Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

In recent years the use of capacity utilisation (CU) as a leading indicator for inflation, and hence for interest rates, has fallen somewhat out of favour. The large amount of spare capacity in the developed world in 2009-10 failed to translate into the substantial deflation that many had anticipated. Most economists and investors are eagerly focussing on U.S. labour market data instead, given that the Federal Reserve has tied its interest rate policy to an unemployment rate threshold of 6.5%. So, is it time to throw CU into the dustbin of economic history once and for all? This might be premature; ignore CU at your own peril.

Every month the Federal Reserve Board produces a CU percentage figure for industries in manufacturing, mining and utilities by essentially dividing actual output by capacity, i.e. a maximum sustainable output level. In general, capacity figures are derived from physical product data from government and trade sources or, if actual product data is unavailable, from responses to the Bureau of the Census’s Quarterly Survey of Plant Capacity. The basic rationale behind using CU figures as a leading inflation indicator reads as follows: in economic boom times factories tend to bring their output closer to full capacity, which places growing strains on their goods-producing capital. Excess demand and lack of supply, in combination with failure of stressed equipment, can lead to product shortages, sparking price increases and inflationary pressures. A more detailed explanation can be found in chapter 4 of Richard Yamarone’s book “The Trader’s Guide to Key Economic Indicators” from 2012.

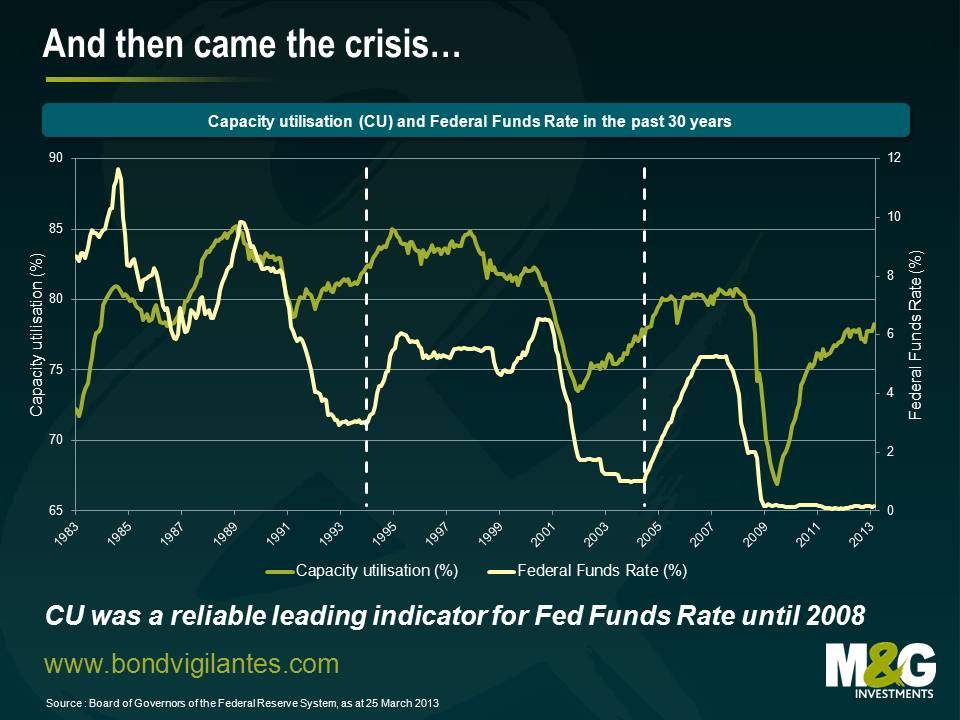

Prior to the financial crisis in the late 2000s, the Fed apparently followed this line of argumentation. As the first chart shows, major hikes in the Federal Funds Rate, e.g. the January 1994 and July 2005 rate hiking cycles, marked by white dotted lines, followed periods of rising CU numbers. However, from 2008 onwards this relationship has clearly broken down. Although CU has risen by more than 11 percentage points from 66.9% in June 2009 to 78.3% in February 2013, the Fed Funds Rate has been kept close to zero. One could argue that despite this remarkable CU growth, i.e. reduction in spare capacity, in recent years the absolute CU level is still below the psychologically significant 80% threshold. For instance, the 1994 rate hike, and the subsequent “death of the bond market”, began at a considerably higher CU level of 82.4% (January 1994). However, I do not find this argument particularly convincing, considering that the Fed’s most recent major rate hiking cycle started at a CU level of only 77.9% (July 2004), 0.4% below the current figure.

