Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

Anyone monitoring the risks in the global financial system knows that those of us who lend to banks are increasingly asking for some kind of security in order to do so. Issuance volumes for covered bonds have increased and more countries have recently passed covered bond laws or are in the process of debating legislation. Andrew Haldane, Executive Director for Financial Stability at the Bank of England, raised greater asset encumbrance at banks as a serious concern in a recent speech.

The speech outlines three “arms races” that banks have been or are now engaged in. One of these is a “safety race” in which investors all want to be first in the queue in case of liquidation. It is true that this “race” to the front of the queue has intensified in the past several years, but many forms of bank lending or trading have only been done on a collateralised basis for some time in the form of repo or derivatives trading with collateral posting requirements. The race for safety has only intensified as many banks have been forced to substitute collateralised central bank funding for other sources of funding that have been more difficult or too expensive to access. In the speech, the topic of pledging assets to receive central bank funds – in many countries the biggest reason for higher and higher encumbrance – is referred to. Repo, derivatives and covered bonds are not mentioned by name, but are implicitly involved in the “safety race”.

Certainly the thesis that investors are less and less willing to provide unsecured financing to the banking system is not new or controversial. That said, if you ran a poll as to the reasons investors have on balance pulled back, we strongly suspect the average investor would cite bail-in proposals and resolution regimes as being at least as important as encumbrance, since under the pre-Lehman assumption of state support the question of asset encumbrance and recovery rates didn’t really come up: the expectation (made explicit in ratings pre-crisis) was that the liquidation of systemically important banks was almost purely hypothetical.

Haldane proposes in the speech that, along with sensible macroprudential measures to curb systemic leverage and risk-taking as well as the speed of trading, regulators look to limit the amount of asset encumbrance at banks. How that sits with a central bank’s liquidity provision against collateral makes for an interesting thought experiment, but the more serious implication is that the real limits on pledging collateral could (if they emerge as policy proposals) be found in the new attempts to bring the repo market out from the shadows, which will form the subject of discussions being carried out by the FSB, EU, IOSCO and other bodies over the course of 2Q and 3Q 2012. Another area limitations may emerge is in covered bond regulations, which are constantly evolving. (Note that the US and Canada, both with longstanding deposit insurance arrangements, already limit the amount of covered bonds that banks can issue, even though neither country has a legislative covered bond framework yet.)

It’s worth thinking about whether limits on asset encumbrance actually benefit senior unsecured bank bond investors. There is at least a case to make that more of the benefits would accrue to shareholders, since leverage without asset pledges should still, all else being equal, increase returns to them, whereas senior unsecured investors, even having potentially better recovery prospects, would have to resort to pushing harder for faster implementation of the Basel III leverage ratio in order to gain protection. Current covered bond issues, at the margin, may be relatively more attractive than they already are, if there were to be a possibility of regulatory limits on issuance.

Finally, what about creditor bail-ins? Discussion continues about how this will be implemented in the EU. If it turns out that new “senior” debt, that explicitly allows write-downs, has to be issued to meet a bail-in debt requirement, it’s hard to argue that any investor would buy it without significantly more information on asset encumbrance. Investors would have to stand a chance of attempting to work out a recovery rate on their debt if they were to commit to automatic write-down in the event of resolution. The paradox is that the more serious regulators have become about bail-in, the more counterparties and lenders have grabbed collateral. The only obvious pressure valve is pricing, which makes it logically very difficult to argue that unsecured bank debt will see a significant rally in the near future.

Asset encumbrance remains a topic to watch, certainly, and it presents more evidence that bank balance sheets remain in a state of flux, so talk of a recovery in the senior unsecured market remains premature.

So some panic buying of petrol in March saw UK retail sales grow 1.8% from February and almost certainly means that the first quarter of 2012 will see positive GDP growth. As the final quarter of 2011 was negative for growth, this means that we’ll probably avoid the two consecutive quarters of falling growth that would have meant we were back in recession.

