose credit rating is only 2 notches above junk status in the knowledge that you won’t get your principal back until long after almost everyone currently on the planet is dead. However, once you look at the bond maths, it’s not really all that incredible. The time value of money means that $100 in today’s money is only worth $0.3 in 100 years (assuming an interest rate of 6% that’s payable semiannually). In other words, 99.7% of the cash flows from this Mexico bond will come from interest, rather than the final principal. The bond will actually behave very much like the 2040 Mexican bond that’s been around since January 2008 – the 2040 bond has a duration of 14.8 years versus 18.1 years for the century bond, so there’s little difference in risk. (As a comparison, the UK 1.25% 2055 Index-linked gilt has a duration of 35.1 years)

So the existence of a 100 year senior bond isn’t a worry per se – indeed, it makes sense for a borrower to take advantage of low US Treasury yields and (at least in EM) historically tight credit spreads to lengthen out its maturity profile. Such behaviour reduces short term funding pressures, and ultimately improves credit quality. And the existence of a very long maturity bond is hardly new; if you consider all the subordinated financial perpetual bonds that were issued in the noughties, we’ve seen far worse.

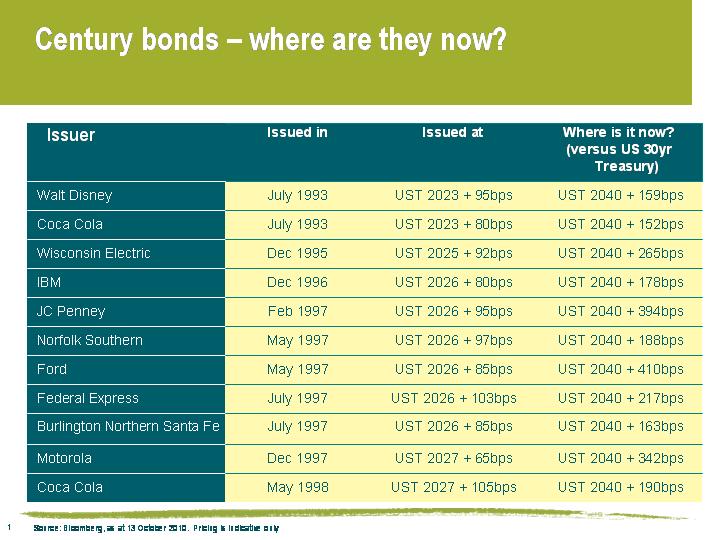

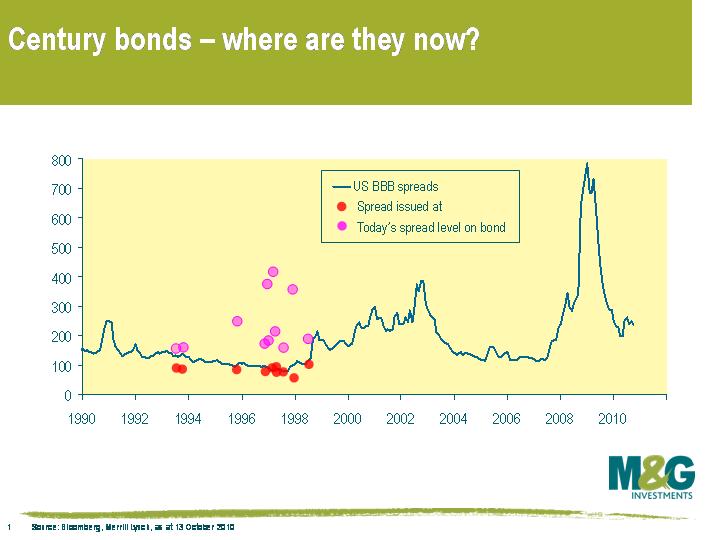

The worrying sign is simply that if a borrower thinks that it’s a fantastic idea to do something relatively unusual because it believes that the terms to do so are very attractive, then it’s unlikely to be such a great deal for the lender. This table shows what happened to the original century bonds that were issued by US corporates in the 1990s (see chart, and note that this is just a selection of the larger issues – century bond issuance peaked at 56 in 1996-97, with very few since)

