Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

We recently published an in-depth note on the high yield market . In it we consider some of the issues facing investors in the era of negative real interest rates and financial repression and how high yield as an asset class fits into the current paradigm.

Our main conclusions are:

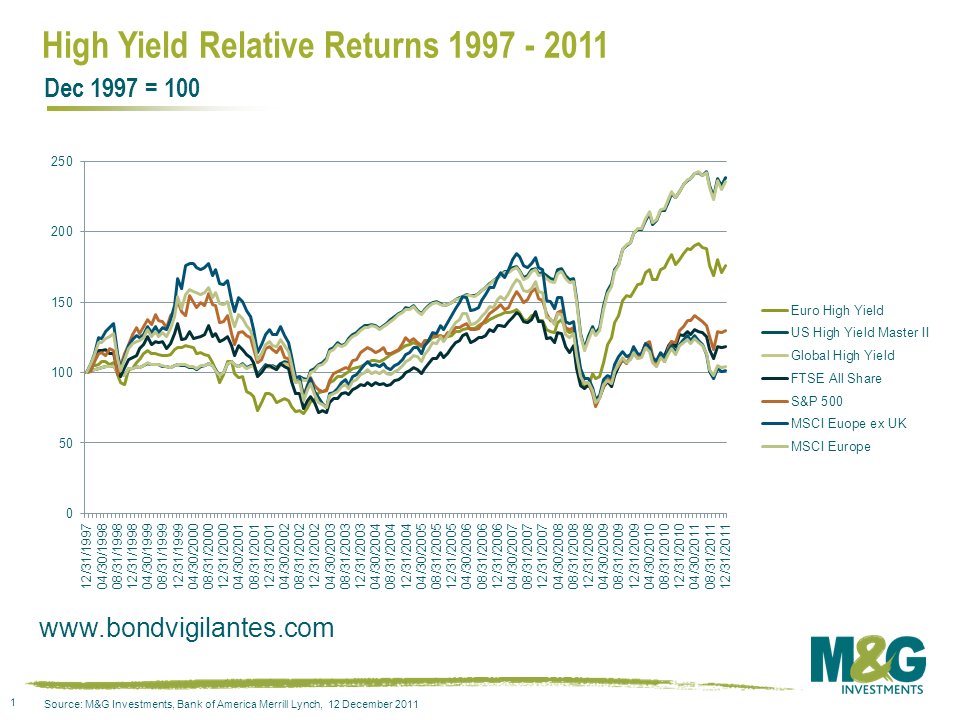

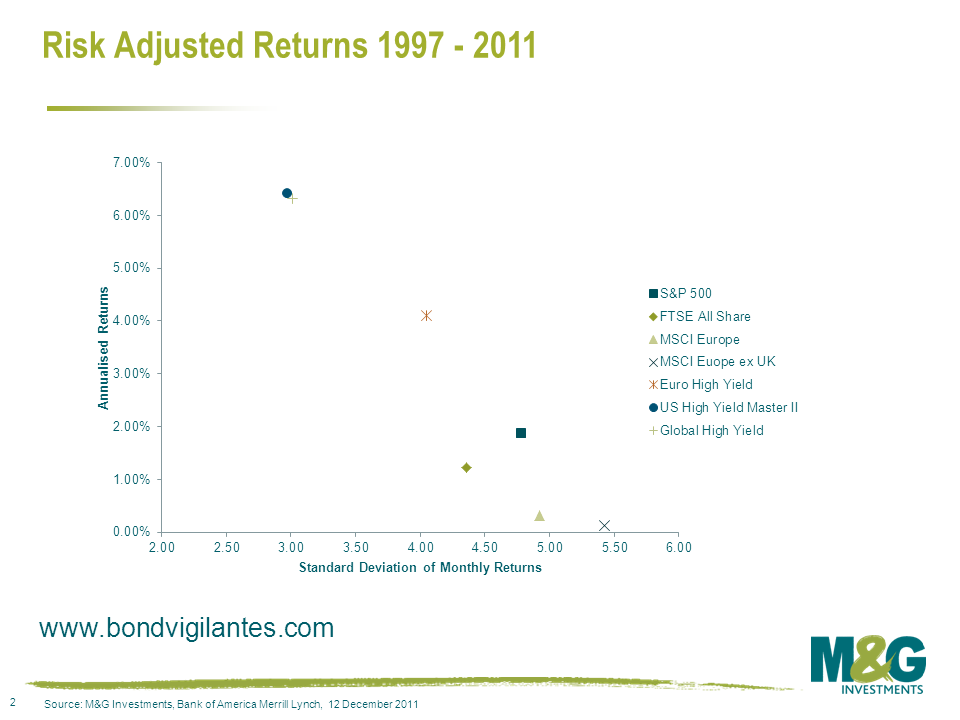

We also looked at the high yield market in terms of current valuations and potential returns after a period of strong relative performance over the past few years (see chart below).

