Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

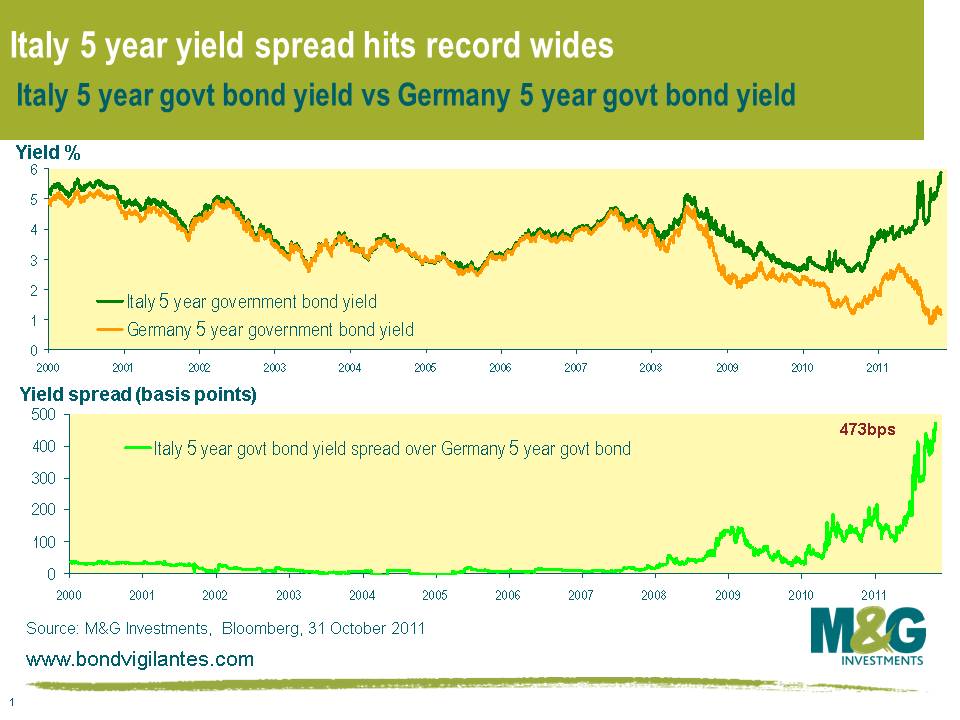

Today we had one of the biggest ever days of peripheral sovereign bond buying from the SMP (Securities Market Programme), with some banks estimating that over €5bn of peripheral sovereign bonds were purchased via the ECB’s bond buying program in an effort to keep a lid on peripheral sovereign bond yields. About two thirds of these purchases were directed towards Italian government bonds, and Italy spreads still ballooned out to Euro era wides. The top chart shows the absolute yield levels of Italian and German 5 year government bonds, and the bottom chart shows the difference in the yields, or the yield spread.

Not great news.

It’s that time of year when the tradition of All Saints’ Day gets blurred with modern commercialism. It is the turning of something scary into something fun, which has become an excuse for children to be rewarded for dressing up and behaving poorly.

In the more grown up world, this quarter’s banking results have been poor and are also dressed up. What’s lurking under the costume?

The oddest thing about this quarter’s bank results is how they turn bad into good by the method in which the banks account for bad news. The banks have for a number of quarters been applying the following make-up to their balance sheets. When their credit quality deteriorates, the value of their debt falls. This looks bad. It reflects their inability to finance and directly affects the future costs of the business when they come to refinance their debt. However, the banks are allowed to take this loss that has been suffered by their bond holders and book it as a profit. You therefore get the oddity that as the outlook for the bank deteriorates, its credit spreads widen, and it is able to book the spread widening on its own debt as a profit.

This has been very significant in the last quarter by a multitude of banks, typified for example by Morgan Stanley, which made $1.14 per share, but with $1.12 per share coming from a widening of its own credit spreads.

In their defence, the banks can argue that they have made a gain because they have sold debt to bond holders who have made a loss. Indeed, if they could buy back the debt at these lower levels they would crystallise the gain. They would also argue they account both ways. So when spreads fall, their profits are reduced.

However, this accounting treatment generally works in their favour. Firstly it makes their profits look less cyclical by increasing them in the bad times and reducing them in the good times – a handy tool for management. Secondly, by definition banks can only issue debt when perceived as a good credit and so are more likely to experience gains from write downs as opposed to losses from an improving credit profile.

