Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

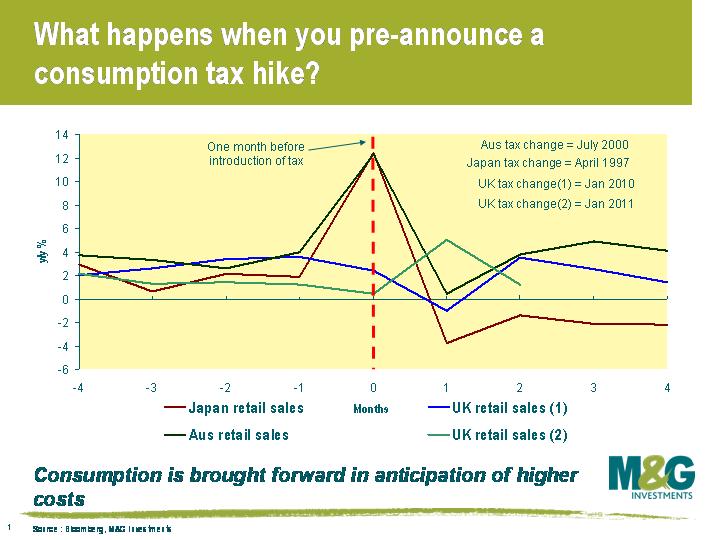

Here’s an update of a slide we produced a year ago following the January 2010 move back to 17.5% VAT from the 15% emergency rate. We were comparing the UK’s retail sales numbers to those in Australia and Japan around the time of their consumption tax hikes, and asking whether we’d see pre-loading of purchases ahead of the sales tax and a collapse back afterwards. The blue line shows that there was some deterioration in sales post the tax rise, but it was probably not as pronounced as we might have expected.

With a move up in VAT again, this time to 20%, we can see how things are going this year. Remember that December’s weather was pretty grim, and that the VAT hike was on 4th January – so there was pent up demand post Christmas and 3 days of shopping in January before the hike came in. We can see that sales rose in January – which wasn’t in the script! Last week though we saw the release of February’s official retail sales data showing a fall of 0.8% compared with January. Department store sales were especially weak (down 3.2% on the month). If we see a similar pattern to last year, we could expect the year on year rate of retail sales growth to turn negative hereafter.

The VAT hike might actually turn out to be relatively trivial to consumers in the scheme of things. Whilst sales fell, shops saw the biggest increases in prices (the deflator) for years – this was the biggest month on month increase in the price deflator since the series began in 1988, and only a part of this was due to the VAT rise. Clothing and footwear inflation was especially strong. The next few months could be very tough for retailers.

Has Bristol Water opened the tap on corporate inflation linked bond issuance? The water utility company came to market last Friday with a small £40m 30 year deal which pays a coupon of 2.701% plus inflation.

The interest payments on corporate inflation linked bonds – as the name suggests – move in line with inflation. Each issue has its own quirks but, as an example, the Bristol Water new issue pays a coupon of half of 2.701% every six months, uplifted by the change in the UK Retail Prices Index from issue (there’s a 3 months lag in the inflation number used because of the delay in collecting and releasing the inflation statistics). The final redemption proceeds in March 2041 are also uplifted to reflect inflation over the lifetime of the bond (giving a “real” return). The bond mechanics are pretty similar to those in the index-linked gilt market, although in this case there is a credit spread as well as the underlying real yield. In this case the bond priced at 200 bps over the 2040 index linked gilt, reflecting both credit risk (Bristol Water is an investment grade company, Baa1 rated by Moody’s) and something for illiquidity (£40 mn is one of the smallest corporate bond deals).

We haven’t had any corporate linker issuance for a year or so but it appears that some firms are now looking at it as an option – we’ve been approached by 3 other issuers in recent months who are considering issuance. Maybe it’s the sustained elevated level of inflation – RPI is currently at 5.5% year on year – that is giving these companies pause for thought. If, like Bristol Water and other utility companies, your revenues are explicitly linked to RPI (due in this case to Ofwat, the UK water regulator) it is eminently sensible to have your liabilities linked to it also. When inflation starts to recede you don’t want to be left with fixed debt payments while your revenues are falling away.