It was announced this morning that the UK economy grew just +0.5% in 2011, a downward revision from +0.7% previously announced. As the chart below from Citi illustrates, the UK economy has stalled. UK real GDP is 4.1% below its pre recession peak, which makes this ‘recovery’ worse than the Great Depression.

The UK’s experience of the past few years is also considerably worse than Japan’s experience in the aftermath of its bubble. Looking back, Japan’s decade doesn’t look all that ‘lost’ in comparison – Japan’s real GDP in 1991 was +2.6%, -0.1% in 1993, +0.9% in 1994 and +2.5% in 1995, and Japan’s average annual real growth rate through the 1990s was +1.2%. It’s also worth pointing out that for all the talk of austerity in the UK, the reality is that government expenditure actually increased by 0.1% in real terms last year. Austerity hasn’t really started yet.

Sterling is the fourth worst performing currency in the world so far today, down 0.5% versus the euro and down 0.3% versus the US dollar. A continuation of abysmal UK growth should result in sterling appearing more regularly towards the bottom end of the currency tables than the top.

Central banking has evolved substantially in recent decades. Part of this evolution has involved a move towards greater transparency around a central bank’s forecasts and operations. The reason for this shift is because it is believed by many economists that by having a central bank communicate its objectives and forecasts, economic agents like consumers and businesses will make better informed decisions and allocate resources more efficiently. Theoretically, the real economy should improve.

The problem is, economic forecasting is a difficult game to be in. Many private sector economists have had a torrid time over the past five years in attempting to assess the state of the real economies of the US, Europe and the UK. If you think that central bankers have had it any easier, then you would be wrong. Time and time again, central bankers have been proven wrong with their economic forecasts.

