Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

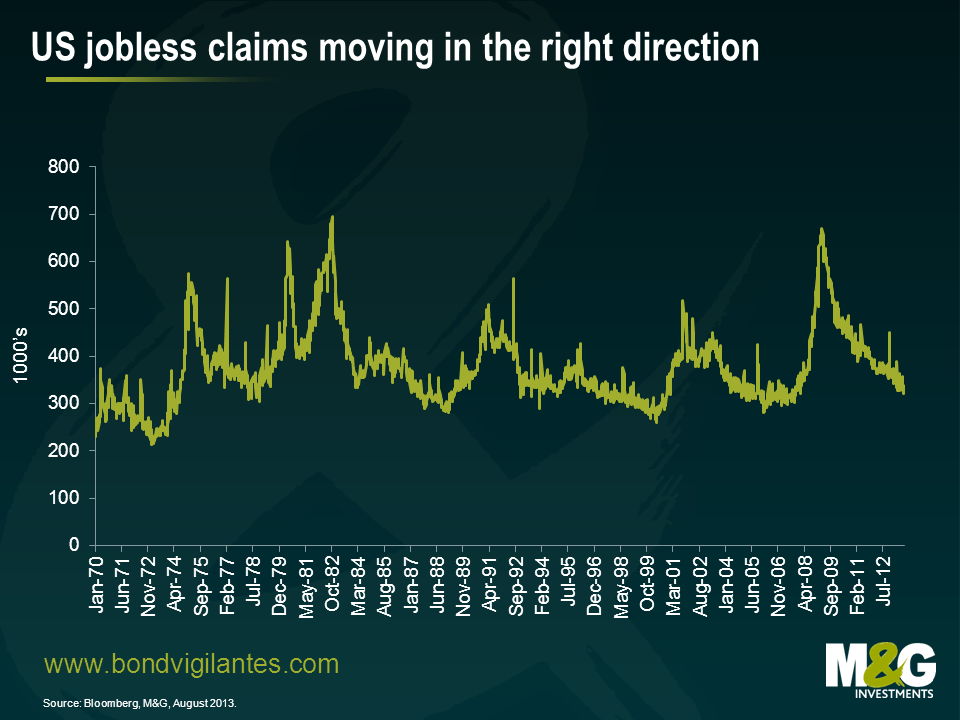

Today’s release of jobless claims shows that the US economy is continuing its healthy response to the stimulus provided by the Fed. Momentum in the US labour force remains in a positive direction.

The very long term chart below shows today’s headline number of 331,000 to be relatively low historically. However, this is actually understating the current strength of the labour market.

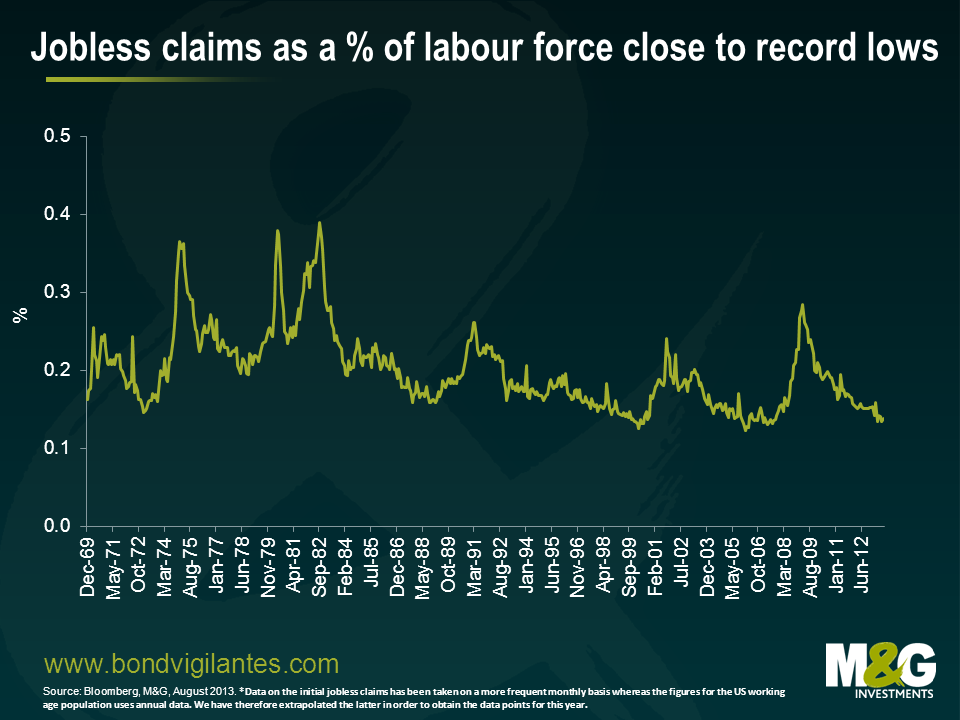

In order to interpret the jobless rate more effectively we need to look at it as a percentage of the ever increasing labour force, and not just the headline number. We have made those adjustments in the chart below.

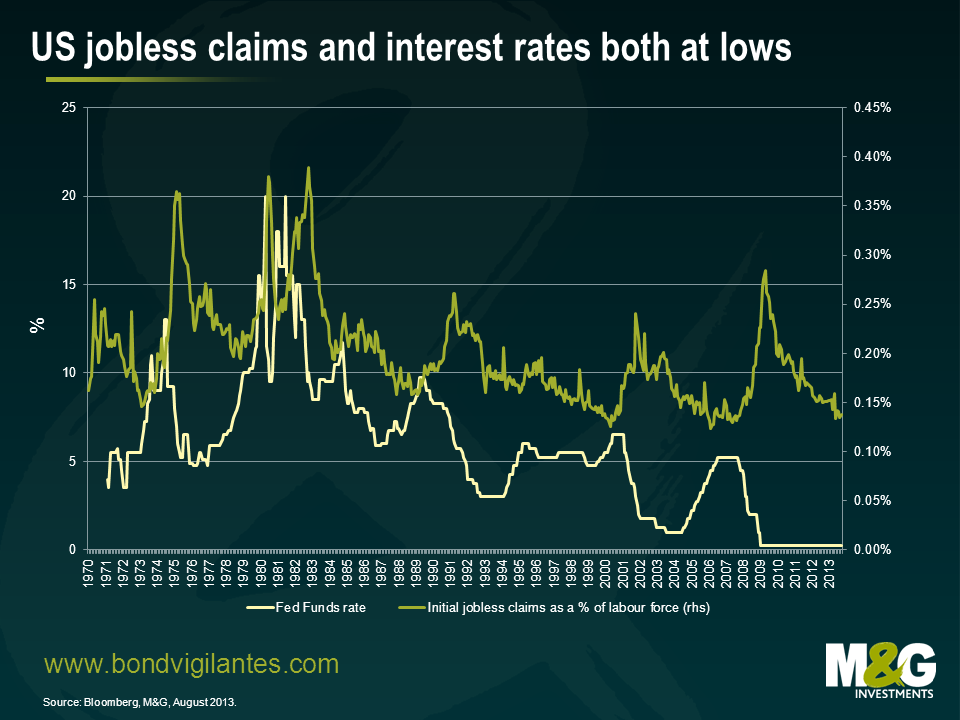

The fact that the economy has thankfully responded to low rates is good, though not new, news. However, the one thing that is very different this time is where we are in the interest rate cycle. At previous lows in jobless claims the Fed has typically been tightening to slow the market down. This time they are still in full easing mode with conventional and unconventional policy measures. This contrasts dramatically with the lows in jobless claims in the late ’80s and the beginning and the middle of the last decade, when the Fed was already in full tightening mode. This is highlighted in the chart below.

