Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

A lot of the cash that’s been created over the past few years is sloshing around the world trying to find somewhere to hide. There has been a huge bid for anything deemed a safe haven asset, a bid that has been propelled by an imploding Eurozone and US politicians that are seemingly looking to bring its $14 trillion poker game to a spectacular finale by committing collective hara-kiri.

The problem is that if you take the US out of the picture, there aren’t enough non-shaky AAA assets to go around. Germany and France have about $1.7tn of sovereign debt outstanding, although France is probably the next AAA-rated country to find its credit rating under threat. The UK has about $1.2tn of sovereign debt, and gilts have been big beneficiaries recently, but a double dip recession in the UK (which MPC member Martin Weale recently highlighted as a risk) will cause a U-turn on austerity measures which in turn will place the UK’s AAA rating at risk. After the UK, Canada has about $1 trillion of sovereign debt. After that you’re pretty stuck – Australia has about $0.3tn, Sweden has $0.1tn, and there are a few countries with even less debt.

Norway is the safest sovereign in the world if you take the cost of insuring against default from the CDS market, but as you’d expect for the world’s best quality sovereign, Norway has very little sovereign debt. As a result, the demand for Norwegian government bonds has massively outstripped supply, and a large gap has opened up between the yield on Norwegian government bonds and the Norwegian Krone 10 year swap rate. The difference between the cash rate and the swap rate is now at a similar level to that seen in October 2008. We think that the strong bid for government bonds issued by Norway, Sweden and Germany is totally justified though – indeed, we’ve been filling our boots with the stuff over the past few months, and given our well documented ongoing nervousness regarding a number of sovereign states’ creditworthiness, we think that there’s still significant value in the safest AAA markets.

The big safe haven bid has also been hitting some emerging markets, but in contrast to the money flying into Norwegian government bonds, the EM safe haven bid looks plain bonkers. The chart below shows the recent price action of Brazil’s 30 year US dollar denominated government bond, where spreads over US Treasuries have tightened from 140 basis points at the beginning of June to under 100 basis points now. Credit ratings don’t count for all that much these days, but if markets think a risk premium of less than 100 basis points is a fair price for a 30 year bond denominated in US dollars that is benchmarked over US Treasuries and is issued by a country that’s rated one notch above junk status then the market’s smoking crack.

This isn’t to say that emerging markets as an asset class are poor value. Much of what has driven financial markets over the past 15 years has been a direct consequence of emerging market countries maintaining artificially undervalued exchange rates. The global current account imbalances that have resulted from these policies go a long way to explaining the behaviour of various asset classes over this period. These global imbalances have lessened since 2007, but they still persist. Developed countries need a sharp devaluation versus many of their emerging market counterparts to restore competitiveness, restore economic growth, and ultimately help reduce debt levels. Overheating emerging markets need their currencies to appreciate, and EM currencies should (with a few exceptions) continue to rally versus developed market currencies.

But buying long dated Brazilian US$ denominated bonds is not how to implement this view. We think that the implied default risk from a number of emerging market bonds is far too low – an implied default risk that has been squished by the huge flow of money into EM debt and a relative lack of supply – and we have selectively put on trades across a number of our bond funds that reflect the view that some areas of the hard currency EM debt market are getting dramatically overvalued.

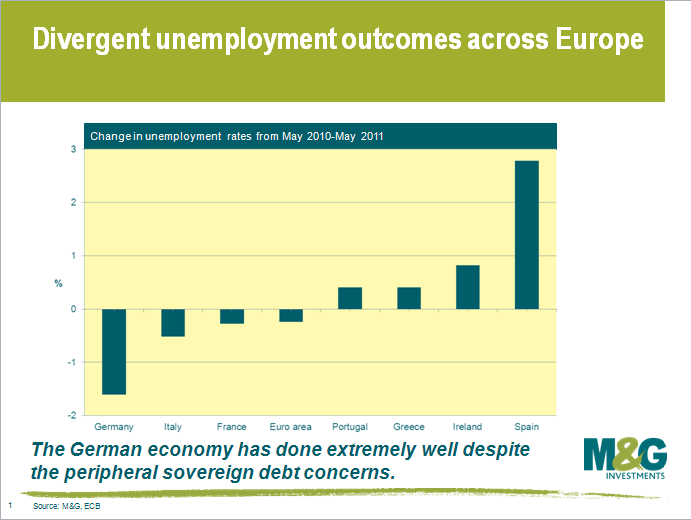

There is a shining light amidst the storm of the European sovereign debt crisis. Europe’s largest economy, Germany, is booming. Since June 2009, the German Federal Statistical Office has had the pleasure of notifying financial markets that the German unemployment rate has fallen. Today we received further confirmation of the strength of the German labour market, with the German unemployment rate remaining at a record low of 7.0%. This equates to a fall in unemployment of 11,000 in the month of July. In total, around 550,000 jobs have been created in the German economy since June 2009. Consequently, German consumer confidence is around record highs.