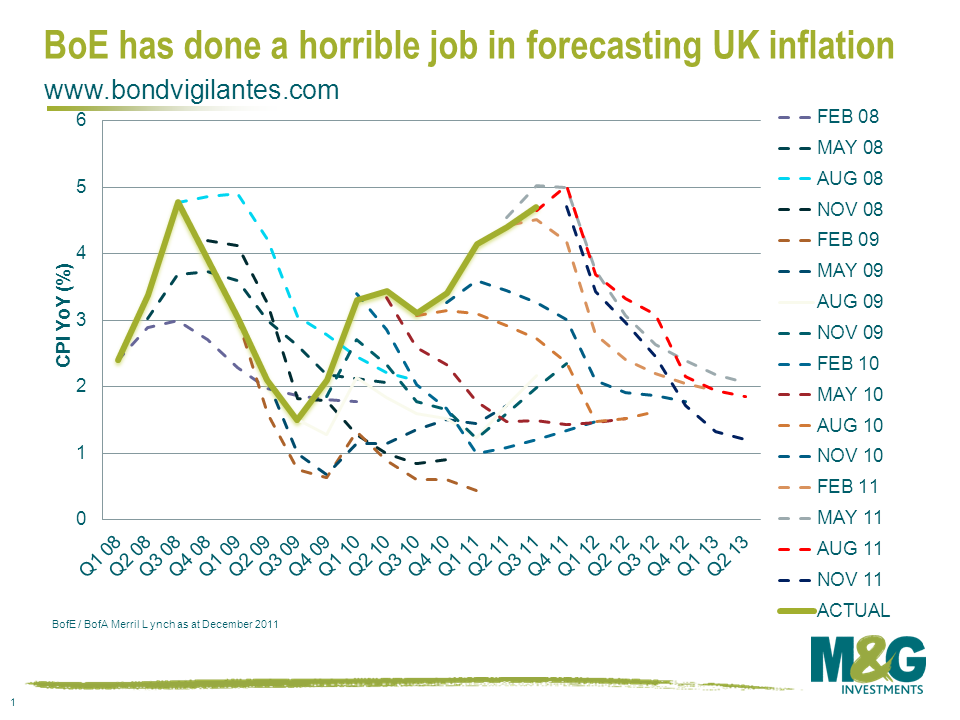

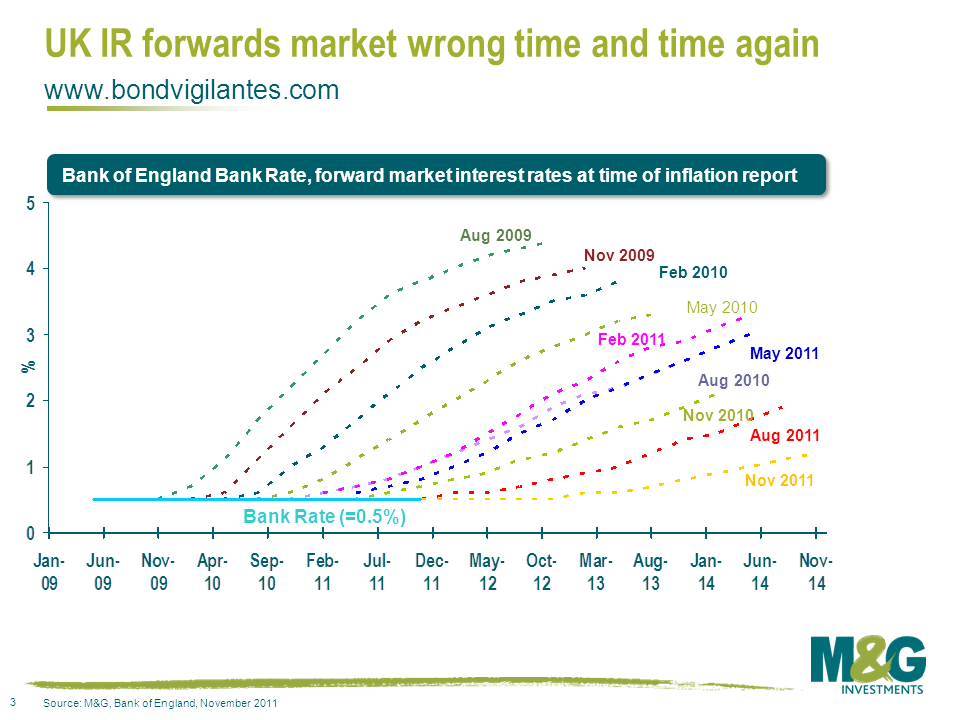

For example, the following chart (courtesy of John Wraith at Bank of America Merrill Lynch) highlights the dismal inflation forecasting record of the Bank of England. It shows actual inflation versus the BoE’s forecasts from the quarterly inflation report. Time and time again over the past couple of years the BoE has forecast lower inflation, and time and time again it has been wrong. This is worrying if you are an inflation targeting central bank.