The banks and their auditors think this accounting use is sound. We, however, wonder how correct it is. Presumably, using their logic, the accountants and management of Lehman Brothers would argue that the quarter it went bust was its most profitable ever because its debt traded at and near to zero. In fact, that last quarter of trading could well have earned more for the company than its previous 100 plus years of existence. Trick or treat.

Current plans are for Greek restructuring to be ‘voluntary’, which means that it would fail to trigger CDS. CDS is supposed to be the cost of insuring against default. If Greek restructuring fails to trigger CDS, then CDS would lose its credibility as an effective hedging instrument against sovereign default. Such actions would have absolutely huge implications as all the banks who have used CDS to buy protection against their sovereign debt, and have consequently reported very little net Eurozone peripheral sovereign debt exposure, in fact have much more exposure than everyone thinks.

So who’s in trouble? Unfortunately, nobody really knows since a major problem with CDS is disclosure. It’s very difficult to figure out who has bought protection on a sovereign and who has written protection. As we wrote here, BIS (The Bank for International Settlements) data from earlier this year suggested that the US banks were large writers of protection and the European banks big buyers of protection. However the US banks in their results presentations claimed to have only small net exposures.

It’s a reasonably safe assumption, however, that on the whole European banks in core European countries would have been net buyers of protection (or at the very least large users of protection) as they will be the ones with a need to hedge exposure. Indeed, in July Deutsche Bank reported that it cut its net Italian sovereign exposure from €8bn at the end of 2010 to €997m by the start of July and had hedged Italian exposure in its trading book by using CDS. UBS this week announced €14bn gross exposure but a €9bn net exposure to sovereign bonds issued by Portugal, Ireland, Italy, Greece, Spain and Belgium.

So the guys most at risk of sovereign CDS losing its credibility as a hedge are in all likelihood the large European banks. It’s the last thing these banks need right now. What will be really interesting is whether or not the banks’ use of sovereign CDS as an effective hedge in accounting definitions remains allowable now that politicians have made a default without a credit event possible. And of course the EFSF/Eurozone rescue is also in trouble if CDS isn’t an effective hedge, since the EFSF is going to attempt to sell protection on new issues of sovereign bonds in order to get their new issue spreads down!

Travelling through Switzerland I can’t help but think that politicians both here and in the UK have a lot to thank their predecessors/electorates for. The relative safe-haven status enjoyed by both economies reflects, at least in part, the arm’s length relationship with the euro. (Swiss readers may not take kindly to being compared with us Brits, but you take my point.)

The eurozone policy makers who are currently trying to thrash out some sort of ‘deal’ have an almost impossible task on their hands. Despite a belated recognition that some leadership is much required, the reality is that a comprehensive solution won’t be reached. We’ve talked before (see here) about the inherent dangers in any monetary union absent fiscal union. Are the French, Italians, the Spanish, even the Greeks ready to be governed by Berlin? Or indeed, if Greece et al are willing to give up all sovereignty, are the Germans willing to take responsibility for the deficit countries of Southern Europe? Fiscal union requires both the debtors and creditors to be compliant. The foundations of the building are unsafe; replacing the roof may help keep the rain out but it won’t ultimately stop the house collapsing.

Absent fiscal union and two outcomes spring to my mind; euro breakup (of some form) or the monetisation of deficits. The former would likely see a return to 1930s depression economics, the latter some would argue risks a rerun of the 1920s Weimar experience. While we’re certainly not predicting a rerun of 1920s hyperinflation, it will be the temptation to inflate that will win out. The structural adjustments required of many European economies will likely prove too big a pill to swallow. German led protests will fall on deaf ears, and German resignations from the ECB will make little difference. Inflating away liabilities will prove an easier sell for economies that have binged on debt and leverage for decades.

Time to visit some inflation protection? Given there is so little inflation priced into bond markets right now, I think so!

Bernanke is clear about why the Fed has embarked on “Operation Twist” – the Federal Reserve has both greatly increased its holdings of longer-term Treasury securities and broadened its portfolio to include agency debt and agency mortgage-backed securities. Its goal in doing so was to provide additional monetary accommodation by putting downward pressure on longer-term Treasury and agency yields while inducing investors to shift their portfolios toward alternative assets such as corporate bonds and equities. Bernanke wants investors to take more risk. He would be much happier if there wasn’t so much cash sitting on the sidelines. Certainly, negative real cash rates will entice investors to search for higher yielding assets.