There are many reasons for the stellar performance of the German labour market. The German economy grew at 1.5% in the first quarter of 2011, or 4.9% over the year. Importantly, the growth numbers were mainly underpinned by strong domestic demand. Initially, the fall in the euro due to concerns over peripheral Europe provided the conditions for a boost in German exports. Now, the growth base has broadened, with domestic investment and consumption becoming increasingly supportive. It is our view that without the euro currency in place, the German Deutschmark would be the strongest currency in the world, German bunds may have negative yields, and the German economy would probably be in recession. The Swiss are experiencing this phenomenon through the strong appreciation of the Swiss franc in recent times. Is the Swiss franc a new safe haven?

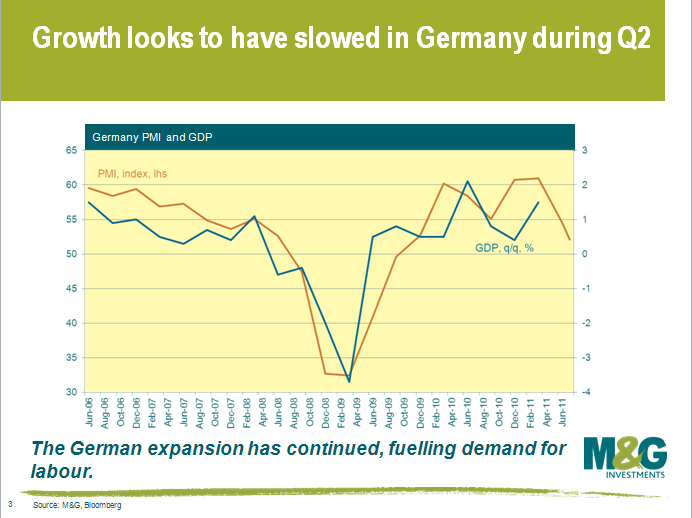

Of course, GDP is entirely backward looking. It is important that we also assess what the forward looking indicators are telling us as well. German business surveys are a good place to start. Despite the current concerns, German purchasing and manufacturing indices (PMIs) for both the manufacturing and services sector continue to suggest that the expansion of the German economy continued in Q2. It isn’t the stellar growth experienced earlier in the year, but a growth rate of around 0.5% in Q2 isn’t too bad considering the concerns around Greece. Despite the worries, the Ifo business climate and expectations index both suggest that the German corporate sector is in a relatively good mood. German firms are telling us that they are planning on spending record amounts on capital expenditure and investment in the coming 12 months as indicated by the German DIHK business survey. Consequently, it is not unreasonable to expect that the German labour market will continue to improve in coming months as firms look to invest in profitable projects.

In a way, the strong German growth outcome is directly related to the peripheral sovereign woes. The euro is currently far too weak for Germany, which means that the German economy is extremely competitive, its economy is booming, and its inflation is starting to accelerate. This is why the ECB has been hiking rates and may hike again before the year is out. But the flip side of German growth is the utterly miserable growth rate in Southern Europe, which is because the euro is far too strong for these deeply uncompetitive economies. Fernanda Nechio, an economist at the Federal Reserve Bank of San Francisco, estimates interest rates based on a Taylor rule analysis for peripheral Europe and core Europe. Her analysis suggests an ECB target rate of around 3% for core Europe, and a target rate of around -3% for peripheral Europe. On the one hand, the ECB is hiking rates to tighten monetary policy for the stronger core European nations, and on the other it is retaining loose monetary policy by maintaining liquidity arrangements for the weak peripheral European banks.

Some might say, the German economic party is the result of the peripheral European economic funeral. The German public bailing out southern Europe is the cost that they need to pay for strong growth outcomes and rising standards of living. Bailing out peripheral Europe is like a tax that has until now been deferred. To quote Dolly Parton: “If you want the rainbow Germany, you sometimes have to put up with the rain”.

So the results of the bank stress tests are out. Do they add anything from an investor viewpoint?

