Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

In the true spirit of October 31, today we thought we would try our best to try and scare you. Five charts, each more scary than the last.

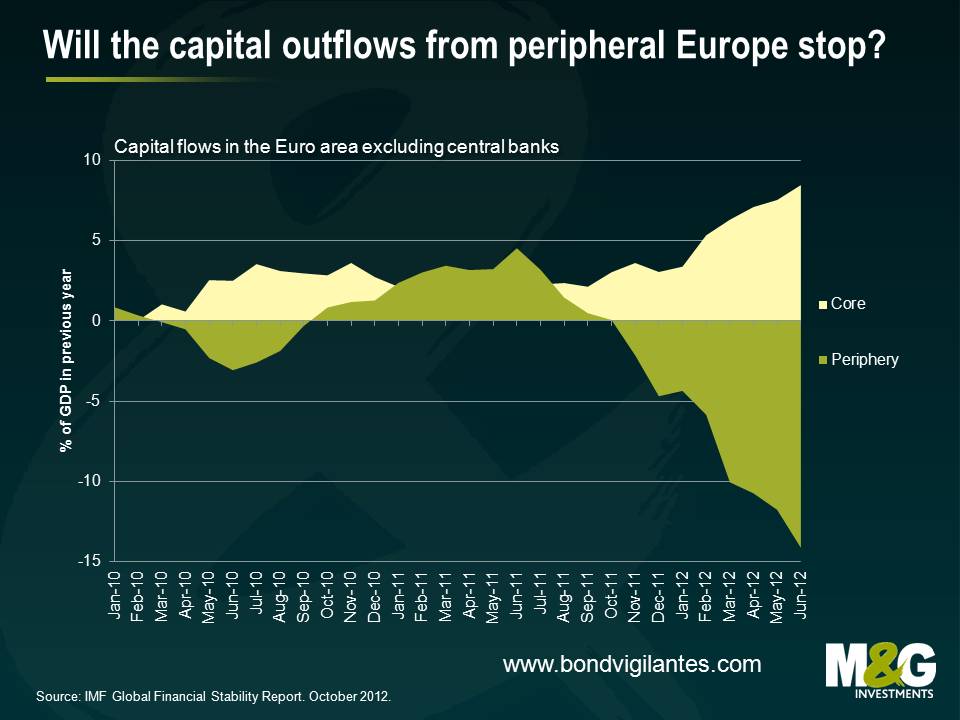

1. Capital fright

Uncertainty in Europe is having a significant impact on investor and consumer confidence. This is manifesting itself in a flight to quality for capital, which the below chart highlights rather well. Most economists agree that capital flight may destabilise financial markets, raise a country’s borrowing costs, reduces a country’s tax base, and can have major ramifications for the domestic banking system. If capital is the lifeblood of an economy, then the blood is draining out of the peripheral economies.

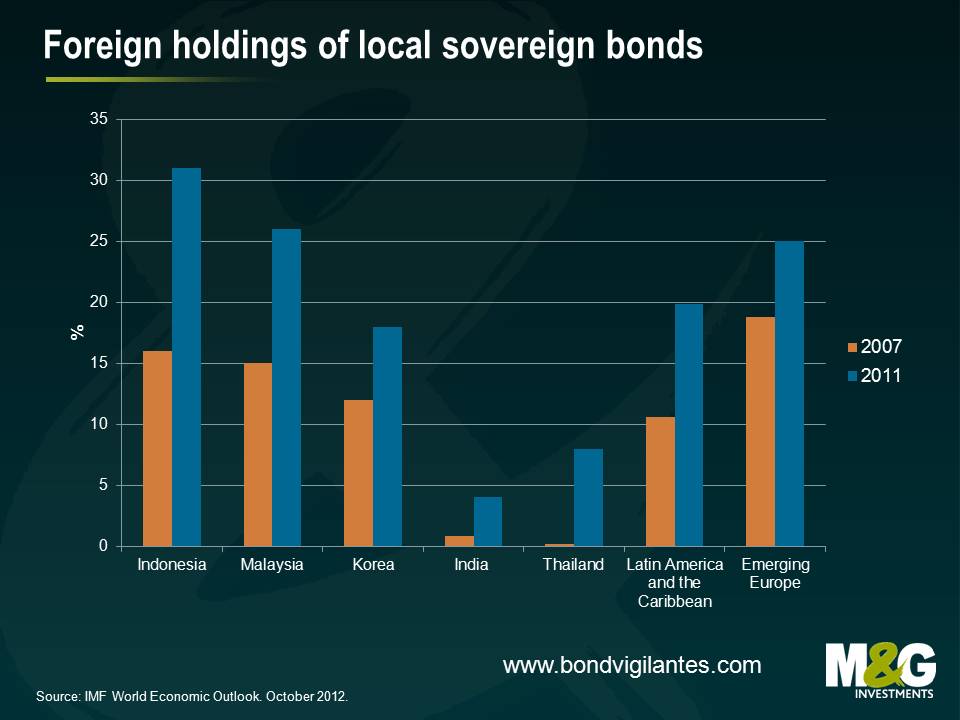

2. Ghostly foreign holdings of local sovereign bonds

On a related note, many emerging market countries have seen large capital inflows since 2007. We describe the percentage increase in foreign holdings of local sovereign bonds as ghostly. As quickly as the inflows appear, they can reverse again. This is a major risk in our opinion and is something we wrote about back in July.

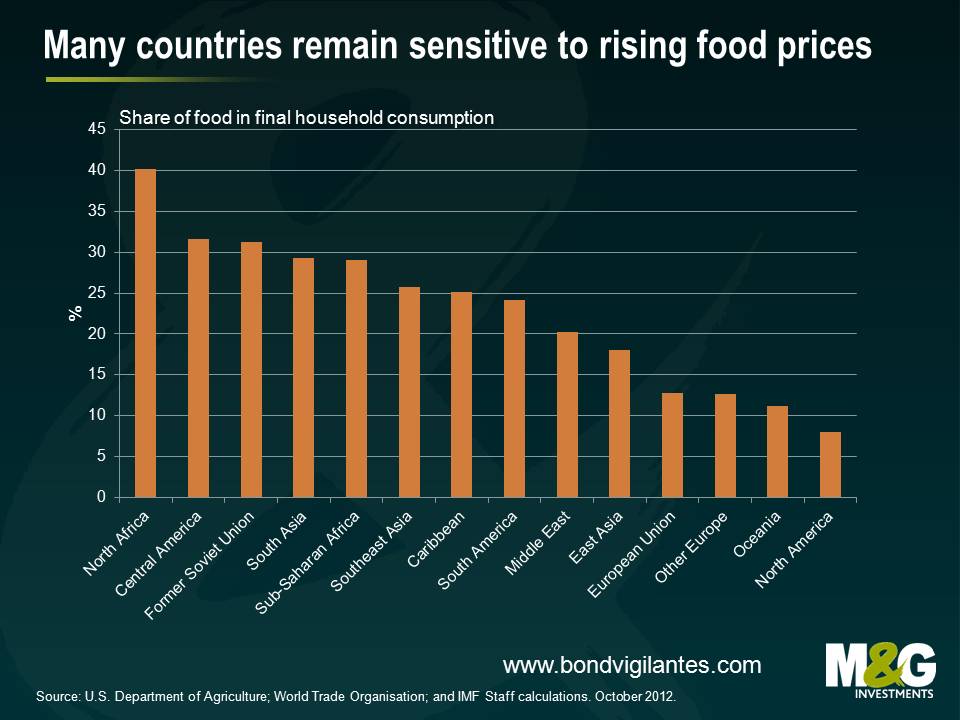

3. Country dependence on trick or treats and food

It remains the case that for a substantial proportion of the world’s population, food remains the largest component of their consumption baskets. With global warming, rising populations, tightening supply dynamics and growing global demand, food prices and inflation will continue to have a large influence on the majority of us. How will governments and policymakers respond?

