Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

A couple of weeks ago I headed back to my hometown of Sydney, Australia. In between the barbies, the beach and a few beers, I managed to get around and film this short research video.

Australia is the 13th largest economy in the world and those that live there enjoy a very high standard of living. Growth is dominated by its service sector which makes up around 70% of GDP, whilst the total mining sector represents around 20% of GDP. With one of the most expensive housing markets in the world, a strong currency and the possibility of a China slowdown clearly on the horizon, will Australia’s economic performance over the next twenty years be as strong as the last?

At the end of October, the Citigroup Inflation Expectations survey showed a record jump in UK inflation expectations. The medium term expectation for UK inflation rose from 3.3% in September to 3.9%, and the number of people expecting inflation over 5% also rose significantly. Inflation expectations have become increasingly important in the UK because, as part of Bank Governor Carney’s new forward guidance regime announced in August, the Bank can raise rates even if unemployment remains high if inflation expectations become “unanchored”. Of course the period when the Citigroup survey was conducted was one where the major UK energy suppliers had announced annual price hikes of around 10%, and this spike in inflation expectations may well not persist. But it will have worried the Bank, and the gilt market fell on the release of the data.

Whilst UK inflation was making the news for its potential to surprise on the upside, Europe faced a very different scenario. October’s euro area CPI reading came in at an annual rate of 0.7%, down from 1.1% in September and below the market’s expectations. A Taylor Rule would suggest that with inflation so far from the ECB’s target of 2%, the central bank should be aggressively easing monetary policy (beyond today’s 25 bps cut, and beyond the zero bound to include QE?).

The next M&G YouGov Inflation Expectations Survey for the UK, European and Asian economies will be released in December. These M&G YouGov surveys are based on the best practice methodology discussed by the New York Fed (for example asking people about inflation rather than “prices of things you buy” as that sort of question tends to make people think solely of milk, bread and beer). We also have a bigger data sample than many of the other inflation surveys. Finally we also ask some interesting supplementary questions on issues like government economic policy credibility. As inflation expectations become increasingly important to central banks we think that we need to pay more attention to them – to date they have been well anchored, despite money printing through QE, but if this changes then so will central bank behaviour.

The Q4 M&G YouGov Inflation Expectations Survey will be released through Twitter. Follow @inflationsurvey to get the release time and date, and also to access the detailed report in December. The feed will also tweet on other inflation surveys and measures of inflation expectations. We hope you find it useful.

To encourage you to follow @inflationsurvey and be first to get the survey results, everybody who does so (and existing followers) will be put into a draw to win one of 15 copies of Frederick Taylor’s The Downfall of Money. This is the story of Germany’s hyperinflation of the 1920s, where the Reichsmark fell to 2.5 trillion to the US dollar, and the economy collapsed – arguably sowing the seeds of the Second World War.

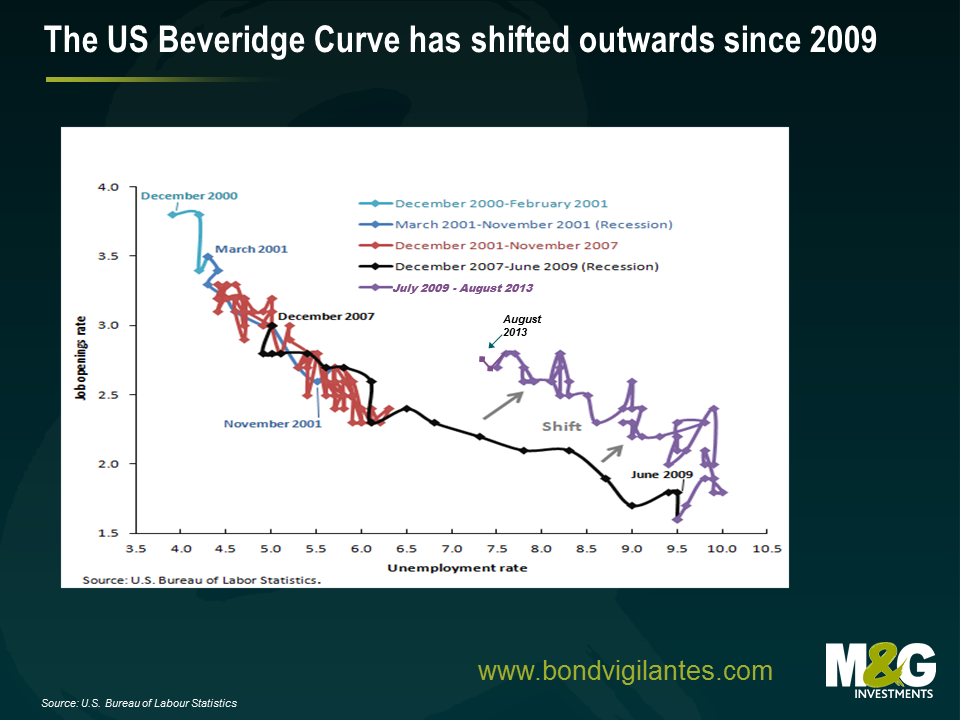

I am sure that many of us are familiar with some of the better known economic theories concerning unemployment which have previously been discussed or alluded to on this blog e.g. Okun’s Law and the Taylor Rule, but perhaps a lesser known theory (which has been receiving growing attention from economists in recent times), is the Beveridge Curve.

Using data on job vacancies and unemployment, the Beveridge Curve indicates how efficient an economy is at matching unemployed workers to job vacancies and can indicate where in the business cycle an economy sits. Looking specifically at data for the US from December 2000 onwards, the jobs market behaved as you’d expect; changes in the supply or demand for labour causes movement along the curve (this is particularly apparent during the highlighted recessionary periods). But what is particularly interesting – and glaringly obvious – is the shift which occurred post June 2009. The looping movement “back up the curve” is less surprising as after an economic contraction, this would be precisely what you would expect during a recovery period (i.e. falling unemployment teamed with an increase in the job vacancy rate as firms start to hire again).