But a couple of things make me nervous about the UK’s growth prospects, quite aside from worries about the Eurozone debt crisis or China’s cooling economy. Firstly, it looks as if Quantitative Easing will come to an end in a couple of weeks’ time when the Bank of England buys the last of the £325 billion of gilts of its programme, and even Adam Posen is no longer voting for more QE. And the pound is becoming exceptionally strong (helped in the last couple of days by that perception that money printing is at an end).

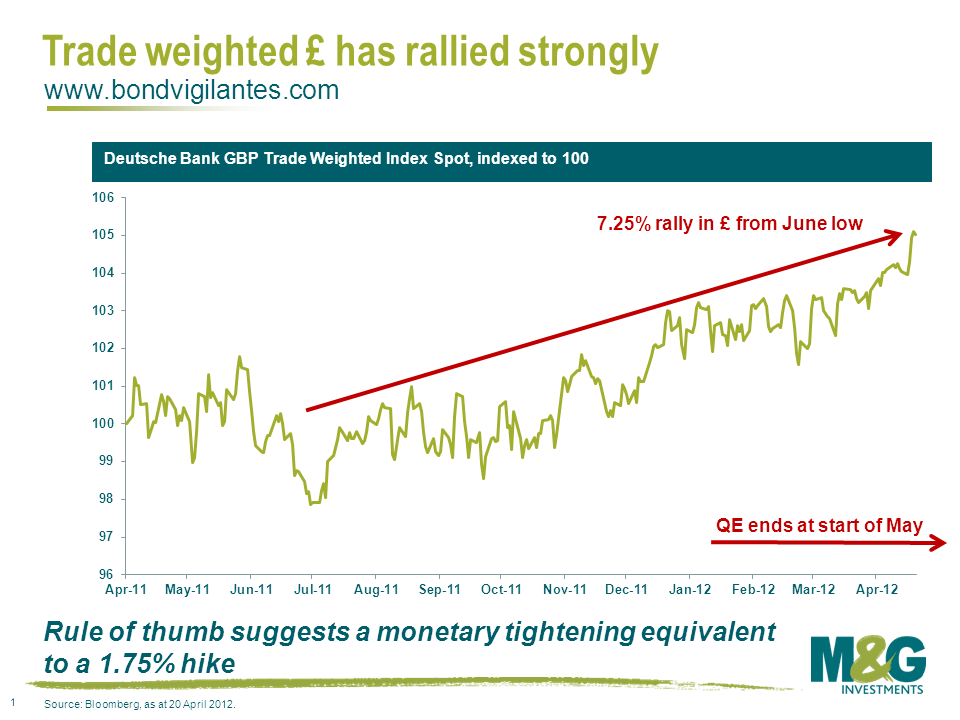

This chart shows that trade weighted sterling is up by over 7.25% since June last year. Today it hit its highest level since August 2009. The old rule of thumb was that every 4% appreciation in the pound was equal to a 1% rate hike (and vice versa for a depreciation). On that basis, if this relationship still holds, the move since June should be equivalent to a significant monetary tightening of 1.8%. Given this, like traditional monetary policy, will likely act with a lag (another rule of thumb is that it takes 6 months for a rate change to feed through into the economy), there could be big headwinds for the UK economy over the next few months. On the other hand, the strength of sterling could mitigate Bank Deputy Governor Paul Tucker’s fears that inflation could be around 3% for the rest of the year.