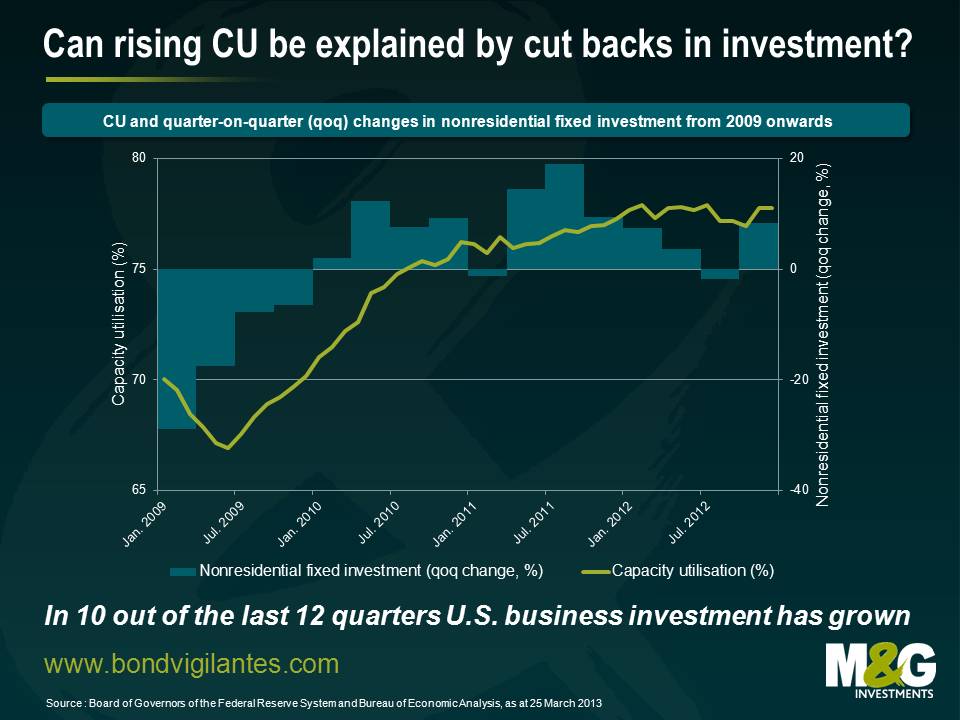

Another aspect worth exploring is the relationship between CU and business investment spending. Maybe U.S. companies have simply slashed their investment plans and decided to run down their plants and equipment after the financial crisis, scared to invest their cash safety blankets. In this case, rising CU numbers would merely be an artefact and no indicator for economic recovery and inflationary pressure. The second chart shows both CU and quarter-on-quarter (qoq) changes in non-residential fixed investment for 2009 onwards. With increasing CU figures, investment changes get less negative in 2009 before they enter positive territory in Q1 2010. Throughout the following three years, business investment has grown in 10 out of 12 quarters. Slightly negative qoq changes of -1.3% and -1.8% were recorded in Q1 2011 and Q3 2012, respectively. It should also be noted that the decline in qoq investment changes from Q3 2011 to Q3 2012, which was addressed in a Wall Street Journal article from November 2012, has come to an end by jumping to +8.4% in Q4 2012. Considering this pattern of investment spending, recent CU increases cannot be explained by cut backs in business investment. Therefore, I believe that the rise of CU is indeed a strong sign for an ongoing recovery of the U.S. economy.

In conclusion, although at the moment the Fed seems to be preoccupied with the unemployment rate, I believe it is worthwhile keeping an eye on CU. If CU continues to rise, while being backed up by growing business investments, this would indicate inflationary pressures too strong to be forever ignored by the Fed.

Guest contributor – Tolani Benson (Financials/Sovereign analyst, M&G Credit Analysis team)

Hungary has a substantial amount of debt outstanding – the IMF estimates levels were around €75bn at the end of last year, corresponding to 74% of GDP. Its local currency debt makes up a decent proportion of emerging market indices, constituting a not insignificant 4.6% of the widely used JPMorgan GBI-EM Global Diversified Index. A drop in Hungarian government bond values and/or the Hungarian forint means a drop in the index.

Not an EM investor? A substantial proportion of Hungarian sovereign debt is also owned by its banks, which are themselves owned by the Western European banks you may be more familiar with. Hungarian government bond holdings at three of Hungary’s biggest foreign owned banks were equal to between 10% and 25% of their parent banks’ tangible common equity at YE 2011 (2012 data isn’t out yet for the Hungarian banks). These three large parent banks have all had to receive bail-out capital from their respective governments since 2008 – a writedown of their Hungarian government bonds would not be a minor event for any of them. Appetite for recapitalising banks in the Eurozone is moving increasingly away from government capital injections towards bailing in unsecured senior and subordinated creditors and uninsured depositors, as we have seen with this week’s debacle in Cyprus.

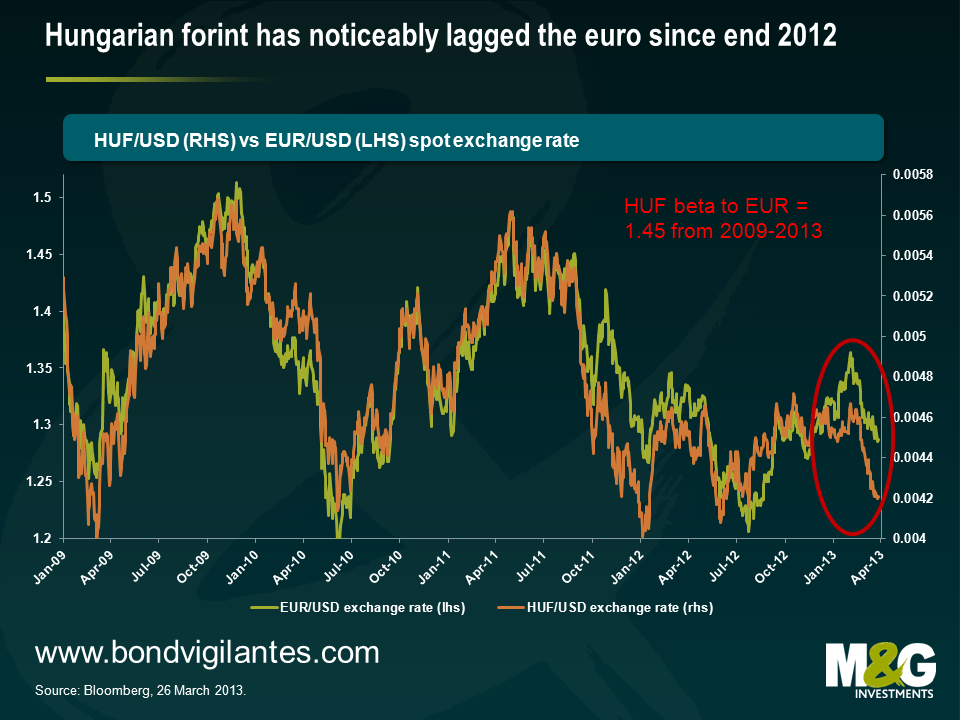

So what is going on in Hungary? Hungary’s currency, the forint, has always been a high beta version of the euro (see chart), but it has significantly underperformed since mid-October, plummeting 10% against the euro. And on Friday we saw the forint reaching a 52-week low after S&P changed their outlook on Hungary to negative (currently rated BB by the agency).

