World Cup

The Bond Vigilantes World Cup Model

By Joe Sullivan-Bissett

26 June 2026

Poor economic growth prospects, high unemployment, large debt burdens, poor public finances – it is all too easy for analysts and economists to say that the euro won’t be around indefinitely. Yet here we are, coming up to the five year anniversary of the Lehman Brothers collapse and having lived through a number of sovereign debt crises, and the euro remains the single currency for the Economic and Monetary Union (EMU) after being established in 1999. Many will argue, as we have in the past, that a monetary union is unsustainable without a full and proper fiscal union and that to devalue internally through lower unit labour costs is too painful for countries like Ireland and Greece. This would likely result in a divergence of growth within the Eurozone. However, we have to acknowledge that the European Union members and European Central Bank have done a remarkable job of managing the short-term symptoms of the crisis and have met every challenge that having the monetary union in place has produced so far.

That said, the long-term challenge remains: convergence amongst the Eurozone members so that a single monetary policy based on some level of price stability is as relevant for Germany as it is for Greece. The difficulty in achieving this convergence is the main challenge facing the EMU today due to the difficulties in operating under a single monetary policy and a single exchange rate.

With this in mind, now is a good time to think about whether the most ambitious currency union in history has the legs to go the distance after all. What are the main reasons why the euro will survive and prosper in the future?

Leading indicators like the PMIs and industrial production are pointing toward positive growth in Q2. Consumer confidence is improving, while unemployment numbers are starting to slowly improve in some countries as well. Of course, Europe is not yet out of the woods and continues to face significant growth headwinds which we have written about before. Nonetheless, it may be that we are witnessing the some early signs that the substantial structural reforms in the periphery are starting to bear some fruit.

Importantly, the Eurozone is showing signs of rebalancing. Unit labour costs (ULC) rose too quickly during the boom years in peripheral Europe and in Germany they did not increase enough. This eventually resulted in a large difference in competitiveness within the Eurozone which has started to dissipate (though countries like Italy and France still have further work to do – see our blog here). Turning to current account balances, Italy and Ireland are running a surplus, Greece has reduced its large deficit and Spain and Portugal are running small deficits.

These are small, but necessary, steps toward ensuring the survival of the euro.

In contrast to the southern European countries and Ireland, Germany has experienced an economic boom. Unemployment is low, exports are strong, inflation is low, the consumer sector is vibrant and we are starting to see some signs of house price appreciation in parts of Germany. A large reason Germany has done so well during the period of turmoil is because its external competitiveness has not been offset by a rising currency. For example, Germany’s real exchange rate under the euro is around 40 per cent below where the deutschemark used to trade against the US dollar.

Germany is operating as the China of Europe (at least from a trade surplus perspective) – a massively undervalued exchange rate is generating the world’s largest trade surplus of around €193bn a year (China’s is running at around 150bn USD a year). This surplus is overwhelmingly being generated through trade with other Eurozone members (like Italy, Greece, Spain, Portugal and Ireland).

The surplus capital that Germany’s improved international competitiveness generated has found its way into southern Europe and Ireland. German banks and investors were part of the international community that lent to the respective governments and businesses of the peripheral countries in search of higher yields than their own German bunds were offering. Of course, if this capital had not been provided, the southern European countries and Ireland would not have had the ability to build up so much debt (in 2008, around 80% of Greek, Irish and Portuguese government bonds were owned by foreign investors). Additionally, ULC growth could have been more constrained in these countries (particularly in the public sector) and the gulf in competitiveness between Germany and the peripheral countries would be less pronounced than it is today.

Germany has been the greatest beneficiary of the common currency. Any default would devastate its banking system and export industry. Germany is on the hook, so it is very difficult to see why it would abandon the euro.

Germany currently benefits to a much larger degree from the euro than the heavily indebted countries. This is because the single currency has robbed these nations of the ability to become more competitive through currency devaluation (compare the experience of these countries against the UK for example). Additionally, interest rates are way too restrictive and deflationary forces have taken hold due to excess capacity and ultra high unemployment rates. Countries like Greece and Ireland have not had a recession, they have had a depression.

Because policy makers in southern Europe and Ireland have no access to the monetary policy or the currency lever, there remains only one possibility to gain competitiveness – painful austerity and internal devaluation through reduced wages. This is the only way that these countries can hope to compete with the likes of Germany in the globalised environment.

So why doesn’t a country leave? Greece, Ireland and Cyprus have severely tested the euro in recent years yet remain in the union. The strongest argument that has been put forward is that the costs of leaving the EMU will be too painful relative to the gains. Capital outflows, skyrocketing inflation, bankruptcy on a national scale, mass unemployment and social unrest do not make the option particularly enticing. And just imagine what will happen if Italy or Spain decide to get out. To retain the euro is the least worst option for the debtor countries.

It has now been a year since ECB President Mario Draghi delivered one of the most important speeches in the history of Europe and stated: “Within our mandate, the ECB is ready to do whatever it takes to preserve the euro. And believe me, it will be enough.” In stating these remarks, Draghi convinced the markets that the ECB had unlimited firepower to support its members and more specifically, Spain and Italy. Immediately, yields on peripheral European sovereign bonds fell from dangerously high levels that made borrowing unsustainable over the long term and are currently much lower than their levels a year ago. It is fair to say the market still believes Draghi and is now pricing risks more appropriately. With the ECB taking tentative steps towards forward guidance, it may not be long before we see further unconventional monetary policy measures like a new LTRO announcement.

Despite the problems – the concerning outlook, the record levels of unemployment and debt, the proposed tax on savers in Cyprus – no country has left the EMU. The EMU has in fact added new members (Slovakia in 2009 and Estonia in 2011) and may add more (Latvia in 2014). European countries remain open for trade, have continued to enforce EU policies and have not resorted to protectionist policies. EU banking regulation has become stronger, the financial system has stabilised, and new bank capital requirements are in place.