As you would expect to see, interest rate policy works with a lag. Given that we are unlikely to see conventional tightening for a while, one would expect the US economy to remain in decent shape.

A bear market in bonds can be seen as predicting a future normalisation of rates. If, like the Fed, you recognise that this time around things are not all normal, then you could expect short rates to stay low and employment growth to continue. The extent of the current bear market in bonds is therefore limited by the new environment we are in, where conventional economic systems have been amended and changed by the financial crisis.

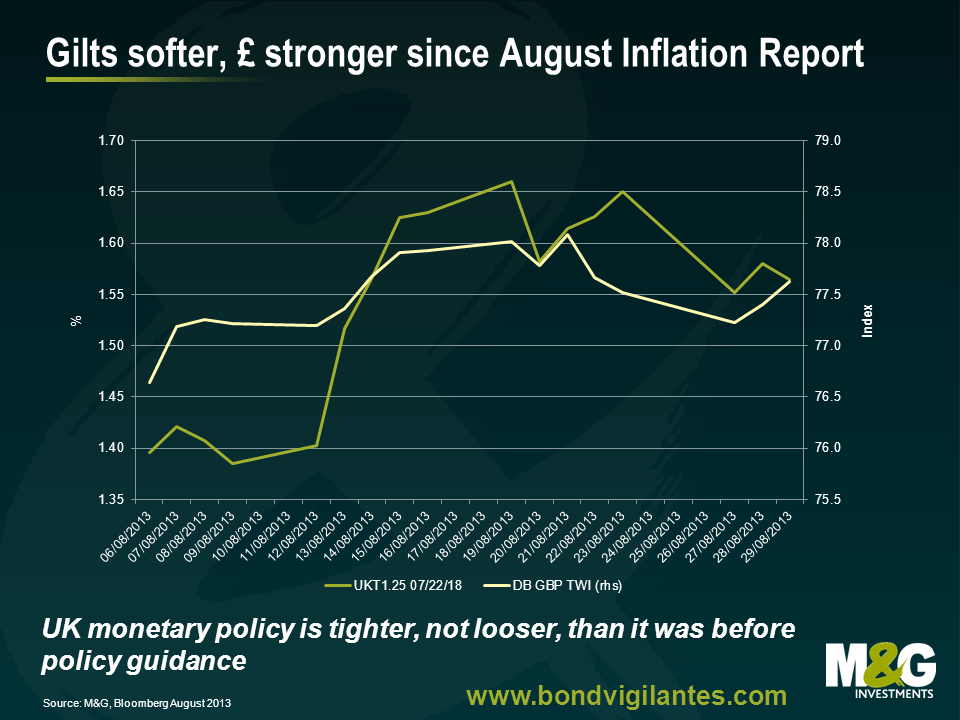

Millwall FC wasn’t the only team to trek up to Nottingham yesterday from London and to come back empty handed (at the hands of the mighty, mighty Forest). Team Carney from the Bank of England also had an unproductive time of it in the East Midlands as the new Governor gave his first speech in the role to the CBI, Chamber of Commerce and the Institute of Directors. Since the publication of the August Inflation Report, in which the Monetary Policy Committee delivered its framework for forward guidance, the markets have done the opposite of what the Bank had hoped for. The gilt market has sold off – not just at medium and long maturities, which are largely outside of direct Bank control and are more dependent on global bond market trends, but also at the short end, where 5-year gilt yields have risen by 20 bps in under a month. There has also been a de facto tightening of UK monetary conditions through the currency. Trade weighted sterling is 1% higher than it was before forward guidance came in. Both the gilt market and the pound went the “wrong” way as Carney discussed forward guidance yesterday afternoon. The Overnight Index Swaps market (OIS), which prices expectations of future official rate moves, fully prices a 25 bps Bank rate hike between 2 and 3 years’ time.

So why don’t markets believe Mark Carney? In yesterday’s speech he was clear that the UK’s economic recovery was “fledgling”, and weaker than recoveries elsewhere in the world. He spent some time discussing how a fall in unemployment to the 7% threshold would mean 750,000 new jobs having to be created, which would take some time, possibly three years or longer. And even if growth picked up, it didn’t necessarily follow that jobs growth would be strong. But two things led gilts lower yesterday afternoon. Firstly there was the announcement that UK banks would be able to reduce the amount of government bonds that they hold as a liquidity buffer so long as their capital base is over 7% risk-weighted assets – potentially triggering sales of tens of billions of gilts over the next couple of years. But more importantly, Carney’s attempted rollback from the “knockouts” stated in the Inflation Report was not strong enough.