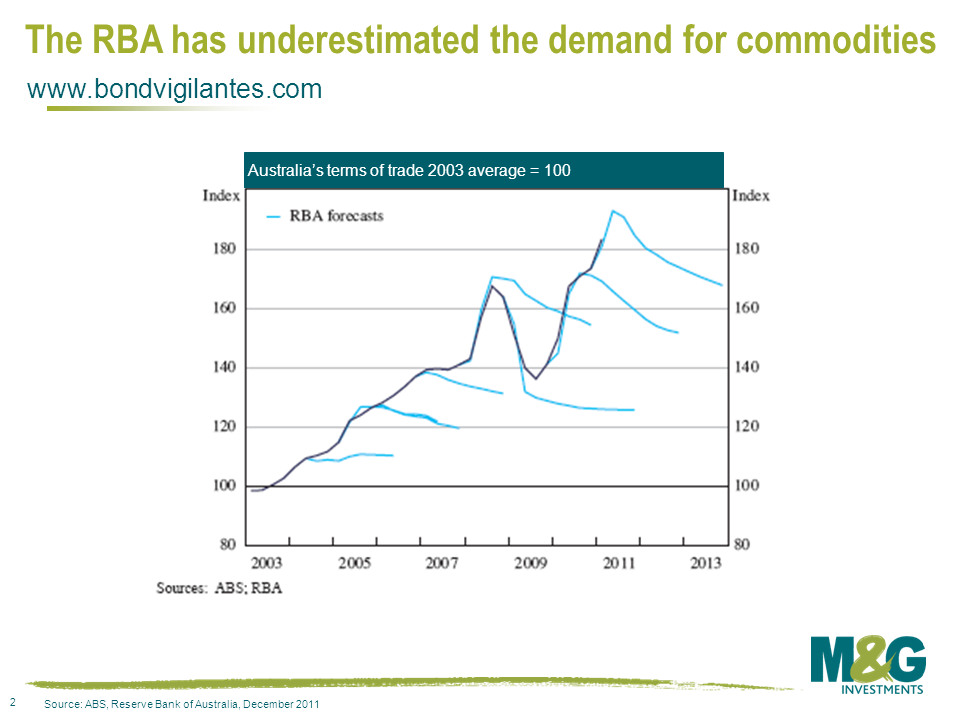

This poor record of forecasting is not limited to the Bank of England. The chart below shows the record of the Reserve Bank of Australia in forecasting Australia’s terms of trade. As you can see, the RBA’s forecast of a fall in the terms of trade has repeatedly been proven wrong, largely caused by the boom in China and its appetite for Australian commodities. The RBA should be right on top of developments in resources markets – and it probably is – but this has not helped the RBA in determining the future course of Australia’s terms of trade.

The charts above highlight how two central banks, the BoE and RBA, can be totally inaccurate in forecasting major economic variables. Of course, there are many more examples of central banks providing inaccurate forecasts including this amusing lowlights package of Ben Bernanke.

Of course, markets have shown that this poor forecasting record is not limited to public institutions. The forward market for interest rates has repeatedly priced in interest rate hikes and has continually been disappointed by the Bank of England’s lack of action (in fact, the BoE has done the opposite to hiking rates and pumped the economy with further QE).

Let’s turn now to the US Federal Reserve. In January 2012, the Federal Open Market Committee (FOMC) took the extraordinary position of indicating that interest rates will be at exceptionally low levels until late 2014. The markets have read this as an assurance that interest rates are on hold until that time. But I am not so sure.

From the January monetary policy release – “In particular, the Committee decided today to keep the target range for the federal funds rate at 0 to 1/4 percent and currently anticipates that economic conditions–including low rates of resource utilization and a subdued outlook for inflation over the medium run–are likely to warrant exceptionally low levels for the federal funds rate at least through late 2014”.

I have underlined the most important part of this statement. The FOMC’s forecast that interest rates will remain low or on hold until late 2014 is based on the FOMC’s forecasts of US economic conditions, in particular resource utilisation and inflation over the medium run. And as we have seen above, these forecasts are frequently plain wrong.

We won’t be surprised to see the Fed hike rates before late 2014. And that is because central banks are terrible forecasters of economic variables, just like the rest of us. If we start to see a real improvement in the fortunes of the US economy (and there is already evidence of this occurring) and inflation expectations start to rise, then the Fed will face a substantial dilemma. Will Bernanke and company hike rates in order to maintain inflation fighting credibility, or will they maintain ultra-low interest rates in order to support the real economy? Should they fail to act in an environment of higher inflation outcomes, we will have the clearest indicator yet that the financial crisis has caused central banks to have a re-think about the goals of monetary policy.

Over the last few weeks we have witnessed a meaningful bounce in inflation breakevens in the UK, Europe and the US. When breakevens are rising, it is a signal that the fixed income market is anticipating higher inflation than has been priced in. It also means that index linked bonds are outperforming conventional bonds. In the UK, the linker gilt of 2016 has outperformed the conventional gilt by 45 to 50 basis points in yield terms since the start of this year.

Why have the bond markets started to price in higher levels of inflation?

Perhaps there is an element of geo-political risk affecting the oil price, which feeds into the inflation baskets in a plethora of forms? Yes, but I don’t think oil is the major culprit here, although in the US, where oil is taxed far less than in the UK or Europe, inflation is far more sensitive to changes in the oil price. See Jim’s blog here.