But what could have caused this shift in the Beveridge curve, which if it remains, could imply a long term increase in structural unemployment?

1) Inefficiency. The shift is essentially indicative of an increase in the job vacancy rate. So perhaps we could argue that there has been a short-term reduction in the efficiency of job matching due to labour market conditions. Indeed, this inefficiency could in part have arisen from a decrease in labour mobility, linked to the US housing market. Since home prices are still below the pre-crisis peak, this could result in reluctance from jobseekers to sell their homes, which could in turn geographically limit their search. If this were true, in time the curve would be expected to shift back in line as the housing market recovers and jobs and workers get matched more quickly.

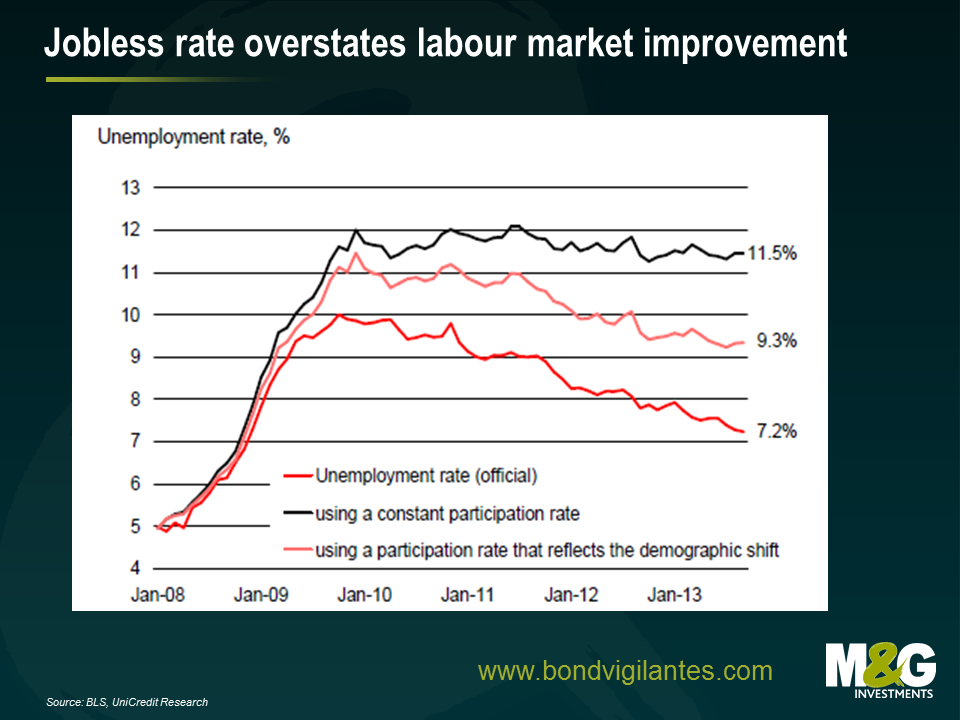

2) The labour force participation rate. Perhaps the shift has been caused by the post-crisis increase in unemployment. As the theory would have it, as the number of job seekers increases relative to the population, this would cause an outward shift of the Beveridge Curve. The US has however witnessed the exact opposite since 2009 – a fall in both the unemployment and labour force participation rates. On this point, research from Unicredit suggests that the fall in the latter is causing the unemployment rate to be understated were it not for the decline in the labour force participation rate, unemployment would stand at 11.5%. This signifies that the US may well have an underlying structural unemployment problem that is currently being ignored.

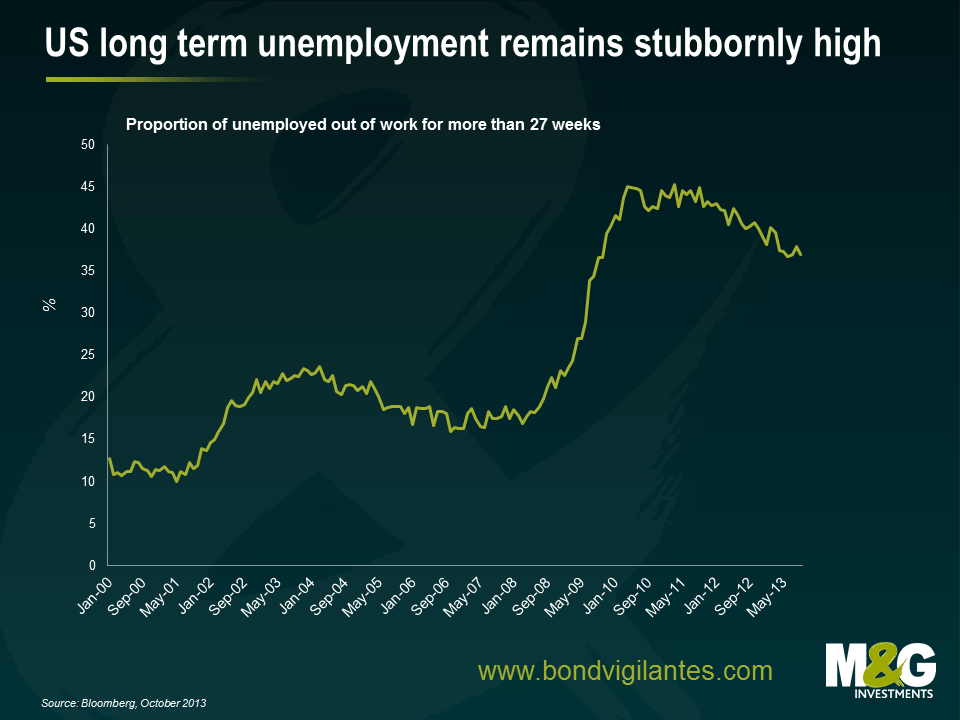

3) Long term unemployment. If caused by a fundamental mismatch between an employer’s requirements and an employee’s skill set (which deteriorates as more and more time is spent out of work), long term unemployment could cause the Beveridge Curve to shift outwards. Indeed, the proportion of unemployed workers who have been without work for 27 weeks upwards has increased since June 2009 and remains high, suggesting that a long term structural shift may have occurred in the US.