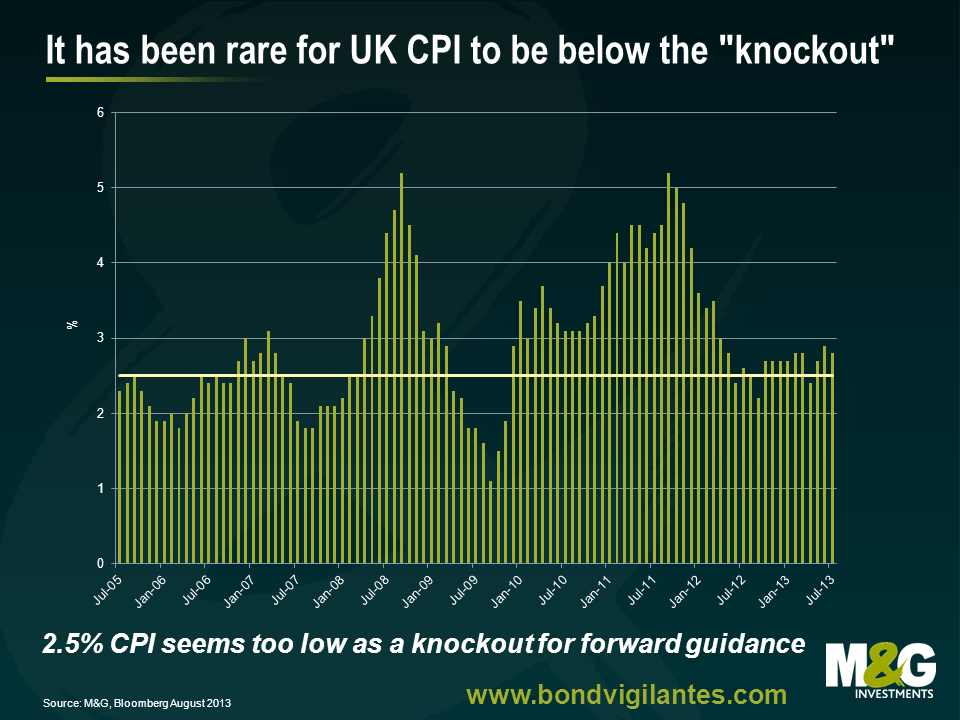

On page 7 of the Inflation Report, after detailing the forward guidance linking rates and asset purchases to the 7% unemployment rate, there are three “knockouts” which would cause the guidance to “cease to hold”. The first knockout is the most important. If CPI inflation is, in the Bank’s view, likely to be 2.5% or higher in 1 1/2 to 2 years’ time then the unemployment trigger becomes irrelevant. The other two knockouts were that medium term inflation expectations become unanchored, and that the Financial Policy Committee judges that the monetary policy stance is a significant threat to financial stability.

So for all the talk of the UK’s weak economy, and the accommodative stance that the Bank will take to allow the unemployment rate to fall to 7%, perhaps over many years, don’t forget that if CPI inflation looks likely to be at 2.5% or higher, the MPC will ignore the jobs market promise. Since the middle of 2005, UK CPI has been at or above 2.5% most of the time, through a strong economy and (for longer) the weak economy. Since the start of 2010 there have only been 3 months of sub 2.5% year-on-year CPI. And in 2008 and 2011 the year-on-year rates exceeded 5%.

Of course, the Bank of England can forecast inflation to be whatever it likes over the next 1 1/2 to 2 years. Its inflation forecasts have famously been awful for years, always predicting inflation would return to 2% when it always was much higher than that. But it will be important for Carney to earn some credibility here in the UK, and the days of the Inflation Report’s “delta of blood” inflation forecast always showing a mid point for future inflation of 2% must surely have ended when Mervyn King left. What does the outside world think about the prospects of UK inflation being below 2.5% in the future? Here the news is better – the consensus broker economic forecast is for CPI to fall to 2.4% in 2014 and 2.1% in 2015. And the implied inflation rate from the UK index-linked gilt market is for an average of 2.8% per year over the next five years on an RPI basis, which given the structural wedge between RPI and CPI suggests that the market’s CPI forecast is somewhere below 2.5%. M&G has launched a new Inflation Expectations Survey, together with YouGov. We should have August results shortly, but in our last release we saw that 1 year ahead UK consumer expectations of inflation ran at 2.7% (a fall from 3% a quarter earlier) and 5 year ahead expectations were at 3%. Higher than the 2.5% target, but consumer expectations are often higher than the market, and the 3% level has been stable (well “anchored”).

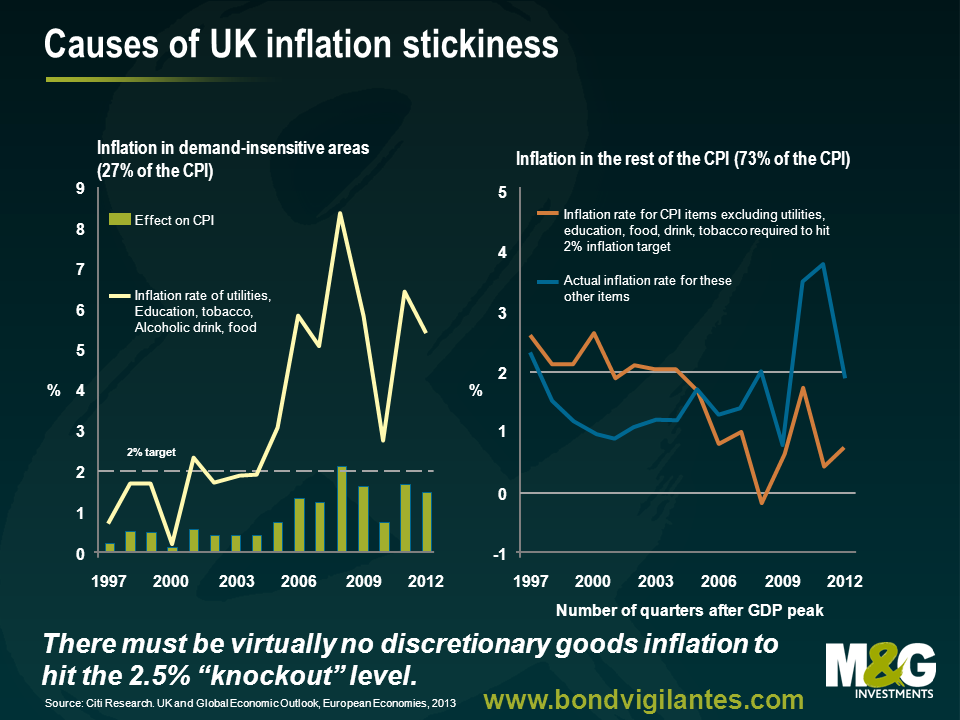

But as we have seen, UK inflation has been notoriously sticky. Not because consumers are demanding more goods than the shops can supply (although there has been some long awaited good news from the retail sector lately, with sales stronger), as in general real incomes have been squeezed and discretionary spending has been hit. But because non-discretionary items, like food and energy costs, have substantially exceeded the inflation rates of consumer goods. Add to this administered prices relating to public transport costs or university tuition fees and we can see that the UK’s “inflation problem” is potentially something that a monetary policymaker can only influence by forcing discretionary spending into deflation. The chart below shows that so long as the non-discretionary basket of goods keeps inflating at around 5% per year, there must be virtually no inflation in discretionary goods in order to get below Carney’s 2.5% knockout.

So it is going to be tough for the market to believe that the CPI inflation “knockout” won’t have a decent chance of coming into play well before the 7% unemployment threshold is reached. I think Carney missed an opportunity to move away from the knockouts yesterday – he certainly didn’t use the term again, and implied that the gilt market’s move lower was driven by international developments and over-optimism about the prospects for a quick fall in UK unemployment. But the three knockouts were almost dismissed in the sentence “provided there are no material threats to either price or financial stability” rather than given the prominence that they were in the Inflation Report. But it looks as if the gilt and currency markets need something stronger if they are to produce the monetary easing that, from Carney’s bearish analysis of the UK economy, it still needs.