Perhaps rising breakevens owe to fears around money creation? In Europe, at the end of 2011 the interbank market was completely disfunctional, and we were entering a deflationary spiral. But the long term repurchase operations (LTRO) have added somewhere in the region of €1 trillion euros to banks over the last few months, the interbank market has been showing signs of being slightly less disfunctional, and the risks of deflation feel for the moment substantially reduced. In the UK, the mechanism of quantitative easing boosted the prices of conventional gilts more than index linked gilts, as the Bank of England did not purchase linkers directly. This artificially suppressed the relationship between the conventional gilt and the linker (the breakeven), at exactly the moment when money creation ought, in my opinion, to have seen higher inflation risk premia priced in. The strong performance of index linked gilts in the UK either owes to a fear that improved economic data means we are closer to the end of QE than the beginning, so the artificial source of demand for gilts is not going to be in the market for much longer (a relative call), or owes to the market’s deciding that we are not going into a disinflationary or deflationary economy, and are more likely to see on target inflation or higher.

It is worth thinking about the levels of 5 year breakevens in the chart, a relative valuation measure. In the UK the bond market is expecting inflation to average 2.8% a year for the next five years. Remember though that this is RPI inflation, which historically has averaged 0.8% more than CPI. If we assume this historical relationship holds, then this 5 year breakeven implies CPI will be bang on the Bank’s target of 2%. So on this basis the breakeven does not make inflation protection look expensive at all. Considering the 5 year breakeven in Europe, which is currently 1.6%, this is still pricing in inflation being below the 1.8% (ish) target on average for the next 5 years. With aggressive money creation (at last!), surely the risks are skewed to the upside? In fact, only the US market is pricing in inflation to be above target for the next 5 years. I think that this is the correct side of the inflation target for linkers to be valued at, and I believe there is a good chance the UK and European markets start to move towards this US dynamic.

Why? Firstly because of the ultra low interest rates and ultra accommodative monetary stance at the ECB, BoE and Fed. And also because of the large scale money creation we have seen in all three markets and have discussed briefly above. But most importantly to me is the fact that at this moment in time, the three central banks in question all have a clear and visible inflationary bias. They would rather have inflation than deflation (rightly). But now they are showing a propensity to favour above-target inflation over below-target inflation. This is tantamount to a (temporary or permanent, we do not yet know) change in the inflation targets. And this must, in my opinion, see higher inflation risk premia. How do we show this clear inflationary bias? Inflation is significantly above target in all three economies, and yet policy is not only not being tightened, the taps are still very much on!

1993 was a golden year for US Treasury investors, with 10 year yields falling from 6.7% at the start of the year to 5.3% by its end. It felt like nothing could go wrong – and inflation had even fallen throughout the year from 3.3% to 2.7%. Yet on 4th February 1994, the Fed hiked rates by 0.25%. And they hiked again in March, by 0.5% in May and August, and a further 0.25% in November. The annual inflation rate was still actually falling until May 1994, when it hit 2.3%, and on a monthly basis in January, just before the shock hike, inflation was 0%! Yet the Fed was right – there were some price pressures in the economy and these became visible in the third quarter of 1994. Their trigger was a significant improvement in economic growth. At the start of 1993 the economy was growing at under 1% on an annualised rate, but this had dramatically improved to over 5% by year end. By early 1995 though it was back below 1% after the series of aggressive rate hikes – a result that perhaps led the Fed to be much more gradualist in future expansions?

The reason we are interested in 1993-94 is that the price action in Treasuries back then looks very similar in scale and direction to what we saw in gilts and other markets in 2011. The 10 year gilt yield fell from nearly 3.5% to below 2% in a year. Since the start of this year yields have started to rise again, with big moves in the last 3 days. It’s a similar pattern to 1994 but with one big difference – there’s no way that Central Banks are going to hike rates this year is there? And that alone makes a sell off on 1994’s scale unlikely.

A couple of last points though – firstly the US Fed has said that economic conditions “are likely to warrant exceptionally low levels for the federal funds rate at least through late 2014”. But note that this is not an explicit promise, but is totally contingent on the economic activity. And also note that the market no longer believes that “late 2014” is when rates will rise – the market is now pricing in a Fed rate hike in 2013, and for rates to be around 75 bps higher by the late 2014 Fed expected first hike.

And secondly, I have also marked on the chart the date when Walt Disney famously issued a 100 year $ bond, just months before the massive bear market began. I’ve also marked George Osborne’s announcement of the potential 100 year gilt in the UK this week. The Circle of Life? When You Wish Upon a Star?

