Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

Ireland is definitely facing a liquidity crisis, and that liquidity crisis could evolve rightly or wrongly into a solvency crisis. It needs help.

Like any such problem, that help involves emergency short term measures (basically cash funding) and long term advice and financing to solve its structural long term problems. In the next few weeks the short term problem is not the Irish state but the Irish banks. They need funding on a huge scale as their short term funding requirements are enormous, whilst confidence falters and money is withdrawn from the system by nervous counterparts. This difficulty will become a real burden on the Irish state next year as they have previously stated that they will be guaranteeing nearly all the liabilities of the Irish banking system. The ECB, European union members, and the IMF are fortunately all prepared to help. However, negotiating how much burden the Irish people should suffer in this emergency phase is going to be difficult. What can go wrong ?

Lenders tend to impose conditions when disbursing funds; enforced austerity and foregoing some sovereignty are painful for any nation, though more so in this case given the history of the Irish nation’s fight for self rule. Whilst Ireland can possibly claim it does not need help if it reduces or walks away from guaranteeing its banking system, simply copying the Icelandic approach to banking system failure might potentially cause more losses and chaos abroad than at home. Presumably a successful negotiation will result in an element of burden sharing.

The main problem over negotiations is probably going to centre on Ireland’s attractively low tax profile that encourages significant inward investment. This is a critical advantage for Ireland, which is seen as unfair in the European single market by its fellow members. From a European perspective these allowances take jobs and tax revenue away from them, whether it be multinationals or pop stars. However, this is a crucial advantage for Ireland – by giving up this competitive advantage Ireland would effectively accept short term relief whilst losing the long term advantage.

What about the long term ? I have argued here previously (see blog) that the long term problem (which is the root of this short term problem) is the inflexibility imposed on labour and capital markets by the single currency regime. In the short term hopefully the politicians and the financiers can get together to solve the immediate liquidity problem. But I still struggle to see how in the long run all Irish banking debt can be honoured and how being a member of the single currency regime is optimal for the Irish economy.

If you’re not one of the 1,454,441 people who have already seen the “Quantitative Easing Explained” video on You Tube, you can learn all about “The Ben Bernank” and “The Deflation” here.

Guest contributor Vladimir Jovkovic, Credit Analyst

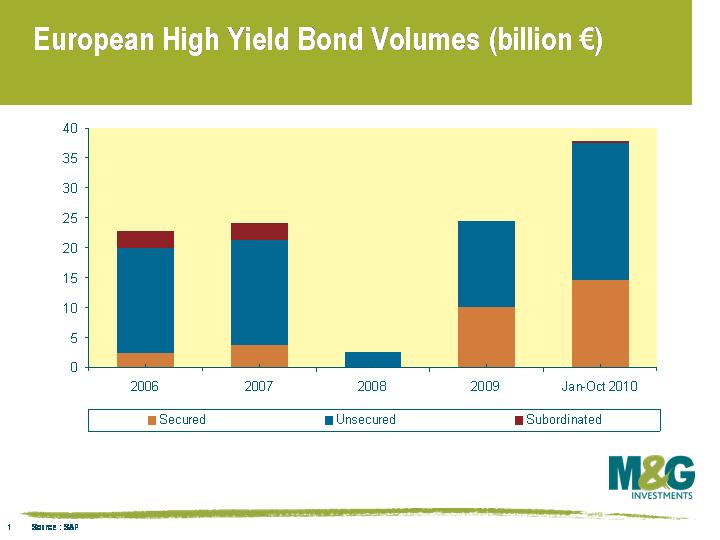

Issuance in the high yield bond market in Europe this year through October has already exceeded the total issuance for the full year in 2009. The novelty since the reopening of the market in 2009 has been the fact that high yield corporates have been looking to refinance senior secured bank loans into senior secured bonds, rather than the more common unsecured bonds. As such, the proportion of secured bonds issued by high yield companies after the financial crisis has been ~40% of total issuance compared with the more muted 10-15% level before the crisis (see chart).

Part of the reason in the shift has been the recycling of loans associated with LBOs into the bond market as the primary loan market effectively shut down. As banks repair their balance sheets and restrict their lending, the public bond market is stepping in to fill the gap.

The question then arises, how will the relationship between senior secured bondholders and senior secured lenders develop? Will lenders continue to have disproportionate control on enforcement of security? Will senior secured bonds create more stability in the high yield market? The answers to these questions will no doubt emerge with time, but meanwhile and more fundamentally, how secure are secured bonds?

For a start, the ‘Senior Secured’ label is not a panacea for bullet proof security. Often the ‘Secured’ label is in fact misleading once you delve into the documentation. Secured bonds often involve pledging security on physical assets (for example plant and machinery), typically with a limit on the proportion of assets and cash flow derived from the assets covered. This in itself will partially define the security of the bond. However, some secured bonds have a security which consists of equity in subsidiaries of the issuer – for example Polish Television Holding which issued bonds secured by share pledges on its stake in TVN, a broadcaster. This is clearly not as secure as security against physical assets; and, therefore, the question then becomes whether these soft security ‘secured’ bonds are justified to have lower coupons compared with unsecured issues.

