Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

In old Siam (now Thailand), kings would ruin unliked courtiers by presenting them with a white elephant – supposedly a badge of honour, but actually a dung producing money-pit. As Wikipedia describes it, nowadays a white elephant is an idiom for “a valuable but burdensome possession of which its owner cannot dispose and whose cost (particularly cost of upkeep) is out of proportion to its usefulness or worth”. The AAA credit rating that Moody’s gave to the UK was one such white elephant. A nice trophy to have, but one where the government believed that costs of upkeep included extreme austerity, now and into the future. The good news is that Moody’s has downgraded the UK, and best of all, has done so ahead of the Budget in March. The white elephant is dead, and now George Osborne can do a bit of fiscal stimulus – housing and infrastructure spending have huge positive growth multipliers, and can be justified easily, especially whilst gilt yields are so low. And if all else fails, we can always “QE” the yields lower still…

In this conference call from this morning, I look at the downgrade, the UK fiscal outlook, and the implications for the markets. The link below takes you to the slide deck and the audio.

http://www.iviewtv.com/teleconference/uk-downgrade-reaction/

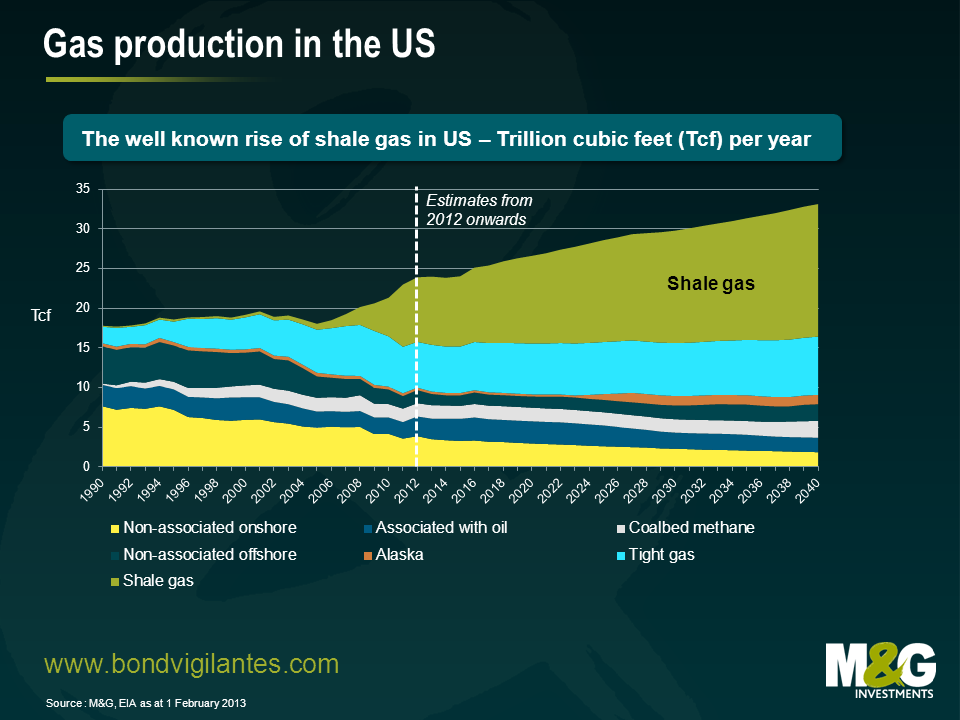

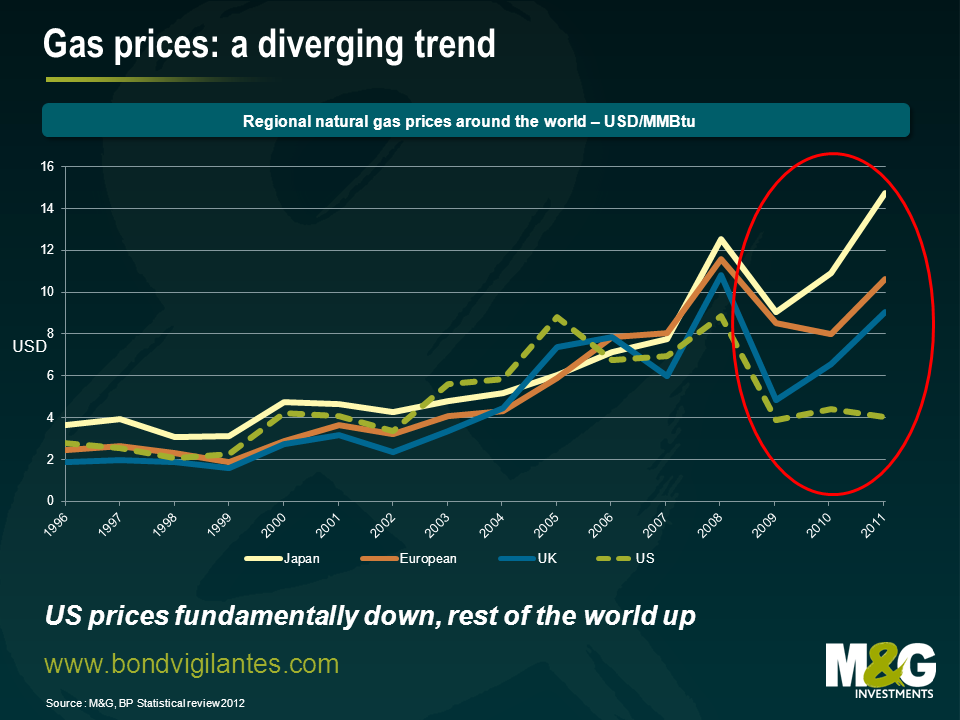

It is commonly believed that – thanks to shale oil and gas discoveries in the US over the past couple of decades – the US is on a path towards energy self-sufficiency. Subsequent cheaper gas prices are boosting competitiveness in some domestic industries, starting from bulk chemicals and primary metals, by lowering the costs of both raw materials and energy.