August is usually a dull month in German politics. It’s holiday season, and national parliamentary politics takes a break at the same time. However, this year German politicians don’t have time to put their feet up. The period of parliamentary recess marks the peak of the electoral campaign in Germany before the general elections take place on 22 September. Many people seem to expect that not only will the holiday period end in September, but also the recent lull in European politics. The hope is that the European Union, and the Eurozone in particular, will finally move on to sorting out its structural issues once the German elections are over. I’m not really convinced that this is going to be the case, and here is why.

Not much upside from a shift in policy

Angela Merkel has indicated she would like to renew the current coalition with the liberal FDP after the general elections in September, while the Social Democrats (SPD) and Greens strive for a remake of their 1998/2002 electoral victory. Merkel’s Christian Democrats are currently far ahead in the polls, but a renewal of the coalition with the stumbling FDP is highly uncertain. On the other hand, a coalition of SPD and Greens looks as probable as an English victory against Germany in a football tournament through a penalty shootout. This could leave the two major parties, CDU/CSU and SPD, with the choice of immediate snap elections or a grand coalition. I tend to believe that they would not ignore the electoral will of the German people who remain very open towards the idea of a grand coalition. The recent figures from one of the major German polls, the ARD-DeutschlandTrend, suggest that 23 per cent would prefer a coalition of CDU/CSU and SPD, while the parties’ preferred coalitions qualified for 17 per cent of the poll votes each. In addition, around half of the Germans have consistently described a coalition of CDU/CSU and SPD as a very good or good option over the past few months. If CDU/CSU supporters are left with a coalition choice between Greens and SPD under the assumption of a shortage of combined votes with the FDP, then polls suggest a strong preference for the SPD. That is, the most likely coalition options after the general elections seem to be: CDU/CSU and FDP (existing coalition) or CDU/CSU and SPD (grand coalition).

It stands out in the current electoral campaign that Europe has not been a major topic. European politics does not feel like a policy area where the major opposition party SPD can win votes or would be able to distinguish itself sufficiently from the government’s policy stance. This has also been reflected by the previous legislature period when the opposition parties widely tolerated Merkel’s course on Europe. Bearing the previous policy stance as well as the current polls in mind, I struggle to find strong arguments why a new German government would fundamentally change European day-to-day politics. I expect a continuation of the pragmatic approach of austerity-focused, but sufficiently accommodative steps to keep the Eurozone together, including another bailout package for Greece that treasurer Schäuble hinted upon. Thus far, this political approach has proven to be fairly successful domestically. It feels that it’d require a major game changer to trigger an immediate change in policy. It seems more likely that any political developments with regard to Europe may rather be undertaken with a long-term time horizon.

Deeper European integration could require a referendum in Germany

While a newly elected German government might find it politically too costly to redefine European day-to-day politics, it could also struggle to conclude long-term structural reforms – ranging from Euro bonds, more centralised European governance of national budgets to full political and fiscal union. The president of the German Constitutional Court, Andreas Voßkuhle, pointed out in 2011 that the German Constitution does not allow for further significant European integration. He concluded that the additional transfer of national sovereignty to the European Union, eg the national budget, would require a referendum. This is very noteworthy as Germany has not had a referendum in its post-war history despite the adoption of a new constitution, membership in the European Union as well as the re-unification of East and West Germany. The preparation of a referendum takes a significant amount of time, and the selection of a date is a sensitive issue. In this instance, it might also take time to explain to the public why the proposed structural changes, eg a political and fiscal union, would be in their long-term interest and how it would affect their life as national citizens. The referendum would most likely be based on the adoption of a new European Union treaty which would provide for the future design of European politics and governance. The ratification process and enactment of the last EU treaty, the Lisbon treaty, took more than five years from June 2004 to December 2009. Factoring for some potential political goodwill this time, wouldn’t the next German general elections in 2017 be a reasonable point in time to ask the political parties to communicate their positions on the subject and to let voters subsequently decide upon their future within Europe (or outside)?

Policymakers are unlikely to bear political and fiscal costs amid uncertainty

This may sound familiar to our British readers whose Conservative party has already announced its intentions to call for a referendum on Britain’s future in the European Union by 2017. In the UK, the Conservative party’s commitment to 2017, as well as the prospect of an indispensable referendum in Germany (and elsewhere in Europe), might have set a reasonable deadline for European leaders to develop a concept for the future institutionalisation and integration process of the Union, including the Eurozone. This could then be ratified across Europe, including Germany. Not 2013, but 2017 could mark a historically important year for European politics as national voters could be asked to re-commit to a deeply integrated (and burden-sharing) Europe. If such a scenario for Europe turns into a national government’s base case, it will be difficult to picture these policymakers agreeing on politically and fiscally costly policy measures that go beyond the current pragmatic attitude towards Europe. This argument could not only hold with regard to the aforementioned countries – Germany (anything beyond emergency bail-outs for Eurozone peers) and the UK (financial regulation and EU banking reform) – but also for governments that currently face a strong headwind in the polls. A very recent example is the political situation in the Netherlands where the current government would be dwarfed to a vote share of 23 per cent from a share of 53 per cent in last year’s elections, while the right wing and euro-sceptical party PVV has gained around 10 per cent in electoral support.

If I had to draw a roadmap for Europe until 2017, then the first part of this political journey would carry significant risk of a slow moving city traffic experience, but which could ultimately end on the high-speed Autobahn.

The disclosure of the latest Federal Open Market Committee (FOMC) meeting minutes last night has pushed the US bond market to new lows for the year, further extending the current bear market in world government bonds. Looking at what the Fed is doing is nothing new. Back in the day when I first started, we had dedicated teams of Fed watchers, trying to work out its next move, as rate changes were frequent and unpredictable. The current policy is to make less frequent changes and be more transparent. So what does the FOMC’s forward guidance by providing its internal thoughts tell us today?

The committee knows that what is discussed will affect the markets, so a stylised version of its discussion needs to be produced. The release of the minutes is a manufactured and glossy disclosure of its work presented to make the FOMC look good and influence its followers. So what was the message from last night?

Well, it is more of the same about the need to tighten as we previously blogged here. The Fed continues to follow the script. The basic scenario is that they need to get the party goers out of the bar with the minimum trouble. This is why the Fed is keen for us to see that they discussed reducing the unemployment threshold at the last meeting. This is akin to saying ‘drink up’ to a late night reveller, with the hint that once they’ve done so there is a chance the bar staff will pour them another drink.

The Fed wants a steady bear market in bonds in this tightening cycle as it is still fearful over economic strength and fortunately inflationary pressures remain benign. This is very different from major tightening cycles in the past such as 1994, when the Fed was more keen to create uncertainty and fear in the bond market as they wanted to tighten rapidly and were still fearful of inflation given the experience of the 70s and 80s.