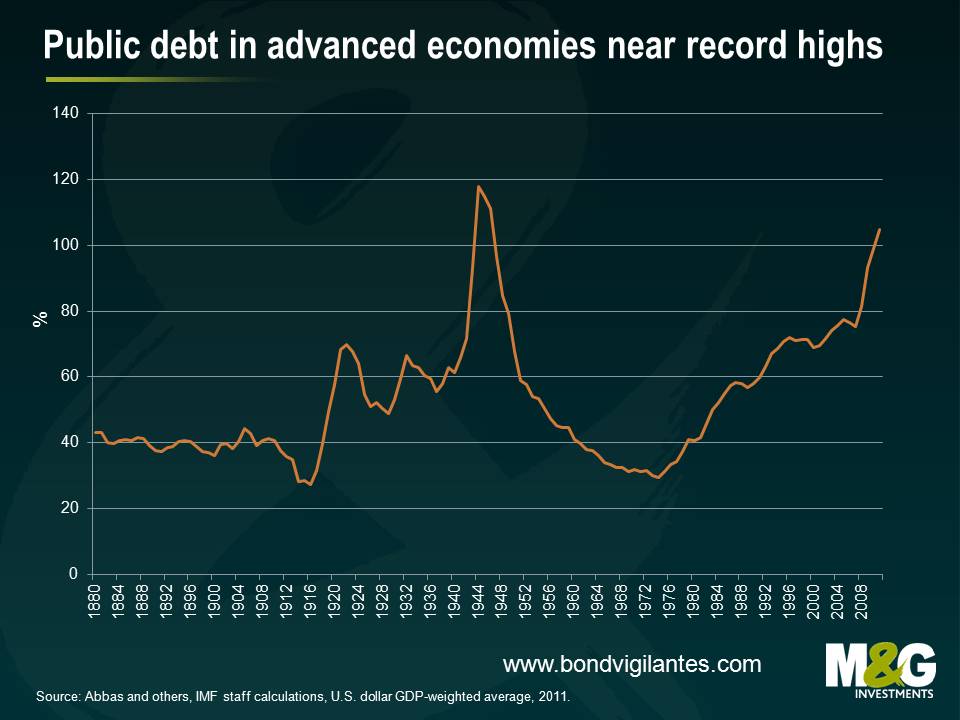

4. Growing public debt and zombie nations

Gross public debt as a percent of GDP in advanced economies is now near historical levels. There is significant debate about how policymakers will address the debt problems that many countries now face. If they don’t, they risk being cut off from bond markets, rendering them as zombies. Is it better to implement fiscal austerity, or try and stimulate growth through further policy stimulus? What about financial repression? Whatever the answer, there is going to be a lot of structural pain in order for many countries to become competitive again.

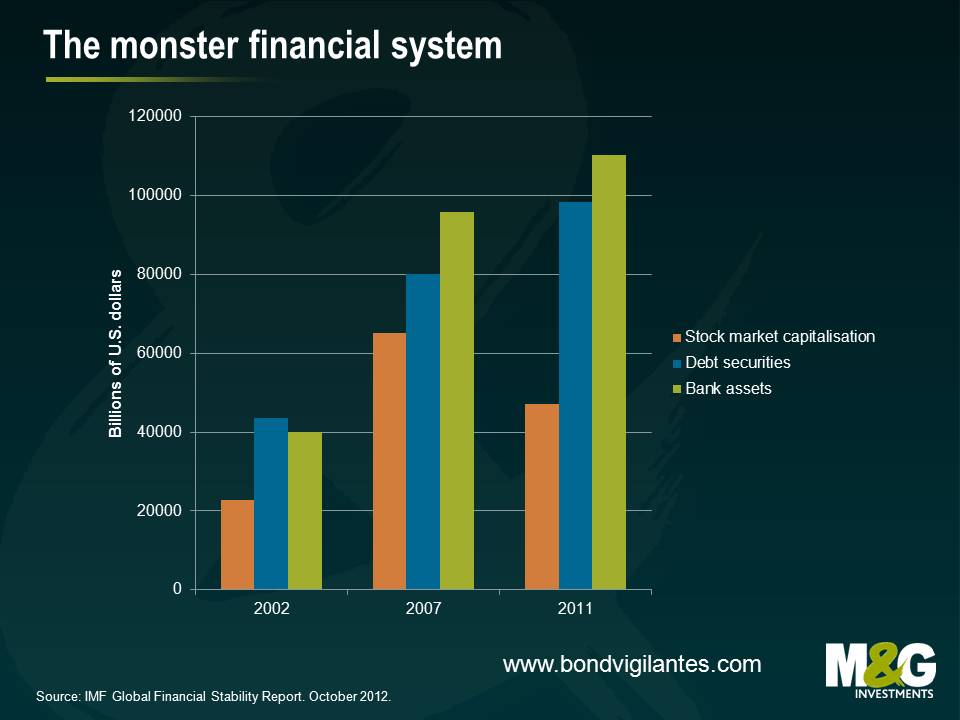

5. The global financial system is a monster

The global financial system can safely be classified as a monster. The global financial system is now valued at USD 255,855,541,100,000 (almost 256 trillion) in size. This is an increase of around 140% since 2002. To put this into context, the Milky Way galaxy is estimated to contain between 200-400 billion stars. As a per cent of GDP, the global financial system has grown to be worth around 367% of global GDP. Good luck to all the central bankers out there who are trying to tame the monster.

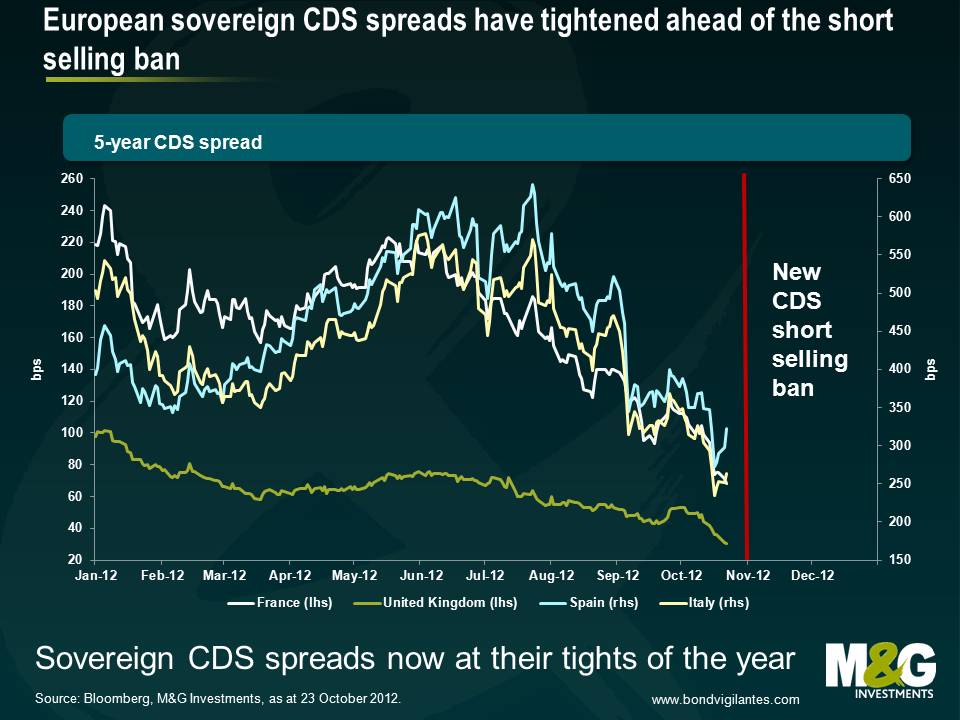

Since the middle of this year, credit spreads on peripheral sovereigns have narrowed considerably. Having been as wide as 600 bps, Spanish 5 year CDS is now around 300 bps, Italy is down from 500 bps to 250 bps. Ireland now trades at just 200 bps. Now at least part of this performance can be put down to Draghi’s speech in July in which he said “within our mandate, the ECB is ready to do whatever it takes to preserve the euro. And believe me, it will be enough”. And after the “whatever it takes” speech, Draghi eventually followed this up in September with the announcement of the Outright Monetary Transactions (OMT) programme in which the ECB would buy short dated government bonds of Eurozone members where bond spreads reflected too high a breakup premium (but with some conditionality attached in return). So is the improvement in credit sentiment a reflection of conviction in the European authorities to “save” peripheral bond markets? Perhaps.

The other dynamic over the past few months might be just as powerful – a growing realisation amongst hedge funds and other asset managers that the EU Regulation on Short Selling and Sovereign Credit Default Swaps, finally published in April, might well force them to close out short positions in the troubled sovereigns. The Regulation states that uncovered (“naked”) sovereign CDS shorts on European Union (not just Eurozone) nations will not be permitted, and must be closed out by 1st November 2012. “Naked” broadly means not hedging an underlying government bond exposure – it covers bearish trades on government creditworthiness. The short can be closed out by either using an opposing CDS contract, or by buying underlying government bonds to the same value. Whilst there is an exemption for positions initiated in a period before the Regulation was published, any short positions put on since then have to be closed out, whether this is a single name CDS or even an index which includes an EU member (for example the iTraxx Sovx CEEMEA index, a CDS index consisting of 15 sovereigns from Central and Eastern Europe, Middle East and Africa, includes Poland, and so a naked short position in the index would be banned). The Regulation is global in its reach and so should forbid even, for example, a Singaporean bank dealing with a US insurance company out of an office in Chile.