But will the US and its domestic companies be forever the only beneficiaries of cheap gas, as many believe? In Davos in January 2013, Royal Dutch Shell PLC signed a 50-year profit sharing deal with Ukraine to explore and drill for shale gas and oil. In fact, shale formations are not a prerogative of the US. Several countries in Europe and Africa have significant shale gas reserves (France, UK, Poland, Germany, Turkey, Ukraine, South Africa, Morocco, Libya, Algeria), and some other countries around the world too (Chile, Canada, Mexico, China, Australia, Argentina and Brazil). Preliminary research has shown that there are 32 countries with more than six times the amount of technically recoverable shale gas than the US. It will be key to understand which ones will prove of high “quality”: in fact US shale basins tend to have rocks closer to the surface (easier to reach) and more porous (where gas is easier to extract), while foreign reserves tend to be deep and harder to reach (therefore more technically challenging and expensive).

Currently in Europe the shale gas debate is divided between euphoria and total rejection. A drilling procedure called “fracking” sees a cocktail of water, sand and some chemicals pumped into a well under high pressure to force the gas from the rocks. Early drillings in Netherlands and Luxembourg were suspended because of environmental fears and contrarian public opinion. In France, fracking is now banned, while in Germany opposition to Angela Merkel is creating a good deal of noise around this topic. In Poland, ExxonMobil just walked away from preliminary explorations that didn’t deliver the expected results and, in Spain, the Basque local government has announced that there is 185 billion cubic meters of shale gas in the Gran Enara field with €40m invested in exploration.

No rapid breakthroughs are expected though. Exploiting shale gas reserves in Europe might be a long, technically difficult, politically tricky and also legally complex procedure, due to questions over property rights – determining who can drill and where. But the need to look for security of supply and cheaper energy sources remains. In particular, as Orlando Finzi – our M&G credit research director covering the energy sector – was telling me the other day, the latter is the subject of a key debate at the moment: EU long term gas contracts which supply most of the gas to Europe have prices linked to oil, but this might all change with recent negotiations between buyers and sellers seeing a modest dilution of the oil linkage. RWE, the German utility, is seeking full removal of oil price linkage in its Gazprom contract via arbitration courts. Where will European prices head to then? If lower, the idea of extracting shale gas may become less attractive than the existing natural gas options. If prices continue to rise, who knows? Also, the need to reduce CO2 emissions may push towards unexplored scenarios. Some think that the current CO2 emissions “cap and trade” system is disappointing (see the chart below): too many permits in the market and therefore no incentives to cut emissions.

Gas is a great alternative to other fossil fuels (and coal specifically, but also oil) to both cut down emissions and potentially to cover when renewables do not generate (for example, wind turbines in a period of no wind). Will European countries, eventually strangled by economic stagnation, fearful of security of supply and in need to cut emissions, find a way to overcome multiple issues to give a boost to shale gas exploration? In a positive political climate, what if UK and Spain will be quick and successful in exploiting their shale gas resources? Will this new energy source support growth, help employment in weak economies and make local companies more competitive in certain industries?

More euphoria is engulfing China. China’s revolution in shale gas is considered by some more a distant dream than a work-in-progress, but there are many new developments worth considering. Chinese public opinion has recently been shaken by the terrible air quality in many cities. China, estimated to have the biggest reserves in the world (50% more than the US as per an early research by EIA) is explicitly moving towards cleaner energy sources and has an incredible appetite for energy (and gas specifically, now fully imported). Even if little information exists, Petrochina, which is currently undertaking the development of shale gas in Alberta via a partnership with a Canadian company, has started shale gas drillings around China. Total is also preparing to sign an agreement, possibly within a few days, with a Chinese partner to explore for shale gas in the country. Furthermore, China just announced that 16 (only domestic) companies won a second round of bidding to explore 19 shale gas blocks around central China, agreeing to invest $2 bn over the coming years. The key issue also in China – and in some other countries such as Argentina and Mexico – will be to understand which technology to use and how to unlock reserves that are very difficult and expensive to reach for geological reasons: I would expect quicker progress only with foreign technology. But local energy needs, resolute politics and a more benign public opinion – now suffocated by smog – make the Chinese case stronger than Europe. If shale reserves are exploited quicker than expected, will China return to the good old days of double digit GDP growth? Will Chinese companies – which are losing their cost leadership position to neighbouring countries such as Vietnam and Indonesia or back to the US – find in local shale gas a new source of sustainable competitive advantage in the next ten years? Will the predicted shift of production and employment back to the US be a temporary adjustment only?

Reading the future of energy remains very complex. The prospects of shale gas developments outside North America will depend to a large extent on politics and developments in international gas markets, such as the future relationship between demand and supply, price relations (Liquified Natural Gas vs. pipelines for example) and movements, costs of production, shape of climate policies (it’s difficult to see how other countries such as Argentina, for example, will be able to persuade foreign companies to help it develop its reserves while it has been busy expropriating assets) and specific local challenges. But imagine a not-so-remote scenario at this point: US shale gas may return less than expected over the long term (as the EIA always reports, the long-term production profiles of US shale wells and their estimated ultimate recovery of oil and natural gas are uncertain), while China and Europe may start exploiting shale reserves quicker, thus reshaping energy pricing dynamics or even the balance of world trade and geopolitics.