Looking at US M2 money supply, an increase of 10.1% over the year to September 2011 should be a cause for concern. A higher rate of money supply growth has occurred on only five occasions since 1984 (including last month). The Fed thinks this is because institutional investors, concerned about exposures of money funds to European financial institutions, shifted from prime money funds to bank deposits, and money fund managers accumulated sizable bank deposits in anticipation of potentially large redemptions by investors. In addition, retail investors evidently placed redemptions from equity and bond mutual funds into bank deposits and retail money market funds.

We have always been told that “inflation is always and everywhere a monetary phenomenon”. According to economic theory, an excessive expansion of the money supply should be inflationary. Arguably, the current expansion in money supply is not inflationary because banks are not lending. Or are they?

Looking at the Fed’s survey on bank lending practices, banks have been loosening lending standards since the third quarter of 2008. The ability of large and medium sized firms to access credit has improved dramatically over the past couple of years. Banks have also reported a loosening in lending standards for credit card loans as well. With the lending standard survey due to be updated at the end of this month, we are keeping a close eye on this indicator. Banks may have reacted to the events of recent months by tightening lending standards again, exactly at a time when the US economy is flirting with recession. On the other hand, ultra-easy monetary policy may result in the banks easing loan standards further in a search for profits.

Some economists believe excess growth in money supply suggests asset price inflation and consumer price inflation. Others believe the increase is a deflationary signal in the short-term as it likely reflects a flight to safety and low expected asset returns. I have some sympathy for this view as the last time year-over-year growth in demand deposits was at current levels the US economy was in a deep recession. The bottom line is, no one knows what impacts extraordinary loose monetary policy is having on the real economy. With so much confusion going on, the only thing that is clear is that central bankers have their work cut out for them in trying to understand this mess. Now we know why economics is the only field in which two people can share a Nobel Prize for saying opposing things.

We’ve already discussed how EFSF doesn’t work as a private sector solution to the Eurozone debt crisis here, and have explained how the idea of turning the EFSF into a monoline insurer is ludicrous here. EFSF bonds continue to perform poorly – the inaugural €5bn 5 year EFSF bond issued in January came with a yield spread of about 40 basis points over 5 year German government bonds, and is today at 150 basis points.

However perhaps more worrying than the poor performance of EFSF bonds is the dire performance of French government bonds, particularly in the last couple of weeks. French spread widening poses a major problem because the tail tends to wag the dog when it comes to credit ratings, as argued here. In other words, widening spreads tend to cause credit rating downgrades, which tend to cause further spread widening. A French downgrade would be particularly problematic to the European leaders who still seem to believe that the EFSF is a tenable solution to the Eurozone debt crisis since the EFSF structure needs AAA rated guarantors. To quote FT Alphaville, the loss of France’s AAA rating would lead to the EFSF beast beginning to eat itself.

The chart below shows how long dated French government bonds have significantly underperformed long dated Germany, with spreads blowing out from 70 basis points in mid September to 124 basis points this morning. More worrying still is that the French spread widening has not come about because Germany borrowing costs have plummeted – long dated Germany bond yields are at a similar level now versus where they were in mid September – but has instead come about because 30 year French government bond yields have jumped from a mid September low of 3.3% to above 4.0% today.

Earlier this month the Nobel Prize for Economics went to Sargent and Sims for their work on cause and effect in macro economic policy. All good stuff of course, but it pains us that nobody is looking at the more micro-economic problems of the modern economy – in particular, WHAT KIND OF WORLD IS IT WHERE YOU ONLY GET EIGHT MONSTER MUNCH IN A PACKET?