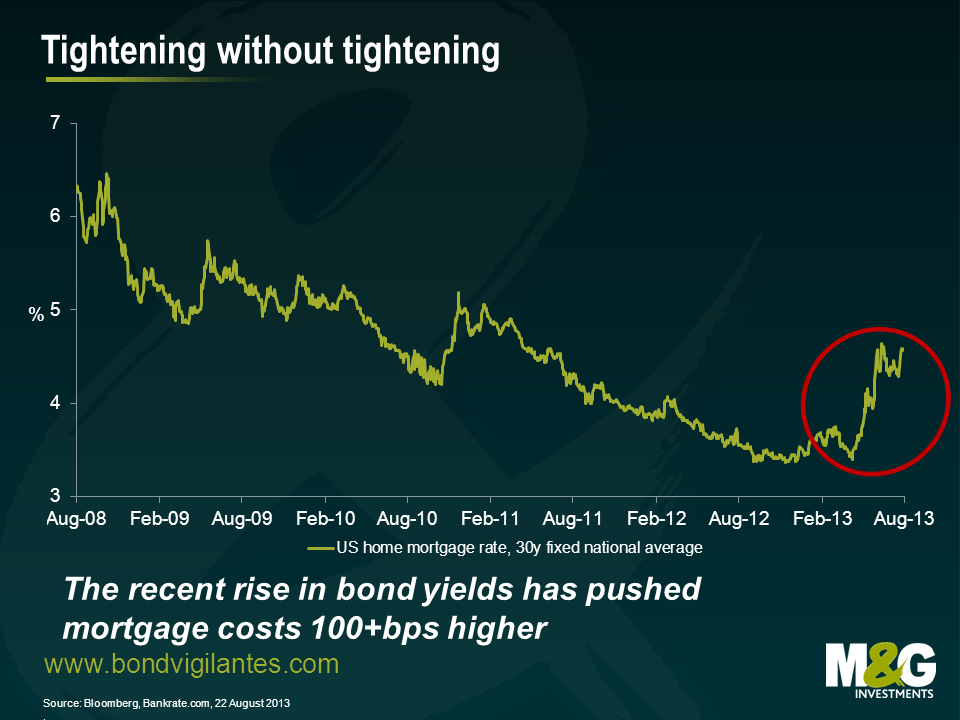

So when will official interest rates go up? Strangely you could argue that the successful creation of a steady bear market in bonds extends the period they can keep rates on hold. Monetary tightening via the long end reduces the need for monetary tightening in the conventional way. For example, as you can see from the following chart, the 100bps or so sell-off in 30 year treasuries since May has translated into a similar move higher in mortgage costs for the average American.

If the Fed has its way in guiding a steady bear market in bonds, then bizarrely short rates could indeed stay lower for longer.

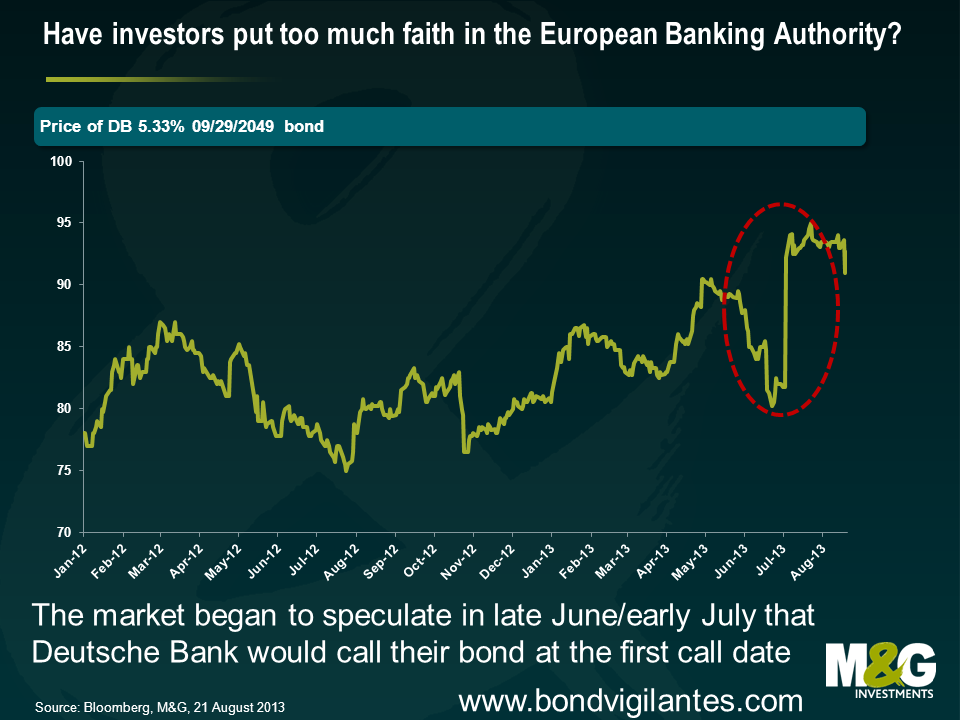

It turns out that market participants may have put too much faith in the European Banking Authority (EBA). The EBA’s answer to a submitted question indicated that non-called bank Tier 1 instruments – or at least those similar to one described by the questioner – cannot simply be reclassified as Tier 2 capital after the first call date. The EBA’s answer to this specific question – which some wrongly characterised as an “EBA ruling” – fuelled speculation that all callable Tier 1 would henceforth be called at the first call date because of a loss of capital credit. Deutsche Bank’s 5.33% Tier 1, callable on September 19, 2013, leapt in price.

The market began to speculate that Deutsche Bank – which has declined to call capital instruments before – would have a change of heart and redeem this bond at the first call date. We don’t want to comment specifically on Deutsche Bank’s decisions here, but this non-call demonstrates why we don’t believe that investors can or should base valuations on their own predictions about whether or when banks will redeem their callable capital instruments. And the point to bear in mind here is that capital credit is just one factor for banks to consider when asking their regulator for permission to redeem an instrument. The importance of capital credit – and of elements within the tiers of bank capital – will vary widely from bank to bank. Finally, regulators need to approve the redemption in any event.

So is this the beginning of a trend of banks not calling their hybrids? We wouldn’t make such a sweeping declaration. First, even with the EU Banking Union project underway, many decisions are still made at the national level with respect to capital. CRD IV, the new Capital Requirements Directive that implements Basel III within the EU, is still being passed by legislatures of the member states. It’s possible that some home country regulators are allowing banks to continue to count their hybrid Tier 1 securities as Tier 1 capital through the end of 2013 irrespective of a call being missed. That may mean redemptions in 2014. Or it may not: these bonds might still be useful for banks as a buffer to protect their senior funding under new rules that banks will have to have a minimum amount of liabilities available for write-down or conversion to equity in case of a resolution.