For those clients who received our Panoramic fixed interest newsletter in December (the latest edition is out now by the way, with a detailed analysis of the global high yield market), you will have seen that I talked about Central Bank Regime Change as one of the key issues for fixed interest investors in the coming years. What I meant by Central Bank Regime Change is this: the days of Central Banks caring too much about inflation are behind us. We’ve had three decades since Paul Volker took over at the Fed and set interest rates above the rate of inflation (a novelty at the time), and we’ve had independence granted to the Bank of England, and seen inflation targets of 2% become commonplace. From here on in though, Central Banks will care about two things – unemployment and debt.

Charles Evans of the Chicago Fed is the only person who will publicly say it (admitting you don’t care about inflation anymore isn’t such good news for your government bond markets), but getting the unemployment rate down aggressively must be the priority for the authorities, otherwise we are doomed to structurally low growth and social unrest. If this means inflation overshoots that 2% level, he is relatively relaxed about that (3% would be very acceptable). And an inflation overshoot helps the developed world’s other big problem – debt. There are three ways to shrink an excessive debt burden. You can grow your way out of it (but with broken banks, austerity and high unemployment, below trend rather than above trend growth looks more likely – look at Greece). You can default on state liabilities to your populations (this is happening) or to your bondholders (less likely for regimes with their own currencies). Or you can set negative real interest rates and erode the debt burden through stealth inflation.

And this is the regime under which we are operating. The IMF put together part of the chart below – I’ve added the most recent period post the Great Financial Crisis. You can see that before the Second World War there was a wide range of real interest rates in the UK, with little pattern. For much of the period the UK was on the Gold Standard with fixed exchange rates. The period also includes the Great Depression where we experienced deflation. After the Second World War the UK emerged with a Debt/GDP ratio of over 200%. You can see that most of the next three decades was spent in low real rate environments, with periods of negative real rates. With financial repression making UK banks hold gilts, and some modest growth, the debt burden was aggressively eroded. The Volker years show a step change in real interest rates to sharply positive rates.

The final normal distribution curve shows the world we live in now. Since 2008 real rates have been sharply negative (justifying the unusual negative real yields on virtually all inflation linked bonds). Remember that no person in authority will ever be able to admit to regime change, but all of us have to understand it’s happening. What it might not automatically mean though is that we are in a big bond bear market. First we have to identify a regime (negative real rates), then understand whether the market is pricing that regime correctly (no, yields are too low) – but then you have to apply any structural overlays which might override your thoughts on fundamental valuation. And it’s here that Quantitative Easing becomes important. As Charlie Bean of the Bank of England’s MPC has stated, QE reduces “the cost of financing a given deficit”. Here in the UK, the Eurozone and the US, Central Banks are keeping bond yields low enough to stop their governments from going bust – and that’s not going to change for the foreseeable future.

The answer was the Bank of England’s Inflation Report cost £4 when it was first published in 1993, and now costs £3, deflation of 25%.

Congratulations to the ten winners picked randomly:

We’ll be in touch and you’ll receive your books soon. Thanks for all the entries.

The news of the Greek default hardly came as a massive surprise, having been years in the making (see Stefan’s blog from 2010) but we have certainly learned a few things, such as the privileged position of the ECB with regard to their holdings of Greek bonds (as I mentioned in a recent blog). Last week’s ECB press conference provided Draghi an opportunity to explain why the institution he heads should have super-senior status. He said the following in response to the question as to why the ECB should be treated differently:

“I can answer saying that the SMP was a monetary policy instrument. So the purchases of Greek bonds done under that program responded to public interest policy – general policy considerations. And as such, they deserve protection. This is one reason. The other reason is that I think the balance sheet of the ECB should be protected, because only through the integrity of the balance sheet of the ECB you can have the ECB independence in pursuing price stability in the whole of the euro area, and price stability is in the interest of all the members. So I think that’s one other reason why this exchange of bonds was quite right to do. But there is a third reason, I think, that people rarely think about this. I mean, we forget that this money is taxpayers’ money. And so the ECB has, in a sense, the duty to do everything to protect the taxpayers’ money that was entrusted with it. So this exchange of bonds was actually the right thing to do from this point of view as well.”

In summary, he stated 3 reasons:

Well, a private sector holder of Greek debt was also:

So,

Given the ECB’s role as lender of last resort, explicitly to banks and implicitly to sovereign states, it is not surprising that corporate credit is becoming more desired and relatively better rated than many sovereigns and banks where the ECB has the potential to become involved.

We rarely go into individual corporate rating actions on the blog, but bear with me. Today Heineken was rated Baa1, BBB+ by Moody’s Investor Service and Standard & Poor’s respectively. Not exciting, and a non-contentious rating. So why is it of interest ?