Well, despite the best efforts of the European banking Authority, we didn’t get the harmonised EU data we were hoping for. To say that there are inconsistencies in the data would be an understatement.

Disclosure varies hugely bank by bank, especially in areas such as their Loan to Value ratios for real estate lending, and that’s before you start trying to factor in the differences in the way property valuations are performed or indexed in each country. Banks, and in particular the tax systems and legal systems in which they operate, are still national. We’re a long way from a harmonised, EU wide banking sector.

There’s also no real information on banks’ liquidity positions. Assumed funding cost increases over the next two years are simply driven by the interest rate assumptions used, with little or no linkage to the banks’ actual and increasing costs of funding. It’s impossible to analyse what is happening to individual banks’ funding sources and costs. The EBA admits liquidity and funding is a critical issue but has backed away from making public its liquidity stress testing, presumably because they are concerned this might provoke further concerns.

One of the most frustrating issues for investors is that the EBA doesn’t stress test the legal entities to which investors and market counterparties are exposed or potentially exposed. So the French mutual groups are tested on a consolidated basis, when in fact debt and equity investors are taking exposure to very specific legal entities within the group, such as CASA within the Credit Agricole group, whose risk profile will be very different to that of the consolidated group.

However, the most important statement from the EBA in our view was the instruction to national regulators to require banks to raise core capital by any means possible, “including where necessary restrictions on dividends, deleveraging, issuance of fresh capital or conversion of lower quality instruments into Core Tier 1 capital.”

This means conversion of debt into equity where other sources of equity are unavailable. In Ireland this has already been accepted as necessary but in most EU countries regulators still do not have the legal powers to push through a forcible debt for equity conversion. Banks could of course try to achieve this via voluntary conversions, but ultimately the incentive for bondholders to agree to a conversion is limited unless there is the very real threat of a more draconian resolution regime to act as a “stick”.

Regulators and governments alike are well aware of this issue. The Financial Stability Board will this week put forward a consultation paper on the subject of international resolution regimes, along similar lines to the EU consultation published in January. These proposals aim to ensure governments can’t be forced to bail out the banking sector and thereby to ringfence the sovereign’s finances from those of its banks.

Equally, the critical issue of private sector burden sharing by the banks in any sovereign debt default also remains unsolved – until we get a clear framework for clarifying the role of banks in investing in sovereign debt, and find a mechanism for ensuring that all creditors, including banks, can and do take losses on investments in insolvent sovereigns, the umbilical cord between banks and sovereigns remains intact.

So rather than waste time sifting through stress test result spreadsheets, investors would be advised to analyse and understand the FSB resolution regime proposals for banks and the European Stability Mechanism framework for private sector burden sharing on sovereign debt. These are the critical issues facing investors right now, and all the stress tests do is highlight how important it is that a solution is found to enable banks and sovereigns to ringfence themselves from each other.

(For those interested in how the results might differ had sovereign debt haircuts been taken into consideration, see this calculator from Reuters Breakingviews)

This weekend’s family activity centred on the final film in the Harry Potter series, Harry Potter and the Deathly Hallows, 10 years on from when we saw the first instalment of the magical film series in 2001. Meanwhile in the Monday to Friday muggle world, the markets are focusing on the modern classical tale of Greece, that also began 10 years ago in 2001 when they entered the European Monetary Union. How will that blockbuster story end?

In the final instalment of Harry Potter, the story centres on the deathly hallows. Spookily, the three elements of the deathly hallows are comparable to some of the magical instruments Greece has at its disposal.

Sadly, they have already used the invisibility cloak to hide the true extent of their debt, in order to gain entry into the Eurozone back in 2001. Unfortunately, for them that magical charm has been exposed and its protection is lost. This leaves them with two further deathly hallows to get them through their current nightmare. They could use the resurrection stone, i.e. they can default and their debt will reappear as a shadow of its former self, remaining in the Euro, but angering the European Central Bank, and investors. Alternately, they could take the option of using the elder wand to threaten to destroy the whole system, and therefore gain support from fellow Eurozone members to band together to keep their debt whole, the Eurozone dream alive, and the European Central Bank happy. Both give very different economic and bond outcomes. Their fate however, like in the Potter series, is not just in their hands but that of their friends and adversaries.