So as November approaches, the market is one-way. Whilst there is likely to be some sort of market maker exemption for having short positions (nobody seems entirely sure), there is no longer any willing counterpart to take the short risk positions off the Eurozone bears’ books. So they are forced to cover these positions at increasingly penal levels, and in doing so exacerbate the squeeze.

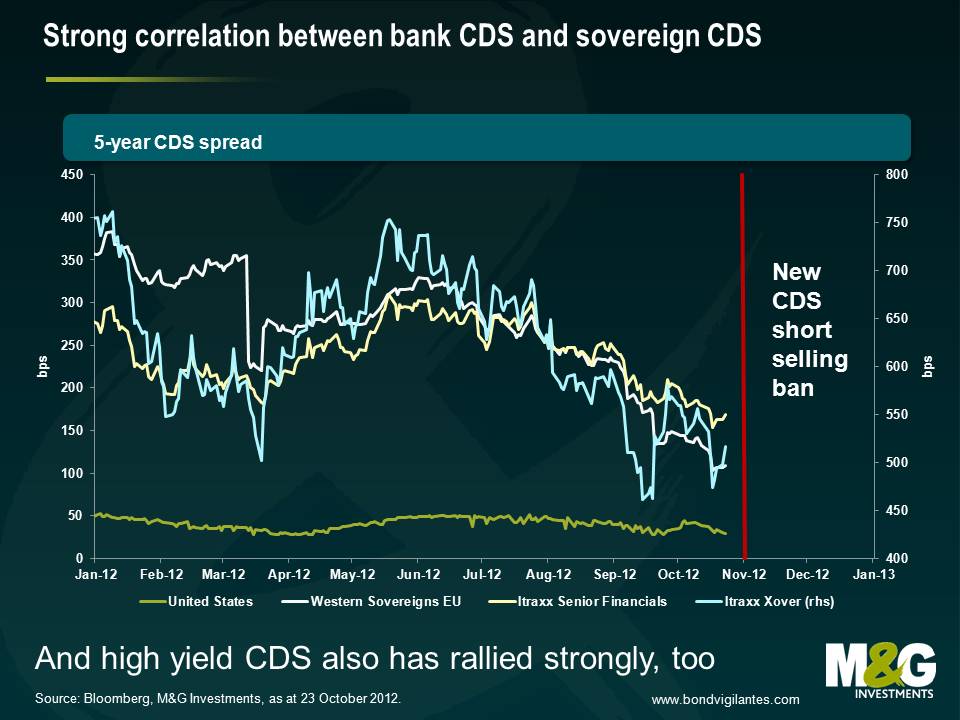

You can see that the impact is wider than just the Eurozone nations – UK CDS has fallen to 30 bps, despite deteriorating growth and fiscal conditions (and the chance of a AAA downgrade in the next few months). You can see a similar impact in the US, and also a very strong correlation with European sovereign CDS and European banks, and even high yield (the Itraxx Xover index on the chart). In other words, might the general rally in bond risk assets in the past few months be at least partly linked to this short CDS ban? Might the Regulatory deadline date at the start of November trigger the end of this trend? And given the high interdependency between the sovereigns and the banking sector in Europe, will short positions in future go into banks if investors are not allowed to short European sovereigns anymore?

Last week Jim attended the annual meetings of the IMF and World Bank in Tokyo. For Bond Vigilantes, he took the camera along and documented his trip. Jim told me that the IMF and World Bank meetings, and even more the conversations and debates beyond the formal schedule, gave him some interesting food for thought. With the fiscal cliff arising and the UK’s failing experiment with austerity, Olivier Blanchard’s views around fiscal multiplier effects have been quite thought provoking. But not only has the conference helped shape his views, Tokyo itself has been inspiring. Much seems to be genuinely different, but at the same time there are many things that make you think Japan might be leading the way for the rest of the developed world.

Postscript: Anyone who was expecting further insights from Jim’s research trips into national sports will be disappointed. This time he didn’t bother to sight new football talent after his lack of success in Brazil. And he still prefers cricket over baseball…

Given the success that central banks have had in targeting inflation over the last decade or so, the recent increase in their powers, and the broadening of their remit to include economic growth, has been largely welcomed by the markets. But have we put too much faith in central banks abilities? And, with record levels of peacetime government deficits and the clear political incentive to tolerate higher levels of inflation, have we come to overestimate their commitment to reining in prices?

In this note, which is part of our quarterly Panoramic series, we argue that we are seeing potential upside risks to inflation as central banks continue to preside over the biggest coordinated global monetary stimulus that we’ve seen in recent history. In our view, the expansion of central banks’ balance sheets signals an unspoken shift in these institutions’ remits that could have important consequences for future inflation rates. It is a phenomenon we have coined “central bank regime change”.

The Bank of England and European Central Bank seem no longer to be primarily focused on delivering price stability. Their new mandate now covers supporting domestic banking systems, offsetting the effects of government austerity measures, bolstering trade and implementing the conditions needed to generate jobs and economic growth.

With central banks’ macroeconomic responsibilities straying ever further into what was previously the state’s domain, their independence is looking increasingly fragile. The hijacking of monetary policy by politicians cannot be ruled out, especially if it enables them to inflate their way out of their growing debt burden. If we get to this stage, inflationary pressures will rise, although central banks’ credibility will be tarnished and policy responses rendered ineffective.

In our view, there are potentially plenty of reasons to expect the current period of low inflation to come to an end. Central banks are still thinking of new ways to ignite growth and they appear to be increasingly tolerant of above-target inflation. But are they moving ever closer to a major policy error that could ruin their inflation-targeting credibility? And should we all start thinking about inflation again?