4) Increasing frictional unemployment. To cause an outward shift of the Beveridge Curve, frictional unemployment – the time period between jobs, caused by redundancies and resignations – would have to increase. Although this could have caused the initial shift, to my mind, this argument is inconsistent with longevity of the shift. If the shift were solely due to frictional unemployment, this impact should have been eroded since 2009 as labour market performance gained some ground.

5) Economic and policy uncertainty. I think it’s fair to say that the US has seen its fair share of economic uncertainty since 2009 and significant political headwinds in 2013 alone. Firstly, with regards to the sequestration earlier this year which saw fiscal contraction manifest most notably via the expiration of the temporary payroll tax and budget caps. Secondly (although more recently so this will not yet be reflected in the data), political headwinds have continued in the form of the prolonged Government shutdown. As such, these headwinds could potentially explain the lasting effect of the shift, in 2013 at least.

On the whole, the outward shift of the Beveridge Curve indicates that there has been a significant change in the US labour market. The key question however is whether or not this shift will prove to be a short term phenomenon that will erode over time as the US recovery strengthens. If we suppose that the shift is temporary and that the US will revert to norm, reading off the graph, this suggests that unemployment for August 2013 should have been in the region of 5.5%, which is well below the Fed’s trigger level to raise interest rates. On the other hand, is this too optimistic and have we instead witnessed a long term shift that is here to stay? The Beveridge Curve is one to watch.

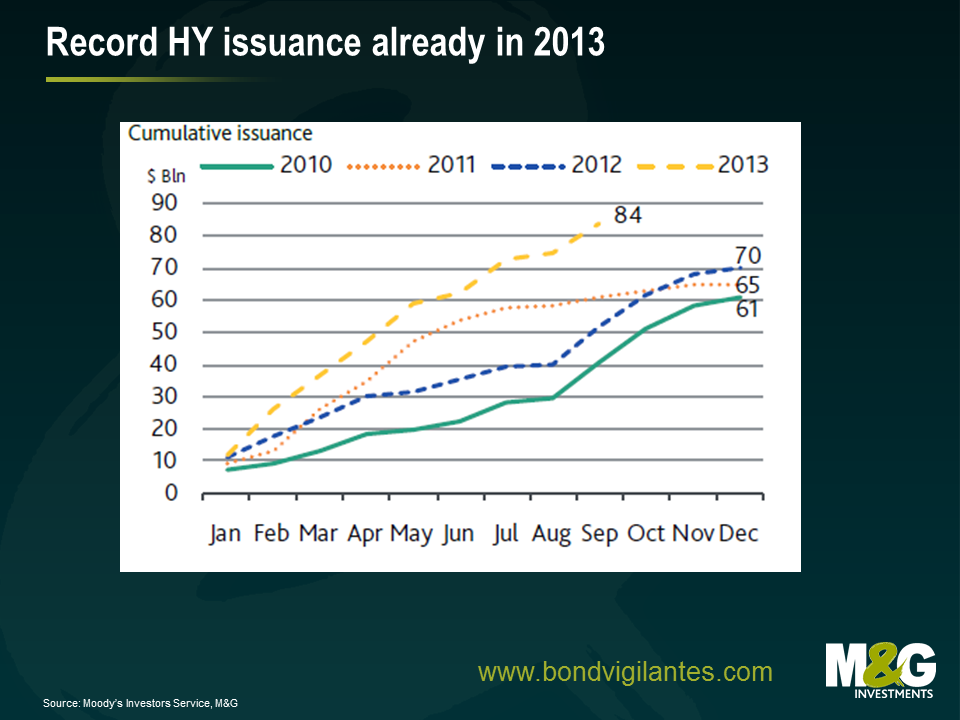

Much like fine wines, we believe that the year in which a bond is issued is an important factor in shaping its inherent character. The right climate in the markets, like the right weather conditions in the Gironde, can influence the nature of a security for better or for worse. 2013 is already a record year for the new high yield issuance in Europe (see the chart below). But will 2013 be one of the great vintages, or will investors just end up with a bad taste in their mouth and a nasty hangover?

First of all, let us consider the conditions in which the current crop of deals has been grown. By and large, it’s been fairly benign this year. With a brief hiccup in the summer, the market has enjoyed promises of excess liquidity from all the major central banks, the Eurozone has shown the first green shoots of stabilisation and default rates have remained low. Happy days then? For issuers and their investment bank advisers, yes, but for investors looking for future returns this is not the case. The perfect conditions for investors to invest capital is when the storm clouds are on the horizon, there is the sniff of panic in the air and only the juiciest of yields from the highest quality issuers can tempt people to part with their cash. In these times, the power rests with the buyers and the risk premiums extracted can be very attractive.

