World Cup currency trading strategies: emerging vs. developed markets

With just under two months to go to the opening match and tensions already mounting within our team (we have 8 different participating countries covered – Australia, Brazil, England, France, Germany, Italy, Spain and USA), we thought it was time for a World Cup themed blog. Our prior predictor of the 2010 World Cup winner proved to be perfectly off the mark. Based on expected growth rates in 2010, we predicted that Ghana would win and Spain would come last – and we know what happened subsequently. However, in defence of the IMF, Ghana were the surprise package of 2010, only failing to reach the semis thanks to a Luis Suarez handball.

However, despite the tradition of ‘lies, damned lies, and statistics’, I still believe in analysing data and making predictions. Was it coincidence that the team that was not part of our predictions (North Korea), given the lack of available economic data, ranked last? Would Argentina have made it to the quarter-finals had it not been altering its inflation statistics?

Historically, the World Cup has been won 9 times by an emerging country and 10 times by a developed country. Will an emerging country win and tie the score this year?

We present two currency trading strategies associated with the World Cup:

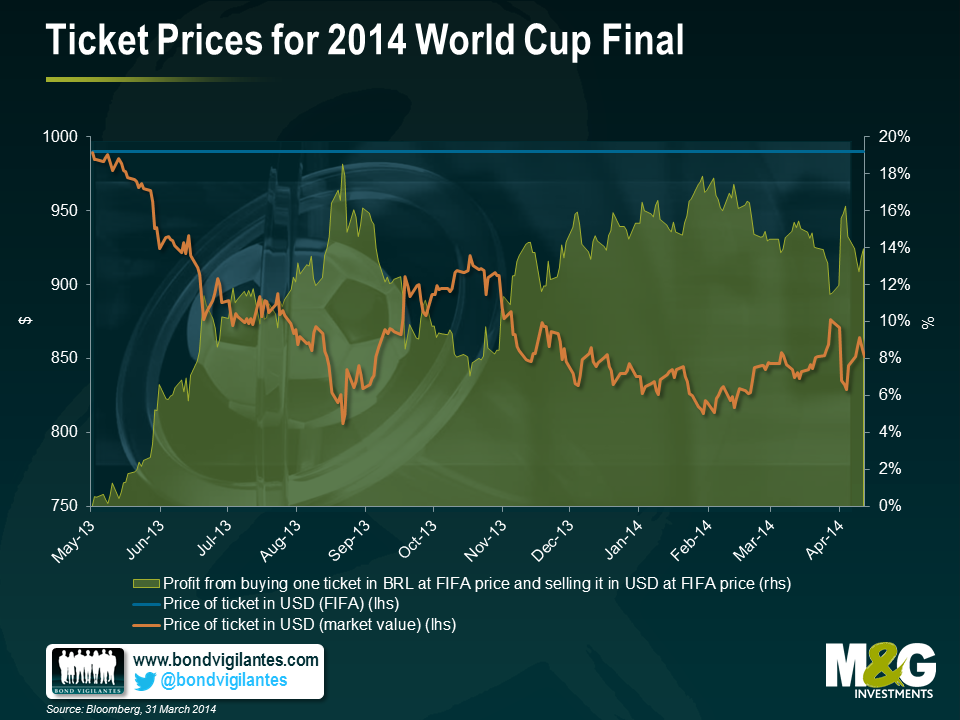

- Arbitrage: in currencies with full convertibility or minimal transaction costs, arbitrage opportunities are very limited. However, currencies that are subject to restrictions on capital flows, taxation or regulatory requirements often offer arbitrage opportunities in excess of the costs associated with these factors. For example, for the World Cup in Brazil, ticket prices for non-residents are determined in USD and in BRL for Brazilian residents. Ticket prices were set by FIFA in May 2013 (1980 Brazilian Reals or 990 US Dollars for category 1 tickets), based on the prevailing US Dollar / Brazilian Real exchange rate of 2.00. As ticket prices remain unchanged in USD and BRL and given the depreciation of the Real since then, ticket prices in BRL are now 14% cheaper than tickets purchased in USD.