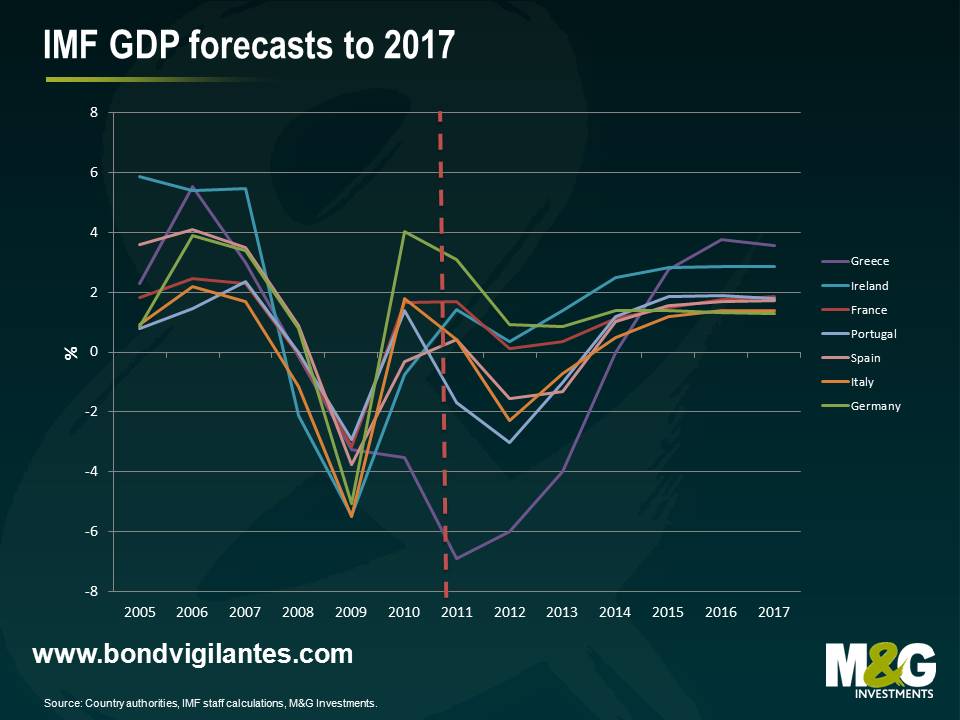

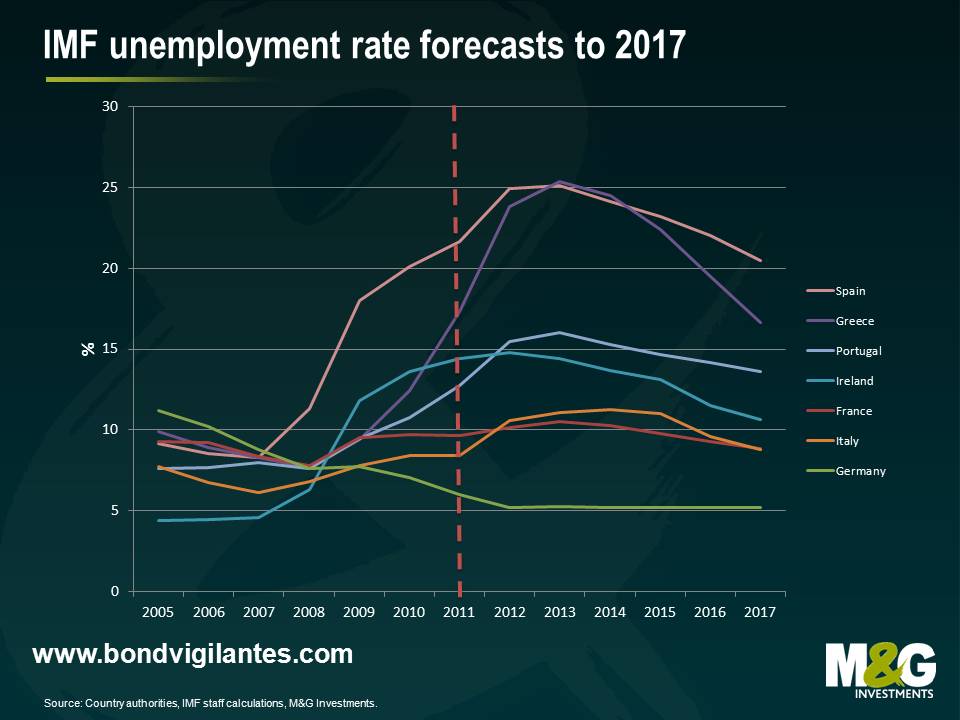

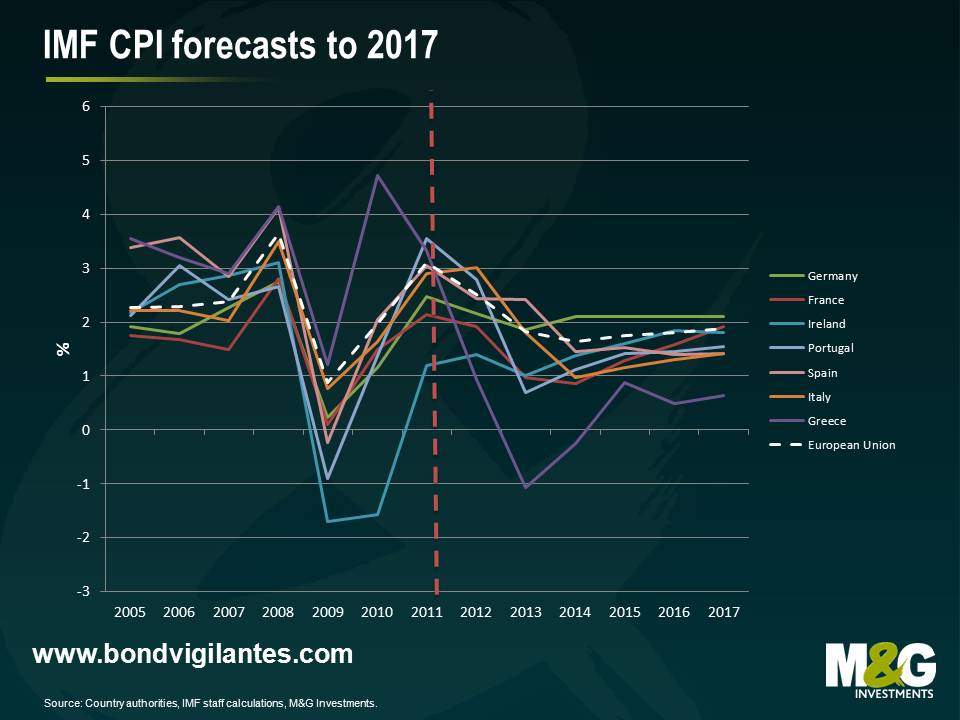

The latest IMF World Economic Outlook came out last week with much fanfare amongst the press and financial markets. We think the IMF produces some absolutely stellar stuff, as we have highlighted here and here in the past. But the forecasts in the IMF WEO, its flagship publication, are laughable. What makes the IMF think that it can forecast five months into the future, let alone five years?

We all want to know what the future holds, so here is the future according to the IMF.

Below are the GDP forecasts for France, Germany, Greece, Ireland, Italy, Portugal and Spain. According to the IMF, Greece, Portugal, Spain and Italy will all emerge from recession in 2014, with all countries growing solidly by 2015. The real stand-out performers will be the nations of Greece and Ireland who will overcome an environment of austerity and the single European currency to register annual growth rates of 3.8 and 2.9% respectively in 2016. Poor Germany will be the laggard of these nations, with a growth rate of 1.328%.

I know what you’re all thinking. That’s fantastic. What is happening to unemployment rates in these countries? Well the IMF has kindly provided a forecast for that too. The good news is unemployment rates are forecast to fall across Europe (perhaps workers will give up looking for work, or maybe mass emigration will help lower unemployment).

And a fantastic job from the ECB will see it achieve its primary objective of monetary policy by keeping inflation below, but close to, 2% over the medium term.

So the best place to live in Europe in 2017 will be Greece. Rapidly falling unemployment, low inflation and one of the strongest growth rates in Europe suggest an excellent standard of living. And it is now cheaper to live there too, with Greek house prices having fallen by 21.6% since their peak. So why are the Greeks leaving?

On the 9th October 2007 the totem pole of capitalism, the S&P 500, peaked at 1,565. Last night it closed at 1,441. So, five years into the crisis, where are we in terms of clearing up the banking crisis?

There’s good news in the US. We have commented on the initial driver of the crisis in the world’s largest economy – the boom and bust of the housing market – on many occasions. Recently, we’ve noted that we’re beginning to see improvement here. This is an important sign that the US is moving on from the financial crisis. Although unemployment remains stubbornly high, it is moving in the right direction and the financial system is looking sound once again. The government’s combination of supportive measures – such as taking equity stakes in banks – and allowing some pain to occur – in the case of Lehman Brothers and housing repossessions – seems to have been largely successful.

The UK economy and financial system have not yet returned to the same state of health and the government still holds legacy stakes in some of the bigger banks. It appears that the problems the country faced five years ago remain, even though they are not as severe as they were. These difficulties are highlighted by today’s Financial Times where the two headline stories relate to the FSA easing bank rules further to encourage lending and help the financial system, and the governor of the Bank of England’s speech at my old university last night where he talked about giving central banks greater flexibility with their inflation targets to help avoid financial crises.

Europe, the third major western financial system, faces its own particular problems. Five years on from the peak we had the strange situation of the German chancellor being taken in a convoy of cars through Athens past illegal demonstrators to try to sort out the continued funding of the Greek state. We have written many times about the questionable sustainability of a politically motivated single currency and the funding of states, individuals and corporates remains difficult in many parts of this system.

We believe financial systems need to be mended by a combination of government intervention and private sector responsibility. The US has led the way in this regard and the UK is trailing, hopefully successfully, behind it. However in Europe the problems have been exacerbated by the single currency regime, where the need for political intervention to solve the problem is relatively large versus the need for private sector adjustments. We are still concerned about whether the necessary political intervention will occur. So, five years on, it appears that the western world is still coming out of the credit crisis, albeit at different speeds and with different levels of success.

This post was originally published on 5.10.2012 in English and has been translated for our French readers.

