Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

Interest rates – both short and long term – are at record lows in Europe. The driving force behind this is the belief that both employment and inflation will be lower for longer. This is something that concerns the ECB and Drahgi’s Jackson Hole speech implies further easing ahead. These appear to be exceptional times.

The story of how we got here is pretty simple: a global banking collapse in 2008, followed by a further severe bout of local damage to the banking system in Europe caused by the sovereign debt crisis in 2011 and 2012.

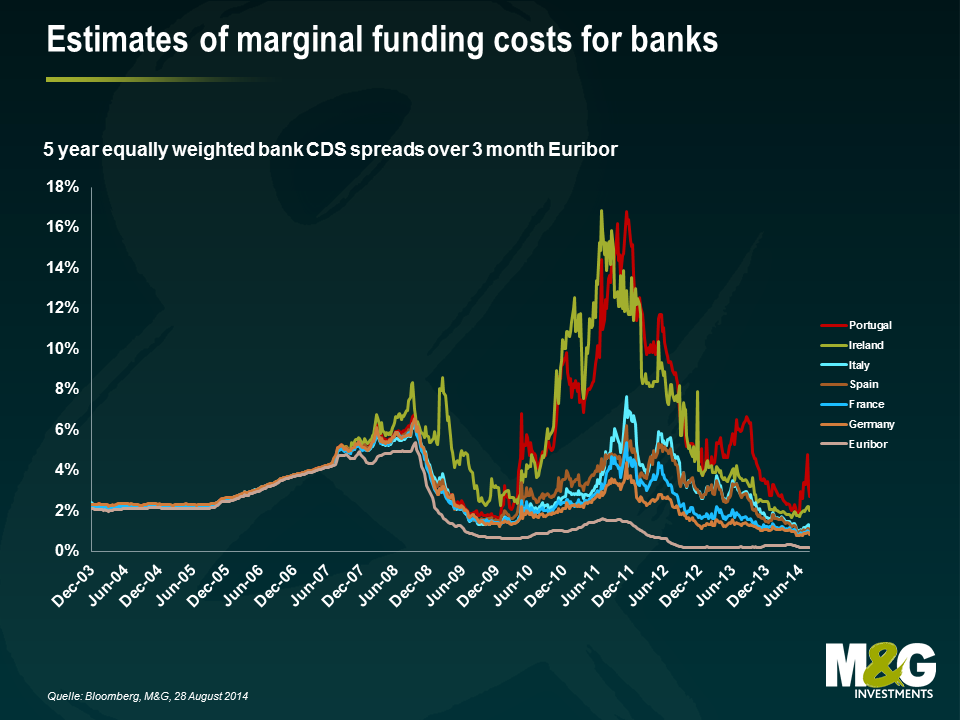

The chart below is an attempt to illustrate where true borrowing rates have been. Taking a proxy for the cost of finance and adding that to three month Euribor gives a better picture of real monetary conditions than by simply looking at the headline ECB rate. Monetary policy in the Euro crisis was tightened in the core, but more so in the periphery.