It is true that Europe remains a huge concern for us. A successful monetary union requires not only political but also economic integration. European politicians must accept greater limits on their policy autonomy and this will be difficult to gain. Economic convergence is necessary. Perhaps most worryingly, a cocktail of lower domestic demand, austerity, reduced wages and high unemployment is normally politically costly and breeds social unrest. However, given the track record that the EU and ECB has shown and for the reasons listed above, perhaps the euro may be around much longer than some economic commentators currently expect.

Since the start of 2011 we have seen the onset of the Eurozone crisis, endemic political uncertainty, a return to recession and a de facto Greek sovereign default. Contrast this to the path the US has taken with aggressive QE, positive growth and a recovery in the housing market. The somewhat surprising fact is that in spite of all this, the European high yield market has outperformed its US counterpart, returning 29.0% and 24.8% respectively*.

There is little doubt that the US presents a more benign fundamental and macroeconomic environment for leveraged companies. Nevertheless, there are still compelling reasons to believe the European market offers the better investment opportunity. Here are 5 reasons why:

Of course there are always mitigating elements to this argument – the all-in yield of the European market , for example, is lower at 5.1% (US is 6.1%) – reflecting both the lower duration of the market, but also the divergence of European and US government bond market yields over recent months. Nevertheless, with lower interest rate risk, lower average cash price, higher credit quality, higher credit spreads and lower default rates, the investment case for the European market continues to look more compelling compared to its American cousin.

*BofA Merrill Lynch US and Euro High Yield Indices 31/12/2010 – 26/07/2013

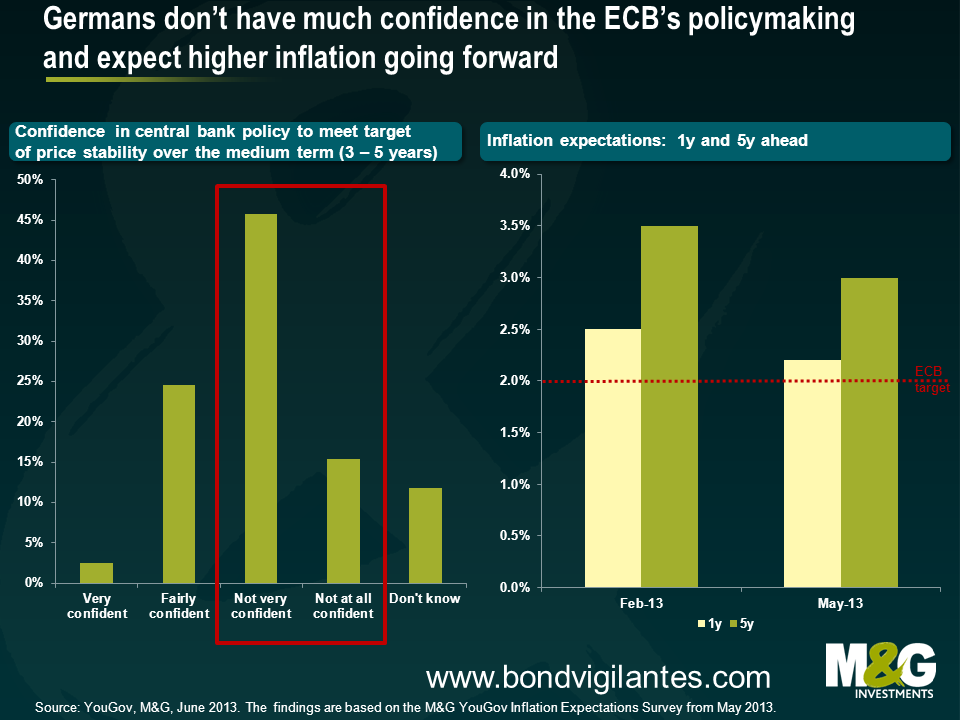

Being a German abroad, I am very aware that one never runs out of German stereotypes to discuss. One of the stereotypes is the German obsession with price stability and fear of price instability. The latest results of the M&G YouGov Inflation Expectations Survey indeed confirm the current worry about inflation amongst the German public. The chart below suggests that Germans have an exceptionally low confidence in the ECB’s policymaking and expect inflation to be above the two per cent target both one year and five years ahead. Although we have seen a declining trend from February to May 2013, inflation expectations over the medium term in particular remain significantly elevated.

It seems to be clear that Bundesbank president Jens Weidmann’s metaphorical use of Goethe’s figure of the devil, Mephisto, as well as other critical remarks by the Bundesbank, may not have helped the German public’s confidence in the ECB’s ability to deliver price stability. However, it looks to me that there are more factors at play that currently shape the German expectation of rising inflation. Earlier this year, I shared my observations on wage dynamics in Germany and concluded that we could see some notable real wage growth in 2013.