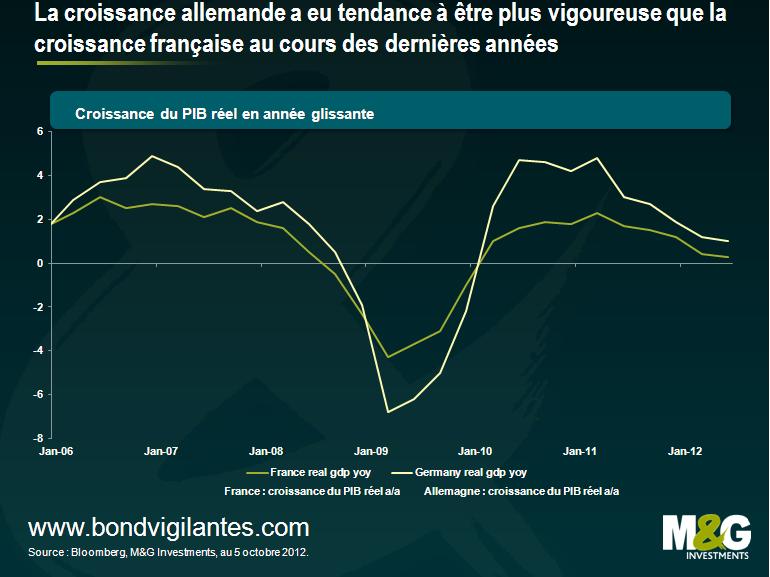

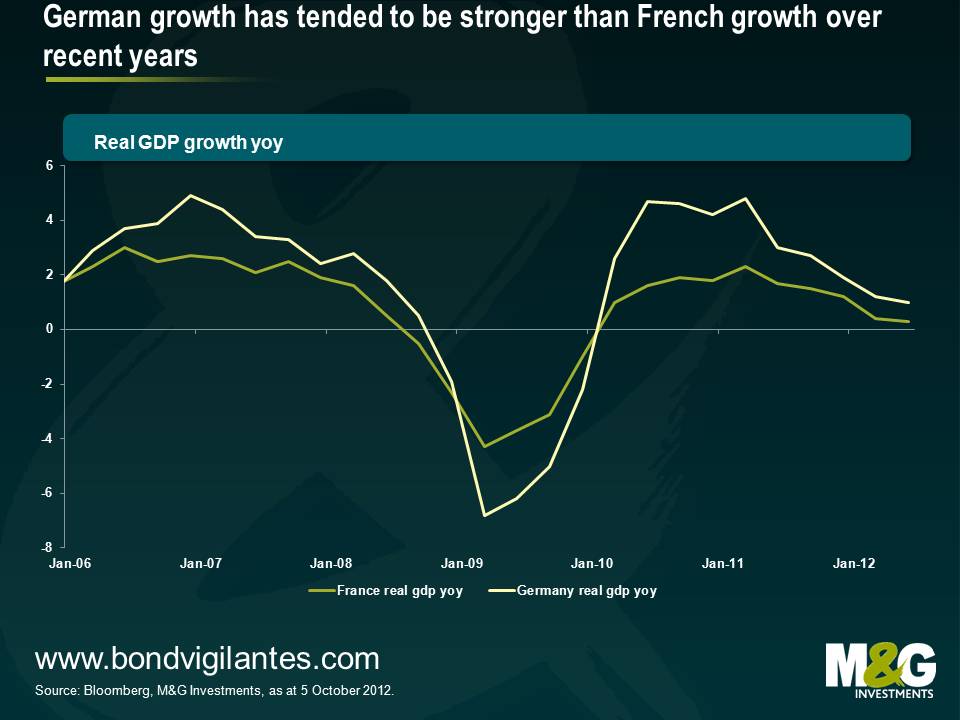

Depuis le début de l’année 2011, la croissance économique de la France s’est révélée extrêmement décevante, en passant d’un rythme annuel de près de 2,5 % à tout juste 0,3 % au second trimestre 2012. Certes tous les pays de la zone euro ont été à la peine durant cette même période, mais la croissance française s’est néanmoins laissée distancée par celle des états du cœur de l’Europe. En Allemagne, la croissance du PIB est ressortie au minimum à 2 % pendant tous les trimestres (à l’exception des deux derniers) et s’établit aujourd’hui à 1 %. Les indices des directeurs d’achat pour le mois de septembre ont fait apparaître une divergence plus prononcée : les PMI des secteurs manufacturier et des services ont à nouveau reculé en France, tandis qu’ils ont progressé en Allemagne.

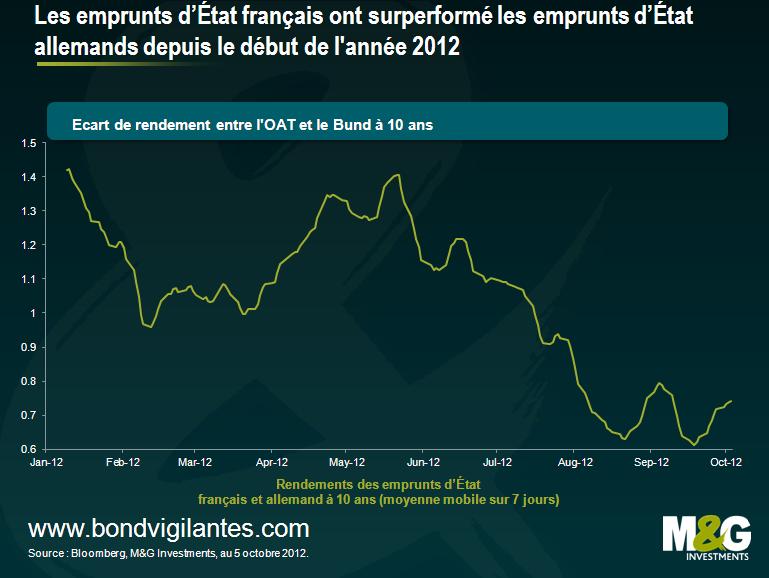

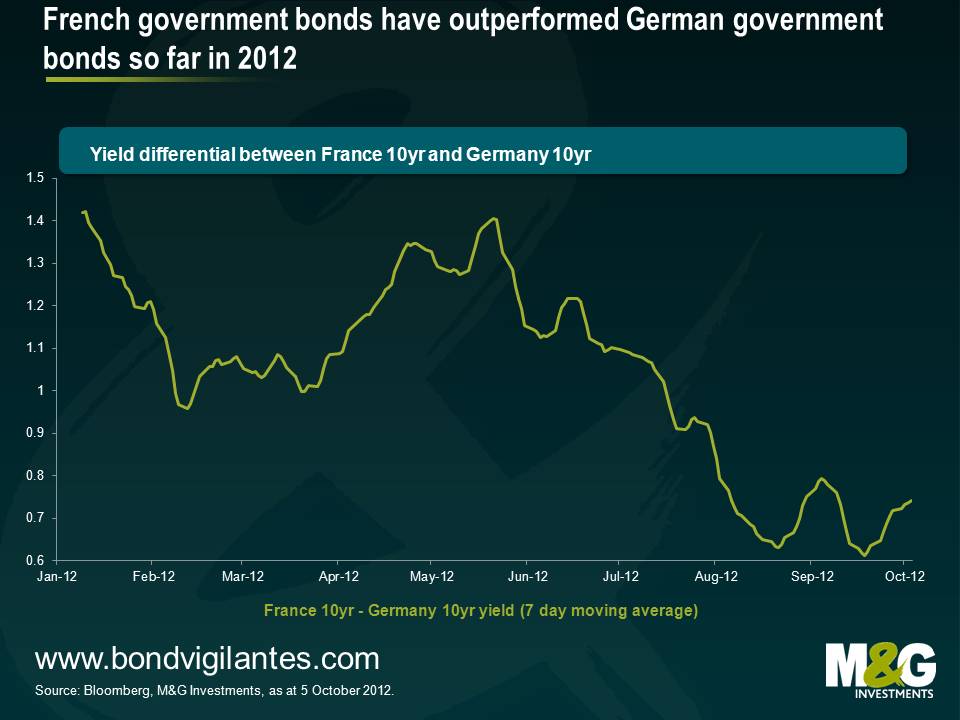

Evidemment, cela pourrait être pire – la Grèce, le Portugal, l’Espagne et l’Irlande ont enregistré une croissance économique bien plus faible et -élément peut-être le plus dommageable- des taux de chômage bien plus élevés. En Espagne, le taux de chômage s’est envolé de 8 % en 2007 à 25 % aujourd’hui, franchissan même la barre des 50 % chez les jeunes. En France, le taux de chômage global n’est « que » de 10,3 %. Et l’autre grande différence est que les marchés obligataires pensent que la France fait partie du « noyau dur » de la zone euro, non de sa périphérie. A ce titre, examinons les CDS à 5 ans (le coût en points de base pour assurer une obligation souveraine contre le risque de défaut) ; celui de la France s’établit à 110 pb par an, contre 300 pb pour l’Irlande, 325 pb pour l’Italie et 370 pb pour l’Espagne. Pour autant, et même s’il reste toujours beaucoup plus important que le CDS de l’Allemagne (54 pb), l’écart entre les emprunts d’états allemands et français s’est toutefois sensiblement réduit depuis le mois de mai, de plus de 1,4 % à 0,75 %. Cette baisse témoigne en partie de l’atténuation perçue des risques de défaut/d’éclatement de la zone euro après l’annonce du président de la BCE, Mario Draghi, de son engagement à faire tout ce qui était nécessaire pour sauver l’euro et de son programme d’achat d’emprunts d’État à court terme émis par des pays en difficulté ; mais, cette amélioration relative coïncide également avec l’élection de François Hollande en mai qui est ainsi devenu le premier président français de gauche de ces 20 dernières années.

François Hollande a été élu sur un programme promettant d’augmenter la pression fiscale sur les riches. Il a également promis de limiter le déficit budgétaire de la France. Dans ce contexte, le projet de loi de finances pour 2013 présenté la semaine dernière n’a guère surpris les français en prévoyant des efforts de rigueur répartis comme suit : un tiers en impôts sur les ménages, un tiers en impôts sur les entreprises et un tiers de réduction des dépenses publiques. Selon les estimations de Goldman Sachs, le taux des prélèvements obligatoires en pourcentage du PIB augmentera de 44,9 % à 46,3 %. Mais, même ce tour de vis budgétaire relativement agressif (et les projections sont basées sur une croissance du PIB supérieure à un niveau jugé possible par beaucoup, surtout au regard de ce même durcissement budgétaire et du climat d’austérité) n’empêchera pas le ratio dette/PIB de franchir le seuil des 90 %. Pour rappel, ce seuil des 90 % est celui qui, selon Rogoff et Reinhart, compromet significativement la capacité d’une économie à croître. Toutefois, si la rigueur budgétaire « fonctionne », la France devrait alors renouer avec un budget équilibré d’ici 3 ou 4 ans.