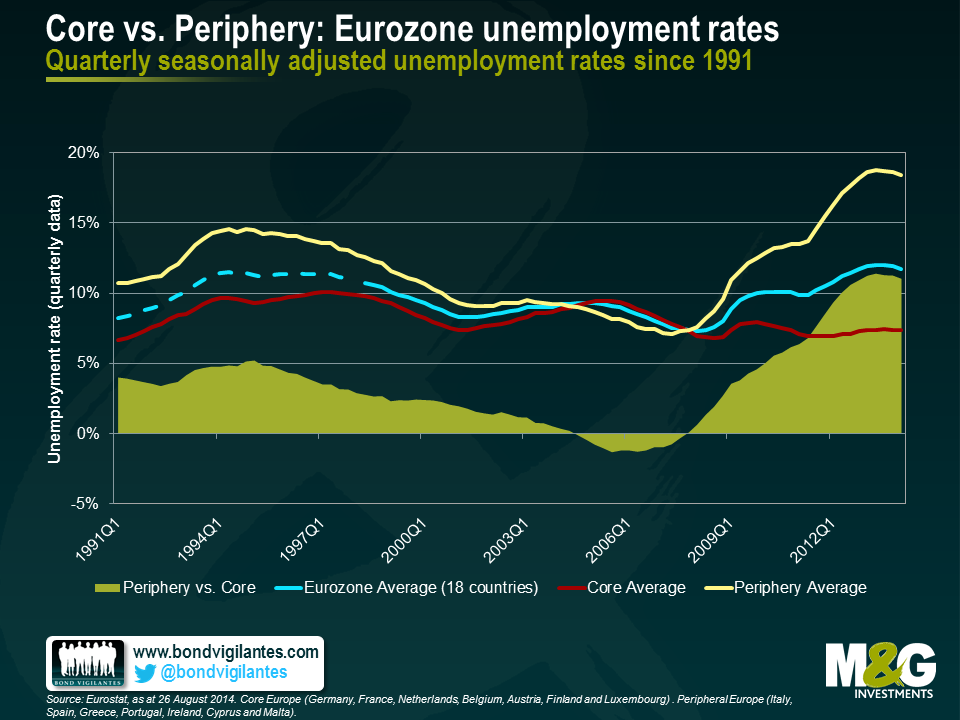

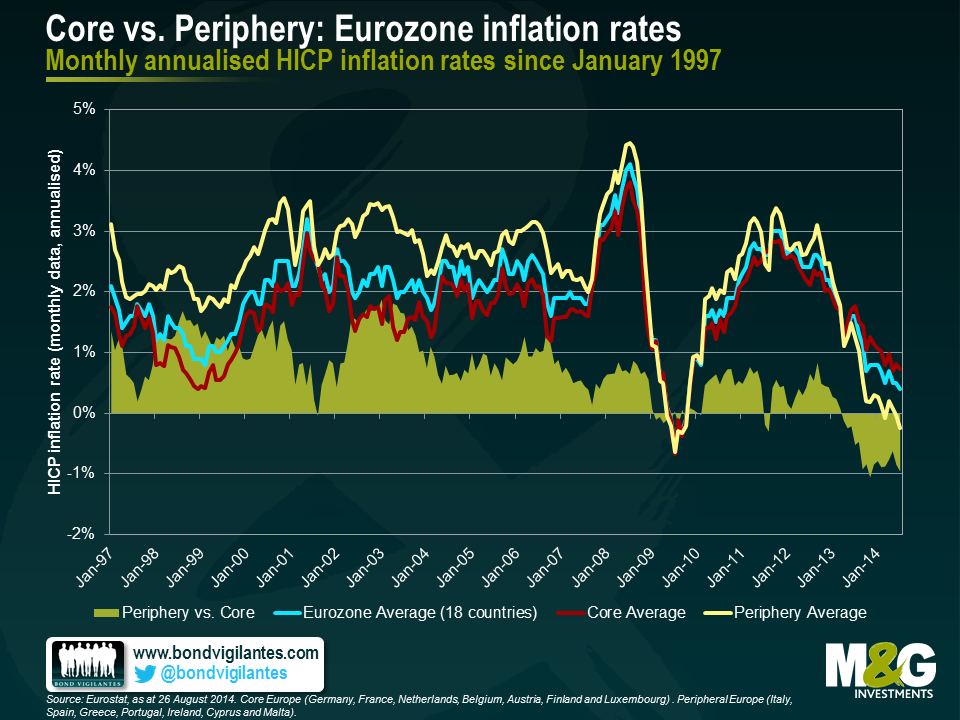

In the following charts we break out the inflation and employment data of the core and the periphery. What we see is that where tighter monetary policy is applied unemployment is subsequently higher and inflation is lower. It is not surprising that the Euro area and particularly the periphery have been weak given the severe monetary shock they took in the Euro crisis. This suggests that monetary policy still works.

Going forward, real monetary policy has effectively been eased aggressively from the summer of 2012 through to now. This should provide a boost to the Euro area, and in particular the periphery. Monetary policy is generally assumed to work with an 18 month lag and interestingly unemployment is already heading down. I expect this trend will continue.

We are in exceptional times from an interest rate perspective, but from an economic perspective unemployment has been this high before from 1994 to 1997, and inflation was below 1.0% in 1999 and 2009.

When economics deviates from markets you have to decide which is correct. I think that monetary policy works, and the huge easing from 2012 will bring about falling unemployment and prevent significant deflation. Exceptionally low interest rates in Europe seem out of line with the current and potential future economic data.

In principle, the European Central Bank (ECB) is well in line with its price stability objective, which it defines as a “year-on-year increase in the Harmonised Index of Consumer Prices (HICP) for the euro area of below 2%”. Nonetheless, July inflation numbers released last week bring the currency union as a whole dangerously close to deflationary territory. The aggregate HICP annual rate of change for the Eurozone fell to 0.4%, its lowest inflation print since October 2009.

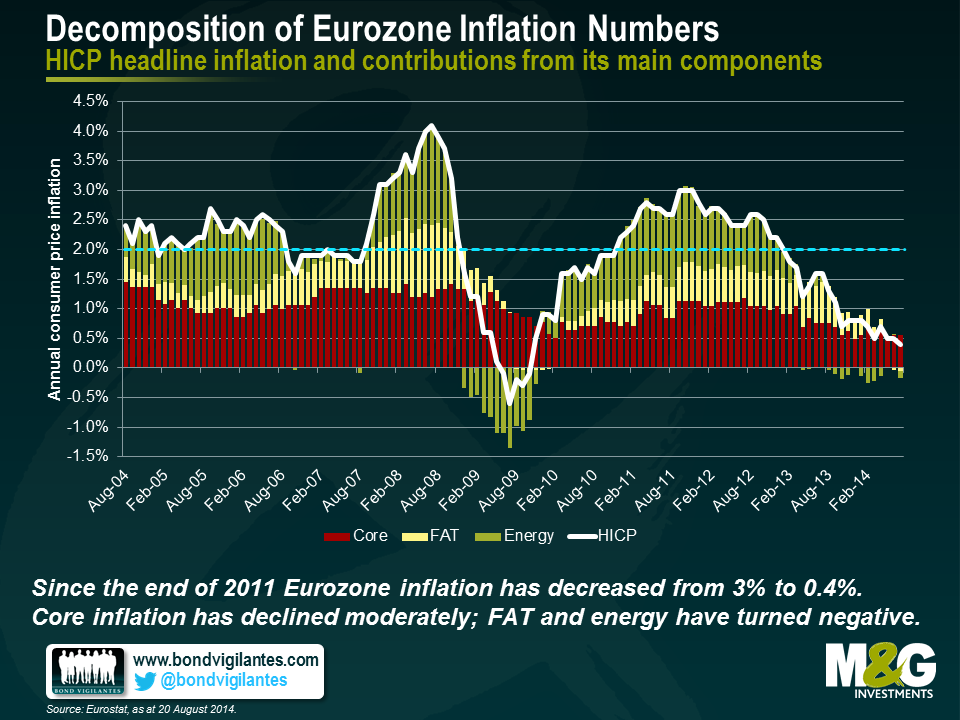

But what has been driving this development? To answer this question we broke down HICP headline inflation numbers into three components: (i) food, alcohol and tobacco (FAT); (ii) energy; and (iii) core inflation, i.e., the remainder when stripping out (i) and (ii) from the headline figure. In the chart below we plotted the contributions of each of these three components to the headline number, calculated by multiplying the annualised monthly changes of the component indices by their respective weights within the overall HICP.

Only a relatively small part of the substantial drop in HICP headline inflation from 3.0% in the end of 2011 to currently 0.4% can be attributed to core inflation. Admittedly, core inflation contribution has fallen from 1.1% to 0.6% in this time period but compared to the other two components it has been much more stable. This result intuitively makes sense as core inflation comprises very different items, such as clothing, healthcare and communications. The inherent diversification subdues core rate volatility as fluctuations in individual item levels are likely to balance out each other to a certain degree. The fall in Eurozone inflation has mainly been caused by FAT and energy. Whereas FAT and energy boosted headline inflation by 0.7% and 1.3%, respectively, in November 2011, by now both components have essentially become a drag, chipping off 0.1% each from the July 2014 aggregate figure. Declining inflation rates in the Eurozone can at least partially be explained by a strengthening of the Euro vs. USD (c. USD 1.27 per EUR in the beginning of 2012 to a peak level of c. USD 1.39 in early May 2014), having a deflationary effect on import prices. In recent months, when the exchange rate trend started to reverse, the oil price dropped sharply (c. USD 114 per barrel Brent in mid June 2014 to currently c. USD 102), which helped to put downward pressure on energy prices. It will be interesting to see how geopolitical developments in the Ukraine and the Middle East are going to affect energy inflation contributions in the months to come.