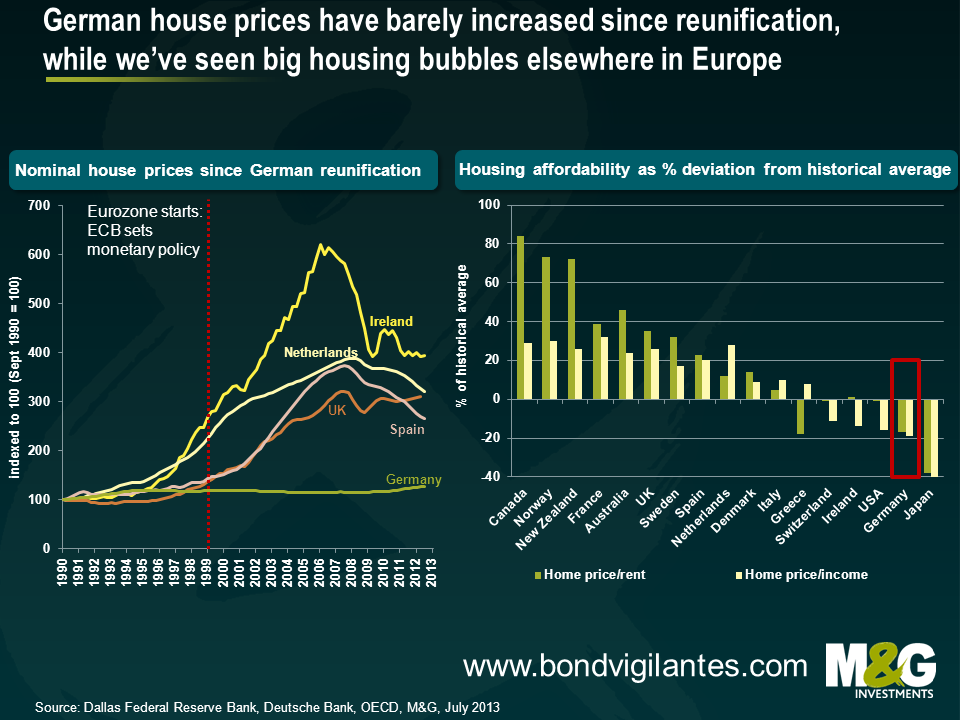

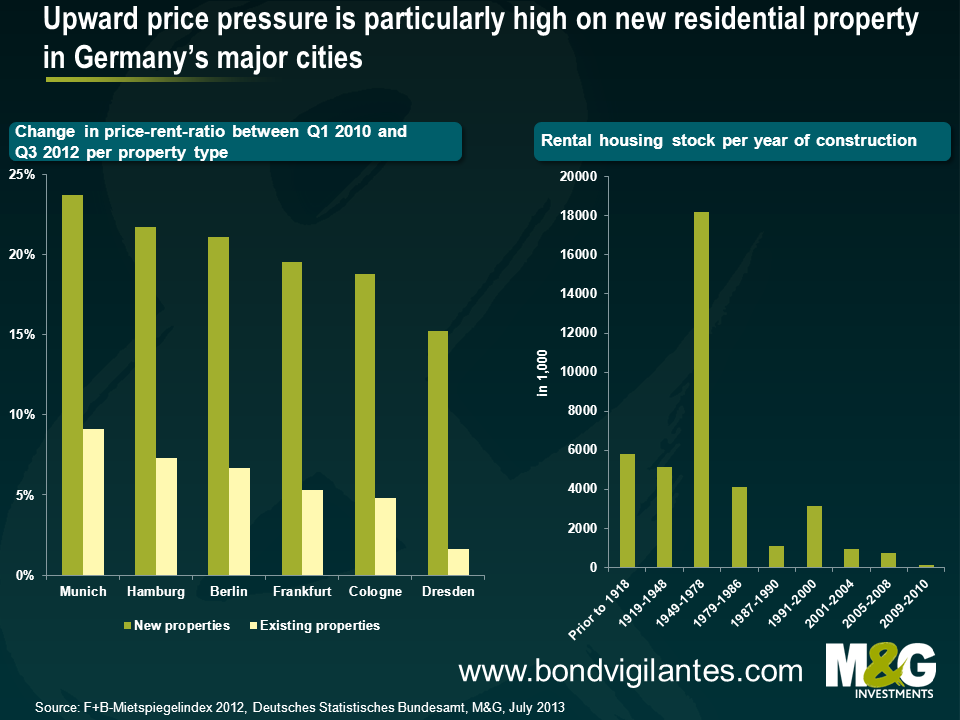

But Germans are also experiencing another form of inflation that is different to most parts of Europe: rising house prices. While an increasing house price level is a form of asset price inflation rather than consumer price inflation, it also has wider implications for the general consumer price level. Firstly, property owners tend to pass on the higher mortgage refinancing costs through increases in rents. For instance, rental costs form a significant part of the German CPI basket (21 per cent) and therefore feed through into the general inflation number. Furthermore, in an environment of rising house prices, homeowners have a greater ability to increase consumption spending by borrowing against the higher asset valuation (although this does not appear to be happening given the lack of German credit growth). The chart below shows that German house prices have increased on average by 10 to 20 per cent from 2007 to 2011, with significant variation dependent on the residential area and property type. The DIW Institute finds evidence that this trend has continued and seems to be accelerating in German cities. Prices for flats in Berlin, Munich and Hamburg are estimated to have risen by around ten, seven and six per cent annually since 2007.

The German housing market history stands in stark contrast to many European countries. ECB interest rates were too high for Germany up until 2008, but too low for the high growth economies of Ireland and Spain. Germany therefore did not experience the credit-induced property boom in the 2000s that subsequently sent the Irish and Spanish homeowners into financial difficulties. Irish and Spanish house prices have fallen considerably since their housing bubbles popped, but they still look high compared to pre-Eurozone levels. The Netherlands is the most recent example of a European economy that is struggling with a bursting housing bubble, with house prices 9.6 per cent lower year on year. The downward trajectory of the Dutch economy seems to be accelerating and is certainly one to keep a very close eye on. Remarkably, house prices in the UK are back to pre-crisis level – and the government’s ill thought through “Help to Buy” scheme might fuel prices even more.

Although German house prices have recently begun to climb, if you expand your time horizon to the point of German reunification in 1990, it becomes evident that the general German house price level has barely increased over the past 23 years in nominal terms, let alone in real terms. The recent increases in house prices at the national level and in cities like Berlin have started from a very low base, and there is significant potential for further increases if you consider that housing affordability, as measured by the home price-to-rent ratio and home price-to-income ratio, is still significantly below the historical average. At the same time, housing in the UK, Spain and the Netherlands remains expensive compared to historical levels. So if refinancing rates are cheap in the current low interest rate environment (the ECB’s monetary policy is arguably too loose for Germany) and house prices are on an upward trend, wouldn’t you expect the Germans to invest in new homes?