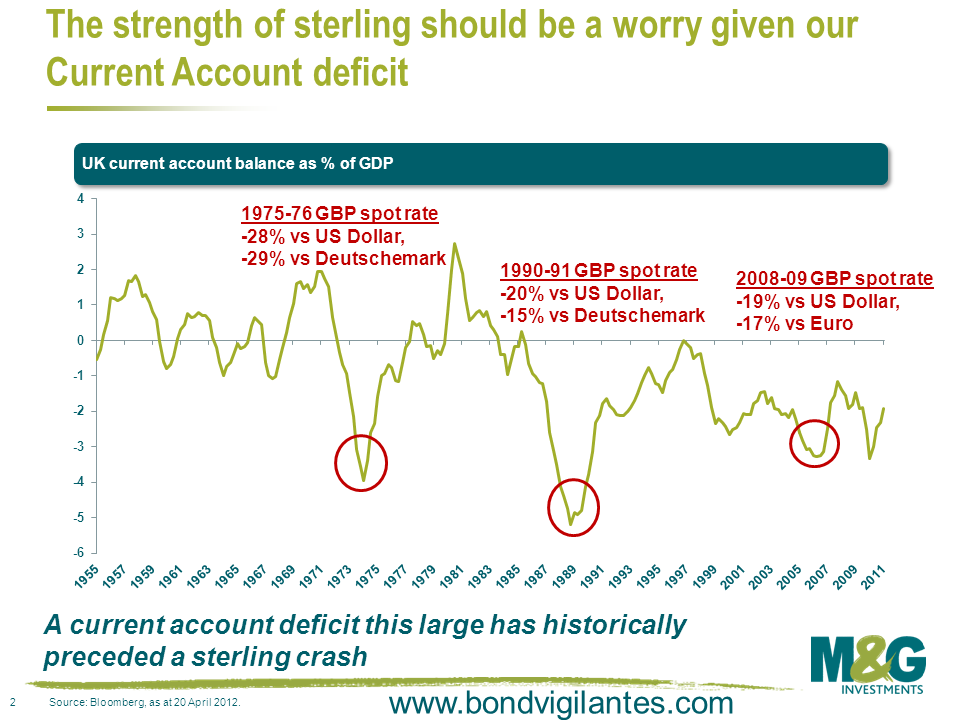

This second chart shows that sterling looks too strong compared with the UK’s current account balance. Typically when the CA deficit has been greater than 2% of GDP we’ve seen significant corrections in the value of sterling against its trading partners, as was the case in the mid 1970s, at the time of the ERM exit, and during the peak of the 2021/12 credit crisis. Recent strength of the pound can only really be explained by a safe haven status that may well not be justified (Moody’s put the UK’s AAA rating on negative watch in February).