Then there is the more contentious issue of relative security in structures that contain secured bonds as well as loans. In the case where senior secured bonds partly refinance existing senior secured loans, whether the new senior secured bonds rank pari passu (equally) with the existing secured loans will depend on whether they share the same position in the capital structure and the extent to which the security package shared is the same. It appears that in recent transactions when existing bank debt is partially refinanced with senior secured bonds the loan holders retain control, whilst when both bonds and loans are refinanced together bondholders have an opportunity to share control.

It is also important to consider the inter-creditor deed, which may determine the loss sharing arrangement between creditors and their effective relative ranking on enforcement. The inter-creditor deed has not always been made available to bondholders, which has made it difficult to ascertain bondholders’ precise rights in an enforcement scenario. For example, the inter-creditor could specify that senior secured bond holders are not part of the instructing group for enforcement proceedings, leaving them in a passive position with respect to controlling negotiations, were a default to happen.

With the rise in issuance of senior secured bonds and their greater enforcement rights compared to the more traditional unsecured bonds, making the inter-creditor available to high yield bonds holders makes sense. It appears, at least for now, with recent high yield issuers such as Exova (testing and advisory services), R&R (ice cream) and Polypipe (pipes for construction) that the tide is shifting in favour of higher disclosure. Greater transparency in the market will carry the benefits of improved liquidity and depth of market as bond holders become better equipped to answer the question ‘How secure is secured?’.

“Drinking poison to quench a thirst” – that’s Dagong Credit, the Chinese credit rating agency’s, view of the Fed’s monetary policy decisions of late. The recent money printing initiatives (QE2) and Dagong’s perception that the US is less intent on repaying its debts were their motivation for downgrading the US from AA to A+ last week – somewhat below the AAA ratings that S&P and Moody’s have for the US. Those US rating agencies rate Poland, Israel, Malaysia and South Korea in the A area.

Now presumably there is a fair amount of politics at work here, but nevertheless the report makes for an interesting read. It contains some of the most punchy language I’ve ever seen in a research report (“in essence the depreciation of the U.S. dollar adopted by the U.S. government indicates that its solvency is on the brink of collapse”). It’s a good job that the report didn’t move the market in any way, or there might have been a somewhat terse conversation with the Chinese government’s reserves managers – who own a mere $868.4 bn worth of US Treasuries.

In the early 1930’s Newfoundland – until that point a sovereign state – was struggling to repay its loans. Rather than default and face the wrath of the British gunboats, it was agreed that the country would be controlled directly from London. Fortunately things have moved on and debt now ranks below a nation’s sovereignty in times of default. Banks are not so fortunate; they aren’t protected from the wrath of their creditors.

Typically if a bank fails another bigger, stronger one is found to assume control. (Which, incidentally is what happened to Newfoundland after the Second World War – it was absorbed into Canada.) Bank failures are a messy business and regulators around the world have been trying to come up with new ways to stop banks from falling over and to limit the damage when they do.

Where senior debt will rank in future bank liquidations, and what the implications are for that market are some pretty serious questions thrown up by this process. Until recently it was assumed that holders of senior bank paper would be treated the same as bank depositors in a bank wind up, i.e. they would suffer no losses. Noises coming out of the western world’s various regulators have pointed to senior debt becoming loss participating in future. I guess if you make a loan to a badly run bank, why should you expect all of your principal back when things go wrong?

Pension funds and insurance companies have thus far held a large number of these securities because of the perceived low risk of capital loss. If they still wish to maintain credit and duration exposure to the banks at the top of the capital structure they will be inclined to switch out of senior paper and into covered bonds.

Covered bonds are secured on a pool of mortgages. Therefore, if a bank fails, you should still receive your interest and principal payments, assuming the underlying mortgage holders continue to make the payments on their homes. In a fortunate coincidence, the new capital requirements that are being imposed on banks incentivises them to issue covered bonds as they require less capital to be held against them under Basel 3.

At the other end of the capital structure will sit contingent capital (CoCo) type notes, such as those issued at the end of 2009 and earlier this year by Lloyds and Rabobank. Regulators are very keen for banks to have this sort of countercyclical capital in their balance sheets. Once the capital position (currently the tier one ratio) of a bank hits a predetermined trigger level, these bonds convert into equity and therefore increase the portion of the capital structure that was designed to be loss absorbing all along.

The traditional subordinated notes in a bank’s capital structure – Lower Tier 2, Upper Tier 2 and Tier 1 – according to some, will effectively cease to exist under the new regime. This implies a bank’s capital structure will in future be made up of deposits, covered bonds, senior notes, CoCo’s and equity.