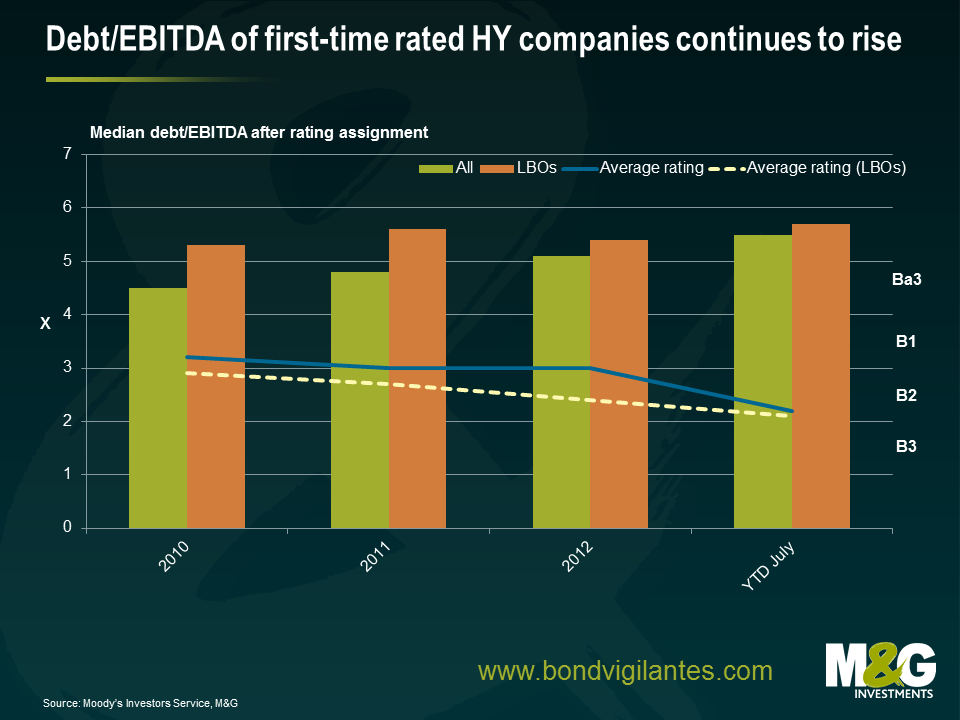

In contrast, we can see from the chart below that in today’s sunny climes a) the quality of issuance has been deteriorating (measured by credit rating and leverage) b) structural features such as weaker legal covenants*, optional coupons and subordination are becoming more common and c) given the market has been strong, the coupons and hence future returns investors can expect has greatly diminished. Valuation, as always, is at the heart of it all.

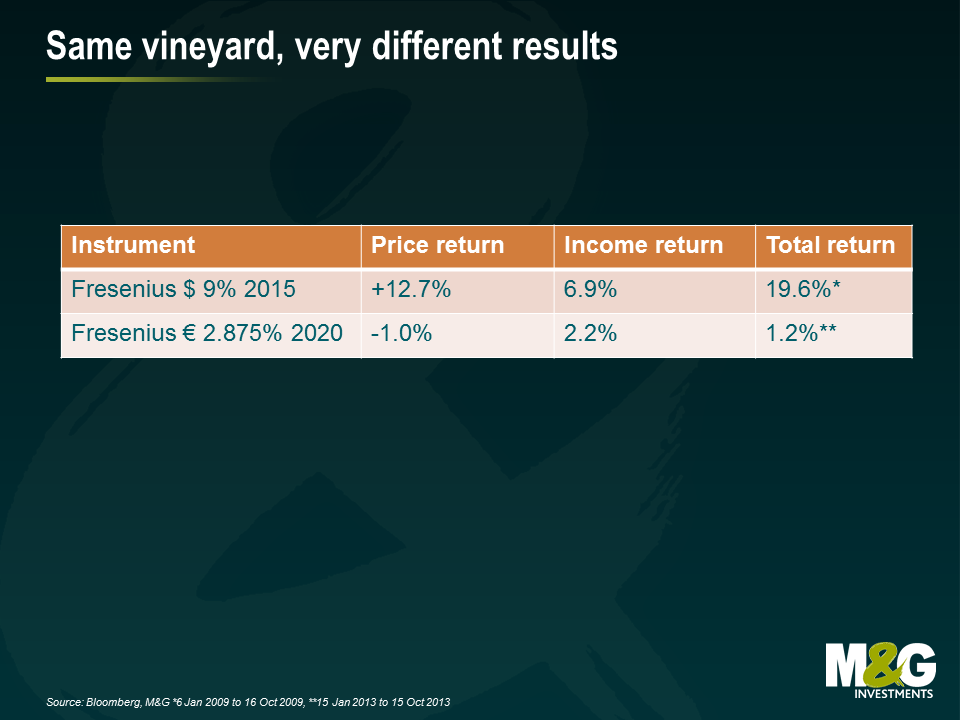

Take for instance, the respective returns experienced by two bonds issued by German healthcare provider Fresenius (one issued in 2009, the other issued in 2013). The USD 9% 2015 bond issued in the vintage year of 2009 performed admirably over the first nine months of its life. In contrast, the EUR 2.875% 2020 bond issued in January 2013 has been far less fruitful for investors. Products of the same vineyard, but with some very different results.

Of course we are not comparing like for like; 2013 is not 2009, but it illustrates the importance of market conditions and your starting point for valuations when it comes to assessing prospective returns.

There is a silver lining, however. The wave of new issuance is good for the long term development of the European high yield market. More bonds and issuers means more depth and more diversification. There is also greater scope for differentiation between different fund managers as the investment universe grows. The stock selection decision is becoming ever more important.

Nevertheless, whereas the quantity of the 2013 vintage is beyond dispute, we believe its quality is somewhat dubious. The 2013 crop is arguably more Blue Nun than grand Bordeaux.

*One new development has been the introduction of “portability”. A standard high yield covenant obliges the issuer to buy back all bonds at 101% of face value in the event the business is sold. This protects bondholders from an adverse outcome in the case of unexpected M&A. Exceptions to this are now being introduced into the legal language governing the bonds allowing issuers to be bought or sold without the obligation to redeem their bonds – allowing a so called “portable capital structure”. We do not like this dilution of bondholder rights.

As Mike just reported, we remain concerned with a number of internal issues as well as external vulnerabilities facing emerging markets. With economic growth fuelled by excessive credit growth, deteriorating current account balances and potential contagion risk if the Fed tightens monetary policy (leading to capital flows back to the US and Europe), another big sell-off can certainly not be ruled out. Combining the above with what are now fairly unattractive valuations, the overall macro EM story continues to be a none too compelling one for us.

However, what do we think of the situation at the company level? As a counter-argument to our cautious macro-economic outlook, a number of EM companies possess solid balance sheets despite their home country’s economies often being stuck in quicksand. Why not invest in solid EM-based multinationals if they have strong balance sheets, solid cash flows, sizeable global market share in their segment and an ability to diversify their revenues internationally? Let’s take a closer look.