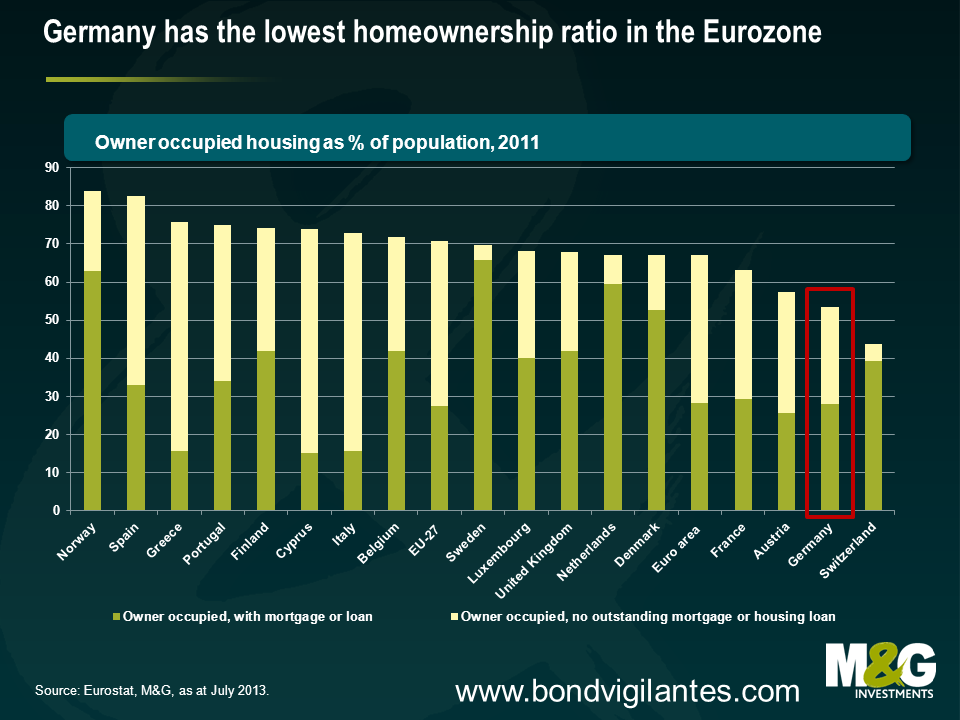

Well, so far they haven’t really done so, at least not by European standards. Homeownership has increased in recent years, but still remains significantly below the levels of the rest of Europe. Only about half of the population lives in their own houses (the German census from 2010 suggests that homeownership stands at 45.7 per cent, while the Eurostat figures above are around 8.7 per cent higher). This compares with an average ownership level of around 70 per cent in Europe. Let’s have a look at some of the reasons why Germany has not seen a property investment boom yet.

Homeownership is less widespread for a number of historical, cultural and economic reasons. For instance, domestic credit lending has been fairly strict and, as a result, Germany has not seen a mortgage boom which inflated the US, Irish and Spanish housing bubbles (sadly tight lending standards did not apply to overseas lending, as illuminated by the 2008 crisis and more recently by German banks’ exposure to Detroit’s default). The average initial repayment rate stands at around two per cent currently and the average loan-to-value ratio remains below 80 per cent. To put this into context, loans without an initial repayment rate and a loan-to-value ratio of more than 90 per cent were very common in the US prior to the financial crisis. Also the recent mortgage loan growth rates of 1.2 (2011) and 0.3 per cent (2012) show no evidence for a hot property market.

Historically, the German housing culture has been to rent a property, and it takes a long time for culture to change. The predisposition to rent can be traced to the policy measures by the German government after WWII. The government responded to the acute lack of residential property by highly subsidising social housing instead of providing cheap funding for new private home builds. The chart above shows that German housing investment saw an enormous boom from 1949 to 1979 and that most of the current rental property stock dates back to this period. Many of the German baby boomers were brought up in rented flats and houses – it has been the norm, not the exception. However, the chart also presents strong evidence that it has become significantly more expensive to rent in the last 3 years, particularly in more prosperous urban areas. Property developers have managed to push up rents for new residential property by more than 20 per cent. The German government released a report in October last year suggesting that the demand for urban housing in the strong economic regions remains high due to continuous migration flows from the economically weaker regions of the country. It is estimated that Germany faces an annual construction demand of 183,000 residential apartments until 2025.

Given the considerable demand for new urban housing and the current favourable investment environment, German house prices may be set to rise for some time. In particular, price inflation for new property developments in prosperous urban areas, such as in Hamburg, Stuttgart and Munich, seems to be baked in the cake for the next years. However, a housing bubble is not in sight yet as we are not experiencing any excessive credit growth given that banks remain capital constrained, and valuations are not in bubble territory as housing affordability still looks reasonable relative to historical levels. Germany is currently heading for a natural adjustment of its house prices, and this may be a positive development for the Eurozone. That is, an increase in property investment would subsequently lead to a decrease of the excess German savings rate, bring down the enormous current account surplus and therefore help the Eurozone rebalancing.