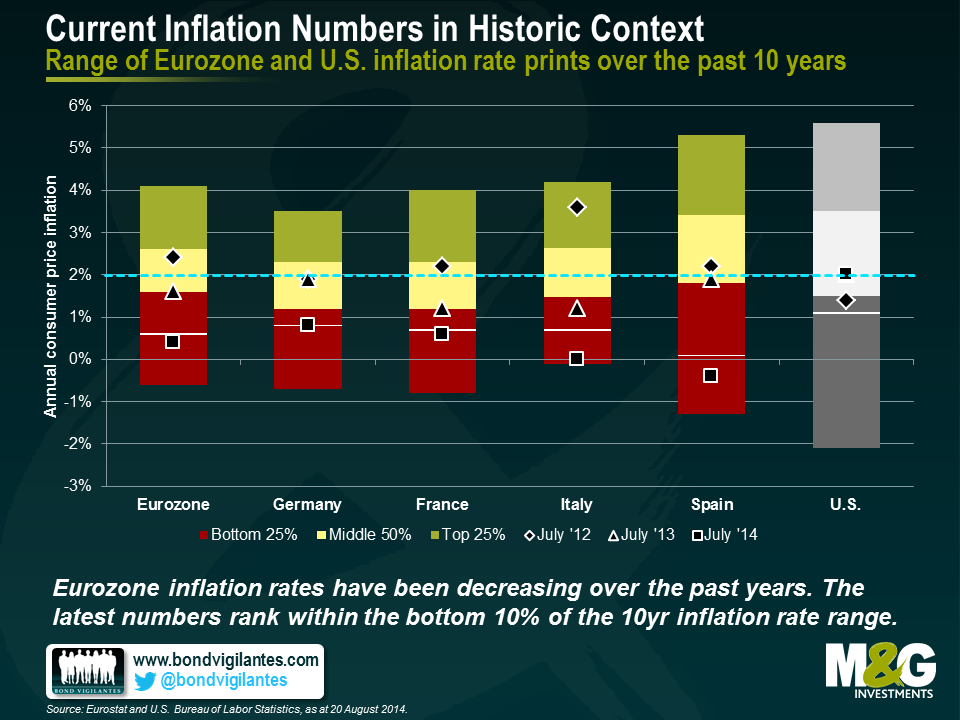

Now let’s turn towards inflation rates of individual countries. The two biggest Eurozone economies, Germany and France, showed July inflation rates clearly below 1% (0.8% and 0.6%, respectively). The periphery experienced either no inflation at all (Italy with 0%) or even deflation (Spain with -0.4%, Portugal with -0.7%, Greece with -0.8%). Undoubtedly, these numbers are low. But how do they compare with historical inflation rates? We took a look at the past ten years of inflation rate data (HICP annual rates of change, published monthly) for the Eurozone in total, its four main economies and, for comparison, the United States. For each entity, we ranked the numbers from smallest to largest and divided the range of inflation rates into three bands, containing the bottom 25%, middle 50% and top 25% of data points, respectively (see chart below). The white lines mark the border below which the bottom 10% of inflation rate prints are located for each data series. In addition, we highlighted the most recent inflation numbers as well as the figures from one and two years ago.

We can draw a number of conclusions from this chart. For instance, inflation rate spans for Germany with 4.2% (-0.7% to 3.5%) and Italy with 4.3% (-0.1% to 4.2%) are significantly smaller than for Spain with 6.6% (-1.3% to 5.3%) and the U.S. with 7.7% (-2.1% to 5.6%). Most importantly, the chart puts the drop in European inflation rates over the past years into some statistical context. July 2012 inflation prints still rank within the middle 50%, or even in the top 25% in the case of Italy. Except for Germany, inflation rates exceeded the ECB’s upper limit of 2% back then. However, the most recent data points from July 2014 can all be found in the bottom 10% of the 10-year inflation rate ranges. German inflation is exactly at and the French figure slightly below their respective bottom 10% thresholds. Italy’s and Spain’s inflation rates have fallen deep into their bottom 10% ranges. Italy’s current 0% inflation figure marks in fact the country’s second lowest monthly reading within the past 10 years. In contrast, U.S. consumer price inflation is not on a downward trajectory but numbers have been bouncing back and forth between 1% and slightly above 2.0% over the past two years. The July 2012 print of 1.4%, for example, ranks in the bottom 25%, whereas inflation rates both for July 2013 and July 2014 sit with 2% within the middle 50%.

What does this mean for fixed income investors? For a start, the divergence of European and U.S. inflation rates, in combination with substantial differences in real GDP growth (Eurozone with -0.4% in 2013 and 0% in Q2 2014 vs. U.S. with 2.2% and 4.0%, respectively) and labour market strength (Eurozone with 11.9% unemployment rate in 2013 and 11.6% in Q2 2014 vs. U.S. with 7.4% and 6.2%, respectively), reinforces the argument of an on-going decoupling between the two economic areas. The progressive fall of Eurozone inflation rates well below the 2% level gives the ECB some room for manoeuvre. European interest rates are likely to stay at essentially zero for the time being, and we should not be surprised if more accommodative monetary policies, such as asset purchases, were implemented by the ECB going forward in an attempt to stimulate economic recovery.

On the right is UK Chancellor George Osborne, the austerity axeman. On the left was opposition leader Ed Miliband, the fiscal freedom fighter. But it now appears that Miliband and co are so alarmed that Cameron and Osborne are better trusted by the electorate to run the now booming UK economy that they are quietly embracing Tory austerity. The Liberal Democrats have accused the Tories of pursuing austerity for austerity’s sake, but are still targeting eliminating the budget deficit in the next three to four years. That essentially leaves the Scottish National Party, which is urging Scots to vote for independence so that Scotland can ”escape Westminster’s austerity agenda”.

The problem with all this austerity posturing is that it’s built on a completely phoney premise. As confirmed by data released today, there hasn’t been any UK austerity, at least not for a couple of years. Indeed, that probably goes a long way to explaining why the IMF predicts that the UK will have the fastest growing economy in the developed world this year.