Well, for the previous 25 years of my career this large corporate has not had a credit rating, and has decided at last to join the vast majority of debt issuers by having a rating. Rene Hooft Graafland, Heineken Executive Board member and CFO, commented “the award of these credit ratings underlines our commitment to transparency and diversification of our funding sources”. Now one could argue that given the company has been going for over 150 years, and has issued reasonably regularly in recent years, it is a bit late to the party. Why now?

Heineken was previously able to access the credit markets without a rating as its long history and name recognition in Europe gave it a technical boost. It was perceived by retail investors to be a good credit, on the strength of its well known brand and its relatively conservative financial profile, and so had no need to involve rating agencies. If anything, there was the risk of the company obtaining a rating below the market’s perceived credit risk.

On a simple front acquiring a rating increases the number of investors who will buy the deal, from unsophisticated index funds who buy anything in indices (now it’s rated its debt will enter various indices) to other investors who are rating constrained, or unable to do credit analytical work themselves because of their small scale, and international investors who are not as bekend (au fait) with the credit as they would like, and appreciate the validation of the rating agencies.

However, I think there is an emerging, more potentially significant underlying message. Given the collapse in credit worthiness of many European sovereign states, I think that corporates are very keen not just to show their relative attraction versus each other to source cheap funding, but to make the point that with the help of the rating agencies they can be perceived as a home for previously “risk free” money that was once allocated to government debt.

I’ve just finished reading Dan Conaghan’s newly published book The Bank: Inside the Bank of England. It’s very good – and essential reading for all bond geeks. We met with Dan a couple of weeks ago (he’s coming in for a lunch with a few clients next week) to talk through some of the themes in the book. First of all it’s a big surprise just how little has been written about the Bank of England over the past couple of decades, especially given how much has happened over that period – independence in 1997, the credit crisis and the bank bailouts, and Quantitative Easing in particular. Perhaps the best insight so far came in Alistair Darling’s autobiography, and like that book, the striking thing here is the criticism that Governor Mervyn King comes in for. King comes under attack for both his refusal to take advice and his reliance on a handful of people within his beloved Economics Division, but more seriously for his slow and perverse responses to the UK banking crisis and in particular the Northern Rock bank run.

Elsewhere there are a few other things that caught my eye. I hadn’t realised that in a late 2009 speech, Chief Economist Charlie Bean talked about one feature of Quantitative Easing being that it lowered gilt yields “so reducing the cost of financing a given deficit”. I’ve not seen that benefit of QE – i.e. reducing the national debt burden – ever mentioned again (I saw a former German ECB council member talk today and he described QE type regimes as “fiscal dominance” of politicians over central banks).

And there’s Paul Fisher of the MPC being questioned by a Treasury Committee about whether the Bank of England could intervene in the foreign exchange markets to change the value of sterling to hit the inflation target. “The exchange rate policy is part of monetary policy…the MPC can intervene in exchange markets if it thinks it is appropriate to help meet the inflation target”. Again though, not something I’ve ever seen discussed since, but worth bearing in mind especially as the pound remains so strong (we could sell loads of freshly printed expensive fivers and set up a SWF! We could put the proceeds together with the imaginary £28 billion that the government is getting from taking over the Post Office pension fund?).

Finally there’s a fair bit of debate about the next Governor of the Bank of England (Mervyn King’s term ends next year so there could be an announcement after the summer). Following the failures of the Tripartite arrangements during the credit crisis (Michael Fallon MP to the Governor regarding the actions of the Tripartite during the credit crisis: “Who was in charge?”. Mervyn King: “What do you mean by “in charge”? Would you like to define that?”) there’s a suggestion that an outsider like Lord Sassoon, commercial secretary to the Treasury might be the first external appointment for three decades. I’ve no view on Lord Sassoon, but I would be disappointed if Paul Tucker, current Deputy Governor, didn’t get the top job. I think markets would too – he has the right mixture of intellect, pragmatism and experience to cope with the future issues that the ongoing credit crisis will throw at the UK.

So a competition. We’re giving away 10 copies of Dan Conaghan’s book. The question is this:

It was first published in 1993 and cost £4. It now costs £3, a fall of 25%. Which influential publication is this (clue: you can find the answer in the book…)?

This competition is now closed.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.