Some may argue that for a highly indebted nation suffering from a stagnant economy, a devaluing currency should be a good thing – Hungary becomes more competitive, economic activity picks up, government revenues increase, the deficit decreases, and government debt levels fall – great.

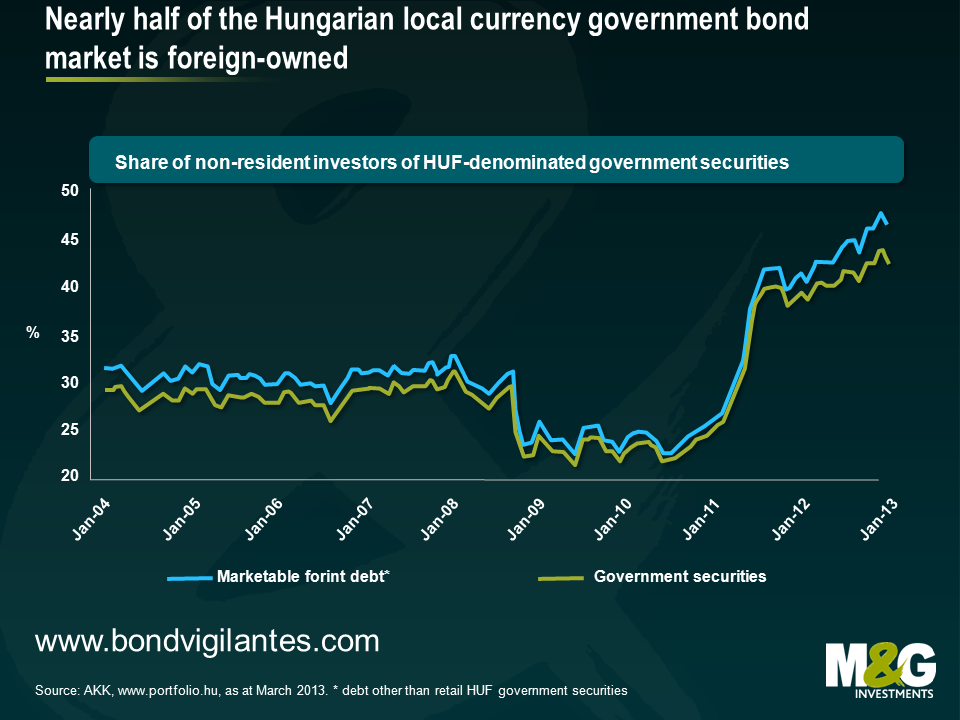

If only things were that simple. Forint weakness is a serious problem for Hungary. It has huge amounts of foreign currency debt across the whole economy; the government, its citizens, and corporations. The weaker the forint becomes the more expensive it is for both the public and private sectors to service their debts. Plus, almost half of the government’s local currency debt is held externally (see chart), making it extremely vulnerable to sell-offs in the forint. If foreign investors pull out, Hungary’s funding costs will soar and the country will struggle to refinance. The ECB puts the Hungarian economy’s gross external debt (i.e. any liabilities held by foreign creditors, including foreign owned domestic debt) at almost 130% GDP. Economists Reinhart and Rogoff in their paper ‘Growth in a time of debt’ have estimated that growth is significantly impaired when external debt is beyond 60% of GDP, and growth rates are halved above 90% of GDP. In their 2003 study with Miguel Stevanso, ‘Debt intolerance’, they also found that when external debt to GNP ratios are above 30-35% in emerging market economies, there is a substantial increase in the likelihood of a credit event. Hungary is well beyond these threshold levels, which should set alarm bells ringing.

Though the weak forint has helped Hungary’s trade balance, it is not enough. Despite posting a trade surplus of €6.8bn in 2012, GDP contracted by 1.5%. Unemployment is high and rising, reaching 11.2% in January this year. Hungarian businesses have been stifled by the credit crunch that has come about as a result of the government’s measures to reduce its citizens’ foreign currency debt burdens by writing off huge amounts of individuals’ debts, forcing losses onto the banks and restricting their ability to lend. And herein lies the root of most of Hungary’s problems; government policy.

Since taking power in 2010, the current government has been chugging out reams of controversial and counter-productive policies whilst making countless changes to the constitution. Such behaviour has been making investors uncomfortable, causing the forint to devalue. The business environment in Hungary is far too volatile to attract external investment – the key to growth – due to constantly changing regulation, heavy industry levies, and the possibility that the government may nationalise private corporations. Economic policy has been questionable, relying more upon one-offs such as the highly contentious appropriation of citizens’ private pension fund assets onto the government balance sheet, and much less upon vital structural change. Attitude towards the IMF since requesting a bailout loan in 2011 has been confrontational, with various government departments dismissing any need for assistance. The government started publishing anti-IMF propaganda in local media portraying the IMF as a threat to the country’s sovereignty. Unsurprisingly, any IMF deal now seems to be off the table.

Even more troubling than the government’s handling of the economy are the changes it has implemented at key institutions. It has thrown out the independence of the central bank by taking control of appointments, dismissing independent members, and placing the government’s former Economy Minister in the top seat as Governor, and in the process replacing the hawkish former governor, András Simor, who consistently resisted government attempts to influence monetary policy. The most concerning change is doing away with the Constitutional Court’s ability to perform its intrinsic function. Its power to overrule legislation that is deemed unconstitutional has been removed, so that it may only object on procedural grounds. This also allows any previous rulings by the Constitutional Court to be thrown out, effectively allowing the government to undo work done by the court to protect Hungary’s citizens in the past.