However, German government interference might distort the natural adjustment process of German house prices. Decreases in rent affordability are a real concern in the German public at present. Consequently, not only the left-leaning German parties, but also Angela Merkel’s Christian Democrats (CDU) have agreed upon a “Mietpreisbremse” in their electoral manifesto, a policy to cap the maximum rental growth rate that can be imposed if a flat or house is re-let. The FDP, the CDU’s coalition partner, seems to be the only major German party that doesn’t support such a policy initiative. Therefore, it is very possible that we could see some sort of “Mietpreisbremse” after the general election in September. This policy would potentially have a disinflationary impact. Subsequently, this might be reflected in the public’s medium term inflation expectations which could then trend downward from the current elevated levels. Ultimately, the rental cap might also affect house prices. The prospect of being restricted in the ability to pass on higher prices and financing costs to the tenant in form of higher rents could make property investment less attractive. This argument may be countered by suggesting that a shortage of supply could cause a squeeze in the German property market and actually keep pushing prices up if residential investment doesn’t pick up. That is, Germany could see further asset price inflation, but a slowdown of the rental growth rate and, consequently, of CPI inflation. Against this background, it’s definitely worth to keep an eye on both the German housing market and inflation expectations!

Moody’s, the credit rating agency, published a report a few days ago on the asset backed securities market. One section of the report has attracted some media attention – it details the agency’s thoughts on UK interest-only residential mortgage-backed securities (RMBS).

Moody’s reaches the fairly unsurprising conclusion that when interest rates start rising in the UK delinquencies on interest-only mortgages will pick up. They go on to say that this effect will be greater in the non-conforming sector than in the prime segment of the market. This makes sense, as borrowers who have an impaired credit history usually fall into the non-conforming bucket and are therefore, on average, more likely to have trouble paying their mortgages than those who qualify as prime borrowers.

This isn’t as bad for RMBS deals that are backed by interest-only mortgages as one might think. A large proportion of RMBS deals are structured with features that protect investors in the more senior notes to the detriment of those who own the more junior ones. A variety of trigger levels are usually built into the deals which amongst other things reference delinquencies and credit enhancement. If these triggers are hit, cash flows are diverted to the most senior tranche of notes, bringing forward their maturity date and increasing their yield.

A deal I have been looking at recently is 95% backed by interest-only mortgages and has a trigger when 7.5% or more of the mortgages are more than three months in arrears. Delinquencies are currently much lower than that but if they did breach the 7.5% level the deal would switch from paying pro-rata to sequential. This means that any excess cash that is generated through repossessions or borrowers re-mortgaging will all be paid to the lenders at the top of the stack instead of being shared by all the note holders. An increase in interest rates and delinquencies would in this instance clearly be of benefit to the senior notes.

Another dynamic to be aware of is when the mortgages backing the deal were originated. Mortgages taken out closer to the peak of the credit bubble in 2007 are generally of a lower quality because lending standards were weaker and borrowers generally have less equity in their property. As a result, these mortgagees have less of an incentive to keep paying their mortgage each month.

Holders of junior notes in later vintage deals should definitely be worried by the prospect of higher interest rates in the future. Senior note holders – whilst remaining attentive to movements in the market – should be fairly comfortable with the credit quality of their bonds, even in a climate of higher interest rates.

We aren’t the first to have a look at George Osborne’s “Help to Buy” scheme. It has been met by warnings far and wide. Sir Mervyn King stated that “there is no place in the long run for a scheme of this kind”, whilst Albert Edwards from Societe Generale was a little more blunt when he wrote that it was “a moronic policy”. Even the IMF and the OBR are getting in on the act, warning that the scheme may have more of an impact on the demand side of the house price equation, rather than fix the real issue which is a lack of supply.

What alternatives does Osborne have? Seeing as rising house prices do almost nothing to help the UK’s biggest problem, the Government should target the bigger problem, which is the UK’s dearth of investment. Construction is a very low productivity investment. The UK needs investment in infrastructure, education, plants and equipment. Without this the UK has very weak long run growth potential.

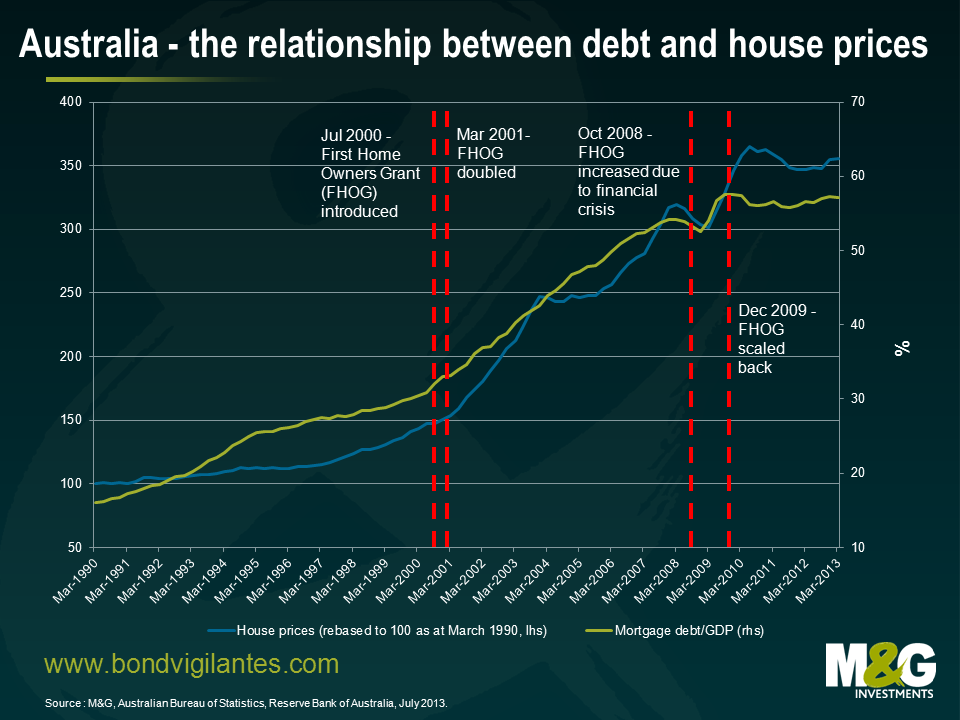

Now don’t get us wrong. We can see what George Osborne is trying to do. By announcing the “Help to Buy” scheme in the latest budget, the Chancellor is doing his best to stimulate economic growth through construction which will hopefully encourage consumption through the multiplier effect in an economy that has been anaemic since the financial crisis. The Government coffers will start to look better too due to higher stamp duty and income tax receipts. Who knows, it might also help in the polls. And it will work. We know this because Australia and Canada – two of the most expensive countries for housing in the world – have been running schemes like this for years.