So far this year returns for the high yield market seem solid if unspectacular; 2.9% for the global index, 4.5% for Europe and 3.4% for the US. However, these overall numbers mask some interesting gyrations within the markets. It’s been a mixed year for government bonds but a solid year for credit spreads. Indeed, recent moves in the sovereign bond markets continue to focus investors’ minds on the haunting spectre of interest rate risk. The high yield market is not entirely immune to such fears but we need to remember that interest rates are only one driver of performance. High yield returns are also subject to factors such as changes in credit spreads, default rates and carry.

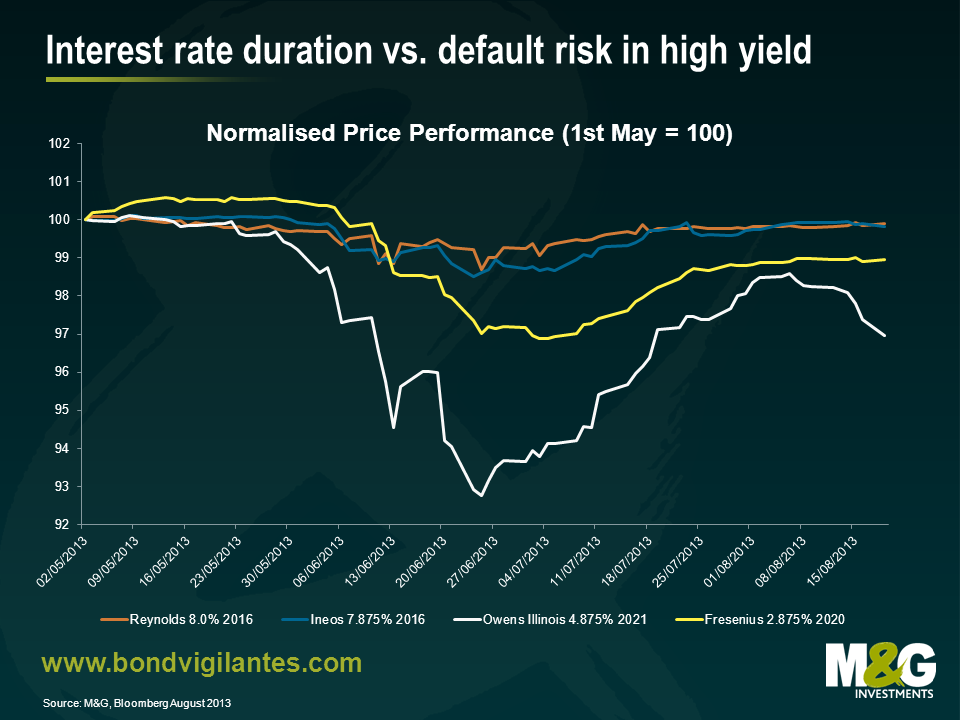

To illustrate this, we have two sets of bonds below: two long dated BB rated bonds (issued by German healthcare business Fresenius and US listed packaging group Owens Illinois) and two short dated CCC bonds (issued by the global chemicals company Ineos and another packaging group, Reynolds). The BB bonds carry relatively more interest rate risk than the latter due to their longer maturity, but less credit risk given the higher credit rating.

| Price | S&P Rating | Moodys Rating | Spread (bps) | Modified Duration (yrs) | |

| Fresenius 2.875% 2020 | 100.25 | BB+ | Ba1 | 162 | 6.1 |

| Owens Illinois 4.875% 2022 | 102.6 | BB+ | Ba2 | 313 | 6.1 |

| Ineos 7.875% 2016 | 101.25 | B- | Caa1 | 503 | 2.1 |

| Reynolds 8.0% 2016 | 100.125 | CCC+ | Caa2 | 565 | 2.8 |

Source: Bloomberg, M&G, August 2013

So how have these bonds fared over the past few weeks ? The chart below shows the relative price performance.

The chart shows that none of the bonds were immune to the volatility we saw over the summer. Indeed this was a relatively rare period where interest rate duration and credit risk premia moved in tandem. However, what is clear is that the longer dated bonds suffered more during the correction. When we consider total returns, this becomes more stark. The table below shows the impact of the different coupons over the three months in question. Again, the shorter dated CCC bonds fare better.

| Period 01/05/13 – 19/08/13 | Price Return | Income Return | Total Return |

| Fresenius 2.875% 2020 | -1.05% | 0.85% | -0.20% |

| Owens Illinois 4.875% 2022 | -3.03% | 1.37% | -1.66% |

| Ineos 7.875% 2016 | -0.18% | 2.31% | 2.13% |

| Reynolds 8.0% 2016 | -0.10% | 2.37% | 2.28% |

Source: Bloomberg, M&G, August 2013

The point here is that judiciously taking on more default risk in the form of a higher coupon and or spread whilst at the same time minimising your interest rate risk by focusing on short dated bonds, is one way that fixed income investors can ride out greater volatility within the government bond markets and still look to generate positive total returns. In this environment, default risk (as opposed to duration) really is the lesser of two evils.

The governor at the Bank of England stepped forward last week with guidance about its future plans and conditions regarding the tightening of monetary policy. Ben gave his views on the announcement here last week, but what I am going to focus on is the 7 percent unemployment rate ‘knockout’.

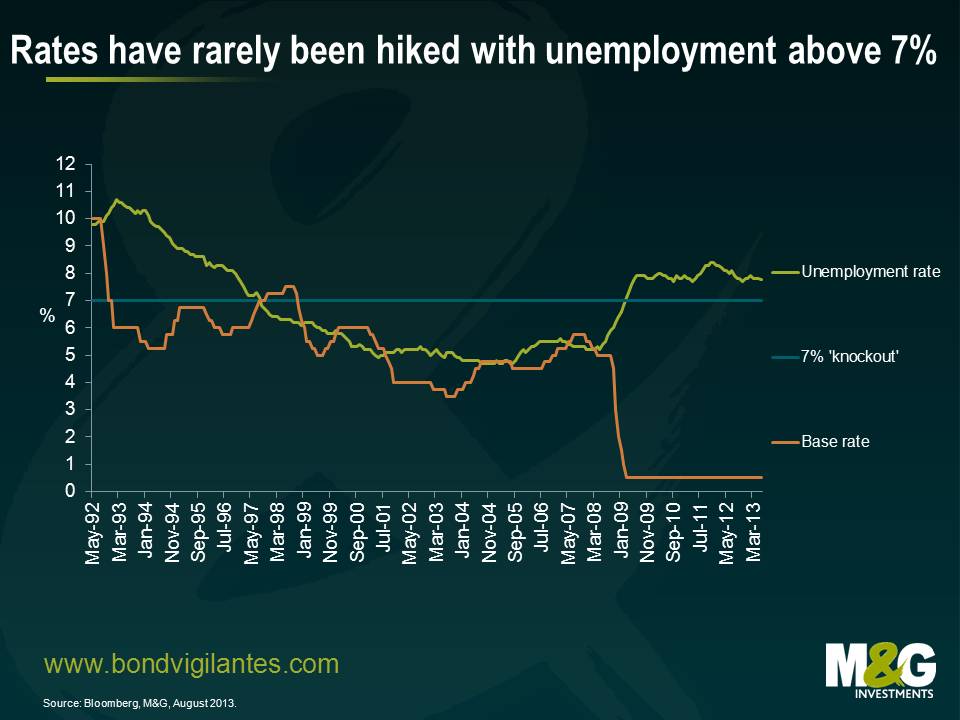

Firstly, why has the Bank of England decided to use the unemployment rate as an indicator of inflationary pressures? Well, in the press conference they expressed that this is a good indicator of excess capacity. This has some obvious logic to it, so let’s explore this knockout level in an historical context.