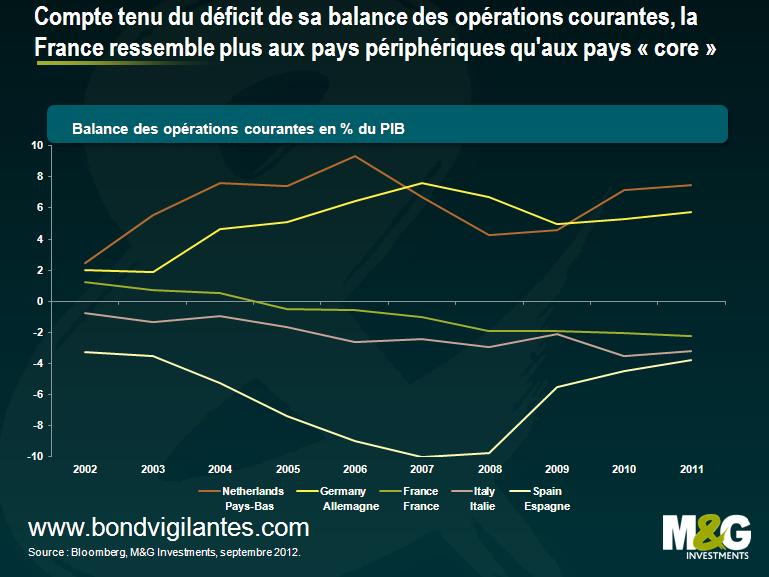

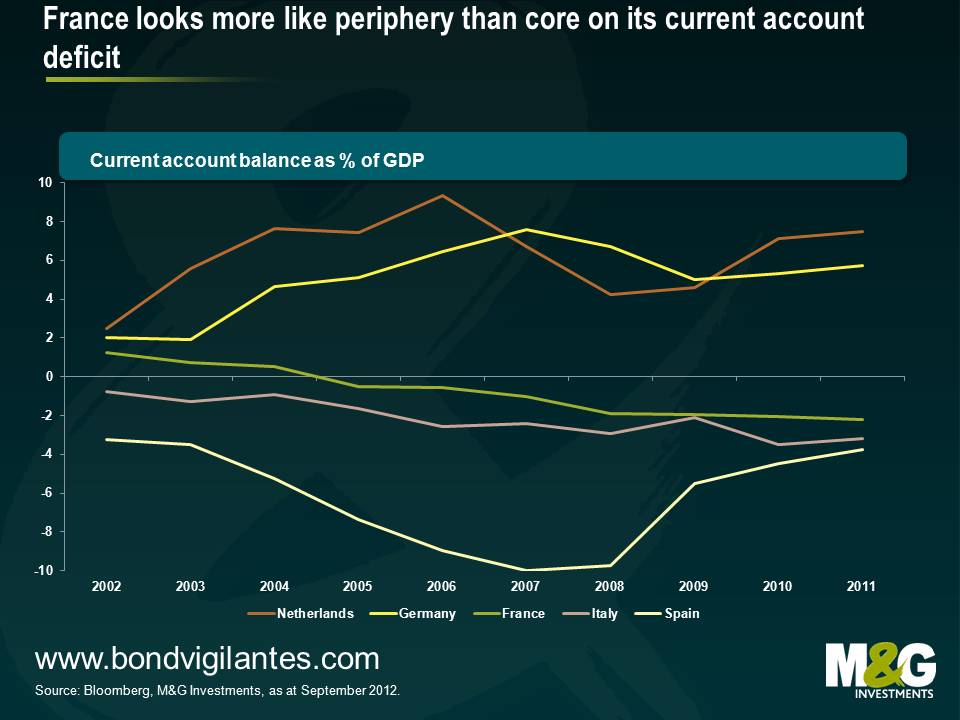

Mais, revenons à la capacité de la France à combler son déficit budgétaire par la croissance. La compétitivité de l’économie française est un point qui continue de nous préoccuper. Le déficit de la balance des opérations courantes de la France est considérable, ressemblant ainsi plus à celui de l’Espagne ou de l’Italie qu’à celui de pays du coeur de l’Europe comme l’Allemagne ou les Pays-Bas (mais, il n’est pas aussi important que le déficit de 5,4 % du Royaume-Uni, la raison principale pour laquelle nous pensons que la livre sterling est extrêmement surévaluée).

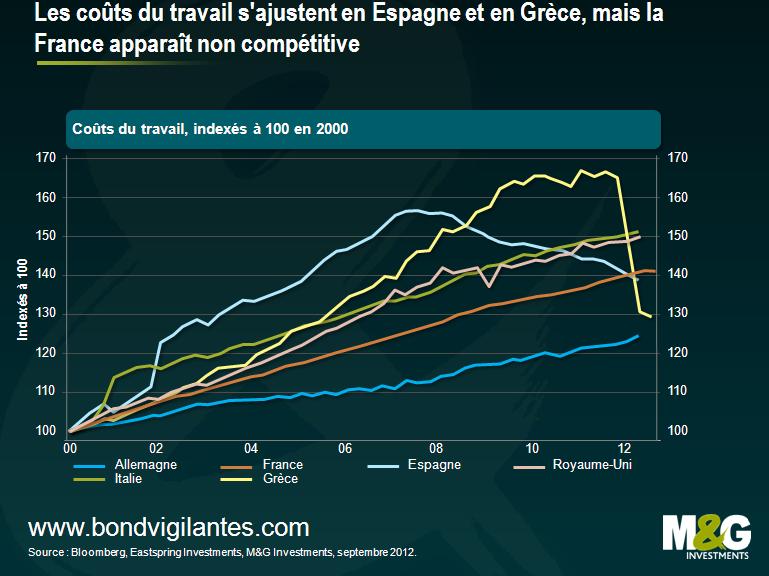

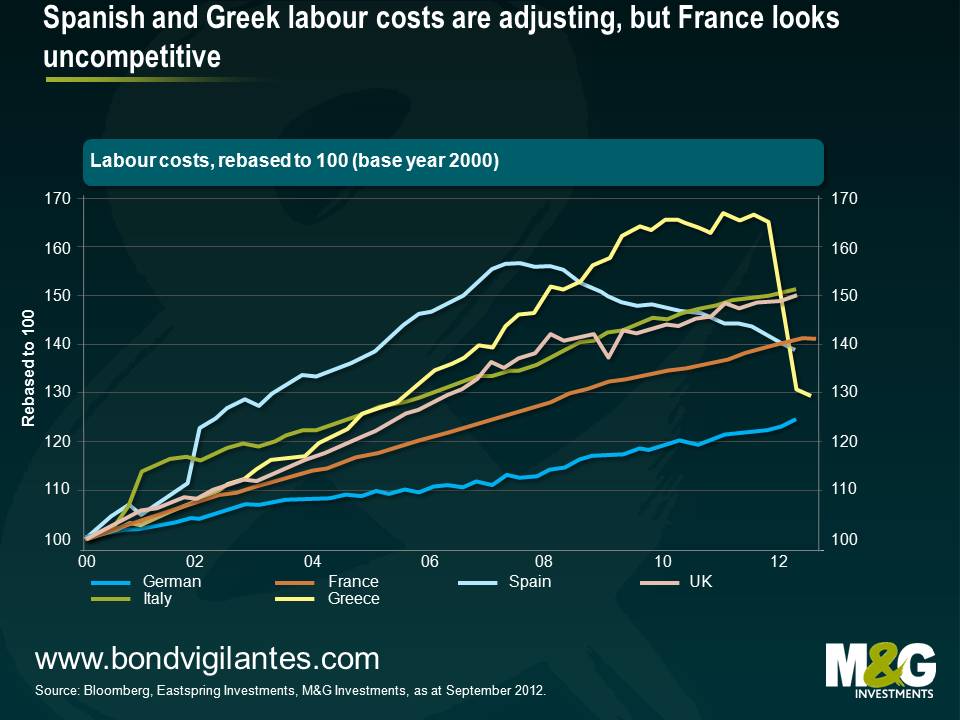

Dans un modèle économique typique, un pays accusant un tel déficit de sa balance des opérations courantes dévaluerait sa devise afin d’aider ses sociétés exportatrices. Mais la monnaie unique de la zone euro ne le permettant pas, c’est donc une dévaluation interne qui doit plutôt se produire. Depuis la création de la monnaie unique, l’économie allemande a surperformé, principalement à la faveur de la vigueur de ses exportations. Ceci n’a pas été une coïncidence – après l’effondrement du mur de Berlin, les entreprises allemandes ont convenu avec les syndicats (une sorte de néo-corporatisme dans le cadre duquel le gouvernement, les sociétés et les salariés sont des partenaires sociaux au sein d’un système capitaliste) de limiter la croissance des salaires et ce faisant, d’empêcher la délocalisation de l’activité manufacturière en Orient où la main-d’œuvre est meilleur marché. Ainsi, au cours des 12 années écoulées depuis la création de la monnaie unique, le coût du travail en Allemagne a augmenté de moins de 25 %, contre 65 % en Grèce, 55 % en Espagne et 40 % en France. Par rapport à l’Allemagne, le coût du travail en France s’est donc renchéri de 15 % ou plus, une détérioration significative de la compétitivité du pays parmi les États du « noyau dur » de l’Europe.