I’d been feeling pretty pleased with myself since last Saturday – I managed to get Sky TV, broadband and a landline installed in my flat. That was until earlier today, when after discussing some of the recent activity in this sector with our telecoms and media analyst, I was left feeling something of a technology dinosaur.

These three services sold as a single package is called a “triple play” offer. However, I have since discovered that this is so 2010. These days it’s increasingly about “quad play”, whereby consumers access video, broadband and voice services both inside and outside the home. Inside the home is provided by your cable, copper telephone line and/or satellite dish whilst outside connectivity is provided by a mobile network. The most visible example of this business model in the UK comes from Everything Everywhere (EE), mostly due to their……um……interesting adverts featuring Kevin Bacon. EE allows a subscriber to make voice calls, surf the internet and watch video content either at home or on the move via a combined mobile and fixed line broadband connection. Advances in mobile technology (4G) now mean that seamlessly streaming a film in your house on your iPad as you eat breakfast and then on your journey to work should be possible. This is the direction the industry is moving in the UK, with Vodafone, 3 and O2 expected to launch later in the year once they secure the necessary 4G spectrum that is currently being auctioned. In the US and portions of Western Europe it is already there.

So quad-play has a clear consumer proposition, i.e. ubiquitous and fast media consumption and connectivity from a single service provider. But what benefit do the telecom operators derive from this service? Firstly, they hope to stem the revenue declines and customer churn they have experienced over the past few years as a combination of competition and regulation have ground down prices. Secondly, quad play offers them a cost saving opportunity by shifting data traffic off their mobile networks and on to their fixed line infrastructure as fast as possible, either via an in-home WiFi point or a fibre optic link to the network towers outdoors.

Generally speaking, in each country there is an incumbent telecom operator offering both mobile and fixed line services (the UK is an almost unique exception after BT spun off O2). However, there is also a swathe of mobile-only and fixed line-only operators in each market and hence consolidation in the face of this strong industrial logic seems inevitable.

Last Wednesday, press reports suggested that Vodafone is considering acquiring cable operator assets. Two firms seem to be in their crosshairs for now; Kabel Deutschland and ONO (which operate in Germany and Spain, respectively). Both companies’ bonds rallied on the news that they could be taken over by a company with a much stronger balance sheet – they are both high yield whilst Vodafone is solidly investment grade. We think that Kabel Deutschland would be a better fit but either way Vodafone is clearly interested in fixed line assets across Europe. Last year it bought Cable & Wireless Worldwide in the UK and its interest could also stretch to alternative fixed line network operators like Jazztel (Spain), Versatel (Germany) and Fastweb (Italy).

Similarly, Liberty Global, an international cable operator, recently made a bid for UK cable operator Virgin Media. Virgin’s bonds were weaker on the news as LGI is a lower rated entity than Virgin and plans to leverage the business to a level commensurate with its other European cable investments (UnityMedia, UPC, Telenet). LGI already offers triple play services across its extensive European cable footprint but, along with the usual scale and tax synergies, Virgin brings with it significant experience in mobile as well as providing fibre optic connections to other UK operators’ mobile towers.

What can possibly come after quad-play? Internally we refer to what we believe is the next step as “penta-play”. This involves business models where service providers offer quad play delivery and services complemented by ownership of the content being consumed over those networks. The importance of control over content to a network provider was underlined by the US’s largest cable operator Comcast, with its $17bn purchase of the remaining 49% of NBC Universal it did not already own. If you think this is a US aberration, just think what would happen to Sky if it lost the Premiership contract and why BT has recently decided to park its tanks on Sky’s lawn with its recent expansion into Premiership football and rugby.

And after that? Well the regulators will probably demand these vertically integrated behemoths are broken up but that’s another story…. From a consumer’s point of view we think that consolidation and competition, to provide us with all our communication, entertainment and informational needs under one subscription, will eventually lead to lower prices for services previously purchased separately now being provided as a single service bundle. From a bond holder’s point of view the recent activity suggest M&A risk is on the rise with negative and positive impacts depending own whether you sit in the acquirer or the target, the better rated credit or the company with the weaker balance sheet, and your specific bond covenant protections.

My last research trip video to Asia was deemed by our marketing department to be so bad that we all had to be sat down and told what would be common sense to most people; apparently it’s not a great idea to speak to camera next to a busy airport runway, and you can’t see anything if you record yourself in your hotel room at night with the main lights off. So hopefully this effort is a slight improvement, although I still couldn’t resist a quick stint at Abu Dhabi International Airport, and the majority of it is filmed outside a shisha cafe in London.

You can view the video below.

The trip if anything strengthened my belief that parts of the Middle East debt market look very attractive relative to some of the massively overvalued emerging markets.

Abu Dhabi is said to be the Switzerland of the Middle East, and this appears to me to be largely justified. Abu Dhabi’s sovereign wealth fund is over US$600bn, which works out at almost US$100k per person. The big difference with Switzerland is in valuations. Many Swiss government bonds were until recently trading with a negative yield (meaning that investors were paying money to Switzerland for the privilege of parking their cash there), while the bonds of some AA rated Abu Dhabi state owned enterprises have higher yields than some junk rated EM sovereigns. The rating agencies’ assessment of the Abu Dhabi issuers looks broadly correct to us, so the valuations vis-à-vis EM sovereigns looks completely wrong.

Dubai remains a little worrying. It seems to see itself as Disneyland for adults; while I was out there reports surfaced of Dubai building its first underwater hotel, and yesterday plans were announced to build the world’s largest ferris wheel. Personally I don’t really get the attraction – it is a bit like going on holiday to Westfield Shopping Centre, not exactly my idea of a holiday – although there are many who disagree since apparently more people went to Dubai Mall last year than visited New York or Los Angeles.