Below is a chart of UK unemployment going back 20 years. As you can see, the rate was below 7 percent from 1997 to 2009 – a period of good economic growth where the bank acted regularly to tighten policy to keep inflation under control. In fact this new knockout does not appear to be new news, as the bank rate has rarely increased when unemployment exceeded 7 percent over this period.

Looking at the next chart you can see the regions that currently have unemployment at 7 percent or below and the ones that do not. This regional disparity is not as strong as in Europe, but is something one should take into account.

Mobility of labour is needed for the rate to fall below 7 percent, with work relocated to labour and labour relocated to work. This is beyond the Bank of England’s remit, and is more of a central government economic project. The better regional labour mobility is, the quicker the UK can get unemployment below 7 percent. So, the easier it is to move house, or the quicker transport links are, the quicker unemployment can get below 7 percent. If regional labour mobility in the UK is very rigid then getting below 7 percent may not occur for years.

One new factor that we should take into account is the developing context of the wider European labour market. The UK workforce is not only competing as a whole internationally, but within the domestic economy it now also competes with international labour. The free movement of labour in the European Union combined with high rates of unemployment on the continent means that UK unemployment (spare labour capacity) can no longer be set with reference to our domestic borders. The huge pool of available labour could well dampen reductions in UK measured unemployment, aided by the UK’s tradition of welcoming foreign labour, its diversity of population (especially in areas seeking workers), and the fact that English is a well taught second language abroad. This could well act to reduce the ability of unemployment to fall in the UK despite low policy rates.

Even if the UK economy does respond to monetary policy and we reach escape velocity, labour immobility in the UK and or the supply of continental labour will have a baring on when the 7 percent unemployment rate is knocked out. Using this as a signal to raise rates could well mean that rates stay low for a long time even as the economy recovers.

One of our most popular posts of all time was written back in 2011. The subject was not the US losing its AAA rating, the impact of the default of Lehman Brothers or any other weighty matter of great economic import, but rather a quick look at how packets of Monster Munch were getting smaller over time and the associated inflationary impact.

Hence my surprise when I went into a shop last weekend and saw that Monster Munch packets have now been restored to their old 40g size, replacing the measly and frankly unsatisfying 22g version of recent times.

Further research on the manufacturer’s website revealed that

“ … The re-launch comes in response to growing consumer demand and will take Monster Munch back to the original retro pack design and old texture, flavour and crunchiness that consumers remember and love … Consumers have made it clear through both our own research and within online communities that they miss Monster Munch the way it used to be ..”

I like to think that our blog was the spark that lit the fuse of this virtual nostalgia-laden fast food insurgency. A resounding victory for bondvigilantes.com fighting in the name of consumer activism!

But wait, it gets better. Back in October 2011, the M&G coffee shop charged 45p for 22g, or 2.05 pence per gram. Today, the same shop charges 65p (RRP 50p) for a 40g packet, or 1.63 pence per gram. This is a fall of 20.5% in nominal terms. Put simply, you are also getting more for your money.

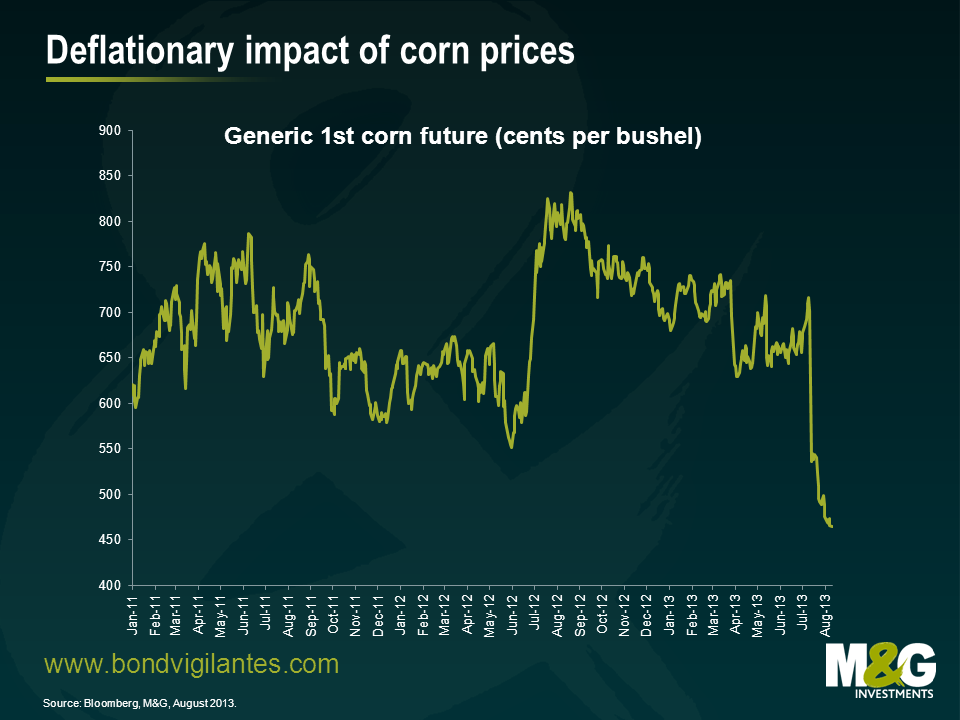

However, before we applaud the manufacturer for their largesse, let’s look at the main raw material. Back in October 2011, we pointed out that the headline cost of Monster Munch closely followed the corn price.

Since October 2011 the corn future has fallen by around 28.5% in price to $4.64 per bushel, a rare case of deflation in recent times. In sterling terms, the fall is around 25.5%. Accordingly, the dramatic fall off in corn prices has allowed the manufacturer to pass on part of this benefit to consumers, reducing the headline per gram price, but at the same time retaining some of the benefit in the form of an enhanced profit margin.

So whilst we cannot claim all the credit for this victory, this is a rare piece of welcome news for the consumer of corn based snacks.