Being a member of the EU, Hungary’s actions have not gone unnoticed, but as yet appear to be unpunished. Hungary is like the naughty student that gets called up to the headmaster’s office every day – only the headmaster is the EC, and rather than silly classroom pranks, this bad behaviour is much more concerning. Should the forint continue its gradual demise it is the Hungarian citizens that suffer with a stagnating economy, a credit crunch, and the gradual withdrawal of their human rights. They will also have to deal with the long period of painful austerity that is inevitable when the IMF eventually has to pick up the pieces after years of terrible policy decisions have run the country into the ground. If that IMF assistance involves restructuring of sovereign debt, it is also the holders of EM debt and creditors of some large Western European banks that may be feeling the pain.

If I asked you how the structural problems of the Eurozone may be resolved, I am sure that the suggestion of a fiscal union in which transfer payments will be made by the “rich” Northern member states to the “poor” ones in the South of Europe would rank amongst the top answers. I’ve been wondering for a while if the member states could ever agree upon major fiscal transfer payments and if it would indeed lead to greater degree of convergence within the Eurozone. I feel that we have come closer to an answer to my questions this week. And I am not referring to the issues around Cyprus.

Yesterday the German federal states Hesse and Bavaria filed a lawsuit against the existing mechanism of fiscal transfer between the federal states of Germany, the so-called “Länderfinanzausgleich”. The German constitution states that the objective of this fiscal transfer mechanism is the convergence of the financial power across its federal states. The current system consists of vertical payments between the German state (“Bund”) and the federal states (“Länder”) as well as horizontal payments from federal state to federal state. The eligibility for transfer payment receipts is determined by an index (“Finanzkraftmesszahl”) which indicates the relative financial power of the federal states. Bavaria, Baden-Württemberg and Hesse are currently the only net contributors, while Berlin is the biggest net recipient of these fiscal transfers.

Bavaria and Hesse argue that the current mechanism does not create any incentives for the net recipients to improve their financial position. It is said that sanctions for fiscal mismanagement are missing, while the net contributors are discouraged to consolidate their finances further as long as they have to redistribute their wealth. Basically, one rich German state is arguing why it should transfer its fiscal revenues to a poor (and arguably irresponsible) German federal state. If you already see significant opposition against a redistribution mechanism of wealth within a country, how is it possible to picture Germany, the Netherlands or Finland agreeing on major fiscal transfer payments to Southern Europe? Furthermore, the implication here is that the German Constitutional Court will have to decide if a stricter central enforcement of fiscal discipline has to be institutionalised and which set of sanctions can possibly be introduced to do so. Could you see anything like this to be enacted in the Eurozone in the near future, including lawsuit files from Germany, the Netherlands and Finland in response to any agreement as well as the subsequent court rulings on national and European level? In this context, it might be worth noting that the German Constitutional Court indicated last year that any further European integration, e.g. fiscal union, would require a referendum. Ultimately, German taxpayers might get to decide whether they want their tax payments to be transferred to other parts of Europe.

There remains the question about the potential long-term effect of a fiscal union. Would fiscal transfer payments from the North to the South lead to economic and social convergence in Europe? In Germany, fiscal transfers from the South to the North-East have certainly helped these federal states to converge in terms of their financial power and standard of living since the German unification in 1990. Nevertheless, after 23 years of fiscal transfer payments, the economic situation in these states remains highly unequal. For instance, the German unemployment rate varies significantly across federal states. While the unemployment rate in Mecklenburg-West Pomerania stands at around 14%, it is nearly as low as 4% in Bavaria and Baden-Württemberg. And the historic ties of companies, the geographical location and different geostructural fundamentals, infrastructure disparities, qualitative differences between educational and research institutions and many other factors might prevent them to ever fully converge.

This is the crux of the Eurozone matter for me. Only if we accept the fact that full convergence and homogeneity in Europe will not be achievable – even within a fiscal union – we may become sufficiently pragmatic to deal with the Eurozone issues. We might finally arrive at the conclusion that we could be able to improve the economic prosperity and dismantle some social stress in the periphery, but that we will not make these economies as competitive and prosperous as Northern Europe as a whole. Take the US as an example. No one expects the standard of living, the average income level and economic competitiveness to be anyhow equal or homogenous across the country. Despite a long established currency and fiscal union, the economic situation and opportunity set still varies enormously depending on whether you live in New York, Detroit, Kentucky or Las Vegas. But you can reasonably move from Detroit to Kentucky if you want or have to because the same language is spoken and partly similar traditions are followed. You certainly won’t be able to say that about your move from Athens to Munich. It has been taken as a given in the US that some degree of inequality and heterogeneity is the function of a free market economy (the rest is a function of bad policy-making), and that might be one of the reasons why the US model, including monetary and fiscal union, has managed to succeed.

This would be an inconvenient and unpopular insight in Europe which would fundamentally question the current ambitions of the European convergence project. If you discount the possible long-term return of the Eurozone to its member states because of a lack of German support for a fiscal union, you might want to ask where the Euro project is heading.

With the UK’s 2% CPI inflation target having now been exceeded for 39 consecutive months, last week’s budget formally acknowledged the on-going situation and changed the Bank of England’s remit.

Although chancellor George Osborne maintains that medium-term price stability represents “an essential pre-requisite for economic prosperity”, the updated remit simultaneously introduces the concept of flexible inflation targeting in the short term, asserting that the Bank of England committee “may wish to allow inflation to deviate from the target temporarily” in exceptional circumstances, i.e. as the result of shocks and other disturbances. In short, inflation targeting looks like it will continue to take a back-seat to the pursuit of growth and employment with the chancellor accepting that inflation is likely to rise further and may remain above the 2% target for the next two years. It is also interesting to note that there is no restriction on how far inflation is permitted to deviate from its target, nor has any time limit been set for any such deviations.