We have discussed food price inflation in previous blogs and seen how UK supermarkets were able to raise prices and outperform their European peers who had cut prices in periods where commodity prices fell. So when Stefan Isaacs casually commented that Monster Munch appeared to have shrunk in size from when he was a kid, it was time for the kind of quantitative research that modern economists appear so reluctant to perform. Off to the M&G tuck shop we went…

10 monster feet, 10 monster feet, 8 monster feet. Plus some toes. We ran our model and calculated this was an average of 9.33 whole monster feet per packet. It made us wonder – have Monster Munch shrunk? Unfortunately, due to a change in ownership, Monster Munch’s holding company couldn’t provide me with any statistical information. However due to the popularity of this snack to many an 80’s child there is an on-line cult following with numerous people blogging about their experience of the product. So with a little searching it was found that a Monster Munch retailed for around 5-10 pence in 1977 when Monster Munch was launched as “The Biggest Snack Pennies Can Buy”, weighing in at 26g. The bag purchased in our canteen a couple of days ago was 45 pence for a smaller bag of 22g.

How does this compare with both food price inflation, and with the price of maize (the biggest ingredient)? Although the price of Monster Munch is soaring above normal food price inflation the price increases are broadly in line with the price of maize. We’ve plotted two lines though – one just based on the price of a standard size packet of Monster Munch, and one reflecting both that price and the inflation hidden by the shrinkage of the packet. You can see that the “hidden” inflation resulting from a 15% reduction in the packet size. This makes an additional large difference to Monster Munch inflation.

This shrinking of food packaging is something very well known to the Japanese, where despite deflation in the headline numbers for years, the price of instant noodles remained the same – but the size of the plastic tub has been falling year after year. And nearer to home, doing a bit of googling, we found articles referring to a 12.5% fall in the size of Häagen-Dazs ice cream tubs, and a 9% reduction in Scott toilet rolls.

So to address the complaints of our team member, yes you are both getting less snack for your money and it is costing you more.

I was reminded today of the tongue-in-cheek chart that we put on this blog a year ago showing the close correlation between sovereign 5 year CDS (i.e. the cost of insuring governments against default) and the percentage of men aged 25-34 who still live with their parents within the Eurozone founder member countries (credit to JP Morgan). This was a prompt to do an update, and the outperformance of both Ireland vs Portugal and Spain vs Italy over the last year has helped improve the correlation further.

The comment left on last year’s blog is of course totally accurate though, i.e. beware mixing up correlation and causation. And for our British readers, the UK fares OK but not wonderfully on this measure, with 20% of men aged 25-34 still living with their folks (see here for full EU list, data as at 2008). I get a feeling this ratio is going to be rising quite a bit over the coming years.

As an aside and looking at what I wrote last year, it’s interesting to note that France CDS does now indeed trade wider than Colombia, although Colombia has since been upgraded to investment grade. Next stop for (currently) AAA-rated France is BB rated Philippines. Philippines 5y CDS is currently about 5bps wider than France, and hit a high of 870bps three years ago.

There has been a lot of press coverage about the proposal to turn the existing EFSF (European Financial Stability Facility) into a monoline insurer of sovereign debt, where the new structure would be called the European Sovereign Insurance Mechanism (ESIM).

How is the ESIM supposed to work in theory? No concrete details have been announced, but the basic thrust of the proposal is that the EFSF (and subsequently the ESM) acts as a sovereign bond insurer for new funding and exchange offers. Investors, comforted by the ESIM taking the first 40% of losses in the event of any restructuring, would then be willing to again buy new Greek, Portuguese and Irish debt, or (more likely) exchange their existing bonds into new insured bonds at a level somewhere between current market prices and par. In the very optimistic scenario that a lower insurance coverage (25%) would be required by investors for Spain and Italy, Allianz estimates that the EFSF’s leverage on its existing €440bn commitment could apparently be increased to 3.7x.

That’s the theory, but why does the ESIM not work in practice?

Firstly, conceptually, the idea of bond insurance obviously has a somewhat tarnished track record in recent years (the monolines, Fannie/Freddie, AIG etc all come to mind) and the fundamental problem will be persuading investors that they would ever be able to call on the insurance policy provided by the EFSF/ESIM/ESM when they actually need to.

As with monoline wrapped bonds, investors must be comfortable with the underlying obligor from the start, rather than counting on an insurance policy from a Luxembourg domiciled private company (the EFSF) whose mandate and strategy keep changing, which may or may not exist in its current form after the introduction of the ESM in 2012/2013 (and if it does still exist may well be explicitly subordinated to the ESM and other multilateral creditors), and which itself has very little cash but will have to go to each of the member states to claim under its own guarantee policies.