Is there likely to be issuance outside of the utility sector though? Why would corporates issue inflation linked debt in a world where inflation is high and rising? At least when governments issue inflation linked bonds they have some control over keeping inflation low (through tighter fiscal and monetary policy). Well, outside of the utility sector another big type of issuer is infrastructure related companies. Operators of toll bridges (Severn Bridge in the UK, Oresundsbro Konsortiert which runs the bridge between Sweden and Denmark), railways (RFF in France), and PFI projects (Kings College Hospital) all have inflation linked revenues. We also have Tesco – a supermarket which sells most of the things in the inflation basket nowadays – some banks, and a handful of other issuers. But are corporate treasurers going to want to have borrowings linked to consumer prices at a time when inflation expectations are on the rise? On the whole probably not, although the inflation swaps market (a form of derivative where fixed rate payments are switched for payments linked to inflation) allows borrowers to issue debt to match investors’ demand. In the end though you still need to find somebody who is happy to “pay” inflation. So the inflation market is unlikely to ever grow to anything like the size of the traditional corporate bond market, but with investor demand for inflation protection growing, some issuers will see this as an attractive form of issuance much in the same way that the high yield market grew from nothing in Europe at the end of the1990s to the big and liquid asset class it is now on the back of investor demand.

We’re pretty keen on corporate linkers here, not just because we think 2011 is a year of persistently high RPI, but also because they look good value relative to ordinary corporate bonds. For example I could buy a Tesco 2016 index linked bond at 1.2% more yield than the equivalent index linked government bond, or I could buy the Tesco 2016 conventional bond at 0.9% more yield than the equivalent conventional government bond. This is the illiquidity premium. Long may it persist, but whilst it does it probably acts as another reason why we shouldn’t expect bumper issuance in the asset class. Corporate treasurers and CFOs should however get in touch if they feel we could be of help!

Once a year I head down to the Embankment, opposite the Houses of Parliament, to try to film a comment on the UK Budget whilst being heckled by wild eyed men drinking Kestrel Super, and pestered by packs of Italian students mistaking me for Brad Pitt making a movie about a tired fund manager in an ill-fitting suit. Here’s this year’s Budget film. If it sounds like I don’t think that the government are doing a great job on the economy, that would be a fair analysis. But for what it’s worth if we’d ended up with a Labour-LibDem coalition instead I doubt we’d have a AAA credit rating or the stable currency that we have right now. On the other hand we might well not be looking at the collapse in UK growth expectations that we’re experiencing (the OECD expects just 1.5% UK GDP for 2011), and over the medium term it’s growth that delivers lower budget deficits.

Coupled with Tuesday’s 5.5% RPI inflation print, there’s talk of stagflation again. Certainly there’s enough baked in the cake to make 2011 a very inflationary year, and along with a big fall in February’s retail sales announced this morning came the news that shop prices are rising at their highest rate since 2008. We expect however that 2012 will be a year where inflation moderates, as the VAT hike drops out of the numbers and as below trend growth and high unemployment rates restrict demand.

(Latest news: Moody’s: “Although the weaker economic growth prospects in 2011 and 2012 do not directly cast doubt on the UK’s sovereign rating level, we believe that slower growth combined with weaker-than-expected fiscal consolidation could cause the UK’s debt metrics to deteriorate to a point that would be inconsistent with a AAA rating”. Oh dear – rubbish growth and we lose the AAA…)

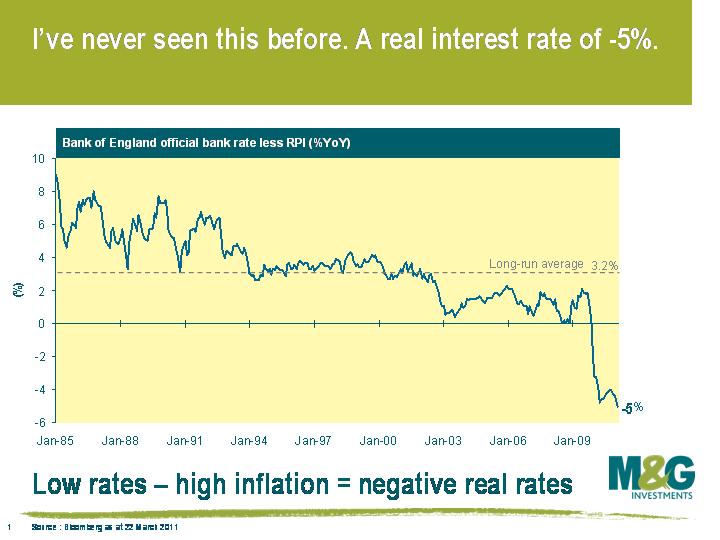

The financial crisis is resulting in the authorities, the public, and investment managers seeing things they did not expect to see. Today’s headline RPI level of 5.5% is a record 5% above the Bank of England base rate of 0.5%, resulting in a negative real interest rate (base rate – RPI) of -5%. This is the most divergent I’ve seen this in my 25 years in the city (see chart).