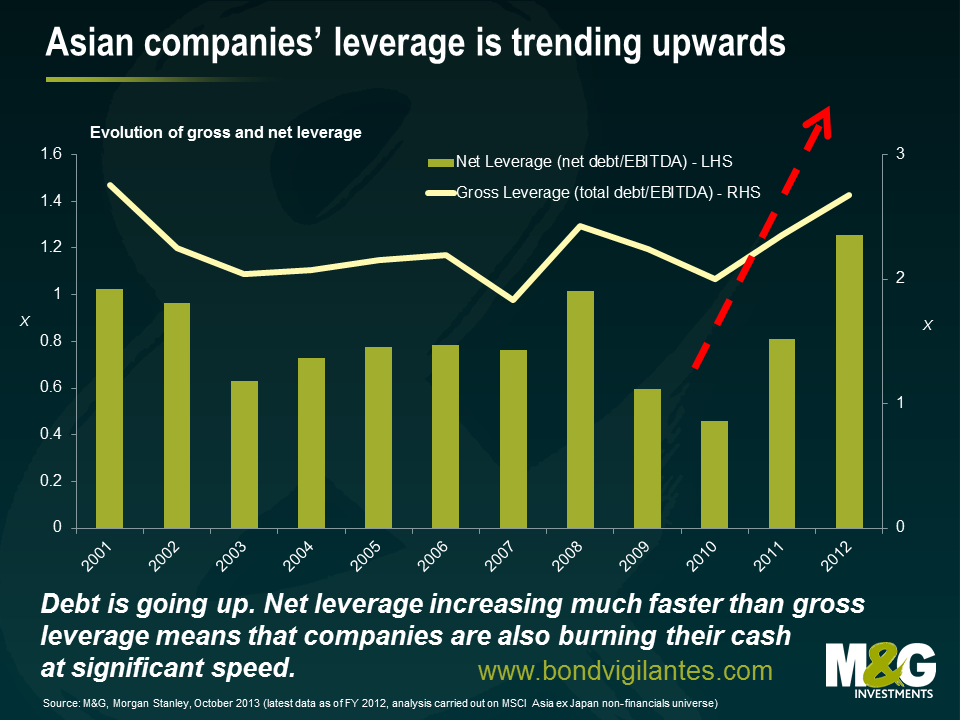

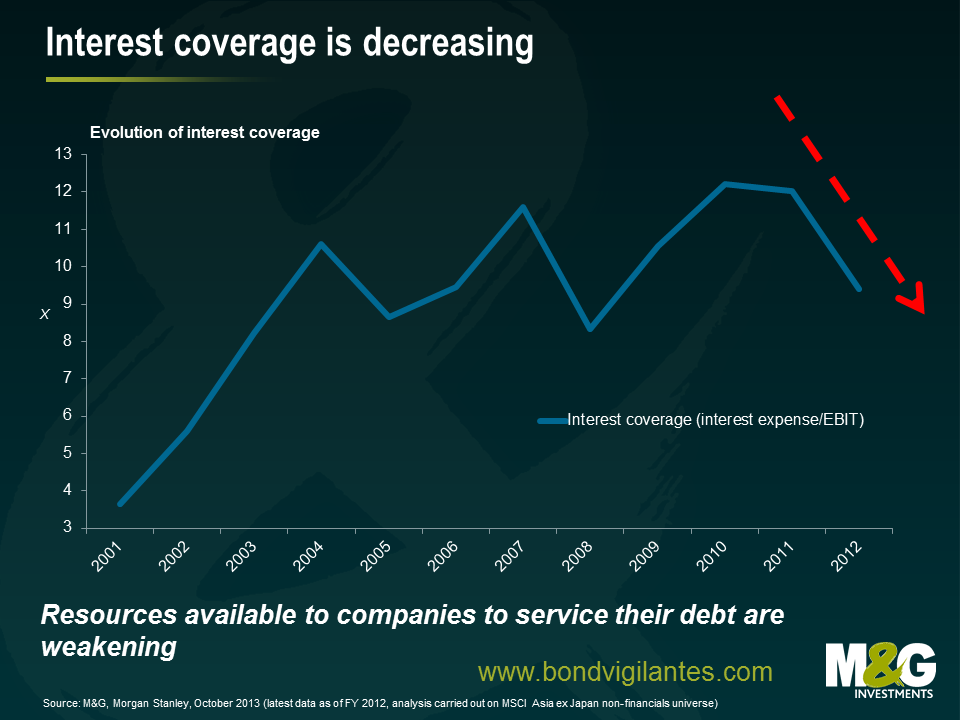

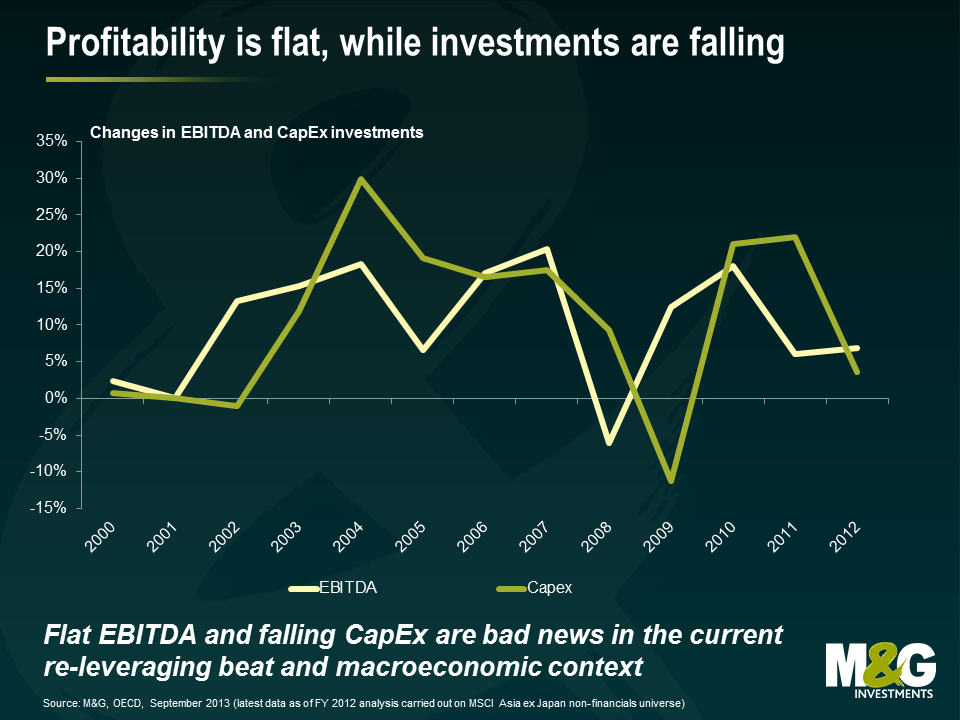

Focusing on the Asian corporate world specifically, this last “stronghold” seems to be collapsing as corporate fundamentals have sharply deteriorated. A worsening economic outlook, slower growth and tighter credit availability from the banking system will create challenges. Leverage has picked up as companies have both taken on more debt and burnt cash (a trend most evident in high yield issuers compared to investment grade). A number of Asian corporates have leveraged up in foreign currencies (mainly USD) while having revenues in local EM currencies, thus becoming increasingly vulnerable (where FX is not hedged) to a potential strengthening of the US Dollar. Operating margins (EBITDA) are flat, and capex has sharply decreased. While reduced capex may be good news for creditors in the short term (other things being equal) as more resources become available to pay back debt, it is not a great foundation to build a company’s future: how do you sustain a business over the long term if you don’t invest? On the other side of the coin, this trend of reduced capex does at least provide some evidence of emerging balance sheet discipline after years of easy credit.

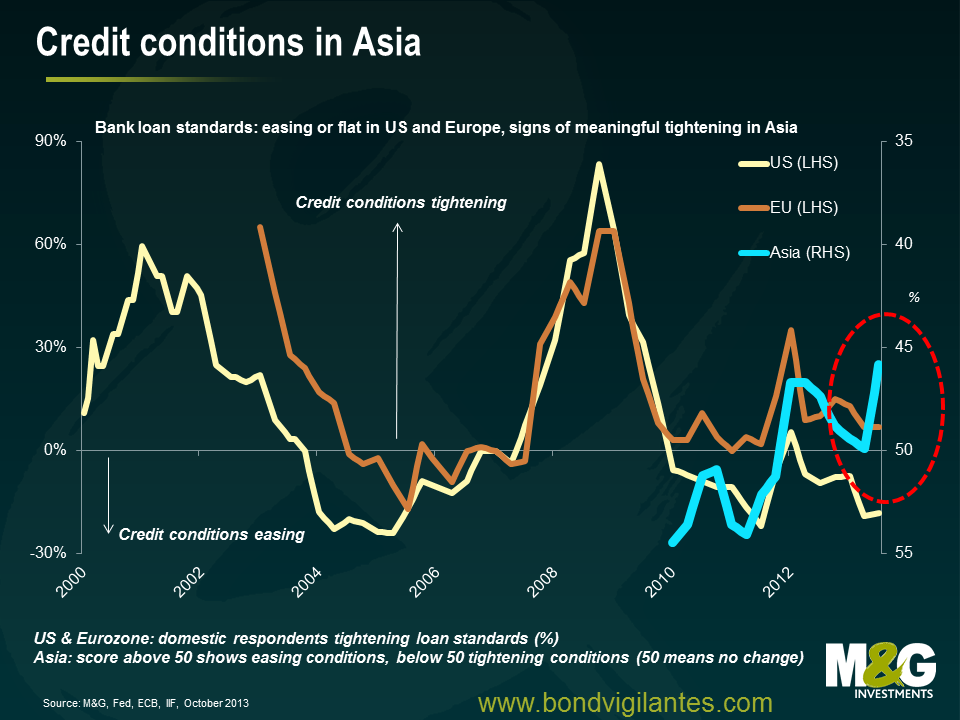

Across EM as a whole, bank loan growth has been broadly unaffected by the crisis in the summer. It was running at a pace of USD 160bn per month in July and August (according to JP Morgan data), the same rate as earlier in the year. However, looking at Asia specifically this is not the case. Despite financial conditions still being in accommodative territory (apart from India and Indonesia, no other Asian EM has hiked rates since mid-2011) a problem of over-leverage – driven by China – is pushing a number of Asian banks to close their wallets. Credit availability via official bank loans (and importantly the shadow banking system in China as well) has not been an issue so far, but corporates will have to rely on bond markets to a greater extent going forward. However, will domestic and international bond investors support deteriorating balance sheets in weakening economies? If not, we should expect to see more defaults next year, bearing in mind that Asian high yield defaults have already increased from an annual rate of 0.8% in early 2013 to 1.8% recently.

Is it only bad news then? Not entirely. Some EM companies will benefit from a stronger USD (exporters specifically) as they will gain competitiveness through being able to offer cheaper goods to the US and Europe, which are expected to grow in the coming years. Also, company specific factors including improving liquidity, stronger cash flows and stabilising balance sheets, especially in the investment grade space, may mitigate some of these concerns. And at the end of the day everything has a price in the market. We think many of the concerns we have highlighted here have been priced in to a certain degree, and while EM corporate spreads have compressed back toward US and EUR corporate spreads since the end of August, they remain well off the pre-May levels. Stock-picking and a clear differentiation between good EM and bad EM, good companies and bad companies, will be the main determinant of performance next year.