The UK’s Help to Buy scheme will take two forms. The first part will offer buyers that qualify an interest-free loan (up to £120,000) from the Government. The second part will see the Government act as guarantor for a proportion of the borrower’s debt. In Australia, the “First Home Owner Grant” has been in existence in some form or another since 2000 and is a one-off grant to first home owners. It is not means tested and differs from state to state (in Sydney, the most expensive city in Australia, first home owners are currently entitled to $15,000 under the scheme). And in Canada, those looking at getting on the property ladder are entitled to a $5,000 tax credit and under the “Home Buyers Plan” can also withdraw up to $25,000 tax free out of their retirement savings to buy or build a home.

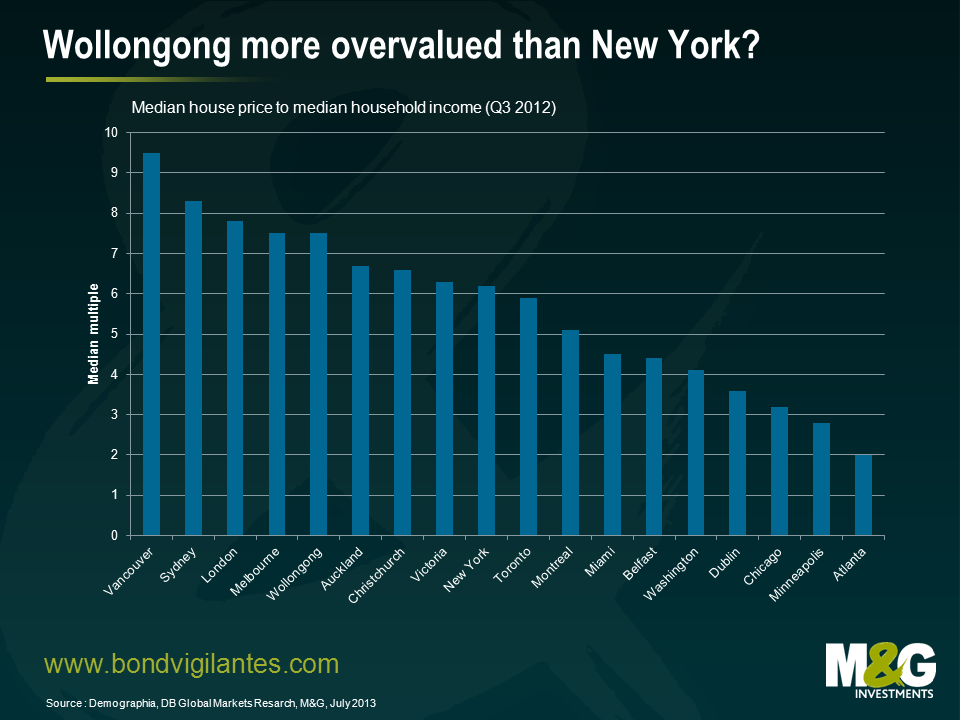

The problem is, these schemes have generally caused housing affordability to worsen in Australia and Canada. The chart below (courtesy of Torsten Slok at Deutsche Bank) highlights just how overvalued house prices are in parts of Australia and Canada. The fact that Wollongong ranks higher than New York on a house price to house income ratio seems like madness to me.

Another interesting result of Torsten’s affordability chart is the prevalence of New Zealand cities like Auckland and Christchurch. And you guessed right, New Zealand also has a form of the Help to Buy scheme, called the Welcome Home Loan. And if you are a New Zealander with some pension savings, you could be allowed access to your retirement savings to get on the housing ladder.

Home buyer schemes push up prices primarily through the accumulation of mortgage debt. Arguably financial companies have done the correct thing in tightening lending standards and reducing loan-to-value ratios. With the UK government now guaranteeing up to 20% of a new mortgage, those “riskier” types of borrowers that previously wouldn’t have qualified for a mortgage now have the ability to enter into the housing market. Demand increases, supply may not respond to the same extent and prices rise. Additionally existing home owners may sell their home and acquire more debt in order to buy a more expensive home. Who knows, mortgage equity withdrawal levels might come back in a big way too. But sooner or later, the house of cards will come crashing down – as we are all very familiar with.