Qatar perhaps sits somewhere in between. It is blessed with huge natural resources, but I’m still bothered on many levels why they bid for (and successfully won) the right to host the 2022 FIFA World Cup. The cost of hosting the FIFA World Cup is relatively trivial for Qatar; more concerning is that they are channelling quite a bit of money into economically and politically wobbly countries such as Egypt, and there are reports today that the Qatar sovereign wealth fund may invest $3.5bn in Russian bank VTB. Why?

I didn’t have a chance to visit Saudi Arabia or Bahrain, but some of the Emirati and Qatari banks provided interesting colour, suggesting they are concerned about investing or lending in Saudi Arabia given current valuations, and the ongoing unrest in Bahrain means that the country’s previous role as a regional hub has almost certainly been irreversibly ruined. In contrast to Bahrain, political unrest in Abu Dhabi, Dubai or Qatar is exceptionally unlikely given that the wealth effects of the economic boom have been widely distributed to the local population, and lower paid workers are on the whole migrant workers and are there voluntarily – if they don’t like it, they can leave.

PS I refer to avocado bathroom suites at the end of the video, but forgot to give Jim the credit for this point. See Jim’s blog from last year here.

Vince Cable has suggested that the government’s shareholding in Royal Bank of Scotland should be parcelled off to UK citizens. The UK government’s ordinary shareholding in RBS Group (A shares) today stands at 65.29%, which goes up to 81.15% including B shares (shares with priority over dividends).

Assuming the UK government would distribute A shares only, this would give us roughly 63 shares each that would be worth £222 based on yesterday’s closing share price of £3.54. This very simplistic way to dispose of the government’s ordinary stake could well be described as fair, though it would leave lots of individual holders and create administration and system chaos. Is there a better way? How can you reduce this administrative nightmare, make the give away more popular, or improve RBS’s future prospects?

How about simply having a lottery, as opposed to the shares being split? We could have a lottery based on the electoral roll for example. However, winners would get substantially more shares each, say 300,000, which at £3.54 a share would be worth just over a million pounds each. We could in effect create more than 13,000 new millionaires. It could maybe even be marketed as the Goodwin Lottery!

A second alternative would be to actually embrace free choice and the market economy via selling tickets for the lottery. This could not only create the same amount of millionaires, but would raise extra revenue for the government. The use of the existing Camelot lottery network would make that relatively efficient.

A third alternative would be to basically “de-mutualise” it. This would involve an open offer for sale of the government’s share holding to individuals, with all proceeds raised contributing to new equity for a new invigorated bank. This would act as a deeply discounted rights issue with the government stake being 100% diluted, and their huge loss being the new investors’ gains.

The ideal solution for the UK economy is to have a thriving competitive banking sector, at a minimum cost to the taxpayer. If the politicians decide the best way to do this is to simply give the shares away then hopefully they may improve their plan to get some of the potential benefits outlined above.