Il est clair qu’une « dévaluation interne » intervient en Grèce et en Espagne où les coûts du travail connaissent une véritable chute (alors que le chômage s’envole). Je n’affirme pas qu’il s’agit là d’un élément positif – à moyen terme, cela va permettre de stimuler les exportations à mesure que les usines se délocalisent dans les régions où les coûts sont moins élevés ; mais, à plus court terme, le frein que cela aura sur la croissance espagnole et grecque pourrait bien s’avérer être le médicament qui tue le patient au lieu de le guérir. Mais si jamais il y a des capitaux à investir dans des usines, des équipements et des hommes en Europe, et si l’incertitude se fait moindre, prendront-ils le chemin de la France ou d’une Espagne restructurée et à plus bas coûts ?

Et une austérité budgétaire musclée et affirmée publiquement ne semble pas être une politique qui donne des résultats probants – à l’image du Royaume-Uni où moins de 10 % des réductions de dépenses projetées par la coalition sont effectifs à ce jour ; pour autant, l’impact psychologique sur l’économie a été sévère et depuis le début de la crise du crédit l’économie britannique a sous-performé non seulement les États-Unis (où de bonnes vieilles mesures de relance keynésiennes ont été mises en œuvre), mais également la zone euro considérée par beaucoup comme une région économiquement dévastée qui, néanmoins, a surperformé le Royaume-Uni de près de 2 % du PIB sur la période (et qui dans son ensemble présente aussi un ratio dette/PIB inférieur).

Les perspectives de la France s’annoncent des plus difficiles sur le front budgétaire – générer de la croissance (ou faire défaut) a toujours été la meilleure recette pour réduire l’endettement public, et même un taux de croissance réel optimiste de 2 % par an (provisoirement fixé par le gouvernement à partir de 2014) n’est pas synonyme d’une réduction notable du ratio dette/PIB – nul doute que le niveau de 40 % à 50 % que nous avons l’habitude d’associer à une économie notée AAA ne semble pas être pour demain. Il se pourrait que la sensible contraction de l’écart entre les rendements des emprunts d’État de la France et de l’Allemagne (pays noté AAA pour le moment encore) se soit révélée excessive. Les risques économiques et sociaux potentiels futurs sont pléthores pour la France – n’oublions pas que le Premier ministre espagnol Mariano Rajoy a été élu sur un programme de consolidation budgétaire et qu’il a fallu moins d’un an avant que les Espagnols ne changent d’avis sur la question.

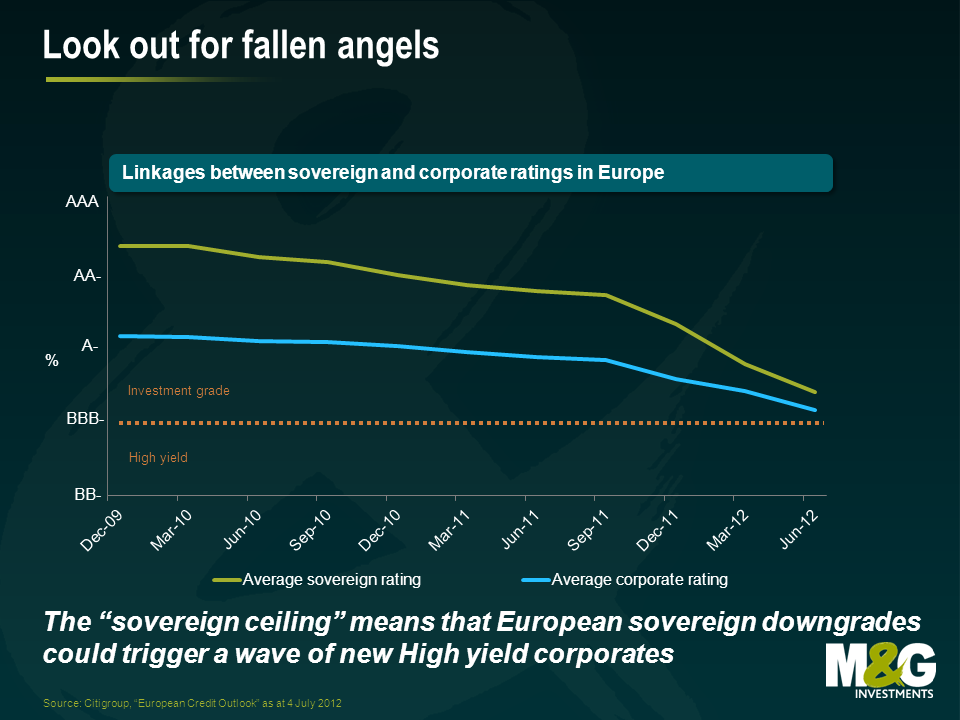

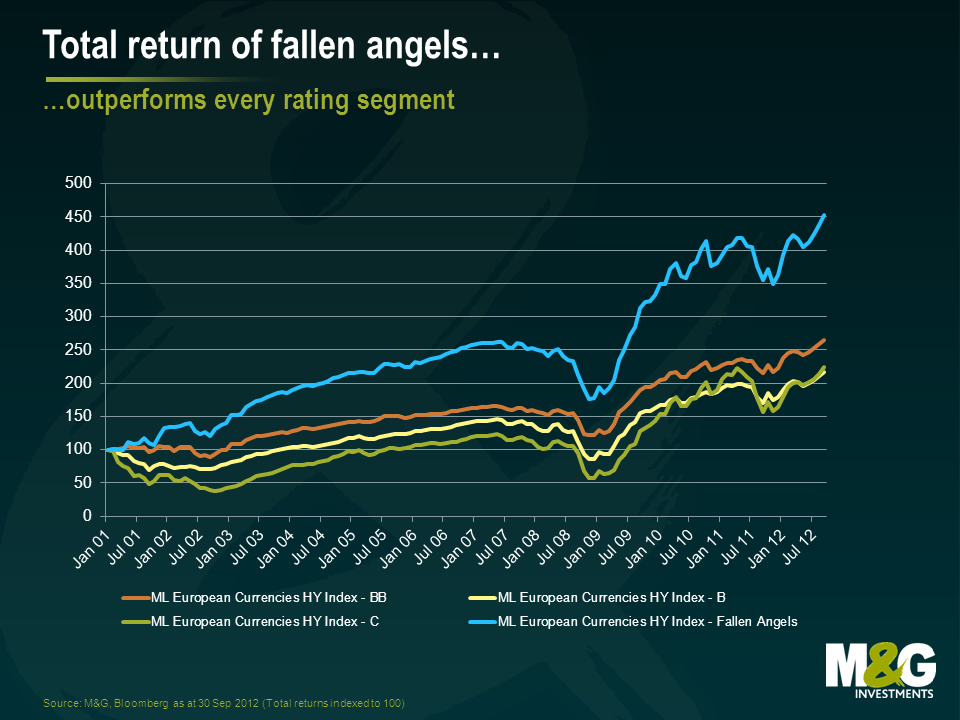

Earlier this year, Stefan highlighted the potential for sovereign debt downgrades to push big European companies into high yield territory becoming “fallen angels”, issuers downgraded from investment grade to high yield. This is something the Financial Times has also recently picked up on. The chart below shows how near the average European sovereign ratings are to sub-investment grade.

Rating agencies have flexibility in “capping” corporate ratings to the sovereign ratings of their respective home countries – the so-called sovereign ceiling. S&P for example has no strict limit on the number of notches by which an entity’s rating can exceed the sovereign but Moody’s is less generous, allowing a maximum two-notch rating uplift versus the sovereign for non-financials (the maximum is one notch above for financials). The reality is that a strong credit worthiness correlation tends to exist due to the likely exposure of companies to their domestic economy, and the ability of the sovereign to tax them (or worse) if necessary.

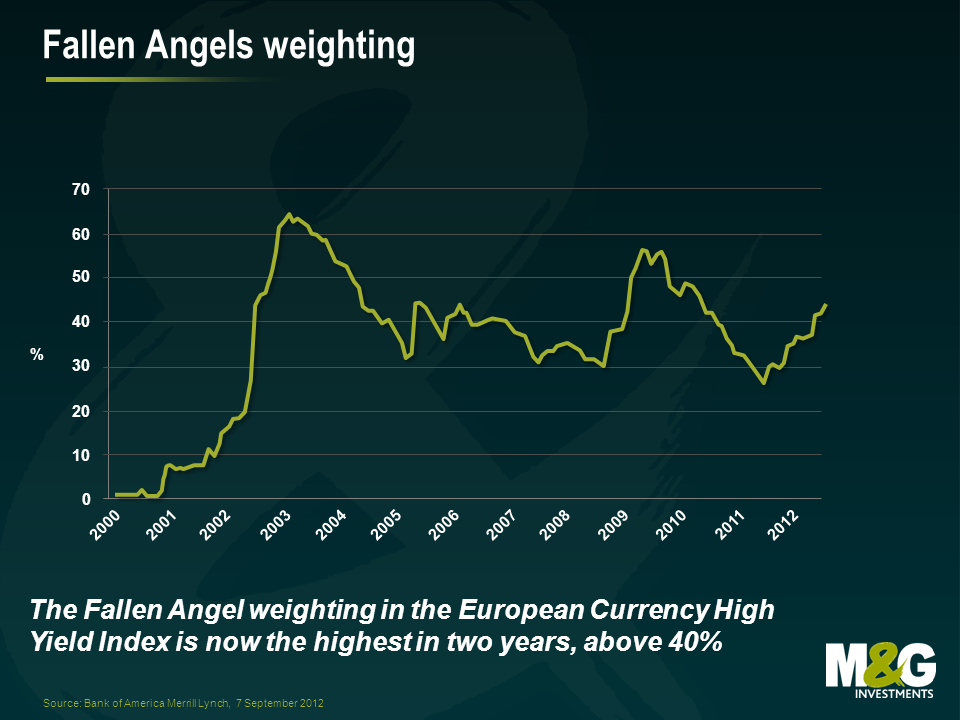

Where the market is not focusing enough is on the current role of existing fallen angels – companies that migrated from an investment grade index into a high yield index since the beginning of 2012. So far this year the fallen angels weighting in the Bank of America Merrill Lynch European Currency High Yield Index has increased by approximately 15% to 43.66%, the highest it has been in over two years.

What is even more interesting is fallen angels’ contribution over time to total return.

Fallen angels have significantly outperformed the original issue high yield portion of the index over time, whether you look at annualised returns over the last 3, 5, 7 or even 10 years (+2.59%, +3.70%, +2.87% and +3.24%, respectively).

Now, many future fallen angels may be different from their predecessors from a credit quality point of view. In the past, downgrades pushing corporates and banks down to high yield were mainly due to company-related issues: worsening balance sheets and poor revenue outlook. They were therefore as risky a bet as the rest of the universe.

Is this still true today? Well, reviewing the list of fallen angels in 2012, 41 out of the 110 European securities downgraded to high yield were due to sovereign downgrades (specifically from peripheral Europe – Spain, Italy and Portugal). This is equal to 37% of the total downgrades: more than one third of the total. This increase in the fallen angel population due to “externalities” (i.e. sovereign downgrades due to the eurozone debt crisis, rather than for the intrinsic worsening of their performance) has a potentially significant impact on the BB segment of the high yield market. Arguably, this increases the underlying quality of the market and, if historical risk/return characteristics hold, this could have a beneficial impact for high yield returns in general. On the other side, given the higher underlying quality of these downgraded issuers (lower leverage, better cash flows, global scale) their yields may be lower upon entering the high yield indices, and the potential for subsequent performance may be weaker than with “real” junk.

Since the start of 2011 French economic growth has been extremely disappointing, falling from an annual rate of nearly 2.5% to just 0.3% in the second quarter of this year. Of course the whole Eurozone has seen weakness over the period, but French growth has lagged that of the “core” over the period. German GDP growth was at or above 2% for all but the last two quarters, and now stands at 1%. Purchasing Managers’ surveys for September show more divergence, with more falls in French manufacturing and services, whilst the German surveys strengthened.

Of course, it could be worse – Greece, Portugal, Spain, and Ireland have experienced much weaker economic growth and, perhaps most damaging, higher rates of unemployment. Spanish unemployment has risen from 8% in 2007 to 25% today, with youth unemployment over 50%. The French jobless total stands at “just” 10.3%. And the other big difference is that the bond markets believe that France is part of the core, not part of the periphery. Looking at 5 year CDS rates (the cost in basis points to insure a sovereign bond against the risk of default), France trades at 110 bps per year, compared with Ireland at 300 bps, Italy at 325 bps and Spain at 370 bps. And whilst this is still much wider than German CDS at 54 bps, since May the spread between German and French government bonds has narrowed significantly, from over 1.4% to 0.75%. Part of this reflects the perceived reduction in general Eurozone default/breakup risks following ECB president Draghi’s assertion that he will do whatever it takes to save the Euro and his plan to buy short dated government bonds of nations in distress, but this relative improvement also coincides with the election of Francois Hollande in May, when he became the first leftwing French president in two decades.

Hollande was elected on a platform of putting up taxes on the rich. He also pledged to cap France’s budget deficit. As such last week’s Draft Budget Law (PLF) for 2013 did not surprise the French population – there will be a fiscal tightening made up a third from household taxes, a third from corporate tax rises and a third from spending cuts. Goldman Sachs estimates that the tax take as a percentage of GDP will rise from 44.9% to 46.3%. But even this relatively aggressive tightening of fiscal policy (and the projections are based on GDP growth higher than many believe is possible, especially in light of that same fiscal tightening and a climate of austerity) doesn’t prevent debt/GDP from rising above 90% in 2013. Remember that 90% is the level that Rogoff and Reinhart say delivers significant damage to an economy’s ability to grow. But if the fiscal austerity “works”, France should be moving towards a balanced budget within 3 or 4 years.

But back to the ability of France to grow its way out of a fiscal hole. Competitiveness is something that continues to worry us about the economy. The French current account is sharply in deficit, looking more like Spain or Italy than the “core” of Germany or the Netherlands (but not looking as bad as the UK’s current account deficit of 5.4%, the most important reason we think that the pound is massively overvalued).

In a typical economic model, a country with a current account deficit like this would devalue its currency to help its exporters. The single currency zone of the Eurozone doesn’t allow this to happen, so instead an internal devaluation has to occur instead. Since the creation of the single currency, the German economy has outperformed, with strength in exported goods leading that strength. This was no accident – post the collapse of the Iron Curtain, German companies had come to agreements with trade unions (a kind of neo-corporatism in which the government, companies and workers are social partners in a capitalist framework) to have wage restraint and thus keep German manufacturing from heading east to the cheaper labour supply. It meant that in the 12 years since the creation of the single currency, German labour costs rose by less than 25%. In Greece they rose by 65%, Spain 55% – and in France by 40%. Relative to Germany then, French labour costs had risen by 15% more, a significant deterioration of relative competitiveness within the core of Europe.

It’s clear that the “internal devaluation” is occurring in Greece and Spain, with labour costs falling sharply (as unemployment rockets). I’m not arguing this is positive – in the medium term it will stimulate exports as factories relocate in lower cost regions, but in the nearer term the drag this will have on Spanish and Greek growth could be medicine that kills its patient. But if there is capital to invest in plant, equipment and people in Europe once, and if, uncertainty fades, would it go to France, or to lower cost, restructured Spain?

And aggressive, publically stated austerity doesn’t appear to be a policy with great results – look at the UK where we’ve done less than 10% of the spending cuts that the coalition have planned, yet the psychological impact on the economy has been severe, and since the credit crisis began the UK economy has underperformed not just the US (where they did some good old Keynesian fiscal stimulus) but also the Eurozone, which is widely regarded as an economic disaster area here despite it having outperformed us by about 2% of GDP over the period (and having a lower debt/GDP level too, if you took the region together as a whole).

So the challenges to the French fiscal outlook are enormous – delivering growth (or defaulting) has always been the most successful method of reducing government indebtedness, and even an optimistic 2% per year real growth rate (pencilled in by the government from 2014) doesn’t deliver a significant reduction in the debt to GDP ratio – certainly the 40% to 50% level that we used to associate with a AAA rated economy seems a long way away. It may be that the aggressive tightening in French government bond yields to those of AAA rated (for the time being) Germany has gone far enough. There are plenty of economic and social buy-in risks to come for France – let us not forget that Spain’s Rajoy was also elected on a platform of fiscal consolidation, and it took less than a year for its population to change its mind about that.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.