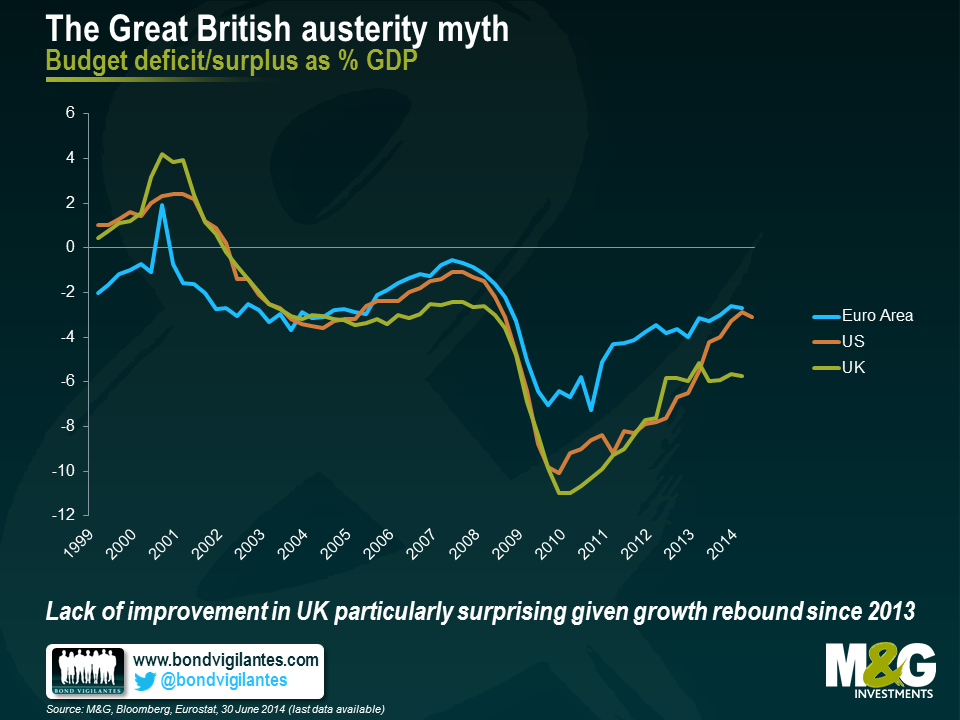

The chart below puts the UK’s budget balance into international context. The US has seen immense fiscal consolidation, which was a major drag on growth in 2011-2013 but which will substantially fall hereafter, and is one of a number of reasons why we’re US economy bulls. Eurozone fiscal consolidation was enforced by markets to an extent, although the Eurozone as a whole – as per the US – is currently running a budget deficit akin to levels seen in 2004-05. And Germany, a country under zero pressure from markets, expects to balance its budget this year. The UK economy grew almost three times faster than Germany’s in the year to Q2, and yet its deficit remains huge by historical standards.

The primary reason for the UK’s unfrugal fiscal policy is an inability to cut back on government spending. It’s not just overspending, however. Tax revenues in the first four months of this tax year are 1.9% below where they were in July 2013, and that’s in nominal terms, let alone real terms. The Office for Budget Responsibility (OBR) will be able to provide more detail on this when they release their summary later today. It’s likely that part of this is due to the front loading of receipts last year, thus making like for like comparisons tricky, and the OBR will probably forecast a pick up in receipts towards the end of this year.

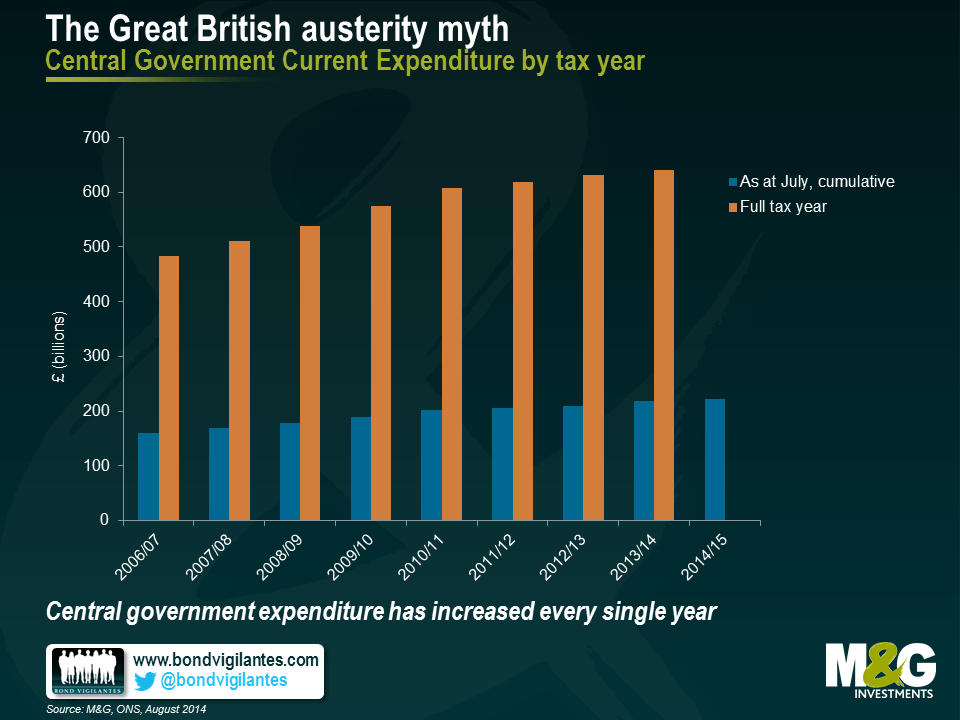

The chart below illustrates how government spending in the UK has increased every single year.