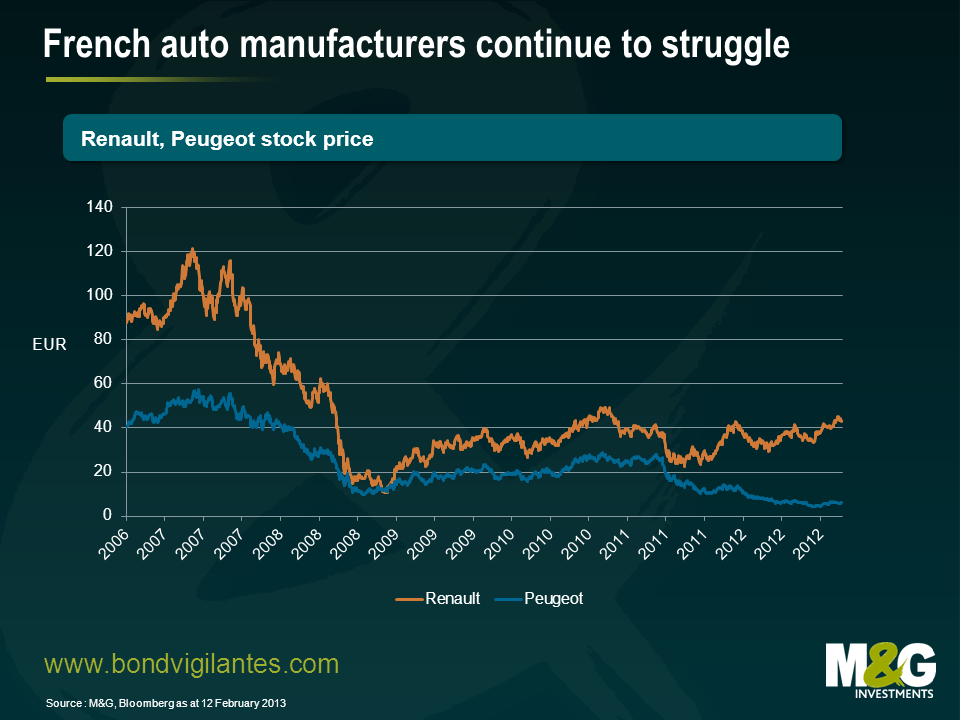

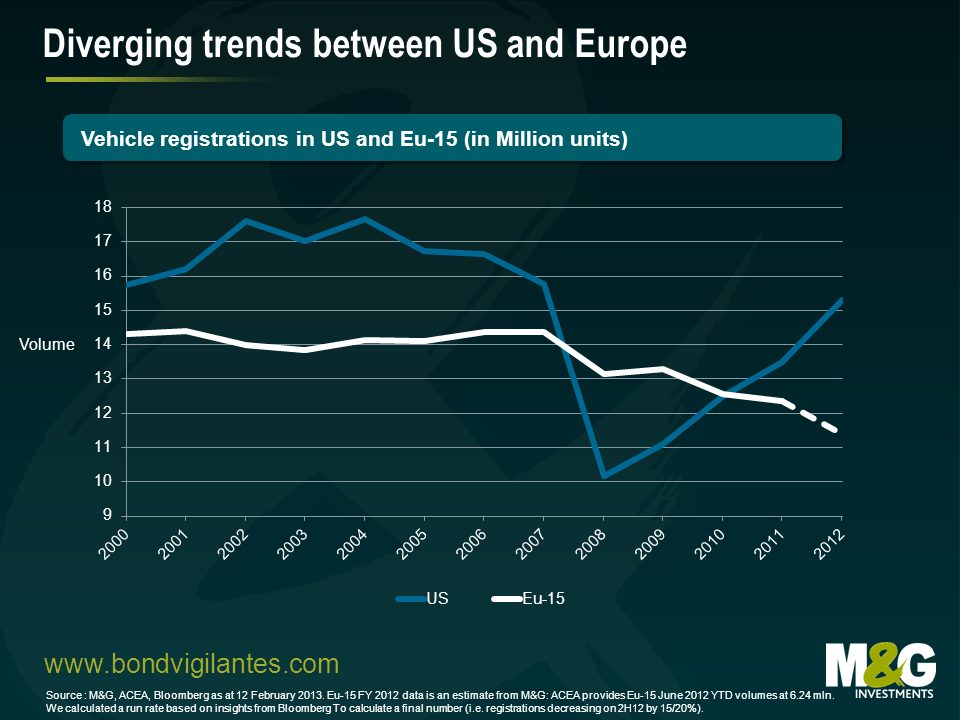

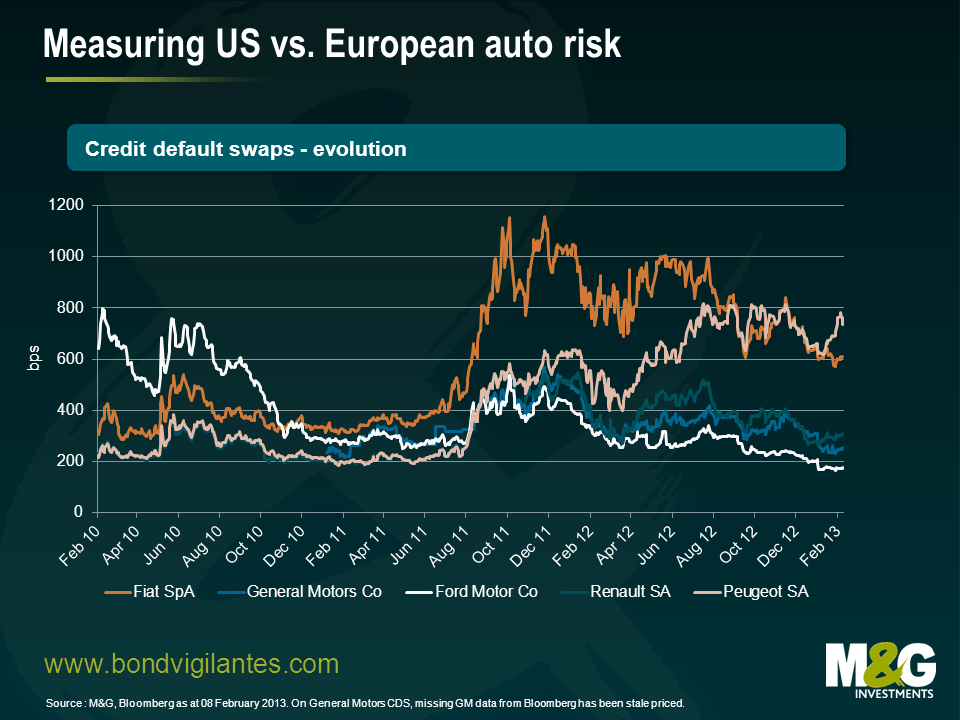

French auto manufacturers Peugeot and Renault report full year 2012 earnings this week. If Peugeot SA’s write down announced on Friday is anything to go by – when it took a €4.7bn non-cash charge – the outlook for the company and indeed other European focussed auto manufacturers continues to be a bleak one. European market conditions have been described by S&P as ‘dire’. Overcapacity and general economic uncertainty have resulted in utilisation rates below break-even profitability for a number of plants. Cash continues to be burnt and unsurprisingly, share prices don’t make for pleasant reading.