Last week saw year-on-year core inflation in the euro area fall from just over 1% in September to a two year low of 0.7% in October (see chart). Such a level is entirely inconsistent with the ECB’s definition of price stability as inflation “below but close to 2%”, and will likely be met with a downward revision to medium term inflation prospects and with it an ECB rate cut later this year.

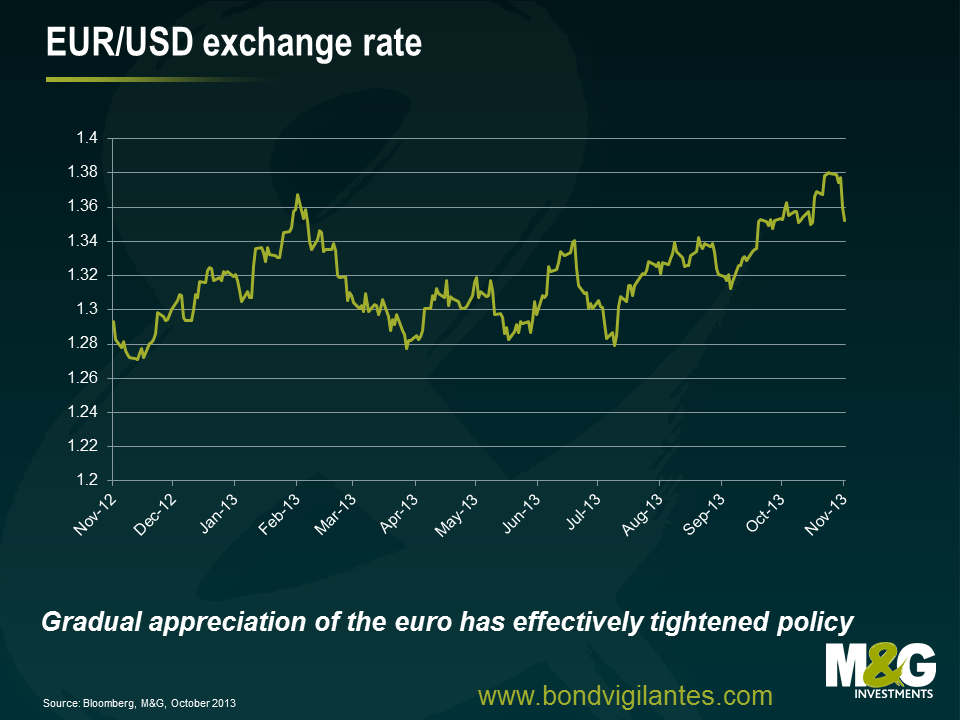

The ECB will no doubt have monitored the recent steady appreciation of the euro (see chart), which has effectively acted as a tightening of policy and will likely have a disproportionately negative effect on the periphery. Coupled with the latest inflation data, the strengthening of the euro will no doubt increase calls from the doves on the Governing Council (who should be acutely aware of the rising risks of a Japanese-style deflationary trap) to run a more stimulative policy.

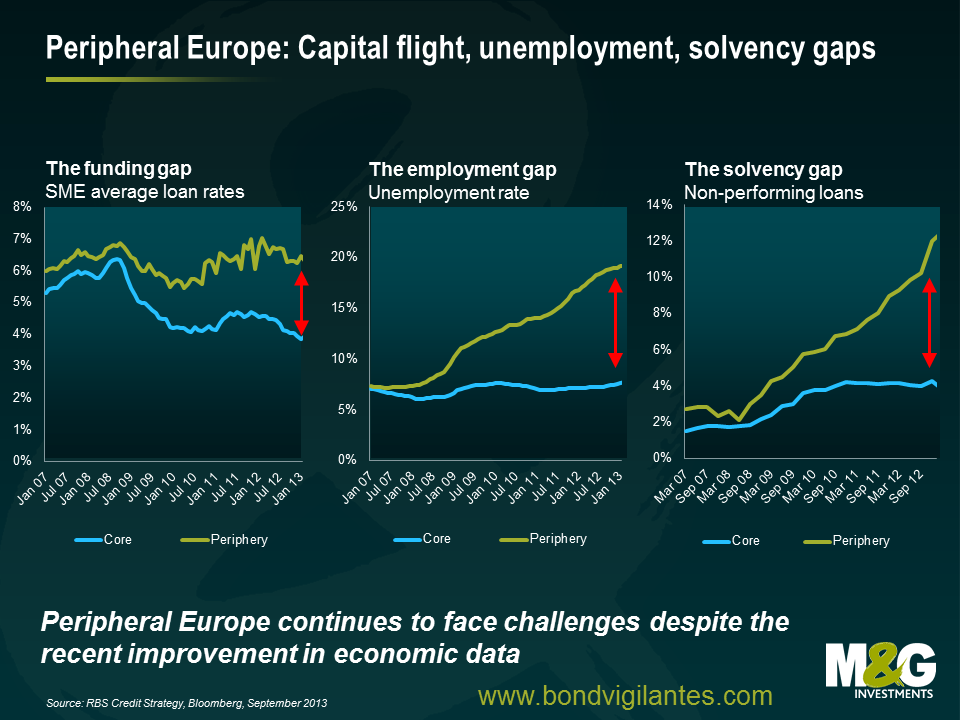

With little evidence of upward pressure on German wages, the internal devaluation required within the eurozone to facilitate a more competitive and balanced economic area has also been dealt a blow. Richard recently noted an improvement in euro area funding costs, and with it a stabilisation of broader economic data. However, this is from a very low base and the challenges that Europe continues to face should not be underestimated. Both unemployment and SME funding costs remain stubbornly high in the periphery and non-performing loans continue to move in the wrong direction (see chart). The ECB understandably wants to maintain pressure on politicians to deliver on structural reforms, and no doubt some harbour fears of leaving fewer policy tools at their disposal once they cut rates towards zero, but the risks of medium term inflation expectations becoming unanchored to the downside should be a wakeup call and a call to action!