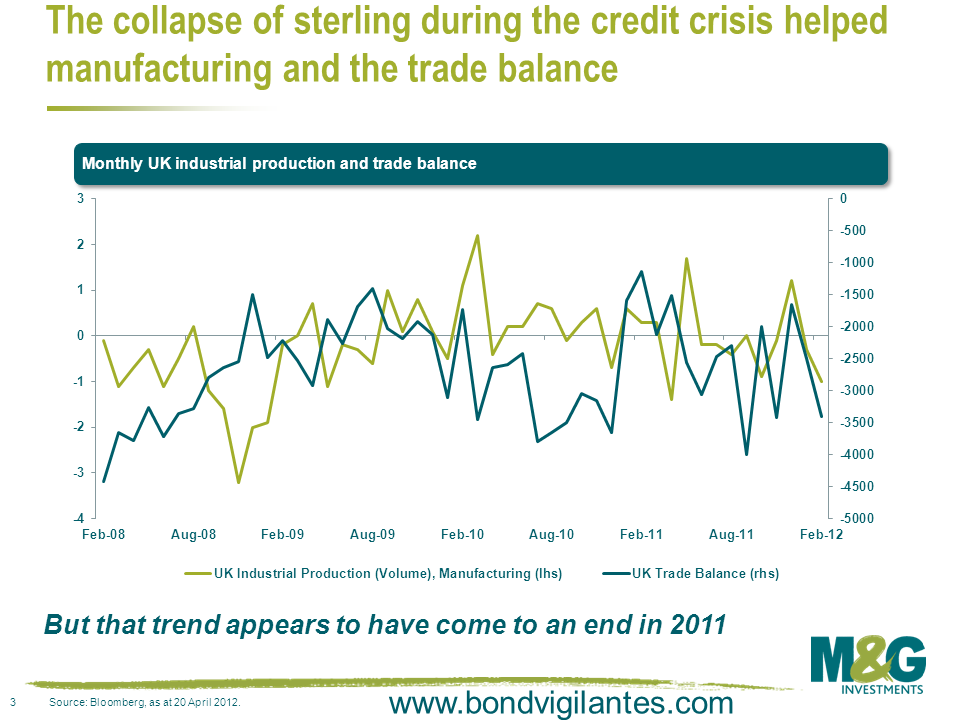

The final chart shows that we had a significant improvement in both UK industrial production and the trade balance in the period post that 2021/12 credit crisis sterling collapse. Industrial production stopped falling and there was talk that the UK would start to rebalance its economy and export its way out of the crisis – that trend came to an end in 2011, and recent manufacturing data have been weak. Whilst the trade balance remained negative through the chart period, you can see some improvement following the big sterling depreciation.

So it’s good news and bad news. The strong pound will help send inflation below 3% during the course of the year, but at the expense of economic growth and a rebalancing of the economy towards manufacturing (just look how Germany has benefitted from the weak euro). You might also consider an elevated level of inflation to be good news for the indebted UK, both at the state and private levels, reducing the value of debts by stealth – I accept that savers don’t see things this way though. It did make me revisit Bank of England MPC member Paul Fisher’s assertion to a Treasury Committee that “the exchange rate is part of monetary policy…the MPC can intervene in exchange markets if it thinks it is appropriate to help meet the inflation target”. If the economy continues to bumble along the bottom, and inflation rates fall sharply thanks to the strong currency, shouldn’t the Bank of England join nations like Switzerland, Japan and Norway in actively selling their currency or talking it down? George Osborne in this year’s Budget speech said “we are also taking the opportunity to rebuild Britain’s reserves”. What better way to do this than to print pound notes to sell into the fx markets for US dollars? Print £380 billion of them and we could buy Apple for the grateful nation. And on the 30th anniversary of the launch of the greatest computer of all time (the ZX Spectrum – my first job was Spectrum games reviewer for the Rugby Advertiser, first review was Daley Thompson’s Decathlon) we should put Sir Clive Sinclair in charge.

The next three weeks will mark uncertain political times in the eurozone. We could see the election of Francois Hollande as the next French president, the first multi-party coalition in Greece as well as some serious debates about early general elections in Germany. An Irish referendum on the eurozone fiscal treaty – and consequently Ireland’s role in the eurozone – will follow shortly after, but may not go ahead on 31 May as originally discussed. The electoral turnout for the elections in France, Greece and Germany might be as uncertain as the impact they will have on market sentiment and the future direction of Eurozone policies.

An election of Francois Hollande in the second round of the French presidential elections on 6 May would certainly shake up the current conservative leadership within the eurozone. As part of his election campaign, he has criticised last December’s fiscal compact which he deems to be too centred on austerity, a result of a strong push from the German Chancellor Merkel. He may aim to renegotiate the treaty and will hope for support from his party’s traditional foreign allies, such as the German SPD. Hollande has also been a supporter of the idea of eurobonds, an option ruled out by the German centre-right government so far. A change to the German government after the next general election in 2013 or even earlier could add momentum to this idea. All German parties from the left of the centre, currently scoring for a combined vote share of around 60% in recent polls, are rather open to the idea of eurobonds, but differ about how the concept should be implemented.

Hollande’s election might also result in tougher regulation of the French financial system. He has openly targeted the banks for additional tax revenue in addition to the EU-wide financial transactions tax backed by Sarkozy. Other measures proposed by Hollande and his party – the French Socialist Party – include a cap on bank service charges, a hike in the tax rate on life insurance products held for less than 8 years, restrictions on stock options as well as revised bonus regulations and a 75% tax rate on annual income above €1 million.