Purely from a bond investor’s perspective – setting equity and deposits to one side – it feels to me as though senior debt will become a rather esoteric asset class. Risk averse investors will buy the covered bonds that the banks are keen to issue, while those looking for higher yields will opt for CoCo’s which they will be forced to issue. If you imagine a situation (shouldn’t be too hard) where a bank gets into difficulty, its CoCo’s are triggered but still falls into bankruptcy. The equity will be wiped out leaving a senior debt holder not only at the bottom of the pile in a liquidation, but also with a claim over fewer assets than they historically would have had, since most of the mortgages would have been pledged to the covered bond pools. Unless they invest in some gunboats, I can’t help feeling that investors in senior bank debt might be in for a rather rough time in the years to come.

We’ve written recently about the bond world going ‘topsy turvy’, in that a consequence of QE may be that the higher inflation economies could end up with having lower yielding sovereign bond yields than the lower inflation economies.

Another way that the bond markets are starting to look topsy turvy is in terms of sovereign credit rating versus a country’s perceived risk of default, whereby a number of lower rated sovereigns are now yielding less than higher rated sovereigns. This is particularly the case if you look at the CDS market, which measures the cost of insuring against sovereign default.

This chart shows French CDS versus a number of single A rated issuers. As you can hopefully just about see, France (AAA) is now wider than single A issuers such as China, Malaysia, Chile, Slovakia and even South Korea (whose 5y CDS reached almost 500 in early 2009). If the perceived risk of French default increases further in the next few months, which is quite possible given the French public’s lack of appetite to engage in any meaningful reform, it won’t be long until France trades wider than another group of emerging markets including BB rated Colombia. France obviously isn’t alone in terms of developed economies seeing their risk of default rising; the big story this week has been Ireland (rated AA-), which yesterday briefly saw its sovereign CDS trade wider than Argentina (rated B-).

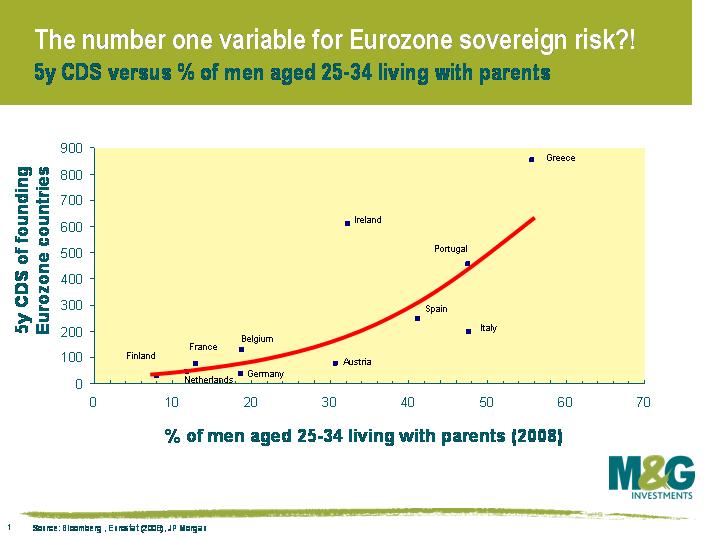

Or, on a more light-hearted note, perhaps austerity, growth and inflation have little to do with default risk. JP Morgan have an alternative explanation (see chart).

Recently, we have often spoken about QE, and how it could result in the demise of the bond vigilante (topsy turvy), and the birth of the currency vigilante. Well, we are getting very close to the presumed launch of further unconventional monetary policy by the Fed on the 3rd of November. The market is trying to work out if it’s shock and awe or a gradual siege mentality that the Fed will deploy. Quite interestingly, the Fed has been asking US bond dealers what they are expecting, and what the markets’ reaction to QE2 would be!

However, this is not a purely domestic issue. The currency vigilantes, as previously discussed, are likely to react by driving the value of dollars down, thus increasing potential inflation and growth in the USA. This is something the Fed would be keen on as long as the decline in the dollar does not become violent and disorderly.

The Fed, however, is not alone in its desire for lower unemployment in a low inflation landscape: many economies around the world face similar issues. This is best typified by Japan. The BOJ has put itself on a war footing and is ready to respond to the salvo the Fed looks set to launch on the 3rd of November. How do we know that? Well, they took no action at their last meeting on the 28th of October, but have brought forward the date of their next meeting to the 4th of November, in order to respond to the Fed’s next round of QE.

As we know from recent currency intervention, the Japanese do not wish their currency to appreciate. So, how may they respond to the Fed? Well, presumably using simple supply-demand economics: in order to keep the yen at the same rate as the dollar they might have to simply match the Fed by printing an appropriate amount of yen, which could be described as unconventional foreign exchange intervention.

This all sounds very inflationary and very bond negative. However, if the vast sums of money that are created in the likes of the USA, Japan, and possibly the UK (70% of the G7 GDP) is initially deployed to buy back government debt, then the bond markets may have no choice but to bizarrely rally in this potentially higher inflationary environment.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.