Claiming under any financial insurance policy is never easy, particularly when investors in this case are likely to be very fragmented and with differing incentives. Bond documentation (and more specifically the articles of association of the EFSF to which it refers) could easily be changed on a political whim, and it is highly unlikely that the documentation would explicitly give investors any practically actionable rights over either the EFSF/ESIM or its guarantors.

There’s also the problem of correlation. The risks of the underlying obligor and the guarantor (and the ultimate sovereign guarantors) defaulting at the same time are highly correlated. Investors are hardly likely to trust that Spain will be willing or able to honour its guarantees to the EFSF in a scenario where Italy defaults, for example.

Getting into the mechanics of the ESIM, setting the required insurance level at what will surely be the outset of a long period of necessary sovereign restructuring is fraught with problems (a bit like buying buildings insurance without having your home valued). Will a share of 40% insurance turn out to be enough of a haircut for Greece, when long dated Greek bonds are already trading at 30 cents in the euro, i.e. implying a 70% writedown? And will 25% be enough for Italy? Given the lack of concrete details it is impossible to verify the calculations or assumptions behind the leverage numbers stated (particularly given that the proposal set out by Allianz is not necessarily a first loss piece, as reported in the press, but potentially a second loss or shared vertical slice).

Allianz argues that the EFSF/ESIM/ESM would be a powerful controlling creditor, with the ability to enforce restructuring on programme countries and the ability to monitor progress against budget targets etc. However, this in itself is an alarming proposition to those who remember the ways the monolines abused their positions as controlling creditors in wrapped transactions. Investors could easily find their entire exposure subordinated in practice to the wishes or votes of the EFSF and/or its largest guarantors such as Germany.

The creation of a new class of partially insured debt for each country would mean several tiers of sovereign debt circulating simultaneously (while the rump of existing bonds runs off), making subsequent restructurings very complex.

Finally, the main supposed benefit of ESIM is the strap line that it doesn’t require any cash to fund. However, this is also its weakness, in that it will still lack the fire-power to deal with a liquidity problem experienced by an individual sovereign. If investors refuse to buy a sovereign’s bonds for any reason (as they have recently) even with a partial loss share arrangement, then it will still require intervention by the ECB or possibly the IMF, who have access to cash to step in and provide the liquidity to refinance maturing issues. Under proposed EU sovereign debt harmonisation proposals, however, the ECB will be able to play a full voting role as a creditor in any subsequent restructuring, meaning that existing investors can in that scenario expect to find themselves outvoted by the rescue liquidity provider, whose own incentives will be to minimise losses to the ECB’s own largest controlling shareholders (starting with Germany).

So the idea that a sovereign insurance policy provided by the very same (or, at best, ‘related’) group of stressed sovereigns would provide “reassurance to the market” seems a ludicrous one. If markets believe that this proposal is a solution to the Eurozone sovereign debt crisis then there is room for disappointment.

We heard yesterday that Fitch has followed Moody’s lead and begun downgrading UK banks’ credit ratings. This reflects the reduced level of support offered by the government. Fitch only actually downgraded Lloyds and RBS – both to A – but Moody’s went further last week, downgrading a total of 12 banks and building societies. These new ratings have not entirely removed the implied tax payer support – only an element of it.

Using Moody’s data, if we remove the implied support provided by the government, the ratings of the big 4 UK banks would look like this:

| HSBC | Aa2 (current rating) | A3 (no support assumed) |

| RBS | A2 | Baa2 |

| Lloyds | A1 | Baa1 |

| Barclays | Aa3 | A |

Within the building society sector, five of the eight firms that were downgraded are now sub-investment grade.

Banks are already finding it hard to finance themselves and any negative noise coming out of rating agencies obviously isn’t going to help lower the yields at which they can borrow. As the cost of issuing senior unsecured debt rises (the lower tier two primary market is effectively shut), the incentive for institutions to issue secured debt and asset-backed securities increases. This would likely put further pressure on senior unsecured bank bonds. Lenders in the senior unsecured part of the capital structure would become more subordinated, with a claim on fewer assets in the event of a workout.

Government support has diminished, rating agencies have predictably reacted negatively, and the banks will continue to face funding pressures. It’s unlikely that we see a light at the end of the tunnel any time soon.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.