Allowing more flexibility simply reflects the reality, and it can therefore be argued that this is probably based on the theory that whilst current inflation rates are hurting consumers, hiking rates to bring inflation down – by raising mortgage and loan rates – would hurt even more. Wage growth is only just above 1% per year, so the authorities perhaps feel that overshooting the inflation target is unlikely to create an inflationary spiral based on rocketing pay settlements.

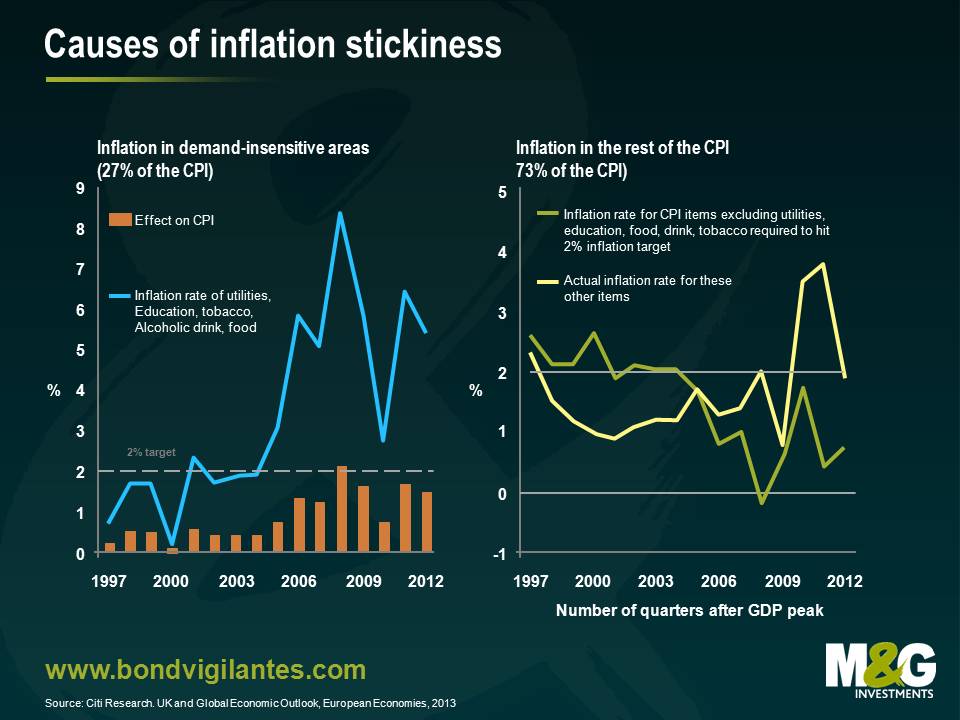

Citigroup’s Michael Saunders has presented an interesting piece of research which he believes breaks down the root causes of inflation stickiness. The research shows that for most of the inflation basket, there isn’t a problem and for the 27% where there is a problem, it is not clear that hiking rates would be a solution.

The first graph demonstrates the inflation generated from demand-insensitive areas (e.g. goods that have relatively static demand curves, regardless of changes in the price) such as utilities, education, tobacco, food and alcoholic beverages. This part of the basket contributes to 27% of the overall CPI figure. In recent years, this proportion has persistently exceeded the Bank of England’s 2% target thanks to formulae on these prices which allow “inflation plus” rises, and in the case of food, volatile weather. The Bank of England explains this away by treating it as a one off shock; Michael Saunders argues that this portion of the CPI basket is seeing a consistent series of small shocks, and is therefore predictable. Therefore in order to compensate for the above-target growth in price level of these prices, the inflation rate of the remaining portion of the basket of goods would have to see much lower inflation to offset this and to meet the 2% target. The required adjustment is demonstrated by the green line in the second graph, while the actual inflation rate for this portion of the CPI basket is shown in yellow.

As you can see, Citigroup’s research shows that the actual inflation rate for the remaining portion of the CPI basket of goods must fall considerably ( from around 2% per year to around 0.7% per year) if the formal 2% inflation target is to be met. Indeed, in the aforementioned Bank of England remit, George Osborne himself concedes that the impact from both regulated and administered prices have together contributed to the persistent inflationary environment.

It is subsequently made clear that in the current environment of deliberately loose monetary policy and the ensuing departure from the inflation target, UK above-target inflation is baked into the cake unless the Bank of England tries to depress demand for the remaining demand-sensitive proportion of the basket. If this inflation overshoot is not curbed over time, this could potentially affect expectations of future inflation, calling the Bank of England’s ability to deliver medium term price stability into question. Therefore, despite champagne being removed from the CPI’s 2013 basket of goods, let’s hope that over time the Bank of England’s credibility is still something the UK can celebrate.

Still outstanding, but probably not for long. Although this gilt has a maturity date on 12th December 2017, there is a call option for the government at par (100) on 12th December this year (hence the 2017-13 date), and given the current price of the bond is well above par (108-ish) it will get redeemed, unless they forget. This is what’s known as a “rump” stock. Although it was once a £1 billion issue, most has been bought back over the years by the Bank of England or Debt Management Office, so there’s only £14.5 million left in the wild.

This gilt issue was announced in June 1978, when Rivers of Babylon by Boney M was number one in the UK music charts, and, most importantly Nottingham Forest FC had just won the football league. Forest would go on to win the European Cup two years in a row. And it was a proper competition in those days, not a stupid league like today. Shilton, Anderson, Burns, Lloyd, Clark, McGovern, Needham, O’Neill, Bowyer, Robertson, Birtles. And Clough and Taylor. You can read a bit more about this great team here.

Inflation in 1978 was 8.4%, so 12% was a nice real yield, although inflation had averaged 15.8% over the past 5 years, so it wasn’t a no-brainer. In fact your real return from gilts in 1978 was -20%, and -22.6% in 1979. Ouch. It wasn’t until 1982 that there was a positive real return, a lovely 29.2%. The interesting feature about gilts at the time was that they were issued partly paid, with 15% of the purchase price payable on the 15th June, 30% on 27th June and the rest on 14th July. We’re not really sure what the point of this was? To allow gilt investors to gear? To manage money market flows? Any veterans care to let us know?