The bond bears think that the relationship will be normalised by a rapid increase in the base rate and a fall in inflation towards more normal levels. The bulls would suggest that the inflation measure reflects temporary factors and will therefore decline to more normal levels with only modest rate increases by the Bank of England.

However, the fate of the base rate and inflation does not sit with the bond bulls and bears but with the Bank of England Monetary Policy Committee (MPC). Their policy of ultra low rates means the MPC is missing their CPI based inflation target of 2% on a regular monthly basis. Since September 2007, inflation has been above 2% in 35 out of 42 months.

Why are they doing this? Presumably the MPC believes that the high inflation rate will be temporary in nature, however there could be other motives behind their policy stance. The Bank of England via QE has previously determined that interest rates had reached their effective bounds in stimulating the economy, as a central bank cannot achieve negative nominal rates. Therefore in order for their rate setting policy to work they have become very relaxed with negative real short term interest rates as they pursue a policy of cleansing the system of its financial hangover from the credit bubble as best it can.

Lets hope from the Bank of England’s point of view that the hair of the dog cure of ultra low real rates is actually an appropriate diagnosis of a fragile, staggering UK economy. Otherwise we could all end up in a dizzy inflation spiral.

Applications for London 2012 Olympic Games tickets are now open. You beauty! Having been at the Sydney 2000 Olympic Games, I can honestly say that attending the Olympics is one of the highlights in my sport watching career (which includes watching Australia qualify for the football world cup, George Gregan’s tackle against New Zealand in the Bledisloe Cup and Steve Waugh’s last ball century against England in 2003). Ticket prices for the public range from £20 to £2,012 and oversubscribed events will be decided by a ballot which suggests it may all come down to luck. Or is there a way of enhancing my chances through the economic theory?

The answer is – probably. Sports that are unpopular are unlikely to see an oversubscription for their tickets, suggesting I could apply for those tickets and reasonably expect that I will receive an allocation. But I am after the big events, like the opening ceremony. Besides, I could likely pick up a ticket for the unpopular events and sessions on the day.

Like all good statistical models, I’m going to have to make some assumptions. If I assume that those applying for tickets are rational consumers, meaning as price increase demand will fall, then the most demand for tickets will be for the £20.12 tickets. There will be less demand for the £2,012 tickets. However, my unlimited wants (in the case, £2,012 tickets) can only be met with scarce resources (my budget). So I’m not willing to spend all my hard-earned cash on the most expensive tickets. I am also assuming that there are equal amounts of each ticket category for sale which is probably not the case.

Having settled on a price range, I now have to assess how many tickets I want for the opening ceremony. The Olympic Stadium will have a capacity of 80,000. London 2012 chairman Lord Sebastian Coe has mentioned that for high-profile events like the opening ceremony, 50% of tickets will be available to the public. This brings my ticket universe down to 40,000.

The population of the United Kingdom and Northern Ireland was 62 million in 2010. But other European countries may also apply for tickets. For these European countries, the combined population is around 454 million.

I am going to assume 1% of the UK population will apply for opening ceremony tickets and 0.5% of the population of the other European countries. This brings a total of 620,000 + 2,270,000 = 2.89 million applicants for 40,000 tickets of various price categories. Therefore each applicant will have a 1.4% probability of obtaining a ticket.

I want a ticket for my girlfriend and myself, which of course is two tickets. But we will have a greater chance of obtaining tickets if we both apply for a ticket each, rather than if I apply on my own for two tickets. This will increase our collective chances. Additionally, each applicant may apply for 4 tickets each.

To maximise our chances of obtaining a ticket, my girlfriend and I should follow the following rules. Firstly, the most expensive tickets will have less demand so we should apply for the most expensive tickets that we can afford. Secondly, rather than just one of us apply for two tickets, we should both apply for four tickets each. This is because the ceremony will likely be many times oversubscribed, suggesting that any surplus tickets will be easily disposed of in the official ticket resale service to other spectators for cost price. Who am I kidding, if we are lucky enough to get any surplus tickets I am sure there will be some takers amongst the bond vigilantes!