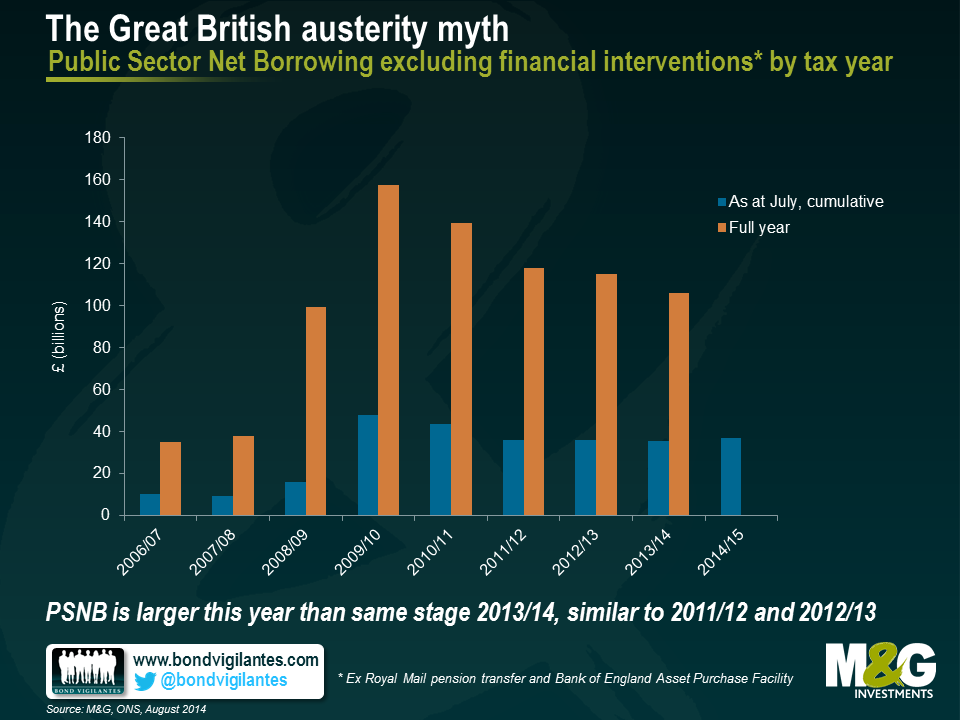

An addiction to spending combined with weak tax revenue growth means that the Public Sector Net Borrowing figures are going nowhere fast. In the four months to July, Public Sector Net Borrowing (ex financial interventions) was actually higher than in 2021/12, 2012/13 and 2013/14. Again, the OBR will have more to say about this later, but there’s no denying that the UK’s government finances make grim reading.

Now all that said, I’m not suggesting that the UK government should necessarily adopt tighter fiscal policy. While current fiscal policies aren’t sustainable in the long term, loose fiscal policy has recently been successful in generating strong economic growth, and more importantly it appears to have helped encourage the private sector to finally start investing. Furthermore, you would traditionally expect countries that run sustained loose fiscal policy to have relatively steep yield curves, but the opposite is true in the UK at the moment, with some longer forward yields close to record lows. In other words, the markets don’t care – yet – and a good argument can be made for the government to fund some much-needed and ultimately productive UK infrastructure investment. All I’m saying is that the UK electorate deserves a lot more honesty in the debate.

France has a unique social model. It originates from the end of the Second World War, when the National Council of the Resistance (NCR) hastily put together a plan to rebuild the country after five years of Nazi occupation. Despite not having any official political affiliations, the NCR was in fact influenced by left wing individuals and the “National Front”, a communist party. The NCR’s “action plan” helped shape France in the aftermath of the war and is one of the reasons today that trade unions have such a prominent position in society and why the French are so fond of their “established social rights”.

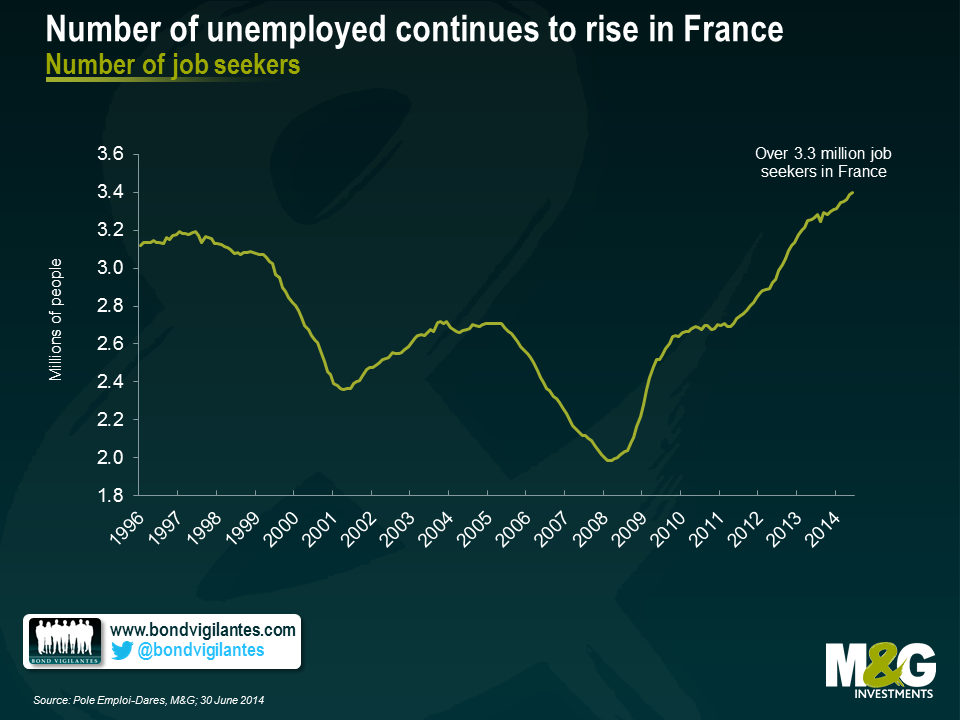

Since then, reforming France has always been a difficult task. Given that it was announced last week that the country has experienced a second consecutive quarter of no growth, it seems obvious that some sort of change is urgently required. France has grown by only 0.1% in the past year. Despite extremely low interest rates and fiscal tightening, the government’s budget remains in structural deficit and the debt to GDP ratio has increased from 77% to 93%. More worryingly, despite French President Hollande’s very vocal claim that he would “invert the unemployment curve” by the end of 2013, the number of job seekers continues to rise at an alarming rate, hampering consumer confidence and business spending.

So what can the Hollande government do in a country that is difficult to reform and where scope for public spending is limited?

First of all he should aim to simplify France’s highly complex tax regime, which over the years has become almost illegible. This toing-and-froing over taxes continues to hurt the French economy by creating uncertainty and hampering business investment. In the last 2 years alone, French legislators have created 84 new taxes, for a total of €60 billion Euros.