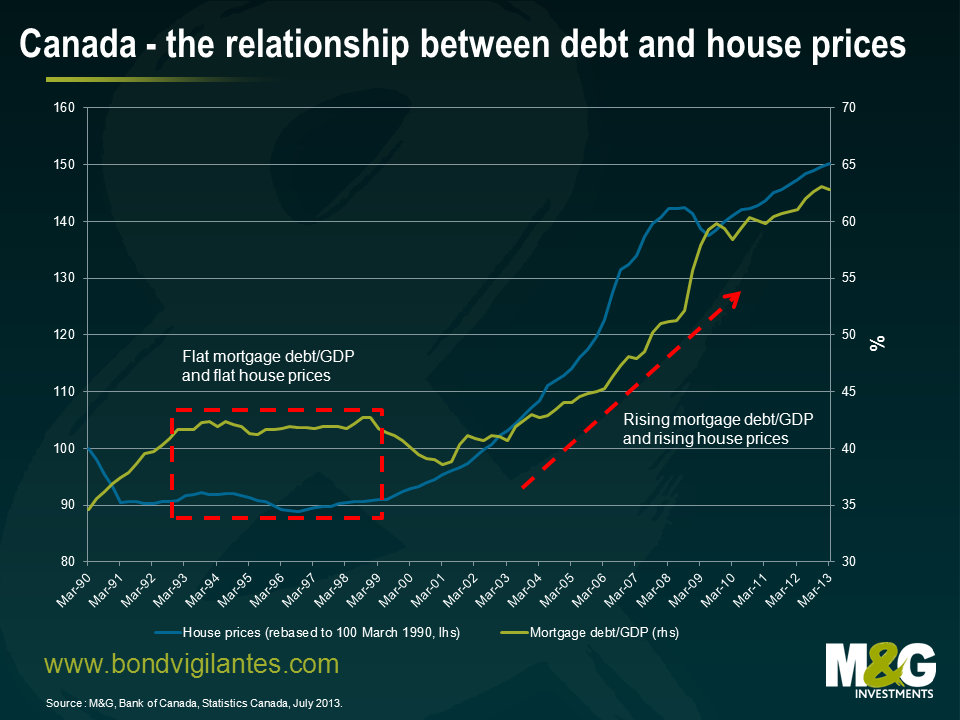

The charts below highlight the relationship between rising levels of mortgage debt and house prices in Australia, Canada and the UK. Australia is a very interesting example as the First Home Owners Grant has been increased and decreased over time with house prices suitably responding.

The UK’s Help to Buy scheme is most likely going to encourage a further accumulation of mortgage debt, leading to higher house prices, causing housing affordability to worsen from current levels for those who don’t have access to the scheme. Arguably, this scheme will also make income inequality much worse, so those who aren’t in a financial position to buy a property will fall even further behind. It will also worsen the wealth age gap, i.e. it’s the older, existing homeowners who are most likely to benefit, to the detriment of younger people who don’t have a home and need somewhere to live.

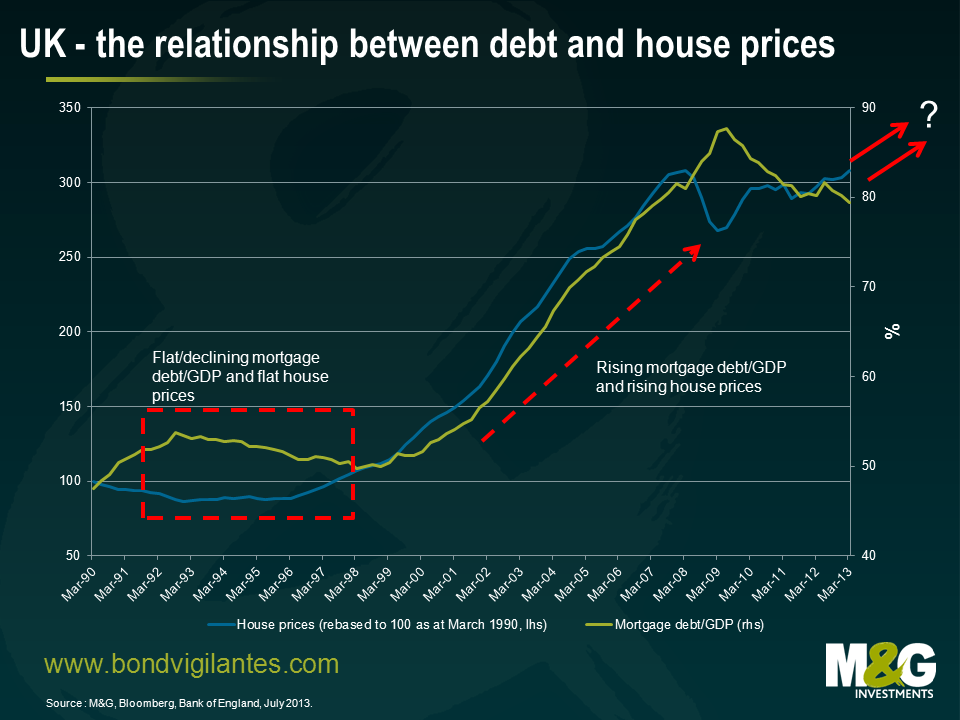

We have already seen evidence of house prices increasing in the UK, with yesterday’s RICS house price balance at levels not seen since January 2010. This data is consistent with the stronger house price data we have seen recently from mortgage lenders Halifax and Nationwide indicating that we are back at pre-crisis highs. One has to wonder whether a scheme encouraging financial companies to lend and consumers to borrow is the brightest thing to do in an economy with £1.26 trillion (or 80% of GDP) mortgage debt outstanding. Especially as it is designed to make an already expensive asset even more expensive, which could lead to financial instability if the economy wobbles and ultimately cost the taxpayer big time.

With house prices set to rise further in the short term, the question has to be asked – is this a help to buy or help to sell scheme?

Just when you thought the Fed had well and truly killed the carry trade, a surprisingly dovish Mario Draghi reminded markets yesterday that Europe remains a very different place from the US. Having previously argued that the ECB never pre commits to forward guidance, yesterday marks something of a volte-face. ‘The Governing Council expects the key ECB interest rates to remain at present or lower levels for an extended period of time.’ The willingness to offer guidance brings the ECB closer to its UK and US peers, the latter having been in the guidance camp for some time. This firmly reinforces our view that the ECB retains an accommodative stance and an easing bias.

The willingness to offer forward guidance to the market no doubt came after some long and hard introspection within the Governing Council. So why the change ? Firstly, the ECB is worried that it may miss its primary target of maintaining inflation at or close to 2% over the medium term. Secondly, Draghi indicated an increasing concern that the real economy continues to demonstrate ‘broad based’ weakness, and finally, as has been the case for some time, the Council worries that the Eurozone continues to labour with subdued monetary dynamics. This sounds increasingly like Fed talk of recent years.