Much has been written about Iceland’s response to its banking crisis, and whether its decision to put its banks into administration and swiftly force losses onto bank creditors has proved to be the key to restoring economic stability. Does this provide a model that Ireland and others should have followed? Commentators such as Paul Krugman and the IMF were quick to point out that Icelandic GDP expanded by 2.2% in Q3 2010, setting it firmly on the path to recovery, though the subsequent 1.5% contraction in Q4 showed that Iceland’s problems were far from fully resolved. While it’s hard to place too much weight on notoriously volatile Icelandic macroeconomic data, given the small size of the economy (with a population of just 319,000, a single factory closure or even just a few families catching a nasty cold could materially influence output), it is worth digging beneath the surface to find out what is really going on as there are still some interesting lessons for the rest of Europe.

So what did Iceland do apart from putting the banks into administration? For a start, they were quick to prioritise national interests above obligations to other European countries, most notably in refusing to compensate the UK and Netherlands for the bail-out of Icesave depositors. While I am not arguing that this was in any way morally correct, it certainly did give politicians the breathing space needed to work on other measures, both by reducing the national debt burden and by giving citizens some say in their future. A further referendum on the subject is due in April, after previous compromise measures were firmly rejected by the Icelandic population (given the amounts involved, the outcome of these negotiations will be critical for Iceland’s debt position). Of course, it is much harder for the peripheral Eurozone countries to simply ignore the EU demands that their citizens honour not just their sovereign debt but also their banking sector liabilities to avoid banks in core Europe (and the ECB) having to crystallise losses on their periphery exposures. But equally it will be hard for elected governments in the periphery to maintain the long term support of their populations for the austerity measures needed to repay all the bank and sovereign liabilities if they don’t give their citizens some sort of say in the matter.

Secondly, Iceland was both willing, and, crucially, able, to embark on a comprehensive restructuring of other debts within the financial system, not just bank liabilities. Debt levels of households and corporates were also unsustainable, and simply writing off bank liabilities was never going to be enough to reduce the overall leverage of the country. The popularity of inflation linked mortgages in Iceland meant that when the currency collapsed in the wake of the banking crisis, and the soaring cost of imports led caused inflation to spike close to 20%, a large proportion of the population found themselves unable to service their mortgages. Similarly, a large number of corporate and consumer loans had been denominated in foreign currency, and the collapse of the Icelandic krona meant that these loans also created a heavy burden on borrowers. Like several other countries, Iceland proposed mortgage forgiveness, allowing for partial write offs of debts and capping loans at 110% LTV to limit negative equity. However, unlike other countries, Iceland also attempted to clarify how the inevitable losses would be shared; partly by the newly created (and primarily state and creditor owned) banks, partly by the state’s housing fund, and partly by the insurance and pension funds who had invested in Icelandic mortgages. After long wrangling with the IMF, it appears the basic principles of this restructuring agreement have been agreed by all sides, though the devil will of course be in the detail.

This ability to get savers and borrowers around the table together to hammer out a burden sharing agreement is critical – of course it is much easier in a small country, especially once foreign creditors have already been snubbed, but it’s a process that I believe other countries will have to go through. The politics are also much simpler in a country with a relatively young population, where borrowers outweigh savers – countries with different demographics and a strong savings and pensions sector will find it much harder to implement debt forgiveness measures. However, ultimately they may have to try. Interestingly, Hungary has set a precedent for dealing with recalcitrant private pension funds by effectively nationalising them, and while a drastic solution, it is not unthinkable that similar measures could be implemented elsewhere in the EU if that is what is needed to bring all creditors to the table.

Finally, in the wake of the crisis, Iceland imposed capital controls to prevent the flow of funds offshore. While this has costs to the population, particularly savers stuck with devalued krona savings, it has proved useful in enabling the government to fund its budget domestically. Again, this sort of measure wouldn’t be easy for Eurozone countries to implement unilaterally, but in a country such as Ireland where the banking sector is effectively state owned, it would be interesting to see whether capital controls could to some extent be achieved via administrative measures.

The jury is still out on whether Iceland’s restructuring will ultimately be successful, and as highlighted above it will be tricky for Eurozone members to implement the same measures, but Iceland certainly provides an interesting case study in dealing with a financial crisis.

The European Central Bank firmly laid its cards on the table at last Thursday’s press conference. Trichet et al are in no mood to risk potential second-round effects of rising wages. According to JP Morgan the phrase ‘strong vigilance,’ uttered by Trichet during his prepared remarks, was used one month prior to all policy moves during the last tightening cycle. Not surprising then that Bunds sold off and the Euro climbed. A 25 basis point hike in April to 1.25% is now all but a done deal.