Listening to the Bank of England Quarterly Inflation Report press conference – the first with Mark Carney steering the ship – a song immediately sprung to mind. The song was written by a former student of the London School of Economics, Sir Michael “Mick” Jagger with his colleague Keith Richards in 1965. There is no better way to analyse the current thinking of the Bank of England than through one of The Rolling Stones best songs, (I Can’t Get No) Satisfaction.

The new BoE Governor began with the positive news that “a recovery appears to be taking hold”. This wasn’t news to the markets, as more recently we have seen a remarkably strong string of economic data. However, the very next word in Mr Carney’s introduction was “But…”. What followed was, in my opinion, the most dovish sounding central bank policy announcement since the darkest days of the financial crisis.

Carney firmly announced his arrival as the global independent (excluding BoJ) central banking community’s uber-dove through the acknowledgement of a broadening economic recovery in the UK, and then making explicit that the BoE remains poised to conduct more, not less, monetary stimulus. Until now, these two conditions were considered by bond markets to be pretty much incompatible.

Carney told us that the BoE will maintain extreme monetary slack (in terms of both the 0.5% base rate and the £375 billion of gilts held) until the unemployment rate has fallen to at least 7%. He went even further than this, stating the MPC is ready to increase asset purchases (QE) until this condition is met. However, there are two conditions under which the BoE would break the new, explicit link between monetary stimulus and unemployment: namely, high inflation and threats to financial stability. Did the new governor have to put these caveats in place because other members of his committee would only agree to the announcement if they were mentioned?

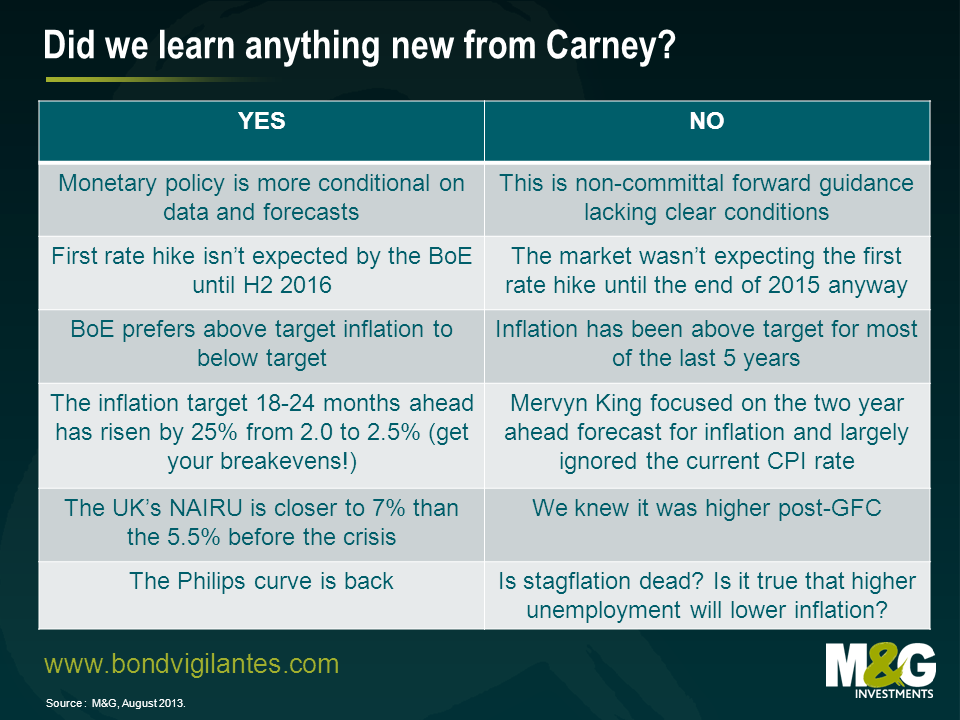

The new framework announcements were broadly in-line with what we were expecting. In that respect, the Governor’s major announcement was not too much of a surprise. The market agreed and there was a relatively muted response. Carney was supposed to fire our imaginations, so the question is – did we learn anything new? The “yes” and “no” arguments are outlined in the below table.

The market suspected Mr Carney would bring in some forward guidance, but I think the most interesting implication of this announcement today is that he felt the need to do something, but did not feel the need to increase asset purchases through QE. Mervyn took on the first part of Friedman’s equation, the supply of money. This was not inflationary as the transmission mechanism was broken, and the cash was hoarded and not released into the real economy. Could Carney be the governor to focus on the second part of the equation, money velocity? Forward guidance is designed to give individuals and companies the confidence to borrow in order to spend or invest. If they do, velocity will return as the transmission mechanism repairs. I believe we are considerably less likely to see an increase in QE under the new governor.

If forward guidance does not have the consequences Carney intends, and my belief that he is more focused on the transmission mechanism than his predecessor, what might Carney do next? At that point, he might increase schemes akin to Funding for Lending, and hand banks cheap funds at the point at which the banks release the loans to borrowers. This way, banks are heavily incentivised to lend at levels that are attractive to individuals and companies.

Carney told us that if and when unemployment reaches 7%, policy will start to tighten. But then he stated that if inflation exceeds 2.5% on the BoE’s shocking 2 year forecast (is this a rise in the inflation target?), or if inflation expectations move beyond some unannounced bound, or if financial stability is under threat, then he might have to break the newly explicit link between unemployment and monetary policy. And then he stated that even if unemployment hits 7%, this will not trigger a policy change, but a discussion around one.

I don’t think we actually got pure forward guidance, but a pretty muddled variant thereof. Bond markets are rightly unsure as to how to react, and have struggled for a satisfying interpretation. All we can really take from the BoE is that they will need to be sufficiently satisfied that the UK economy has reached escape velocity before hiking rates or reversing policy.

The early summer surge in bond yields will have focused the minds of many investors on the allocation of assets in their portfolios, particularly their fixed income holdings.

The largest risk to a domestic currency fixed income portfolio is duration. When investors discuss duration they are more often than not referring to a bond or portfolio’s sensitivity to changes in interest rates. Corporate bonds however also carry credit spread duration – the sensitivity of prices to moves in credit spreads (the market price of default risk).

Exposure to interest rate risk and credit risk should be considered independently within a portfolio. Clearly the desirable proportion of each depends heavily on the economic environment and future expectations of moves in interest rates.

I believe that the US economy and, to a lesser extent, the UK economy are improving and at some point interest rates will begin to move closer to their (significantly higher) long-term averages. We may still be a way off from central banks tightening monetary policy, but they will when they believe their economies are healthy enough to withstand it. Since a healthier economy increases the probability of tightening sooner, and is positive for the corporate sector, one should endeavour to gain exposure to credit risk premiums while limiting exposure to higher future interest rates.

In the latest version of our Panoramic series I examine the US bond market sell-off of 1994 to see what we can learn from the historical experience. Additionally, I analyse the power of duration and its importance to fixed income investors during a bond market sell-off.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.