Anyway the 20 tweeters who came up with the correct answer were:

@RobinNGhosh

@RichardPhilbin

@peds52

@Invest_Advisory

@Yogi_Chan

@byronburghart

@JeremyBeckwith1

@SeanGConnery

@m1kee123

@Partegas

@adamgrimsley

@DanBland

@Dario_Gainnini

@krista_andria

@hellocanuhearme

@amirriz 1

@EdBagenal

@HarpRob

@ssaxim

@NickRilley

Please DM us with your address so we can send you a copy of Mark Glowrey’s The Sterling Bonds and Fixed Income Handbook. Thanks for all of your entries.

After years of inactivity, the combination of strong corporate balance sheets and cheap funding has sparked demand for takeover deals. The largest and highest profile deal this year has been the acquisition of H.J.Heinz by 3G Capital and Berkshire Hathaway. It is exactly the type of business that Berkshire Hathaway’s Chairman and CEO Warren Buffett typically goes for: profitable growth; a very recognisable brand; and years of emerging market growth forecast in the future.

Berkshire Hathaway and 3G Capital are buying Heinz for $72.50 per share, a 19 percent premium to the company’s previous record high stock price at the time the deal was announced in mid-February. Including debt assumption, the transaction was valued at $28 billion. Berkshire and 3G will each put up $4.4bn in equity for the deal along with $12.2bn in debt financing. Berkshire is also buying $8bn of preferred equity that pays 9%.

Let’s not beat around the bush. It’s a great company. The business has seen thirty one consecutive quarters of organic growth, stable EBITDA margins, owns a number of globally recognised brands and should be well positioned for future emerging market led growth. Despite this, some are questioning whether Buffett is overpaying for Heinz. So is the price of the deal justified?

The answer, at least in part, lies with cost of debt. The pro-forma capital structure (per the offering memorandum) looks like this:

| PF Capital Structure | Sources ($m) | Net Debt/PF EBITDA |

| Cash | -1,250 | |

| 1st Lien | 10,500 | 3.87 x |

| 2nd Lien | 2,100 | 4.75 x |

| Rollover Notes | 868 | 5.11 x |

| Total debt | 12,218 | 5.11 x |

| Preferred Equity | 8,000 | 8.46 x |

| Common Equity | 8,240 | |

| Total | 28,458 |

Current price talk on the first lien debt sits at $ Libor + 2.75% (floored at 1%) with the second lien at 4.5%. If this is finalised, the company will see an approximate blended interest cost of 3.9% on its new debt securities. Prior to the transaction, Heinz was rated as a solid investment grade business attracting a Baa2/BBB+ rating. Assuming the deal goes through, its new second lien notes are expected to be rated B1/BB-, some five notches lower than Heinz’s current rating, reflecting the much higher financial leverage and structural subordination.

It’s worth noting that through last year Heinz’s 6.25% 2030 bonds traded in a range of 4–5%, despite the much higher rating and lower financial leverage at the time; albeit some term premium is warranted given the longer dated nature of the debt. The bonds have since sold off in recognition of the greater risk – as things stand they will remain in place.

Now let’s compare the price action of the proposed debt financing to the preferred equity to be owned by Berkshire Hathaway. Whilst the paper is structurally subordinate to all other debt, it still sits ahead of some $8,240bn of common equity and attracts a cash coupon (which can be deferred) of 9% vs the 3.9% weighted average above. It’s also worth bearing in mind that the transaction has been structured to encourage the preferred equity to be retired, at least in part, ahead of both the first and second lien debt, potentially leaving bondholders with significantly less subordination than at day one. I’d argue that this is by far the most attractive (quasi) debt to invest in within the structure, though that is hardly surprising given that unlike Buffett, few of us can write a cheque of this magnitude.

As animal spirits return and the leveraged finance community falls over itself to lend to well known companies, the likely winners in the space will be the private equity community. Whilst we are nowhere near the levels of the great private equity binge of 2004-07, the value of takeovers in 2013 is already running well ahead of 2012. After years of corporate deleveraging, we may now be entering into a period of increased M&A activity. Company managers may find that if they aren’t willing to start leveraging up given the environment of extremely low borrowing costs, then investors like Buffett will do it for them.

The Heinz deal has been another recent shot across the bows of the bond market. Rising leverage has a longer term implication for credit markets, in that it is bad for credit quality. Bigger and bigger companies are clearly in play and this is something we will be keeping a very close eye on.

Stefan blogged earlier this week about the landmark sovereign bailout occurring in Cyprus, and about some of the interesting issues this raises. Sure enough, the parliament did not approve the package in the form talked about at the weekend. The reason? The taxes were felt too painful for the poor and too lenient for the more wealthy. This harks back to a blog I wrote about a couple of years ago, and goes to reiterate the issues we discussed then. However, for now I wanted to highlight some of the issues that this raises more specifically for the European banking system at large.

Firstly, depositors were presumed to be guaranteed by governments up to at least €100,000 in Europe. Last weekend, that notion was dealt a brutal blow by the Cypriot situation. However, it feels to us as though the main reason for the parliamentary delays is that deposit guarantees could and should remain in place – or at least to a greater extent than was implied in the original bailout package. This package stated that those people with deposits of less than €100,000 would pay a 6.75% tax, whilst those with more than this amount would be taxed 9.9%. The politicians that have delayed the approval of the rescue package want to see greater amounts of the burden borne by the wealthier (those with more than €100,000, and perhaps an even higher rate borne by those with greater amounts than, say, €500,000 in deposits), and so lesser amounts of the burden borne by those with small amounts of deposits.