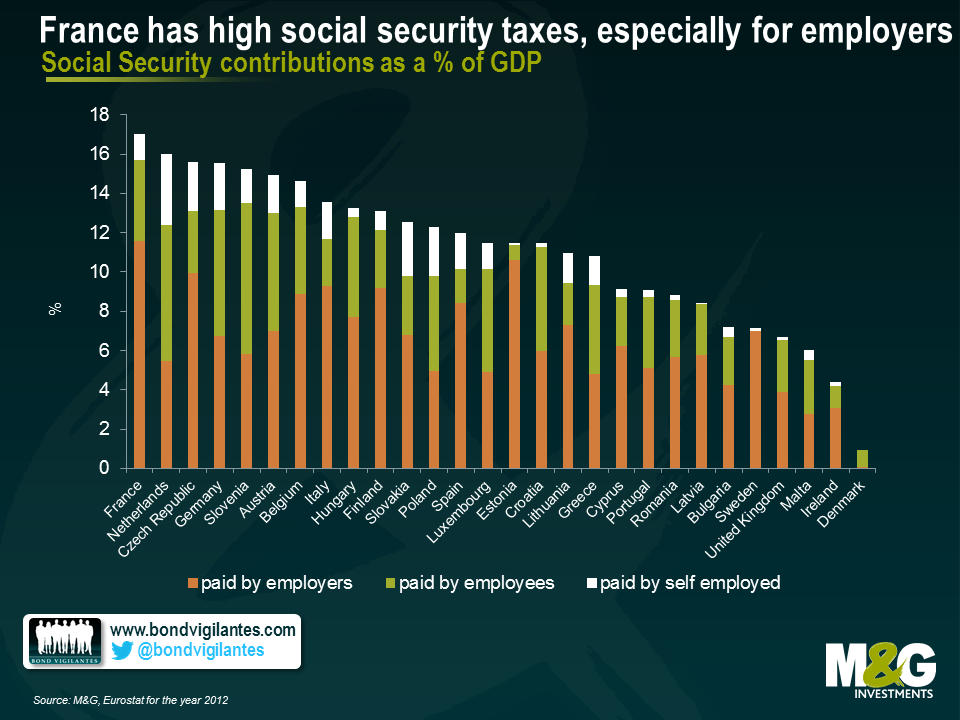

Second, the government must reduce the burden of social security contributions on the business sector. Today, France spends 17% of its GDP in social contribution taxes, the highest amount out of all of the 28 EU countries. While many people in the country believe that this is the price to pay to finance France’s generous welfare system, its financing relies too heavily on businesses. In the rest of Europe the burden of social security payments is shared on average equally between employers and employees. In France, almost 70% of these payments are paid by employers. This has a direct effect on the cost of labour and diminishes companies’ abilities to compete in an increasingly globalised world. The French government has started to address this issue by granting a €20 billion tax credit (CICE) to all French businesses, but much more needs to be accomplished. Indeed, in order to put France on equal footing with its neighbour Germany, employer social security contributions would need to be reduced by a further €80 billion per year.

Finally, the government should also tackle the excessive bureaucracy in the labour market. For example, many small firms today refuse to grow beyond the threshold of 50 employees because exceeding this number triggers a raft of regulatory and legal obligations. It would make sense to push this threshold to 250 employees, and bring France in line with the European norm. The French Labour Code is 3500 pages long and weighs 1.5 kilo, while the Swiss Code, where unemployment is 3% rate, is 130 pages and weighs 150 grams (anecdotally comparing unemployment rates with the number of pages of labour codes for different countries could be the subject of a future blog). This excessive bureaucracy is partially the reason why France’s competitiveness has been declining in recent years. In its latest Global Competitiveness report, the World Economic Forum ranked France 23rd overall, but 21st in 2013 and 18th in 2012. More alarmingly, the country is ranked 116th for “labour market efficiency” (out of a total of 148 countries), 135th for “cooperation in Labour-employer relations” and 144th in “hiring and firing practices”. When asked what the most problematic factor for doing business in the country, the number 1 answer provided by respondents was “restrictive labour regulations”.

As France teeters on the brink of recession, Hollande is today in a very difficult position. A complete overhaul of the French social model would create much civil unrest and probably push the country into recession. On the other hand, doing nothing is likely to have the same effect as France would continue to lose competitiveness on a global scale. In a recent study published by “Le Monde”, 60% of respondents said they were “satisfied” with the French social model, but 64% also declared that the model should be at least partially reformed. The French government should use this as a sign that it can make some adjustments to the French tax system and labour markets, without jeopardising its chance of being re-elected in two years. With its popularity at an all-time low and unemployment at an all-time high, there is no more time to waste.

Green bonds are instruments in which proceeds are exclusively applied towards new and existing green projects – defined as activities that promote climate or other environmental sustainability purposes. They enable capital raising and investment in projects with environmental benefits. The International Capital Market Association (ICMA) set out some guidelines for issuing of green bonds in January 2014.

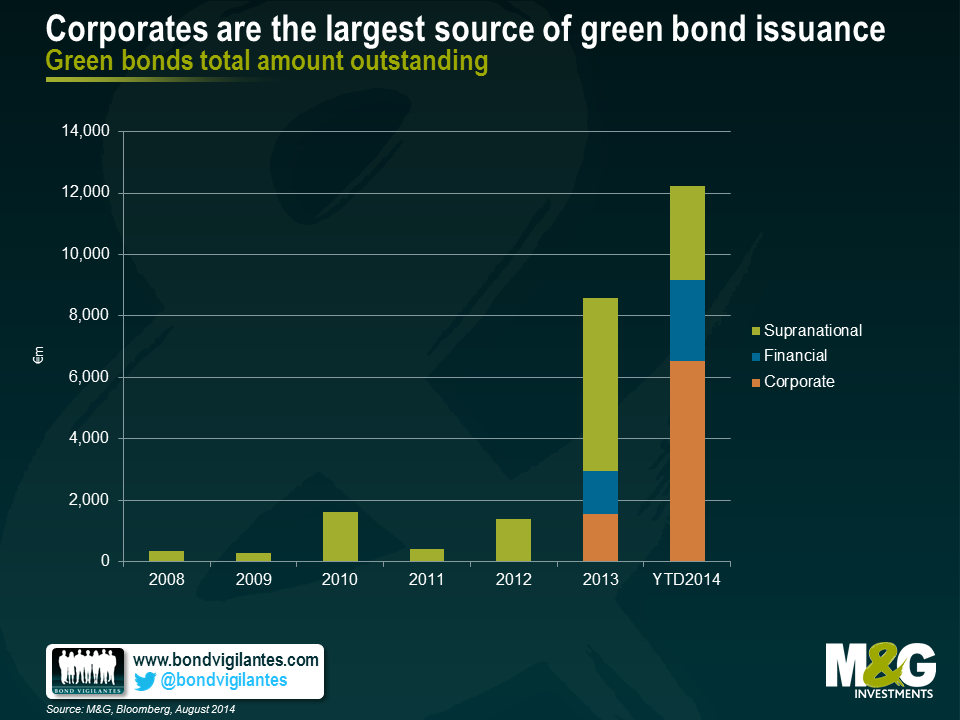

Originally dominated by supranational issuers (for example, European Investment Bank, World Bank and the European Bank for Construction and Redevelopment), financials and corporate issuers are increasingly tapping into this new source of funding.