Critics have weighed in with chants of an impending policy error on the ECB’s part. Whilst accepting commodity price inflation is clearly on the rise, there are limited signs of second round effects. As Jim wrote last month, recent union negotiated wage increases in Germany, Europe’s strongest economy, have proved fairly muted.

It’s hard to argue with claims that rate hikes will merely heap pain on an already embattled periphery. Coupled with structurally high unemployment, fiscal austerity and a seriously damaged banking system, the prospects don’t bode well for growth .

We know that the ECB’s primary and overarching aim is to ensure price stability. As the ECB notes “We… have as our primary objective the maintenance of price stability for the common good.” In fact, the ECB would argue that price stability is a prerequisite for long run sustainable growth and low unemployment. However, as we’ve argued before, if it comes down to a choice between protecting its inflation credentials and growth the ECB will side with the former. Is it right to damage Europe’s growth prospects to tame an inflation rate that currently stands at 2.3%, largely due to factors outside the ECB’s control?

Some argue that the ECB should not be so nervous about losing its inflation fighting credibility. As MPC Member Adam Posen points out in a recent speech, the Deutsche Bundesbank did not lose its anti-inflationary credibility post the oil shock of the late 1970s, despite inflation running above its 2% target for over six years. Posen claims that despite regularly overshooting both its inflation and money supply target, the Bundesbank was able to keep inflation expectations anchored through the “transparency and flexibility of its monetary framework.”

Perhaps the ECB should give serious thought as to whether it could also engineer a similar scenario. The consequences of prematurely embarking on a tightening cycle could prove disastrous for parts of the European Community and beyond; even if they’re only doing their job.

“I used to think if there was reincarnation, I wanted to come back as the president or the pope or a .400 baseball hitter. But now I want to come back as the bond market. You can intimidate everybody.”

James Carville, Clinton administration advisor, 1993

When we started the Bond Vigilantes blog back towards the end of 2006, the world looked pretty different – and even the term “bond vigilantes” had fallen out of use. Looking back at our first couple of months of blogging, we were writing about the first signs of weakness in the Chicago housing market, our worries about aggressive lending by the UK banks, and the new developments in the supercharged CDO market. But this was still a world in which Central Bankers had “won” the war on inflation after a two decade long battle, where the term “sovereign debt crisis” was solely used in relation to the emerging markets, and where Lehman Brothers and Bear Stearns sat at the top table of global investment banks.

Today, we’re slowly emerging from the biggest downturn since the Great Depression of the 1930s. Interest rates are stuck around record low levels, Central Banks have been printing money and bailing out private businesses, and the banking sector remains on the critical list. We worry about the solvency of even the biggest and strongest western governments – and some, like Ireland and Greece have only avoided default thanks to loans from the IMF and the EU. Yet despite high levels of unemployment and empty factories, inflation is staging a comeback. Not as a result of rampant consumers demanding more goods (at least in developed economies), but driven by price shocks in the global commodity markets. As emerging market populations have grown, and got richer, energy and food inflation have become a problem.

As populations feel the squeeze from two directions – mediocre income growth and higher goods prices – being a self-proclaimed “bond vigilante” feels somewhat uncomfortable. Is it right that the markets should have the power that James Carville talked about in the famous quote at the top of this page? Is a AAA credit rating worth more than half a million jobs? Is stable inflation more important than growth? Or maybe we should ask, like the soldiers in this Mitchell & Webb video, “are we the baddies?”.

But we should also remember the costs of high levels of inflation (at its extreme, in Weimar Germany or Zimbabwe) or debt default (Latin America in the 1980s) and realise that there is no simple link between rampant borrowing or money printing and a happy population. We can still argue however about the timing of fiscal austerity or monetary tightening – and we often do, even within our team.

So this blog is here for us to share our views on the things that matter to bond investors – inflation, interest rates and the global economy – as well as to talk about the bond markets themselves. Over the past few years we have blogged about value in high yield bonds, the outlook for emerging market debt, and new developments in the inflation-linked bond markets. We’ll also make sure we let you know our views on the traditional investment grade corporate bond markets – being a good bond vigilante should also be about identifying deteriorating trends in corporate behaviour, as well as that of governments.

Please get in touch if there is anything in particular you’d like us to look at. Running money for our investors will always get priority, so we may not respond immediately, but it’s been great to hear the views of our readers, however forthright! In one week alone I was accused of both being an apologist for the US Tea Party, and a member of a Marxist sleeper cell.

So thank you for supporting this blog, we hope you like the new look and feel – and let’s hope bond markets stay interesting, but not too interesting.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.