My guess is that this is the key issue here. If the tax rates are not changed, then I would expect to see some significant moves in Spanish, Italian and other peripheral deposit flows and movements. As a risk, this must not be underestimated by the Troika. Why not maintain the deposit guarantee and generate the amount raised by the taxes, through taxing more on those with more than €100,000, more still on those with more than €250,000, and more still on those with more than €500,000?

Secondly, subordinated debt bail-in is a key part of the package, and without it one senses the Troika will not part with the bailout funds needed. We have expected weaker banks in weaker regions to have to use this as a necessary tool to break the sovereign-bank link for some time now. It is now official, and being used. I would expect more of these to come.

Thirdly and finally, sovereign bailouts of banking systems where the sovereign is already in an over-levered position will no longer be tolerated. It is time to break the sovereign-bank feedback loop (as we previously wrote about here). This has to be through bail-in and burden-sharing. However, the most unpalatable part of the proposed package to us (and I guess to many riotous Cypriots) is this: up until 2007 it was believed that senior bank bondholders ranked pari passu with depositors in the event of a bank failure. And now in 2013 we learn quite vividly that in actual fact in Cyprus depositors are likely to be subordinated to a bunch of wholesale and institutional (ie banks and insurance companies) investors?

The capital stack has been turned on its head in this regard. No one used to buy senior unsecured bank debt because they thought that depositors would take losses before them. Rather, it was because the markets believed 100% in the government guarantee of depositors. The pari passu relationship of depositors and bondholders supported high valuations on senior bank bonds. Thus to be pari passu with depositors, senior bank bonds need to take the same losses as depositors are. In my opinion, this part of the proposed deal is the most disgraceful.

So, I find myself wondering how on earth a deposit tax found its way into the package. The answer to me seems to be quite simple: contagion, or the avoidance thereof. We all know that in Europe and the UK in the future (as in the US already), senior bank bonds will be bail-in-able or writedownable if a bank fails or gets into difficulty. We were originally told that the date for senior bank bond bail-in in Europe would be 2018, although there has recently been much talk about bringing this forward to the beginning of 2015. It has long struck me that this should be the favoured route out of the bank-sovereign interconnectedness problem in Europe: continue to promote and enable senior issuance in Europe by banks, and then implement a higher level piece of legislation that at some date in the future makes all debt in the Eurozone and UK writedownable.

No matter how small Cyprus is relative to the rest of the Eurozone, if the Troika had forced senior bank bondholders to accept losses before 2018 – or is it 2015? – senior bank debt spreads would have suffered significantly across Europe. Given that this is the most attractive funding market for banks at the moment, as it is still cheap to issue from a bank’s perspective, and as sovereigns do not want to have to (or cannot, in the Cyprus case) step in to take on more liabilities on behalf of their banks, the Troika has ripped up the rule book and done the insane.

I think parliamentarians in Cyprus should force a rethink on the sovereign-bank feedback loop, as well as forcing a more palatable (ie Robin Hood) sharing of the burden between smaller and larger depositors. After all, can anyone truly imagine the French, German or any core European government accepting losses for their depositors whilst a bunch of international senior bank bondholders get made whole? Our view is that depositors should be protected (at least to the guaranteed amount) over and above all wholesale creditors, whether senior or subordinated. This is the first step to break the sovereign-bank loop. The second step, only to be used in cases where there is not enough senior and subordinated debt to prevent the sovereign, and so tax-payers, from having to bail out the failed institutions, is to look at forcing losses on depositors, but with preserving the preceding guaranteed amounts of deposits. The final, most radical, and rarest, step is to have to renege on that deposit guarantee amount, so as to avoid tax-payer bailouts and increased probability of sovereign default.

Depositors across Europe are already watching Cyprus carefully. My guess is that many are starting to check the amounts they keep with any one institution or in any region. Subordinated bondholders are already aware of the risks if those banks get into difficulty, but senior bondholders in my opinion are not. These investors must ask whether the Cyprus package is likely to be copied in future cases. And they must also start to wonder if they still have until 2018 before senior bonds can be bailed in, or if it is significantly sooner.

Depositors in Cypriot banks awoke on Saturday morning to learn a harsh lesson. A guarantee is only as strong as your counterparty. With the Cypriot banking system requiring €10-12 billion of bailout funds – some 60% of GDP – the government has been forced to accept burden sharing with depositors. Depositors who went to bed Friday night believing their savings were safe awoke Saturday to find that it has been proposed that those with deposits below €100k in the bank will be “taxed” at 6.75%; those with deposits above €100k will be “taxed” at 9.9%, contributing approximately €6bn to the bank bailout in total. This is regardless of supposed depositor insurance schemes. Depositors will receive equity in their respective banks by way of compensation and potentially bonds entitling those who leave their money in the banks for 2 years to a share of Cyprus’ future gas revenues. The remaining €4-6 billion will likely come from the Troika.

If press reports are to be believed this was a ‘take it or leave it offer’ from the Troika with German and Finnish finance ministers unwilling to go to their respective parliaments without depositor burden sharing. This highlights the very real current challenges of domestic politics within the European Economic and Monetary Union and raises further issues.

Firstly, there are significant political challenges to be faced. Domestic opposition to this deal is likely to be significant, not least as it will be seen to be disproportionately harsh on domestic savers – who had believed their deposits were protected up to €100k, and favourable to wealthy non-Cypriot depositors who reportedly hold huge sums offshore in the banks. It can be argued that those with over €100k in deposits with the banks should bear the brunt of any proposed bail-in. With a small parliamentary majority, the Cypriot government may struggle to pass the necessary legislation. Approval will also need to be sought from Eurozone member states.

Secondly, alongside the recent expropriation of junior bond holders at SNS Reaal the attitude towards tax funded bailouts appears to be hardening. Whilst this crisis has already witnessed both equity and debt written down, the rubicon of depositor burden sharing has now been crossed. Precedent now exists for this approach over the socialisation of losses across the Eurozone as a whole. Whilst the Troika will endeavour to play its significance down, unintended consequences may still materialise.