So what other spells can the participants in this economic fable use? The Greeks would love to cast the “Evanesco” spell (makes the target vanish). This would involve full economic union and therefore making the Greek debt really disappear – a perfect outcome for Greece, unlike the previous attempt to hide it under the invisibility cloak. The Ministry of Magic, better known in the muggle world as the IMF, would love to use its usual magical curse of “Crucio” (inflicts unbearable pain on the recipient of the curse), insisting the over indulgent borrower amends its ways. Hard for the Greeks to bear, but would have the support of the houses of the north. A third potential conclusion to the tale would involve the casting by the invisible hand of the markets (or as politicians might term it, the death eaters) of the appropriately named “Expulso” (a spell that causes an object to explode), the Greeks leave, or are expelled from the Euro, with the potential disorderly reintroduction of a new national currency by the Greek authorities.

Like in this weekend’s movie, battles and losses lie ahead under all scenarios. We think that the “Expulso” conclusion as touched on previously is the likely final denouement. If it happens, it will be very painful in the short term unlike the other options, but in the long term the natural order of national economic stability would emerge as nation states and markets would set domestically appropriate exchange rates, fiscal and monetary policies, thus allowing the efficient distribution of labour and capital, and hopefully an eventual happy ending.

The European Banking Authority’s bank stress test results are due out on Friday evening. Do the results mean anything or is it one for the talking heads? In our view it is a bit like taking a driving test – you can pass the test and yet still be a terrible driver.

The real test of whether anyone trusts you is whether people are prepared to get in the car with you. So whether or not banks pass the 5% Core Tier 1 stress test hurdle, the real test is whether investors and depositors trust them with their money over the long term, and there’s a long way to go before the European banks rebuild their reputation after a series of offences such as speeding, failing to indicate and poor steering.

Of course any raising of the bar in terms of testing could, in theory at least, reduce the number of accidents on the road going forward. The stress tests will give a degree of disclosure that we haven’t seen before, and it’s no surprise that German banks are reportedly squealing about giving so much information in a transparent standardised format. Even those banks not subject to the stress tests, such as Banca Popolare di Milano and Nationwide Building Society, will be expected by the market to provide the same disclosure, and a refusal will inevitably be seen as a sign of having something to hide, a bit like refusing to be breathalysed.

We also need to see how failures will be dealt with. There’s no point the traffic police simply letting offenders off with a caution and allowing them to stay on the road – they need to be locked up, rehabilitated and prevented from causing future accidents. Several European countries, including France and Italy, still do not have a credible resolution regime for dealing with failing banks, which could make driving in those countries potentially hazardous.

And it’s not just about the banks. There also needs to be major improvement in market infrastructure to make the roads safer for all drivers, such as improved repo and derivative market disclosure and practice, better payment and settlement system risk management and clearer international regulatory and accounting standards.

But ultimately what we need to test is the ability of sovereigns to separate themselves from their banks. Not only have the sovereigns guaranteed the banks, both explicitly and implicitly, but the banks are also funding the sovereigns, so there’s not much point stress testing the banks separately from their governments. After all, nobody has yet come up with a credible plan to recapitalise the Spanish banking sector, other than raising yet more quasi government debt via the FROB and injecting it as equity into the banks, perpetuating the excessive leverage of both banks and sovereign.

Regulators are hoping that proposals to ringfence the banks from the sovereign, such as senior bank debt bail-ins, higher capital requirements, and legal ringfencing of specific activities will break this link. These are all steps in the right direction, albeit slow ones. But until holders of sovereign debt, including the banks, can also be bailed-in and forced to take their share of losses in sovereign restructurings, the symbiotic link between the banks and their sovereigns remains. Until then, the roads remain dangerous, and the question is whether we’re on a Road to Nowhere or the Highway to Hell.

By nature I would say I have a tendency towards pessimism. Hopefully the odd sleepless night is a price worth paying for a successful career in bond investing, however it does leave me worrying (there’s the pessimism) that I could miss out on opportunities when markets sell off. It takes a brave investor to buy when all around are selling. Recent market moves and a book I read at the weekend have brought these thoughts to the front of my mind.

The book, The Most Important Thing, written by Howard Marks (The Chairman of Oaktree Capital, not Mr Nice) argues quite convincingly that being a sceptical contrarian (admittedly with robust credit analysis) is the surest route to long term investment success. It’s an enjoyable read (if you like that kind of thing), well written and thought provoking. One passage in particular stuck with me and left me thinking “what would Howard Marks be thinking at the moment?”. In this passage he simplifies a bear market succinctly into 3 stages;

It feels to me as though we are currently in the third phase and if one were to follow Marks’s reasoning we should be looking to add credit risk in names we like. After all, he would probably point out, things can’t get worse (just as they cannot always get better in a bull market) forever.