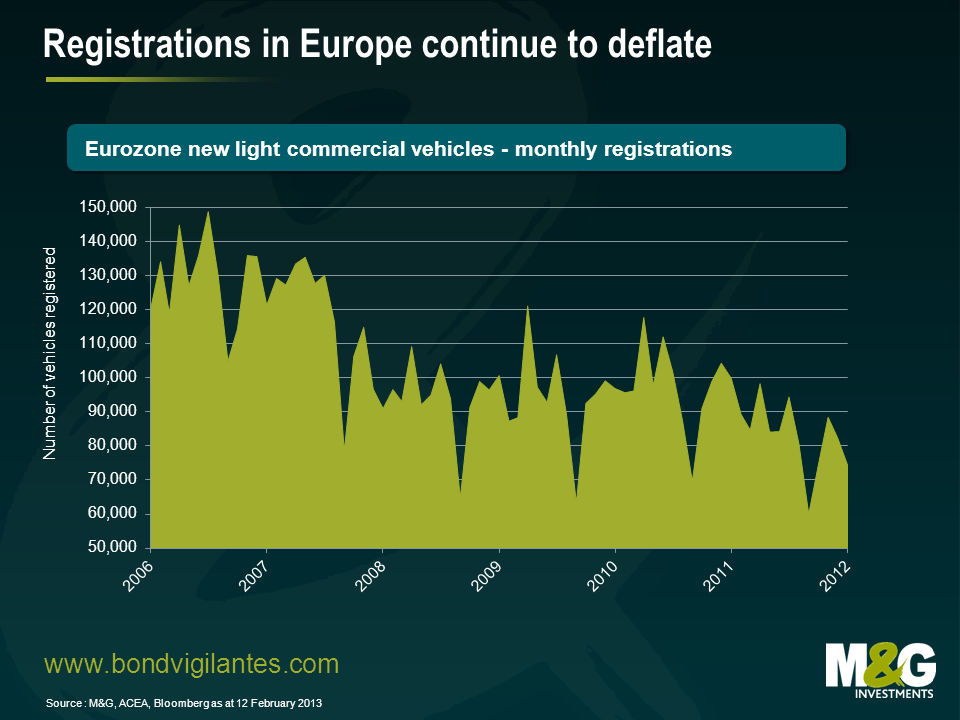

The need for an overhaul of the likes of Peugeot, Fiat and Renault remains acute. European light vehicle registrations are headed for a fifth consecutive year of declines (see chart below), Italian and Spanish registrations are at nearly half their pre-crisis levels, profit margins on compact vehicles are slim and Peugeot, Fiat and Renault are losing market share to investment grade rated manufacturers like BMW, VW and Daimler.

Struggling under a mountain of debt, Peugeot, Fiat and Renault find themselves in a non-too dissimilar position to that of the US auto manufacturers back in 2008/2009. Several years ago GM, Ford and Chrysler were able to successfully restructure, both inside and outside of bankruptcy, allowing them to close capacity, reduce over-indebtedness, renegotiate onerous union contracts and subsequently return to profitability even at levels of production significantly below those pre-crisis. That experience remains in stark contrast to European OEMs (Original Equipment Manufacturers) who continue to labour under many of those same pressures whilst facing ongoing weak domestic demand.

Management continues to struggle to right-size their businesses some 5+ years into the financial crisis in the face of strong political pressure and a determination to avoid job losses. Ironically, the very interference that has hampered change in Europe has now led to Peugeot having to rely on French state support. But these choices cannot be put off into perpetuity and unwelcome decisions are inevitable. Until that point in time, losses will continue to mount, cash will be burnt and creditors will likely favour US over European OEM risk.