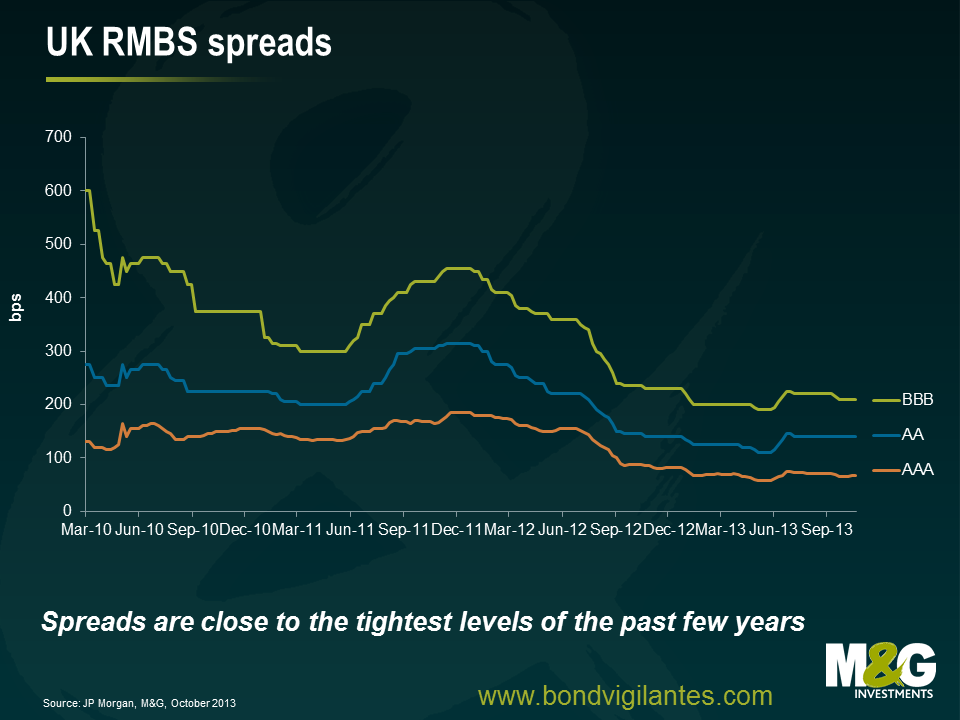

One of the features of the ABS market this year has been the lower levels of primary issuance. That, coupled with increased comfort in the asset class and higher risk/yield appetite has caused spreads to tighten.

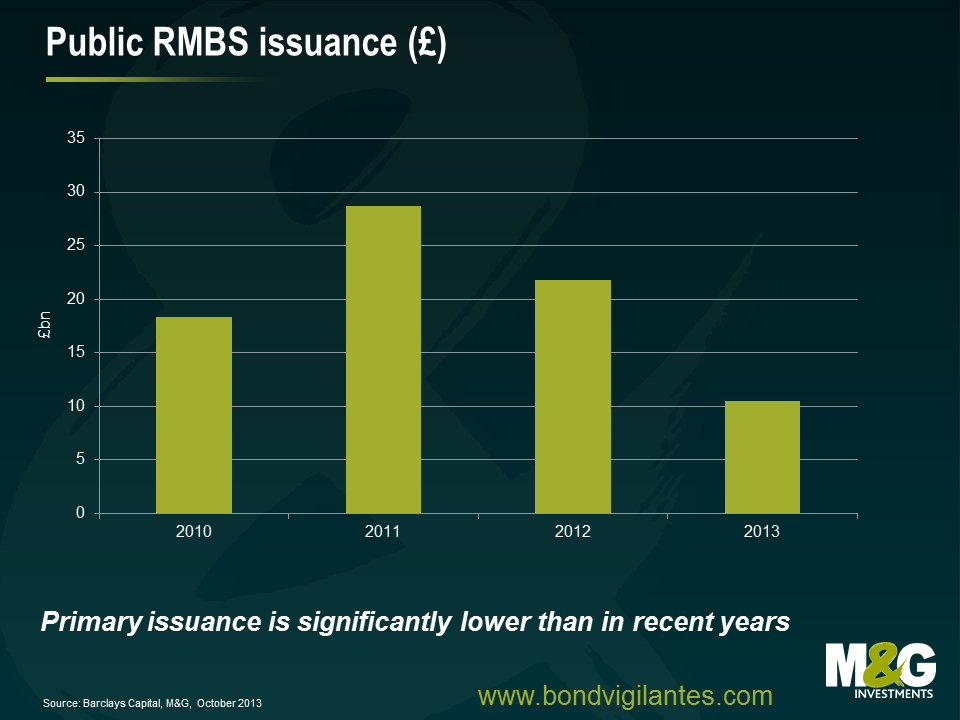

We have had a few new deals, but 10 months in and new issuance volume is only about half the amount seen in 2012, and just a third of 2011 issuance.

What we’ve seen of late, despite the subdued new issuance, is an increase in the number of these securities available in the market. In the not-so-distant past, banks would structure a securitised deal, place some with the market and keep some to pledge to their central bank as collateral for cheap cash.

Now spreads have tightened, and the market feels healthier, some of these issuers are taking the opportunity to wean themselves off the emergency central bank liquidity and are offering the previously retained securities to the public market.

Another dynamic in ABS at the moment is that ratings agency Standard and Poor’s is considering changing its rating methodology for structured securities in the periphery. S&P is considering tightening the six notch universal ratings cap – countries rated AA or above will not be affected, but bonds issued from countries with a rating below AA could be downgraded as they won’t be allowed to be rated as many notches above their sovereign as they were before.

The implication is that securities that get downgraded will become less attractive for banks to pledge as collateral because of the haircuts central banks apply to more risky (lower rated) securities. Our thinking is that southern European issuers will be hit hardest by this change. So unless the ECB loosens its collateral criteria (which it can and has done previously), one would expect to see more of those previously retained deals coming to the market as well.

So whilst we haven’t seen too much in the way of new issuance, it looks like we could be about to see an increasing number of opportunities in the secondary market.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.