The two main parties backing Greece’s bailout have been recovering from the lows in the polls, but both are still far away from an absolute majority on 6 May. Recent polls see the conservative New Democracy party and the Socialist PASOK party combined at less than 40% of the votes, which might not be even enough to qualify for a renewal of their current coalition. This compares to a combined vote share of 77% in the last elections. All the other parties which are likely to pass the three per cent hurdle and to enter parliament are assumed to reject the agreed spending cuts. At present a coalition government seems to be the only option to form a government, either a grand coalition if the two main parties can increase their vote share further, or a multi-party coalition.

The government in Greece has been changing since the start of the Third Hellenic Republic in 1974 between PASOK and New Democracy, between left and right, but not shared. The interim governments in 1989 and 2021/12 have been the only very short-lasting exceptions. That is, the two-party system in Greece where the winner takes it all will come to an end. Given historic and recent tensions, it may be questioned for how long PASOK and New Democracy would be able to form a stable government. Any other, multi-party coalition may lead to lowest common denominator compromises and populist measures which might diminish the commitment to the imposed austerity and re-define the future role of Greece inside or outside the eurozone. Competition will increase in the political system which has never been a catalyst for coordinated and consensual political approaches across party lines.

The FDP, the junior partner in the German government coalition is currently facing a severe threat to its political existence. Since its very strong result in the general election in 2009, the party has been facing probably the most significant decline of electoral support in reunified Germany’s history. The party has failed to pass the five per cent-hurdle in six federal state elections since 2009, i.e. has not been elected into state parliament. Currently, polls suggest that the party would fail to enter parliament in Schleswig Holstein and, more importantly, North Rhine-Westphalia, Germany’s most populous federal state, as shown in the chart below. Elections in these federal states are due on 6 May and 13 May, respectively. If the FDP fails, the current government might come under considerable pressure to call for early elections, as their democratic legitimacy had already been questioned after the FDP’s most recent electoral failures. An early election scenario brings to memory the outcome of 2005 when North Rhine-Westphalia proved to be the stumbling block for the SPD/Greens government. Gerhard Schroeder’s coalition lost the lead in the state as well as the majority in Germany’s upper chamber, and the chancellor subsequently announced early elections which took place in September at the time. It might not be the base case scenario that early elections are going to happen, but it cannot be completely ruled out for now.

How does all this fit together? Of course, there are no certain conclusions to be drawn from this, as many of the outlined risks and uncertainties would have to materialise first. It might be worthwhile though to end with a little “what if” thought experiment.

Jim recently discussed the merits of officially cancelling the gilts bought back through QE, so I thought I would discuss another option that maintains the status quo through the Bank of England (BoE) simply rolling over the QE gilts into new gilts at maturity.

In order to understand the results of this process it is useful to re-examine how QE works.

Simply, QE is the willing exchange of gilts for cash between the BoE and the private sector.

What is the difference between a gilt and cash? Both are denominated in the same common currency, the main difference to the investor is that gilts pay a coupon, usually until a specified maturity date when they funge into cash on a one for one basis. Cash on the other hand has a zero return, unlike a gilt, and exists in perpetuity. Both cash and gilts can be lent to a third party in return for a payment. But that payment is simply a transfer payment for borrowing the asset (cash or gilt) with no extra intrinsic returns being embedded in the cash or the gilt.

Therefore as an investor you have the choice of owning a gilt that pays you extra return until a set date when it turns into a cash security that pays you no return forever, or investing straight away in cash that pays you no return forever.

The holding of a gilt looks intrinsically superior. A buy to hold investor of a gilt with a positive yield will always end up with a higher cash balance than the investor holding cash. Why do investors therefore choose cash over gilts? Mainly, it is due to the fact that the price of a gilt can go up or down, while the price of cash never varies. This risk aversion means investors are willing to forego a positive return in order for certainty when they decide to hold cash.

From an issuer’s perspective this is wonderful and can be taken advantage of. If the government can exchange interest bearing securities for cash (QE) then they can swap interest bearing securities that need refinancing at maturity for non-interest bearing securities that never need refinancing.