Personally I would keep my powder dry for the moment and wait to see what happens in the coming days and weeks. We had a huge sell off in southern European government and financial debt on Monday but UK, US and European Equity indices all fell by no more than 2% – nothing to get excited about in equity terms. At the close of play yesterday the S&P 500 was only 0.5% lower than where it was in June, while the extra yield spread investors are demanding from 10yr Italian government debt over that of Germany is 100bps wider than it was then.

If European policy makers fail to come up with measures to shore things up soon it can only be a matter of time before the equity market heeds the warnings the bond market has been screaming. A significant equity market sell off, if it happens, would no doubt push spreads wider and create more of the opportunities that contrarian investors can wait around for years to pick up.

One section of the European high yield market that has materially under-performed this year is the UK retailer and food producer complex. The rationale is fairly easy to explain: these companies are being squeezed by cost input inflation on one side (cotton, grain, cheese, sofas, whatever it is, it’s more expensive to source) and on the other side, the end customer (the UK consumer) has less money to spend. Result – your sales and profitability suffer and the company’s ability to service its debts deteriorates. The increased credit risk is reflected in higher bond yields. Add to this the fun and games surrounding the European sovereign crisis and it’s easy to see why these names have suffered from the “sell first, ask questions later” knee jerk response of the market when risk appetite wanes.

As I was reclining on my DFS sofa the other day it struck me that these mini non-discriminatory sell-offs often create opportunities. Any good high yield fund manager should always be looking for a bargain, whether he/she is buying a new suit in Matalan or looking to deploy capital in the credit markets. So one question we are grappling with at the moment is this: amongst the beaten up high yield UK retailers and food producers, are there any good deals to be had?

In my view, the answer lies in good old fashioned credit analysis. Looking at each company’s business model. Asking questions like “is this business model viable?” and “are there long term structural issues in the age of online shopping?” Analysing what is driving the top line, what is happening to costs, and crucially for any credit investor, looking at cash flow in this challenging environment and how resilient this cash flow is likely to be in relation to the company’s debt.

If we can find a company that can weather the current storm on the UK high street with its capital structure intact and buy some of their bonds at double digit yields, then this could be a great opportunity.

So now we know that the firewall was indeed an illusion. We had the biggest ever sell off in Portuguese and Irish CDS on Wednesday (and the second biggest sell off in Greece CDS), and now it’s a bloodbath in Italy. Italian 10 year bond yield spreads have widened 25 bps versus Germany to a Euro era record. Long dated Italian government bonds fell as much as 2 points earlier today. Unicredito shares were suspended limit down, as they were exactly two weeks ago.

It now costs Italy 4.6% if it wants to borrow for five years, and 5.3% if it wants to borrow for 10 years. Italy was until recently deemed by the market (not by us) to be the ‘safe’ peripheral country, and a lot of international investors have been overweight Italy versus benchmarks as a proxy against zero holdings in Portugal, Ireland, Greece and Spain. The Italy bulls have put forward arguments such as while the public sector debt/GDP ratio is a worrying 120%, Italy actually has very little private sector debt (a bit like Japan). Or that Italy is too big to fail (it has the third most government debt outstanding in the world at over €1.6 trillion; only Japan and the US have more). Or that Italy has a very big liquid government bond market, with big domestic buyers. Or that its public/debt GDP ratio and its interest burden were much worse in the 1990s and it survived that. Or that Italy’s debt has a long average maturity, meaning that immediate funding costs aren’t too onerous and it can tolerate higher bond yields without seeing its interest burden rise too much (a bit like the UK).

The Italy bears argue that Italy may be seen as too big to fail, but that doesn’t mean that it won’t, it’s too big to bail out. Or Italy’s banks are seeing a slow but steady deterioration in asset quality. Or the deteriorating political situation. The bears’ main worry is how Italy can prevent its high public debt/GDP profile from deteriorating given its appalling growth outlook. Perhaps my favourite Italy statistic is that Italy’s GDP per capita is lower today than it was in 1999, which is remarkable considering the dismal economic performance was during the ‘boom’ years (Zimbabwe and Haiti are two of only a small handful of countries to have fared worse).