This chart is another way of demonstrating that the surge in century bond issuance in 1996-97 occurred at a time when credit spreads reached exceptionally tight levels, and credit spreads in all companies I’ve listed above are now wider (in line with the broader market), with some substantially wider. The red circles are the spreads at the time of each of the issues, and the pink circles show where the spreads on these bonds are currently.

Prior to last week, China and the Philippines were the only EM sovereigns to have issued century bonds. I wouldn’t be surprised if Mexico’s successful deal spurs a number of governments and companies into following Mexico’s example. But if the experience of the mid 1990s is anything to go by, then let that be a warning – the Philippines’ century bond was issued in June 1997, and July 1997 was not a nice time for Asian economies to put it mildly.

Last week we explored a topsy turvy world that quantitative easing (QE) could cause, with the lowest bond yields potentially occurring in the highest inflation economies. We noted that this would be the death of the bond vigilantes, as they are overwhelmed in their attempts to force higher bond yields by the ammunition of the printing press being put to work in government debt.

This begs the question – if the bond vigilantes are dead, who will take their place to enforce discipline?

The sequel to the bond vigilantes could well be the currency vigilantes. QE aims to produce a low interest rate environment with a traditional level of inflation by having negative real yields all the way along the yield curve. However, before you get there the currency vigilantes could well turn up to break up the QE plans. If the authorities are actually or are merely threatening to print money, then economic agents should act vigilantly and avoid this new money by exchanging it for other currencies or assets. It’s the rational thing to do.

It appears that the currency vigilantes may have started already. Economic agents are dumping the QE currencies ahead of the switching on of the printing presses, and that can be seen by their desire for unprintable gold, commodities, domestic companies with foreign (non-QE currency) earnings, and currencies that do not have trigger happy central bankers poised by the printing presses. This has potentially important implications for asset prices, but also threatens a stable QE process. If there is a huge flight from a QE currency, domestic inflation could become rapidly explosive with no immediate growth benefit, so throwing up even more policy challenges.

The bond vigilantes could well be removed from the equation by QE. But in order to effectively implement QE – as desired by any member of the magnificent G7 who tries – this policy might well find its ability to enforce its domestic monetary policy destroyed by the currency vigilantes.

Hi everyone, I’m the new guy on board. I started at M&G last week but the rest of the team is already working really hard to find me a ridiculous nickname.

Yesterday morning, I saw a familiar face in the news. My macroeconomics professor at LSE, Christopher Pissarides, had just won the Nobel Prize in economic sciences (jointly with Dale Mortensen and Peter Diamond). On top of being an exceptional scholar, I have to say that he is also a very good teacher and a very humble and approachable person, sometimes laughing at his own basic arithmetic mistakes while lecturing.

The search and matching theory that the laureates developed models how we end up with outcomes where unemployment persists even though there are job seekers willing to work for a wage that employers are willing to pay.

This theory on the frictions in labour markets is of particular interest in today’s economic environment. The post-recession unemployment rate in the US (9.6%) and the EU (10%) shows little sign of improvement and raises concerns about the speed of recovery. As Carmen and Vincent Reinhardt pointed out in their research looking at historical slowdowns, in the decade after an economic crisis in a developed country, growth remains lower and unemployment higher than its pre-crisis level. This implies that part of the cyclical components of the recession becomes structural.

The centre-piece of the search and matching model, the matching function, intuitively suggests that if the duration of unemployment is large there will be more mismatching in the labour market:

M = m . U n. V n-1

Where M is the number of matches, U is the number of unemployed workers, V the number of vacancies and m and n are constants. Note that m has a negative relationship with the duration of unemployment (falling when the average duration of unemployment rises).