If for example 25% of the national debt has been exchanged for zero coupon perpetual securities (cash), then an 80% debt to GDP ratio effectively gets transformed into a 60% debt to GDP ratio, as 20% costs nothing to finance, never has to be repaid, and so is therefore effectively free finance.

The more of your outstanding debt you can finance at zero cost forever, the more debt you can sustain. If this free financing is undertaken responsibly it can be used as a sensible economic tool. However, if the temptation of free finance results in a misallocation of resources via the state, then it can be very harmful to the economy. This is why many economies have introduced the concept of an independent central bank to remove some of the political process from the real economy.

So far, the BoE has convinced the market that QE is a responsible policy. The use of QE has neutered the bond vigilantes, whilst the next enemy of this policy, the currency vigilantes, remain dormant.

The BoE could officially cancel the gilts or could simply exchange its existing gilts at maturity for new gilts to maintain the windfall gain of free finance. This topsy turvy world of money printing, low bond yields and free financing is a new challenge for investors.

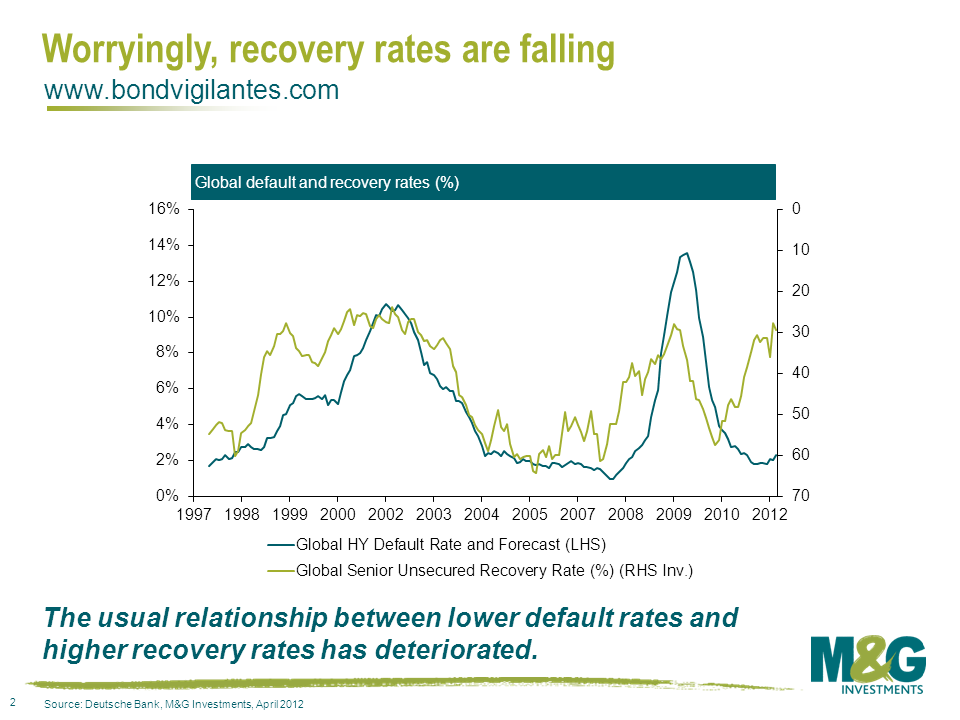

This week saw Deutsche Bank publish their 2012 Default Study, aptly subtitled ‘5yrs of crisis – The default bark far worse than the bite..’ The annual piece is particularly interesting, especially because the market now has five years of data since the onset of the great recession.