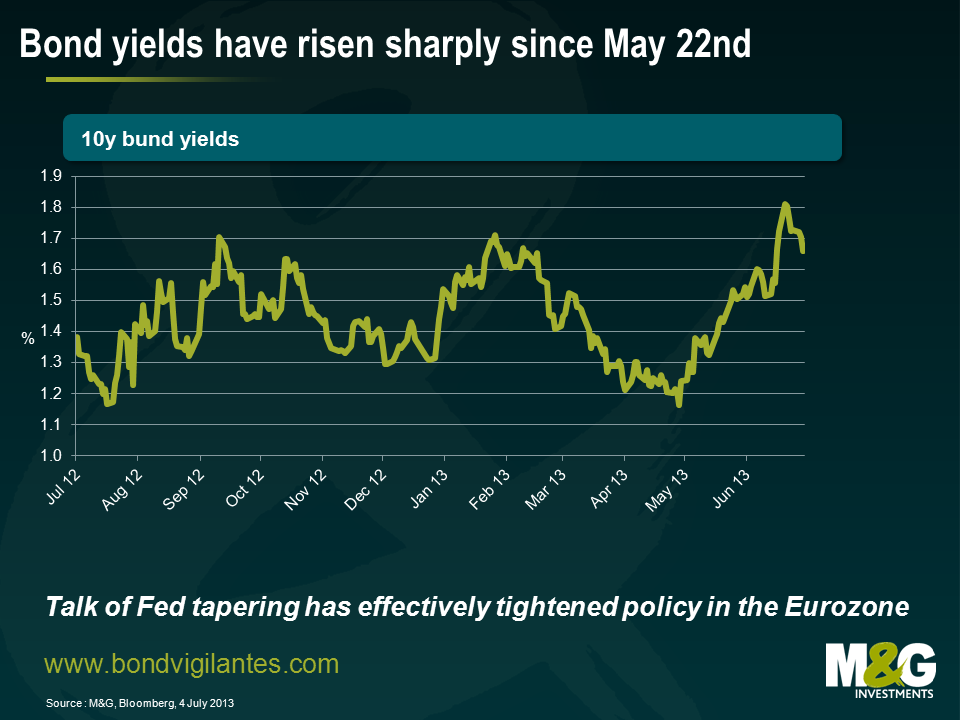

Draghi also expressed his concern yesterday during his Q&A at the effective tightening of monetary conditions via higher government bond yields (see chart) since the Fed’s tapering discussions. Frankly the last thing the Eurozone needs at this stage in its nascent recovery is higher borrowing costs.

Draghi in communicating that the next likely move will be an easing of policy has attempted to talk bond yields down. European risk assets appear to have taken his comments positively but the bond market remains sceptical. At the time of writing only short to medium dated bonds are trading at lower yields.

In conjunction with revising down its 2013 Italian GDP forecast from -1.5% to -1.8%, the IMF has publicly urged the ECB to embark upon direct asset purchases. Is this a likely near term response ? For now those calls will likely fall on deaf ears especially with German elections later this year. The ECB clearly believes that its next move would be to cut rates further in response to a weaker outlook. Buying time seems to be the current approach.

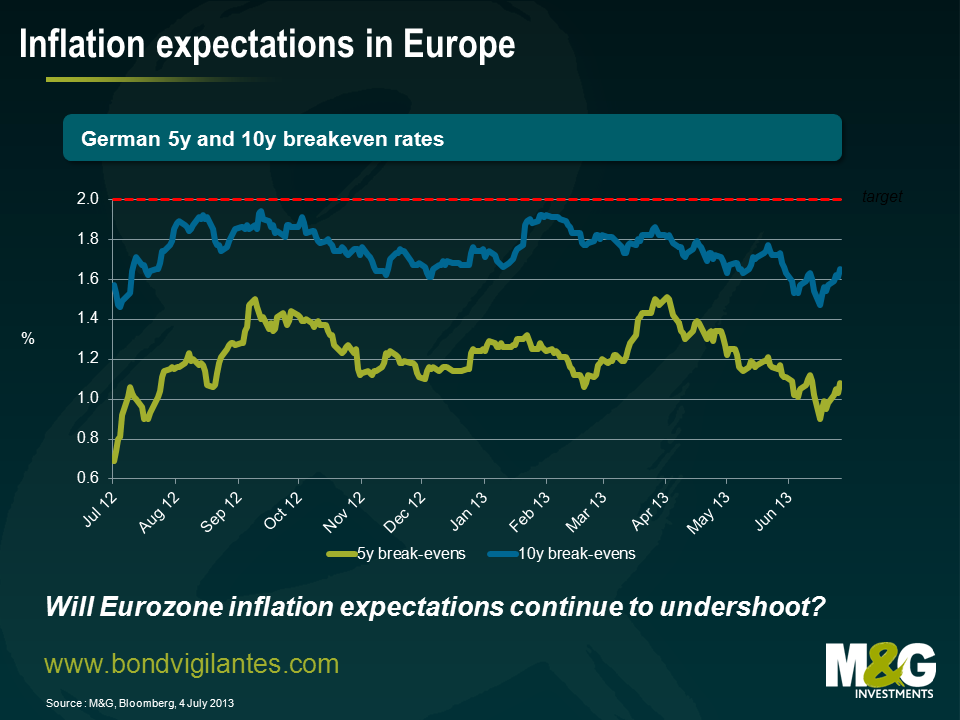

However, should Eurozone inflation expectations continue to undershoot (the market is currently pricing 1.36% and 1.66% over the next 5 & 10 years, see chart) and economic performance remain downright lacklustre across Europe, then the ECB will have to think very carefully about what impact it can expect from a ‘traditional’ monetary response. QE may be some way off, and would no doubt see massive objections from Berlin, but in the same way that the ECB never pre commits, maybe just maybe, QE will be on the table sooner than the market is currently anticipating.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.