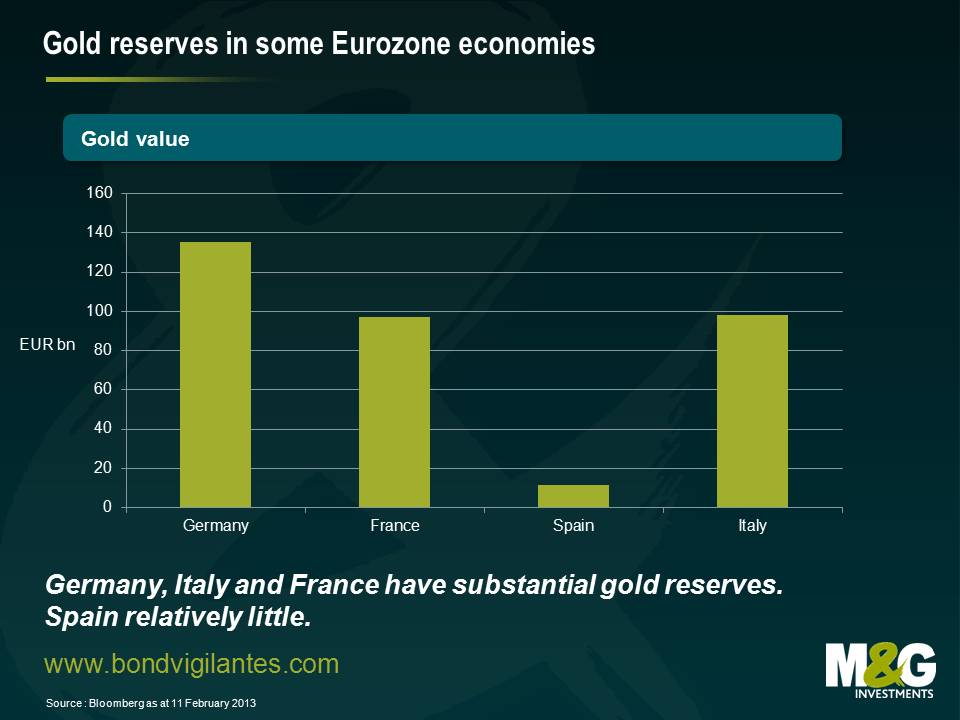

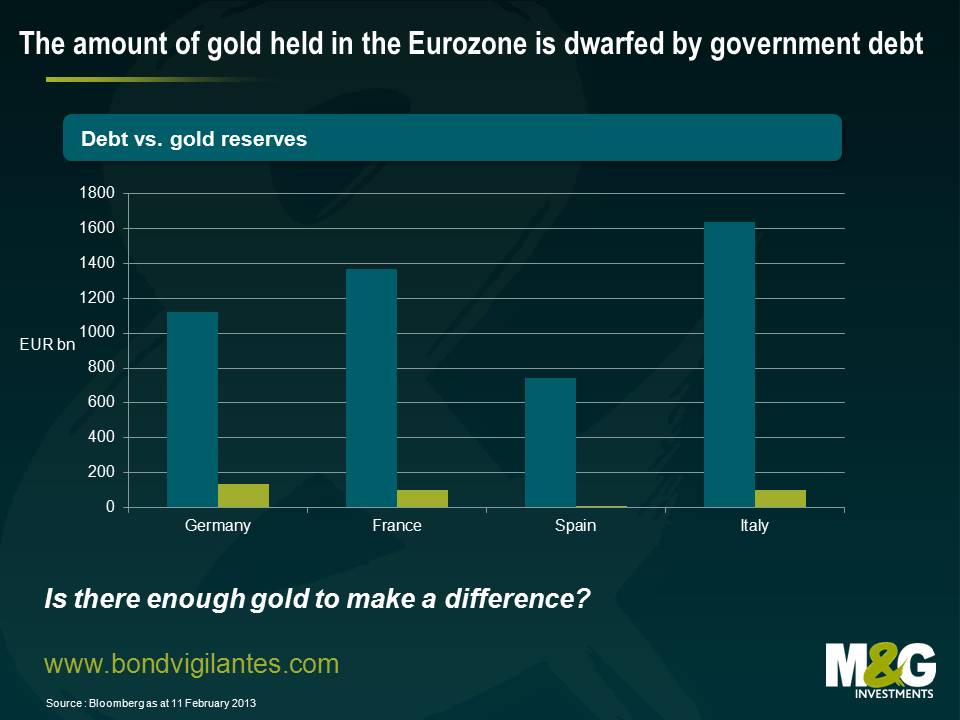

Last week we had Marcus Grubb of the World Gold Council come in to talk through the idea that Eurozone countries with high debt burdens and unsustainably high bond yields should unlock the value of their otherwise yieldless gold reserves by using it as collateral, and thereby borrow cheaply for at least that portion of their financing needs. The chart below shows that Germany (obviously one of the lowest yielding European members but here for interest), Italy, France and (to a much lesser extent) Spain have substantial gold reserves that could be used to collateralise European bond issuance.

When we show gold holdings against outstanding levels of government debt we see that Germany has the equivalent of 12% of its debt in gold reserves (and incidentally as has been widely reported is repatriating 674 tonnes of its gold held by at the Banque de France and the New York Fed back to Frankfurt following a public campaign). For Spain though it’s under 2%. For France and Italy around 6-7%.

I think we can agree that issuing a bond backed by gold reserves would lead to lower borrowing costs – BUT only on that portion of the debt. This would effectively subordinate the pre-existing debt, and any future unbacked bonds. If the existing debt is effectively backed by the assets and tax gathering capabilities of the state, then to remove the gold reserves from these assets is reducing the creditworthiness of the outstanding bonds. Their yields should adjust upwards as a result. This is a bit like a bank subordinating senior bond investors by pledging its best mortgage assets to a covered bond programme – the covered bonds may be AAA rated, but the existing senior and sub bonds are jammed down the structure. Therefore, pledging gold assets as collateral might even lead to a ratings agency downgrade for some Eurozone countries – Italy is rated BBB at the moment, so could get downgraded to junk status if it pledges too many assets to a different bond programme. An unintended consequence. Nevertheless, there might be a combination of much lower gold backed bond yields (which might trade as AAA rated?) and higher existing bond yields that delivers an overall lower funding cost.

But how much scope would you have to issue this gold backed debt? To act as proper AAA collateral, the value of the gold asset at the maturity of the bond should be expected to cover the redemption amount, with a degree of over-collateralisation to cope with volatility in the price. You can see from the chart below though that in the past ten years the price of gold has been roughly between $400 and $1800 per ounce. If you took that as a possible range (and you might want it to be wider still), then what you see today as Euro 342 billion of gold reserves might only be able to collateralise Euro 76 billion of gold bonds – almost too small to be significant? At a lower confidence limit for the volatility of the gold you would be able to issue more bonds, but at higher yields.

What other objections might you have against the concept? Well does it seem a little desperate? Unconventional funding methods imply that all is not well (one of the reasons why under Paul Tucker, the Bank of England’s debt issuance department – before that responsibility went to the DMO – made great steps to modernise the gilt market, doing away with gilts with embedded optionality and quirks, and producing a transparent auction calendar). I think you’d want to get a highly rated issuer like Germany to issue a gold backed bond first, to establish a precedent, before the countries that might actually need to borrow like this did so. Secondly, since Draghi’s “whatever it takes” speech, yields for Italy have fallen from 6% to 4.5% at 10 years, and in Spain from 7% to 5.5% – Open Mouth Policy without any real action has done far more for these countries’ borrowing costs than anything practical. Thirdly, having a claim on gold is not the same as having gold. To invest in such a bond you’d probably want the gold backing the instrument to be held outside of the country involved (and probably outside the Eurozone itself), for example in a custodian vault in Switzerland. Why would a country default on its debt but then send out truckloads of gold to bond investors around the world? My guess is that it would be disinclined to do so. Finally, our Central Bank Regime Change thesis suggests that the authorities will use their ability to create fiat money as a means of economic stimulus and (whisper it) debt reduction. A move towards gold, and its historical ties to the 1930s Depression, seems to be a move in the opposite direction to that desired.

So in summary, I don’t think that the Eurozone economies have enough of this shiny metal to make a difference to their funding costs, and given that, why do something that looks desperate that will cause angst for your existing bond investors and possibly raise your overall cost of funding if it goes down badly?

Incidentally, bonds backed by gold are not a new thing, although they have been out of fashion for a couple of decades. In Tom Wolfe’s Bonfire of the Vanities (1987) Sherman McCoy is trying to buy $600 million of the French gold-linked Giscard bond, and it’s also discussed in Michael Lewis’s Liar’s Poker. The French issued four billion francs worth of gold indexed Rente Giscard bonds in 1973 – they were repayable in 1988 at either par, or 95.39 grams of gold for each 1000 franc note if the link between the franc and gold was severed in the lifetime of the bond, which it was. Sadly for the French government the gold price over the period (of high inflation) rose from around $100 per ounce to over $400 per ounce in the late 1980s. Thus the liability for the French rose to 53 billion francs. This was 1% of gross national product and 5% of government spending. This contemporary newspaper account suggests that the cost was £100 for every man, woman and child in France, and that were the debt to be settled in the metal itself it would equate to six months of global gold output. Some emerging market economies have used their gold reserves as collateral against loans before – South Africa engaged in gold swaps in the early 1980s for example. So the idea’s time might come again.

When deciding economic policy, the buck, so to speak, is left with a combination of the chancellor and the Bank of England. This arrangement exists as politicians should have the final say in a modern democracy, but a modern democracy needs to have a brake on populist politicians, hence an independent central bank.

Today those worlds publicly collide, with Mark Carney, the next governor of the Bank of England, appearing in front of the Treasury Select Committee. This will hopefully give the markets and politicians a flavour of his approach to dilemmas the Bank of England currently faces given the UK’s current economic malaise. What kind of policy will Carney follow? Is he a natural dove or a hawk?

Well at a guess, he has been appointed by a chancellor who wants economic recovery for the benefit of the country, and from a political point of view, an economic recovery that will keep him and his party in power. It would therefore be fair to assume that when interviewing for the position, any respected German central bankers’ applications would have been put straight in the bin.

One can therefore assume that Carney has been chosen to reflect the need at this point of the electoral cycle for a bit of an economic boost. Indeed, yesterday Osborne was calling for a more dovish stance from the Bank of England.

Politicians in the UK have played loose with fiscal and monetary policy over the years. Did we join the ERM in 1990 to drop interest rates to help the conservatives retain power in 1992? A tightening of monetary policy by the creation of an inflation targeting Bank of England in 1997 aligned the economy to the electoral cycle in Tony Blair’s first term. The amendment of the CPI target by Gordon Brown in 2003 brought a handy monetary stimulus ahead of the 2005 election. Given the election is a couple of years away and monetary policy works with a general lag of 18 months, what is the chancellor to do two years ahead of the election this time?

It is an ideal time for him to meddle with monetary policy. With the changing of the guard at the Bank of England he will be able to liaise with a new governor to undertake reforms to make the economy work better, and therefore increase the chance of re-election. The simplest way to boost the economy in the short term is to change the inflation target. This can be explicit, or disguised amongst the current statistical reform of RPI and CPI measures.

The surprise for the markets over the next year could well be a combination of a flat economy encouraging a politically motivated chancellor, and a new central bank head keen to make an impression in his new job, working together to engineer higher growth and higher inflation via an explicit loosening of the inflationary target in the UK.

We have been talking about the emergence of, and the effects of, the financial crisis in our blogs for a number of years now. However, more than 5 years into the crisis even we can be surprised. On Friday the Dutch government nationalised SNS, as capital injections from the private sector failed to appear. This action was undertaken to maintain the stability of the Dutch financial system.

This legal manoeuvre involved a confiscation of all SNS equity and group and bank level subordinated debt by the authorities, and an injection of cash into the bank. The holders of the aforementioned equities and bonds quite simply no longer have these securities. To paraphrase Monty Python, they are ex securities. Investors have lost all legal rights. Instead, they have been offered potential compensation based on the value that the Dutch government ascribes to the securities. However, their judgement of what that amount may be is highly likely to be zero.

We have examined many times the potential weakness embedded currently in financial issuers and how the tiering of debt is becoming more significant for investors. Before the financial crisis, senior and subordinated debt from the same bank were seen as equal under all circumstances except an event of default, in which case the senior bonds would see better recovery values. The fact that for systemic reasons the authorities wouldn’t want the bank to stop operating meant that subordinated debt benefitted from the halo effect of the perceived need to sustain the bank for the benefit of the financial system. However, since 2008, countries all over Europe have been putting in place legislation, in the form of so called “resolution regimes”, to allow them to deal with failing banks, without necessarily having to keep the whole bank going. This use of these recently introduced new laws in the Netherlands allowed the authorities to separate the claims of subordinated bond holders from those of other, more senior, bond holders. This is something we have not encountered before in this form (for example, while the UK government did nationalise the preference shares as well as the equity of Northern Rock, it didn’t actually nationalise the subordinated debt, whereas in Denmark a different approach was followed, leaving bondholders on the wrong side of a good bank/bad bank split). This Dutch approach allows for the quick and efficient bailing in (writing off) of subordinated debt and allows the bank to continue operating, thereby protecting the financial system.

‘Going Dutch’ is an expression used when you agree to share a restaurant bill. However, going Dutch SNS style means subordinated bond holders pick up the tab, as they have been eliminated, losing all the capital value of their investment. They have explicitly provided 1 billion euros of capital to help the ongoing health of the Dutch financial system.

Early intervention of this sort to protect the financial system is obviously bad news for subordinated bond holders, with their status becoming more equity and less bond like. It will be interesting to see what the market and the rating agencies think of this new approach in the ongoing battle to support the financial system. Is it a one off, or something we are going to come to see as common practice?

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.