Thirdly, the Cypriot situation serves as a reminder of the current fragmented approach of depositor guarantee schemes across Europe. Depositor guarantees are only as strong as the sovereigns providing them. In the case of Cyprus with a banking system seven times the size of its economy, clearly those guarantees were worth very little. With depositor rates currently paying very little across Europe it is unlikely to take much to prompt a change in investor behaviour.

Fourthly, it raises real questions about depositor preference. With only circa €2bn of Cypriot bank debt outstanding, policymakers have judged this too small in and of itself to recapitalise the banking system. That may be true. However by favouring senior debt over depositors it does beg the question whether the individual on the street is in theory better off owning higher yielding bank debt than depositing cash.

Fifthly, the ECB has apparently threatened that if the measures are not agreed, then it would withdraw European Liquidity Assistance (ELA) funding for Laiki Bank, Cyprus’ second largest bank, leaving the Cypriot sovereign with the bill for the entire banking sector and having to pay out on deposit insurance in full. This highlights the extent to which a number of banks in Europe remain reliant on ECB funding, and that if that funding is withdrawn then their collapse is inevitable.

Finally, we have yet another example of a country being forced to face a stark choice between ceding sovereignty to Brussels or facing financial ruin. The Eurozone project continues to ask a great deal of its citizens. Bailouts don’t – and won’t – come cheap.

The Cyprus deal will be in the headlines for the next few days. We can’t help but think that the markets will be listening to Cypress Hill – Insane In The Brain for the next week or so. Maybe the Troika should too.

Mark Glowrey has written an excellent guide to the UK’s bond markets, covering everything from gilts, linkers, corporate bonds and high yield, to dealing, settlement, tax and covenants. There’s also some great bond market history and anecdote – I like the story of the two brothers who worked as bond brokers at the London Stock Exchange. Both had been awarded the Military Cross in World War 2, but the second brother had been awarded the Military Cross and bar. The nickname of the first brother was “The Coward”.

We have 20 copies of the book to give away. You can win one by tweeting us (we’re @bondvigilantes) the answer to this question. Add the hashtag #BVbook to help us find your entry in our inbox please.

What’s the highest coupon currently available on a UK gilt?

Tweet us your entries by midday on Friday 22nd March. The 20 winners will be contacted shortly afterwards. This competition is now closed.

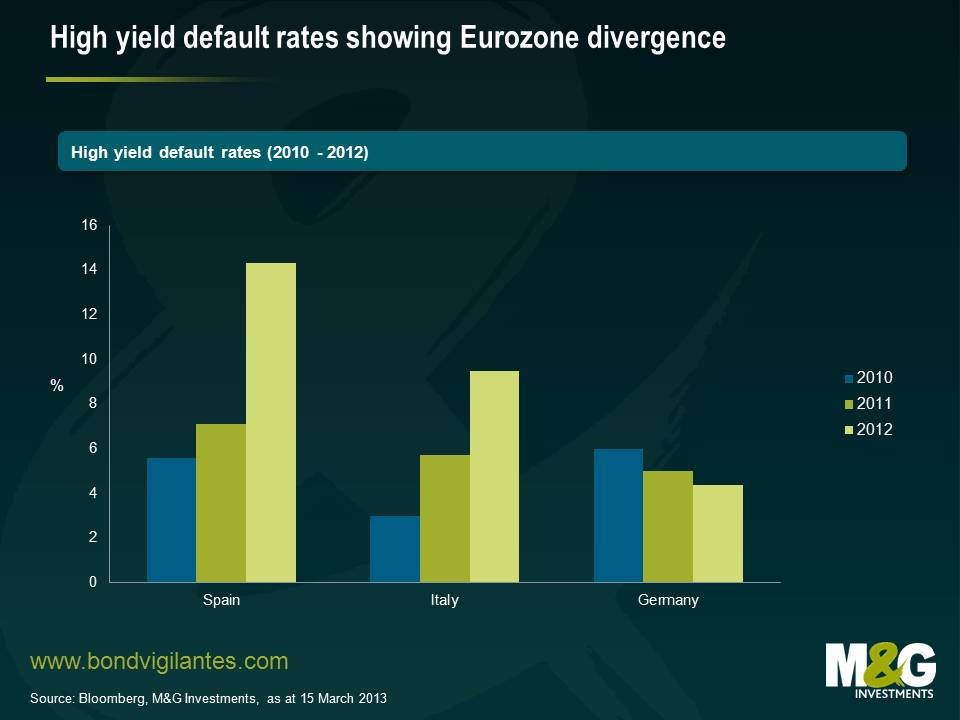

2012 was not a good year for peripheral European defaults in the high yield market. Spain’s default rate doubled from 7% to 14%, while Italy’s went from 5.7% to 9.5%. Clearly, that the Spanish and Italian economies are under stress is not news, but what I thought was interesting though was that German defaults have continued to fall. It is important to point out that this is not just the public high yield market, it also includes private bank loans and it has been those that account for the majority of the defaults.

As the chart below shows, in 2010 Germany had the highest level of defaults of the three countries but over the subsequent years the situation there has improved. The opposite has been the case in the periphery with last year’s jump in defaults looking particularly worrisome.

We have been speaking for a while about the strain that operating under inappropriate policies puts on an economy, and this looks like empirical evidence of just that. Italy and Spain need looser monetary policy and less constrictive fiscal policies. In a pre-euro world these countries would have had full control of these policy tools, been able to devalue their currencies, relieve some of the strain and increase the competitiveness of their economies. This is not an option open to them now (short of leaving the euro) and I can see no way the situation will improve anytime soon. Even with Mario Draghi and the ECB willing to do whatever it takes to save the euro, the only outcome I can see for the next few years is the strong getting stronger and the weak getting weaker.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.