Green corporate bonds, being a nascent asset class, are a place for many firsts. In October 2012, industrial gases company Air Liquide claimed they were the ‘first private company to issue bonds meeting the SRI investors’ criteria’. This bond predated the Green Bond Principles, and technically may not be a green bond, but is noteworthy in having been ‘mostly placed with Socially Responsible Investor (SRI) mandated issuers’. Since then, we’ve had French utility EDF in November 2013 announce ‘the issuance of the first corporate Green Bond’, although that title may just (by a couple of days) go to the Swedish property company Vasakronan. More recently we’ve had consumer goods company Unilever announce in March 2014 ‘Unilever’s green sustainability bond is the first green bond in the sterling market, and the first by a company in the FMCG sector’.

It is apparent that corporate issuers are keen to spur the development of the green bond market as an alternative funding source and, in doing so, raise awareness of the environmental issues they face. Looking at the chart below shows that corporates are now the single largest source of green bond issuance. Whilst it’s clear that issuers and investors both earn brownie (greenie?) points in terms of enhanced reputation for their involvement and support of sustainable projects, green bonds lack a binding internationally recognised definition, they merely adhere to a voluntary set of guidelines.

One of the structural features of green bonds is that they are often issued off existing Euro Medium Term Note (EMTN) programs and guaranteed by the parent company. Cash flows that service bonds come from the issuer, therefore benefiting from the overall cash flows of the corporate, not just the project that is being funded. It is not surprising, therefore, that the credit rating of these bonds is in line with other bonds issued by the same issuer. This dislocation does, however, mean that investors are not able to identify the cash flows from the underlying project.

Corporate bonds issuers often bracket their use of proceeds into ‘general corporate purposes’, which rarely tells investors much about how or where the proceeds are to be used. Is it, for example, for refinancing, M&A, capital expenditure or share buybacks? In contrast, one of the cornerstones of a green bond is that the use of proceeds is defined in the legal documentation of the security, which should bring a degree of transparency. I say degree because, in practice, once the proceeds are deployed the investor may have limited information on the progress of the project and the extent to which it is meeting environmental targets. For instance, are bond proceeds for the specified project leading to an identifiable reduction in greenhouse gases, water and waste?

There is a certain asymmetry in green credentials required between issuers and investors. For an entity to issue a green bond they have to abide by the principles as outlined by the ICMA. Alongside use of proceeds, these also include project evaluation and selection, reporting, as well as management of proceeds. The latter includes a suggestion to enhance the environmental integrity of the instrument through the use of an external auditor, an independent verifier or as some have called it, a Socially Responsible Investment (SRI) rating agency. Yet with so much stringency on the issuer side, there seems to be no limitation on which bonds funds are able to participate in owning such an issue. Whilst issuers are often citing a desire to diversify their funding sources and attract SRI and Environmental Social and Governance (ESG) conscious investors seeking sustainable (both from a cash flow and environmental perspective) fixed-income instruments, the investors themselves do not necessarily need to have such a green bill of health.

Indeed, even a bond issued in a ‘green wrapper’ may not satisfy certain SRI funds which may argue, rightly or wrongly, for example, that EDF is using cash flows generated through nuclear power activities to pay coupons on its green bond. Another angle on this would be to say that environmental projects are receiving credit enhancement through use of corporate cash flows to prop-up investment in green initiatives. Regardless, the burden remains with the investor to determine how green the bond is. The rating agencies have so far not waded into the argument by assigning a relative ranking of ‘greenness’.

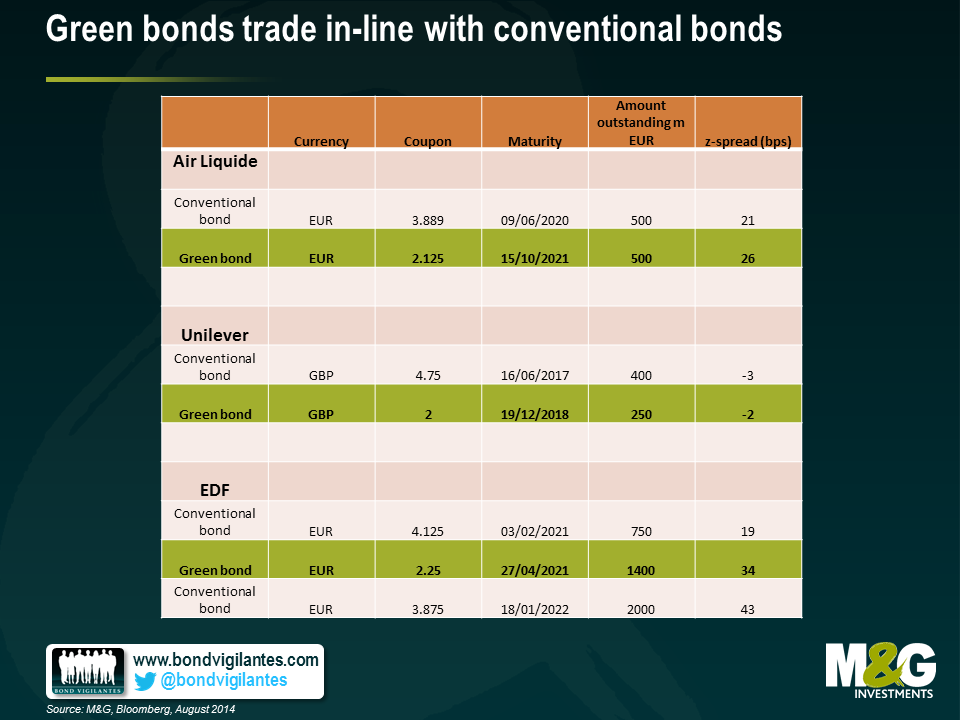

Finally, looking at a few examples of corporate green bond issuers in the table below, it appears that the pricing of green bonds on the secondary market is in line with other (‘non-green’) issues, which to us makes sense given the structural and cash flow arguments mentioned.