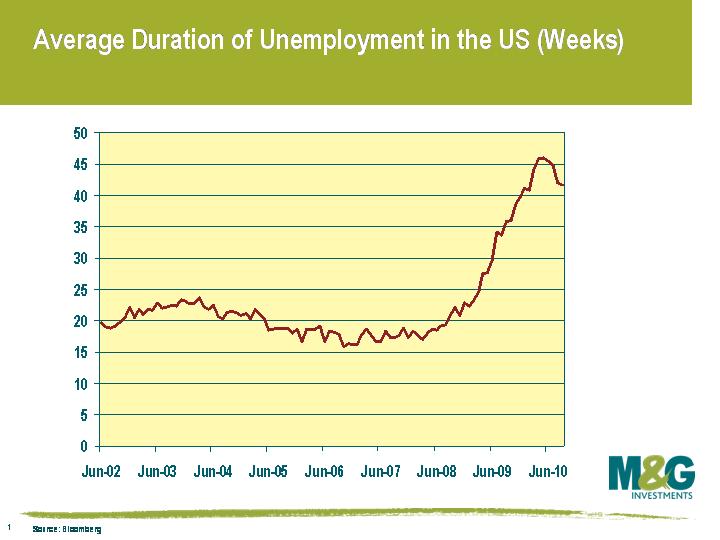

This leads us to think about the problem of the duration of unemployment, which has risen dramatically since the beginning of the crisis, from an average of 17.3 weeks in December 2007 to 41.7 weeks in September 2010.

The central message Pissarides shared with the world on the day he received the Noble prize is clear: “One of the key things we found is that it is important to make sure that people do not stay unemployed too long”.

The central message Pissarides shared with the world on the day he received the Noble prize is clear: “One of the key things we found is that it is important to make sure that people do not stay unemployed too long”.

Long term unemployment is one of the major factors explaining the persistence in the unemployment rate as workers lose their skills and knowledge, and above all their motivation. Pissarides argues that government subsidies should be used to help companies to hire people back and benefits should be accompanied with conditions that encourage people to find a job much quicker. These policies may help to reduce the so called frictions. The Fed is aware that QE is too blunt an instrument to directly address current employment distortions – but with no political consensus for fiscal action, I fear that Pissarides’s message will go unheard. In other developed economies, austerity measures are likely to include cuts in government subsidies rather than increases, which risks letting unemployment become entrenched.

Traditionally the main concern for a bond investor is inflation. It reduces the real returns of a bond, hence prompting higher long term interest rates, and causes the authorities to increase short term interest rates as a policy response. The increases in rates cause the current value of bonds to fall. Inflation is bad for bonds, full stop.

Quantitative easing is now threatening to turn that relationship on its head. The printing of money and purchasing of governments bonds by central banks has the primary aim of increasing inflation, thus, in normal circumstances, lowering bond returns. However the increase in money supply not only reduces its value from a real perspective but also means that the cost of borrowing falls, hence driving short term rates lower, which is a positive event for bonds. Additionally, the purchasing of government bonds by the authorities also drives long term bond yields down and therefore prices higher – again a positive event for bond holders.

Normally, if an economy has higher inflation one would expect it to have higher bond yields. Under QE, if an economic block such as the US is printing money while another economic block like the Eurozone is not turning on the printing presses, one would have traditionally expected that European government bonds would yield less than US bonds due to their position within the lower inflation zone. However, in an extreme example where the US Fed lowered every US Treasury yield to 1% and then bought them back with freshly minted dollars, it could be observed that the US would have both the highest inflation economy and the lowest long and short term government yields.

This may all appear to be counterintuitive, but if you want to stimulate an economy from a monetary perspective you need negative real rates. Usually, when you do this, the Bond Vigilantes turn up and push long rates up, thus negating the government policy. QE rides roughshod over this possibility, and you therefore end up with a potentially topsy turvy outcome.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.