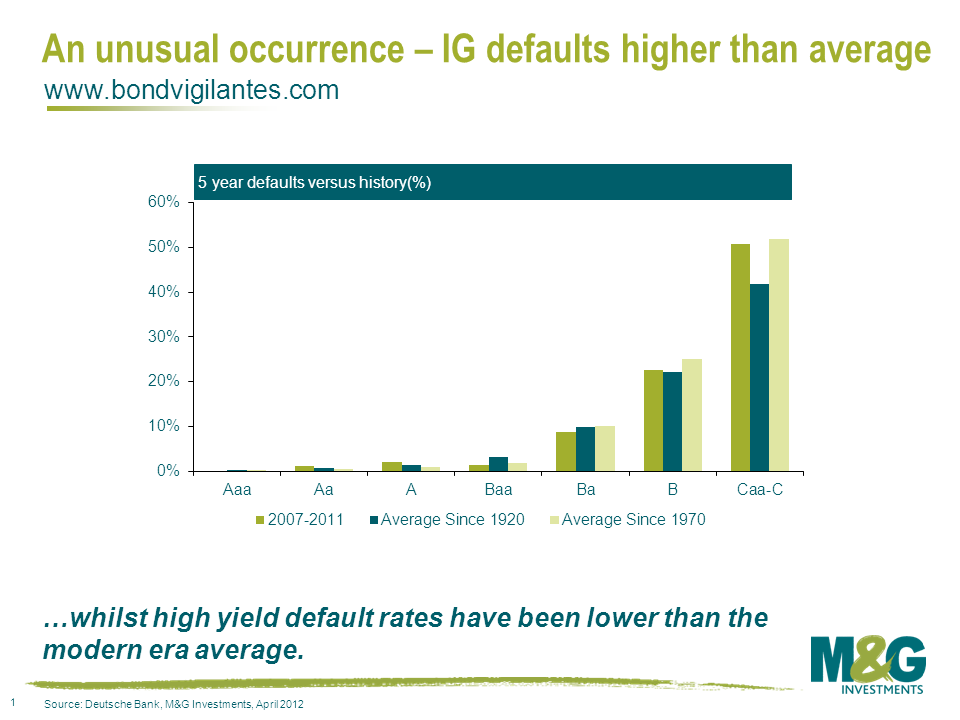

At the risk of failing to do an in-depth report justice it drew out several significant points for credit investors. Firstly, defaults between 2007-2012 have come in significantly lower than most would have expected. Secondly, loss given default (the loss incurred if an obligor defaults) in the last couple of years has been trending higher. Finally, investment grade credit continues to overcompensate investors vis a vis historical default experiences. High yield credit less so.

Whilst default rates have been decidedly ‘average’ over the last five years by historic standards, the statement masks an interesting picture. The below chart demonstrates that lower rated credit, especially sub-investment grade, has ‘outperformed’ the historic experience. Conversely Aa and A rated credit saw a higher default rate of 1.1% and 2.1% compared with a long run average of 0.8% & 1.3% respectively. Much of that can be attributed to the aggressive behaviour of financials (traditionally Aa & A rated) in the run up to the financial crisis and more conservative behaviour on the part of industrials. As Deutsche Bank argue, had we not seen massive intervention on the part of the authorities over the last five years then defaults would undoubtedly have been much higher. Perversely, it’s likely that the sheer extent of excess in the financial system forced intervention on a scale which artificially lowered the ‘market- free’ default rate experience.

An examination of recovery rates shows that there has been an obvious weakening and worrying trend developing over the past eighteen months or so. The following chart demonstrates this is somewhat out of whack with previous experience. Low default rates should typically correspond to strong recovery rates, partly because they are normally accompanied by better economic times. The current ‘artificially’ low default rate has been accompanied by a broad lack of confidence and a challenging environment for capital raising. This has weighed down on recoveries. Whatever the reason, this is an important trend that requires monitoring. Whilst defaults and their numbers garner headlines the loss given default is more relevant for investors.

Given the weakening trend in recovery rates, it would seem appropriate to apply a conservative recovery assumption of 20%, half the 40% traditionally applied, when analysing whether credit is or isn’t overcompensating a buy and hold investor. On this basis, investment grade non-financial spreads continue to significantly over compensate for historic default risk. Based on current market corporate bond spreads, Sterling investment grade non-financial credit is pricing in a default rate of 12.7% over five years, and 12.0% for European non-financial investment grade credit. This compares to a worst case experience of 2.4% for both European and Sterling credit since 1970. Turning to high yield, and again assuming a conservative 20% recovery, the data is less convincing. Whilst broadly speaking investors are still being overcompensated for investing in the asset class with an implied 5 year default rate of 37.9% versus the long-term average of 31.6%, much of the value comes from BB rated credit. At current valuations B & CCC rated credit provides far less compensation for buy and hold investors and clearly support the need for in-depth credit analysis, especially because of the spread dispersion to be found in the lower rated areas of the high yield market.

As far as the outlook is concerned it seems a reasonable call to argue for continued low default rates amongst investment grade industrials in core European economies and the US. Liquidity remains ample, earnings remain broadly strong and financial discipline adequate. On the other hand, default experiences in the periphery and financial arenas are very much at the whim of the authorities. The adjustments needed will undoubtedly take time if they are to happen at all. Without the ongoing support of central banks and creditor nations it is unlikely that default rates will go anywhere but up.

The UK sits unhappily at the very boundary of what debt burden is acceptable for a AAA rated economy. If growth continues to disappoint, or if more austerity becomes socially impossible, the UK will be downgraded – and neither of these possibilities look very remote.

At the moment the UK public sector net debt to GDP ratio is about 63%, equivalent to about £1 trillion (these numbers exclude the debt of the part nationalised banks). Debt servicing costs are over £50 billion per year – a large chunk of our annual deficit. Additionally our debt position is likely to deteriorate before it improves.

But do we really need to be paying interest to the Bank of England on the £300 billion+ of gilts that it holds as part of the Quantitative Easing programme? In fact the Bank holds these gilts on behalf of the Treasury anyway, so the Treasury is effectively paying interest to itself on assets that it bought with “free” printed money. Could we decide that this is a waste of time, that we are unlikely to sell these gilts back to the market in any case, and that we may as well just cancel the gilts we bought for the nation? Gold bugs and inflationists will at this point be spluttering into cups of tea – what about all of the printed fivers that have been set free into the economy like in a modern day Weimar Republic? Well, how about this for a potential statement from the authorities on gilt cancellation announcement day:

“Today the Treasury announces the cancellation of £350 billion of gilt-edged stock held by the authorities. These gilts were bought as part of the Quantitative Easing programme started in the aftermath of the financial crisis. The purpose of Quantitative Easing was to boost nominal growth after what we thought was a temporary fall in UK output. Several years later it appears that this fall in output was permanent – the fall in UK GDP remains more severe than that experienced during the Great Depression. We will therefore make this liquidity injection permanent in order to boost UK growth and reduce unemployment. The Bank of England of course remains fully committed to its inflation target of 2% – a cornerstone of UK economic policy. Should inflation rise, or be forecast to rise above the target range, the Bank may raise interest rates, or sell Treasury Bills to the market in order to drain excess liquidity from the system and return inflation to its target. Today’s action also reduces the UK’s debt to GDP ratio from 63% to 41%, and slashes our interest bill from £50 billion £32 billion per year. This prudent action safeguards the UK’s AAA credit ratings and leaves holders of gilt-edged securities in a stronger position than before.

Note from the Debt Management Office: the gilt cancellation will take place using the same process and precedent set with the cancellation of £9 billion of UK gilt-edged securities acquired from the Post Office pension scheme in April 2012.”

So who would be unhappy with this? No default has taken place (no CDS trigger, no D from the ratings agencies who are only interested in failure to pay private investors), the UK’s public finances become sustainable, the economy gets a boost from the knowledge that the QE cash injected will stay there for the foreseeable future, and a mechanism exists to remove cash from the economy should inflation return. Apart from the fact it all feels a bit banana republicy everybody’s a winner. In fact the genius of this idea is that it doesn’t need to be done at all – if the Bank of England were to start paying gilt coupons and maturing gilt proceeds over to the Treasury automatically you would have an equivalent economic impact, without any of the awkward Zimbabwe comparisons.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.