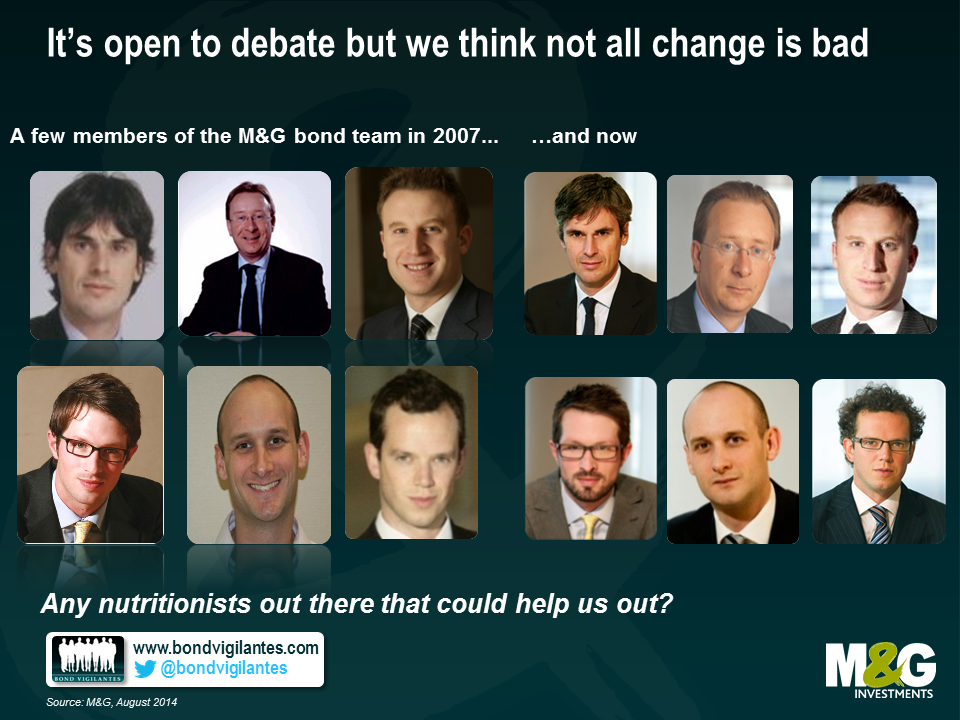

There is a lot of analysis and conjecture about how much impact the financial crisis has had on the global economy and financial markets. There has been considerably less analysis around the impact of the crisis on bond fund managers. In a small attempt to quantify these impacts, we have dug out a few old photos of members of the M&G bond team pre and post-crisis. The photos show clearly where change has been bad.

There is, though, good change. In September there are changes taking place to bank CDS contracts that represent clearly positive progression.

The CDS rules and definitions of 2003 state that there are 3 different credit events that will trigger corporate and financial CDS contracts: 1. failure to pay 2. bankruptcy, and 3. restructuring (this means that a company can’t modify the conditions of debt obligations detrimentally as far as investors are concerned). If any of these are determined to have occurred, then buyers of protection receive par from sellers of protection (and sellers of protection pay out par minus the recovery value of the defaulted bonds, so are in the same situation as if they owned the defaulted bond). In the event of one of these events being triggered, buyers of protection are ‘insured’ against the losses incurred on the bonds.

However, whilst the above works well in most cases of corporate defaults, we have seen several examples in the last few years in terms of banks in which the outcomes have left buyers of protection in effectively defaulted bonds none the better off. For purposes of succinctness and relevance, I would like to mention two of the more recent such cases so as to bring out the flaws of the existing financial CDS contracts, and to highlight the improvements we will soon see.

In early 2013, the Dutch government expropriated the subordinated debt of SNS Bank, which had got into serious difficulties. Bondholders would therefore no longer receive coupons or principal, and so the determinations committee ruled, quite simply, that a restructuring event had occurred. However, the buyers of protection had to deliver defaulted bonds to the sellers, and there being no subordinated bonds left, had to deliver senior bonds, whose value was around 85p in the pound. This meant that they ‘owned’ bonds worth zero, and were being paid out 15p as a result of the protection they had bought!

The most recent example of subordinated CDS not working is still on-going, being the case of Banco Espirito Santo. This bank has seen all the good assets, deposits and senior debt transferred to a new, good, bank, and all the bad assets, subordinated debt and equity stay with the old, bad, bank. So subordinated debt will very likely get a very low recovery (the sub bonds are today trading at around 15 cents). Subordinated bank debt is now, in practical terms, able to take losses and be written down in European banks. Senior bank debt will also become write-down-able at the start of 2016, but as yet legislators and regulators are showing the continued desire to make senior good. In BES’ case, though, with all the deposits and senior debt moving to the good bank (and with a very thin layer of subordinated debt), more than 75% of the liabilities will go to the new entity. In CDS terms, this means that the contracts move to the new entity. So, again, buyers of subordinated protection in BES are left with significant losses on their bonds, but will have to deliver senior bonds which are trading close to and in some cases above par. Not the outcome that the owners of protection wanted or expected. And, frankly, not the right outcome.

So the existing rules around financial CDS are unfit for purpose. Starting in September, new rules will come into place that will vastly improve the economics of these contracts, and in simple terms will make them behave far more like senior and subordinated bonds, which after all is what they are meant to do. The major differences can be summarised into two: a new, fourth, credit event trigger called Government Intervention will be added; and the removal of the cross default provision. The Government Intervention trigger will mean that in instances such as SNS, when governmental authorities impair debt, CDS contracts will be triggered, and in the same case, owners of subordinated protection would have delivered a claim on the Dutch government that was worth zero, through the expropriation, and would have received par from sellers of protection. In terms of the second major reform to financial CDS contracts, current contracts mean that a credit event on subordinated CDS also results in a credit event on senior. This clause will be removed, meaning that in the Banco Espirito Santo on-going case, subordinated CDS contracts would travel with the subordinated bonds, and senior with senior. Unlike the changing faces of the Bond Vigilantes, the changes soon coming in CDS are ones we think are positive.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.