But whatever your view is or was, the reality now is that those pesky bond vigilantes have caught sight of Italy, and that is basically all that matters. As Italy or Spain or whoever’s bond prices collapse, the borrowing costs rise. As the borrowing costs rise, the interest costs steadily rise and the fiscal situation deteriorates. This puts pressure on the banking sector, as the tidy chart below from BNP Paribas demonstrates – it’s hardly a novel idea, but reinforces the point that as Italian & Spanish sovereigns come under ever greater stress, senior financial spreads widen in sympathy. As peripheral sovereigns blow out, banks need to raise more and more capital to cushion themselves against the cost of future sovereign restructuring, but this bank capital will get increasingly expensive just at the time that the banks need it most.

And then there’s the credit rating agencies. Rising sovereign and bank borrowing costs will lead to credit rating downgrades. As Jim mentioned in his blog comment on the subject last year here, a major input into the decisions to downgrade seems to be the movement in bond prices. In other words, credit ratings partly get cut because the bond prices fall. To some extent this is rational, since as interest costs rise with higher government bond yields, creditworthiness falls.

And then there’s the credit rating agencies. Rising sovereign and bank borrowing costs will lead to credit rating downgrades. As Jim mentioned in his blog comment on the subject last year here, a major input into the decisions to downgrade seems to be the movement in bond prices. In other words, credit ratings partly get cut because the bond prices fall. To some extent this is rational, since as interest costs rise with higher government bond yields, creditworthiness falls.

Italy doesn’t have the luxury of Japan, where 95% of Japanese sovereign debt is domestically owned. In Italy, despite the talk of strong domestic buyers, the reality is that only half of Italy’s sovereign debt is domestically owned and the international investors are clearly getting very nervous. Trichet yesterday had a pop at the credit rating agencies, but it’s not going to make a difference – when the confidence genie gets out of the bottle, it’s very hard to get it back in again. It’s a classic vicious circle.

The main purpose of the European Central Bank (ECB) is to use orthodox monetary policy with regard to setting money supply and interest rates to achieve price stability. Today, Trichet reiterated this by restating his desire to “create price stability for the 331 million federal citizens of the Eurozone.” In order to do that, the ECB believes that a combination of controlling money supply and interest rates is paramount.

Unfortunately, as discussed previously, money supply and interest rates are no longer the same in each sovereign state (previous blog). Money is departing the weaker states towards the stronger states, while interest rates for the private and public sector have diverged between nations. This is best illustrated below by the huge discrepancy in short term interest rates different governments face.

The ECB believes that money supply and interest rates matter. If countries experience money supply outflows and high rates, as citizens desert their nations financially (i.e. the small sovereign periphery) then presumably severe deflation and recession are to follow automatically. However, the larger core should experience the opposite problem in a mild way. The ECB and governments are attempting to limit this effect via monetary and fiscal means, though the fact remains they are reducing the size of this problem, and are nowhere near eliminating it.

This means the Eurozone is a Eurozone in name only, one currency, hugely divergent sovereign monetary systems and economic outlooks. The effects of this tightening on the peripheral Eurozone countries has scarily not been felt yet as it usually takes 18 months for monetary policy effects to come through. If you think the periphery is weak now, well according to the monetary orthodox you ain’t seen nothing yet.

As a direct consequence of Moody’s downgrade of Portugal to sub investment grade, now Ba2 to be precise, Portuguese corporate bonds will be removed at month end from Bank of America Merrill Lynch’s (BofAML) main investment grade and high yield indices. This is because the main BofAML indices require the sovereign to have an investment grade rating. (It also looks as if Portuguese corporates will be thrown out of the iBoxx indices, although we don’t have confirmation on this yet). This will affect bonds issued by the likes of Portugal Telecom (PT) and Energias de Portugal (EDP – the electric utility) despite their current investment grade ratings. Those bonds are set to enter the BofAML Global Emerging Markets Credit indices.

Whilst some index focussed investors will be permitted to hold off -index positions, many will be forced to sell out over time, putting further upward pressure on bond yields. Since the start of the year, yields on EDP and PT 8 & 9 year bonds have risen by almost 2% to 7.5% & 8.75% currently.

Given the size of the Portuguese economy its corporates have historically constituted a small portion of broader Euro corporate indices (the same can be said for Greece and Ireland). As of yesterday’s close, Portuguese corporates comprised only 1.1% of the BofAML EMU Corporate Index. However, given the larger size of the Spanish and Italian economies it isn’t surprising to see their corporate bonds form a significant 14% of the index. And whilst Spanish & Italian government bonds currently remain firmly in IG territory, further downward pressure on those sovereign ratings will undoubtedly leave investors in peripheral European credit increasingly nervous.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.