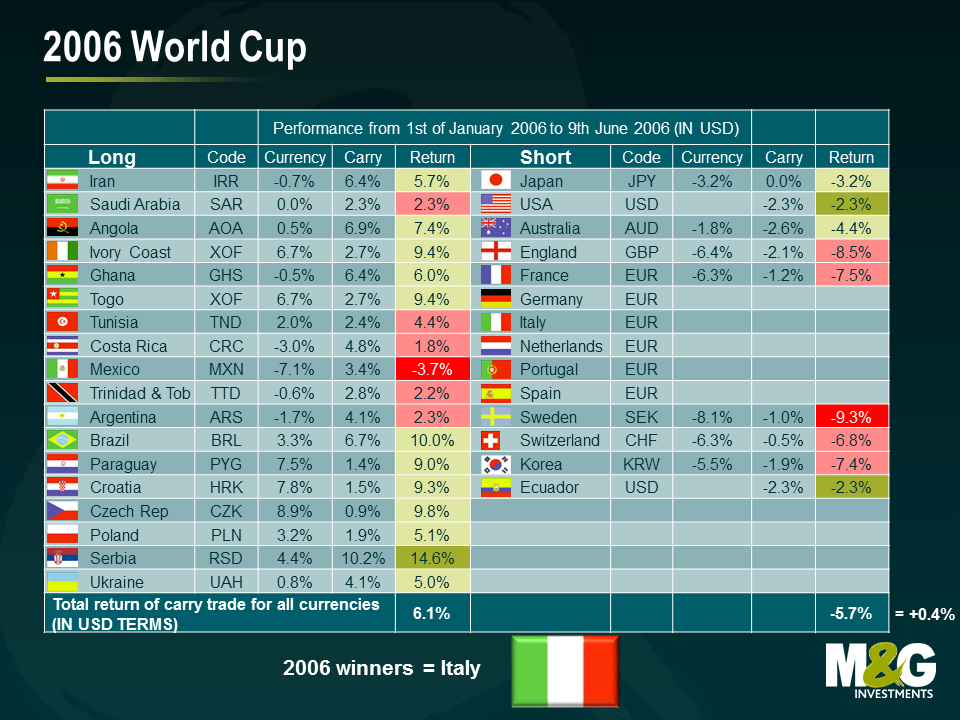

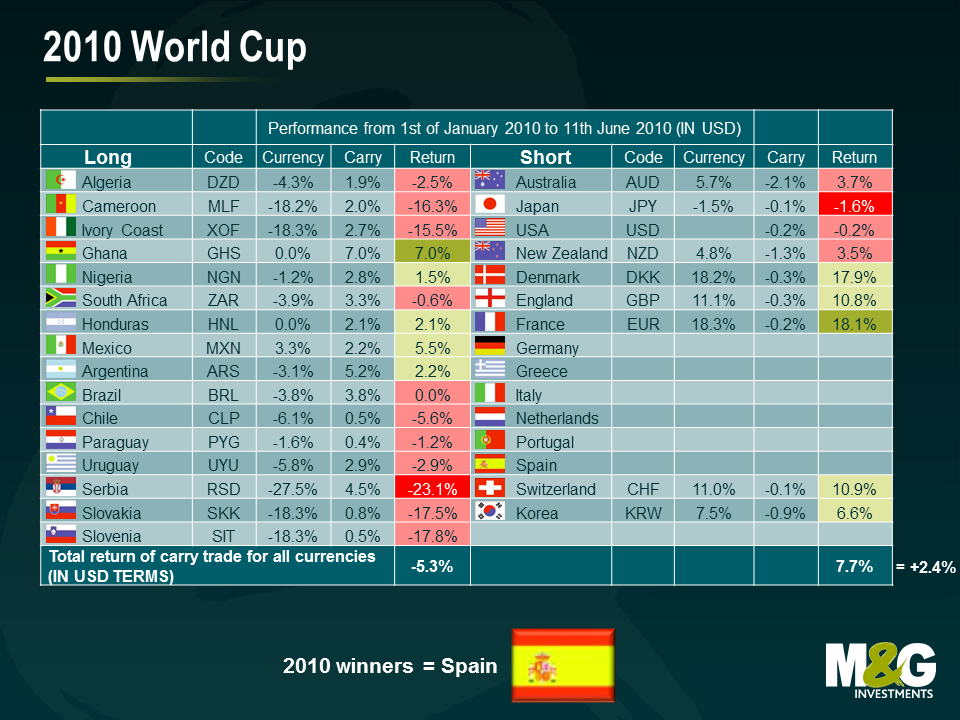

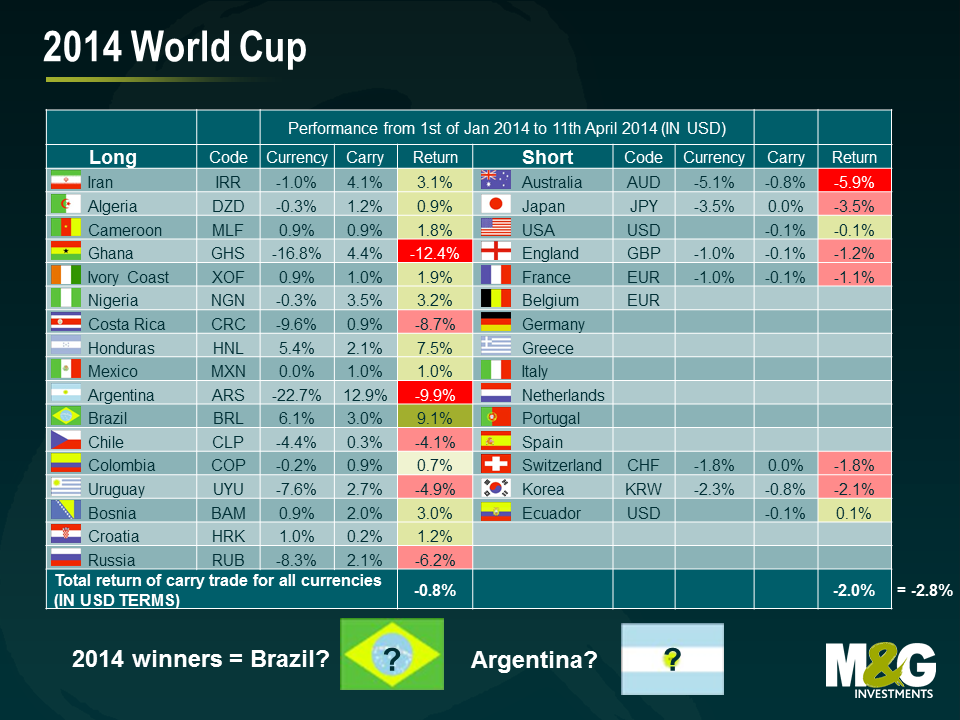

- Currency carry trades: a popular strategy which is relatively easy to implement and which has proven profitable1. We test the strategy by going long a basket of emerging market currencies of the qualifying countries (which are normally higher yielding due to higher inflation, economic risks, etc.) funded by a basket of developed market currencies of the qualifying countries (which are normally lower yielding, which has been exacerbated by quantitative easing). Out of the countries that qualified for the recent World Cups, we arbitrarily classify them as 18 emerging and 14 developed. However, if we measure them by currency, the numbers change slightly. A few emerging countries have a developed market currency as legal tender (for example, Ecuador adopted the US Dollar as its legal tender in 2000), so it makes sense to count them as developed countries. We keep Ivory Coast under the emerging basket, as the West CFA Franc, while pegged to the Euro, is not the same as having Euro as its legal tender.

We test our World Cup carry trade performance during the last 2 World Cups between January 1 (a clean start date once the 32 qualifying teams became known) and the start dates for each tournament.

The EM vs DM FX carry trade posted a small profit in 2006 (+0.4%) and was a clear winner in 2010 (+2.4%)2 . On the football field, however, emerging market lost to developed market in both instances (Italy and Spain won). Ahead of the upcoming cup, the carry total return points to a loss on the EM carry trade so far (-2.8% to the 11th of April). On this basis, I predict that an EM team will win the cup in Brazil.

1For an empirical discussion of emerging market carry trades, see http://www.nber.org/papers/w12916.pdf?new_window=1.

2For simplicity reasons, we have omitted bid-offer transaction costs from the calculations. Given that some of the smaller EM currencies are less liquid and have higher costs (in this case, one buy and subsequent sell), the results slightly overstate the returns of the EM long side. On the short side, we only included the Euro once, to maintain a “diversified” basket of developed currencies.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

17 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox