Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

In 1714, an Englishman called Bernard Mandeville published his poem entitled “The Fable of the Bees: or Private Vices, Public Benefits”. The satire was about a hive of prosperous bees that were living a life of luxury. One day, some of the bees began to grumble that their lifestyle lacked virtue and the bees subsequently turn away from greed and extravagance. This leads to a rapid loss of prosperity as the bees give up their high-spending ways. This was Mandeville’s paradox; frugality and virtue won’t lead to prosperity and commercial dominance. If people spend more, they would have more.

At the time, the thought was revolutionary. The conventional wisdom was the best way to become prosperous was to save, not spend. However, if people were to buy more, then this could create a virtuous circle where everyone stood to benefit. There would be more jobs, higher wages, increased profits, and higher standards of living.

That was 300 years ago. Today, the developed world is a world of consumption. In general, we stopped producing stuff a long time ago. Companies were quick to offshore manufacturing operations, keen to benefit from the low wages on offer in the emerging markets. The price of goods subsequently got cheaper as companies passed on some cost-savings to the end-consumer.

In the U.S., household consumption expenditure (the market value of all goods and services purchased by households) is around 68 per cent of GDP. In the U.K, it makes up around 65 per cent of GDP. German and Japanese consumption spending is around 56 and 61 per cent respectively. In these huge developed economies, consumption makes up around two-thirds of GDP. Strong consumption growth rates will – by and large – lead to a pick-up in economic growth.

None of this is new in the world of economics and government policymaking. What is new is a working paper entitled “The Rich and the Great Recession” which was released by the IMF late last year. In analysing the U.S. recession of 2008-09, the authors find that the conventional macro explanations offered for the recession are flawed. Indeed, the authors argue that the rich (those households that are in the top 10% of incomes and have an average net worth of $3.3 million or more) were the cause of the swings in consumption during the boom and bust (note that the financial side of the crisis is ignored in the paper).

Even though the financial crisis was more than six years ago, economists are still sifting through the wreckage of the global economy looking for clues as to what caused the crisis. Two key macro narratives have emerged:

Both narratives largely focus on the middle class (which is defined as the poorest 90% of American families by household income), and the impact that house prices had on consumption and savings rates. What is interesting about this paper is a new analysis on how the rich behaved in the lead up to the crisis as both narratives ignore the role the rich played in the boom-bust cycle. There are potentially important conclusions for policymakers to draw upon should they wish to kick-start economic growth.

It is largely taken for granted that the rich have a lower marginal propensity to consume than those that are less wealthy. Because the U.S. household saving rate fell over a 30 year period to a low of 2.5%, it would suggest that the wealth narrative is the more correct narrative, as large wealth gains boosted consumption.

For the income inequality narrative to hold true, economists would expect to see an increase in the savings rate as the shift in income distribution towards the rich created excess savings. Most economists explain away this conundrum (rising inequality and a falling savings rate) by suggesting that the reduction in middle class saving outweighed the rise in saving by the rich. The economists from the IMF propose that the more likely explanation for the fall in the saving rate was actually an increase in consumption by the middle class which was accompanied by a decline in the saving rate of the rich.

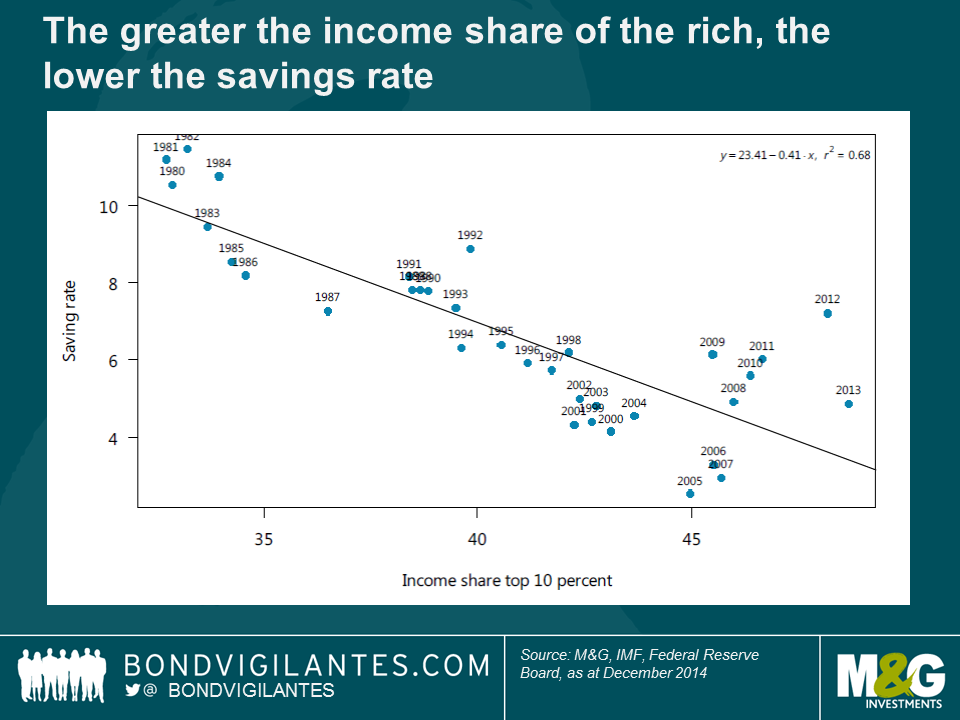

The theory that the fall in the saving rate which ramped up house prices was caused by the middle class is wrong. For starters, the decline in the savings rate had been ongoing for decades before the 2008 recession. Additionally, the rich now own such a large part of income that it is very difficult for their saving rate to deviate too far from the average. The below chart shows the correlation between the income share of the rich and the savings rate is strongly negative. That is, the greater the income share of the rich, the lower the aggregate savings rate.

The key conclusion is this: the rich must have played a key role in driving the consumption boom-bust cycle because they were the group that received the bulk of the income and wealth gains during the period. Today, income inequality in the U.S has never been greater and America’s richest 10 per cent of families own 85% of financial assets. Quantitative easing and record low interest rates have pushed up the value of these financial assets even higher as investor portfolios have been rebalanced towards higher yielding investments.

The authors conclude “the rich now account for such a large part of the economy, and their wealth has become so large and volatile, that wealth effects on their consumption now have a significant impact on the economy. Indeed, the rich may have accounted for the bulk of the swings in aggregate consumption during the boom-bust.” This conclusion is in stark contrast to the conventional narratives put forward for the economic cycle, which focus on the role of the middle-class.

The rich are increasingly driving the bulk of overall consumption growth, which is the main component of economic growth in the developed economies. If policymakers want to generate GDP, then they should encourage the rich to consume and reduce their savings rate.

Mandeville’s observations from 300 years ago still ring true; developed economies in the 21st century depend on the rich.

An overriding theme for U.S. high yield energy companies in the current oil price environment is having sufficient financial liquidity (cash, bank credit, etc.) to cover their obligations as earnings come under pressure due to low oil prices. Maintaining liquidity until oil prices recover will be paramount for energy companies to survive, even for those names that aren’t especially levered. It is likely that most energy-related companies will see a marked increase in financial leverage (and subsequently financial risk) over the coming months due to the depressed oil price environment.

A key source of liquidity for these companies is via their asset-backed bank credit facilities (or more specifically, reserved based lines or RBLs, which are tied to an individual company’s proved reserves, mostly oil and natural gas). These RBLs are often covenanted and most are revalued every six months by the bank group providing the RBL. Obviously lower oil prices means the value of most companies’ reserves have declined and RBLs will be adjusted accordingly, affecting credit availability.

The revaluation of RBLs will be kicking off soon, plus many Exploration & Production (E&P) companies are expected to test their covenant levels even if there is a modest recovery in oil prices. It is our belief that most bank groups will be supportive during the spring review season. Furthermore, we believe most companies will have success obtaining covenant relief as banks are keen to give their clients ample runway to navigate the current commodity price environment.

Last week, U.S. E&P company EXCO Resources, announced that it was granted covenant relief from its bank group in exchange for a c.20% reduction in its RBL. EXCO’s bank group lowered the company’s borrowing base to $725 million from $900 million. The revised agreement also removed the existing total leverage ratio covenant (essentially a cap on total financial leverage imposed by the bank group) until Q4 2016 when it will be re-instated at 6.0x debt-to-EBITDA (a measure of a company’s indebtedness compared to its earnings) with this level gradually decreasing to 4.5x by Q1 2018.

The banks were not entirely altruistic as the revised facility added a senior secured leverage covenant of 2.5x (limiting the amount of leverage allowed where the banks are positioned in the capital structure) and an interest coverage ratio of 2.0x to still ensure the banks have an avenue to re-negotiate the RBL should circumstances deteriorate materially worse-than-expected.

This is encouraging news as it supports our thesis that banks will be supportive of their E&P clients, especially since EXCO was not a distressed or massively over-levered company (relatively speaking) – EXCO’s net leverage as at Q3 2014 was c.3.5x debt-to-EBITDA, but it was widely anticipated that this leverage measure would go much higher in 2015 at current oil prices. The 20% reduction in the RBL is also consistent with our expectations that most companies will see moderate but manageable RBL reductions. It does not mean the company is in the clear as the operating environment is still extremely challenging, but the relaxing of the covenant gives the company some breathing room to navigate with less worry about breaching covenants or running out of liquidity in the near-term. The market has reacted positively to the news as EXCO’s 2018 USD bond is trading up 7 points (it was trading at 68 prior to the announcement).

While not necessarily a precedent (other more-distressed companies have successfully renegotiated their covenants), the EXCO news is encouraging as it demonstrates bank group support for the sector as we expect similar circumstances with numerous U.S. high yield E&P companies over the coming weeks and months. With a number of high yield energy bonds trading between 60 and 90, there is value to be had and opportunities to invest in the sector as long as one can understand and identify those companies with sufficient liquidity and/or those likely to be supported by their bank groups.

Diane Coyle came in to talk about her study of the history of Gross Domestic Product a couple of weeks ago. You can watch a short interview we did with her here. We also offered you a chance to win a copy of her book, and we had over 60 correct answers to this question: he’s regarded as one of the creators of modern GDP statistics, but in 1934 he told Congress that “the welfare of a nation can scarcely be inferred from a measurement of national income”. Who is he?

These were the first 10 names out of the hat and win a copy of book. I hope you enjoy it as much as I did.

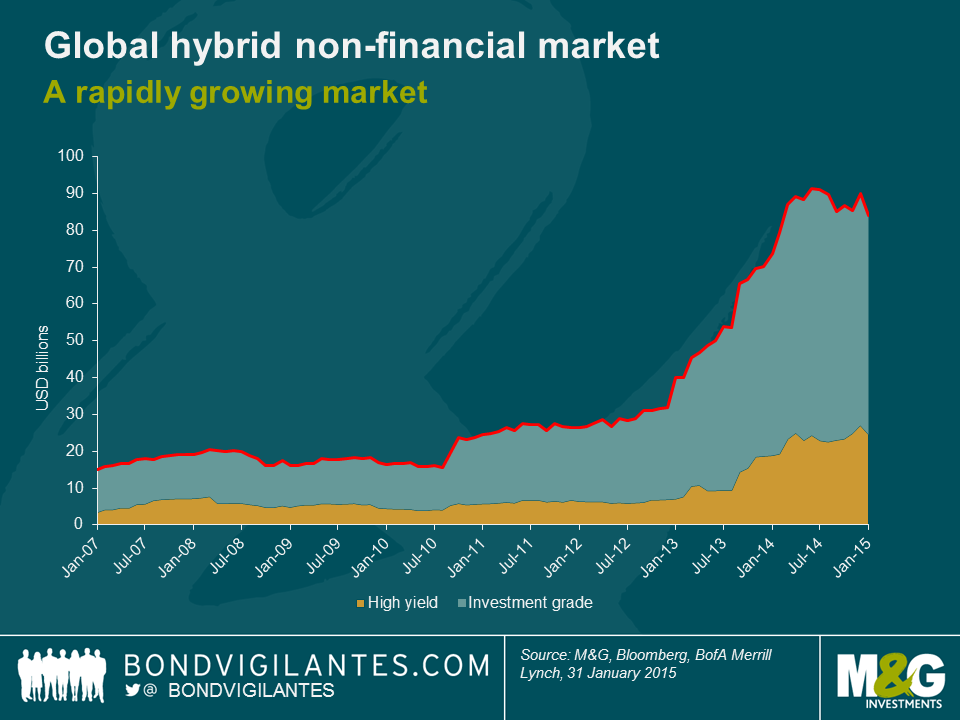

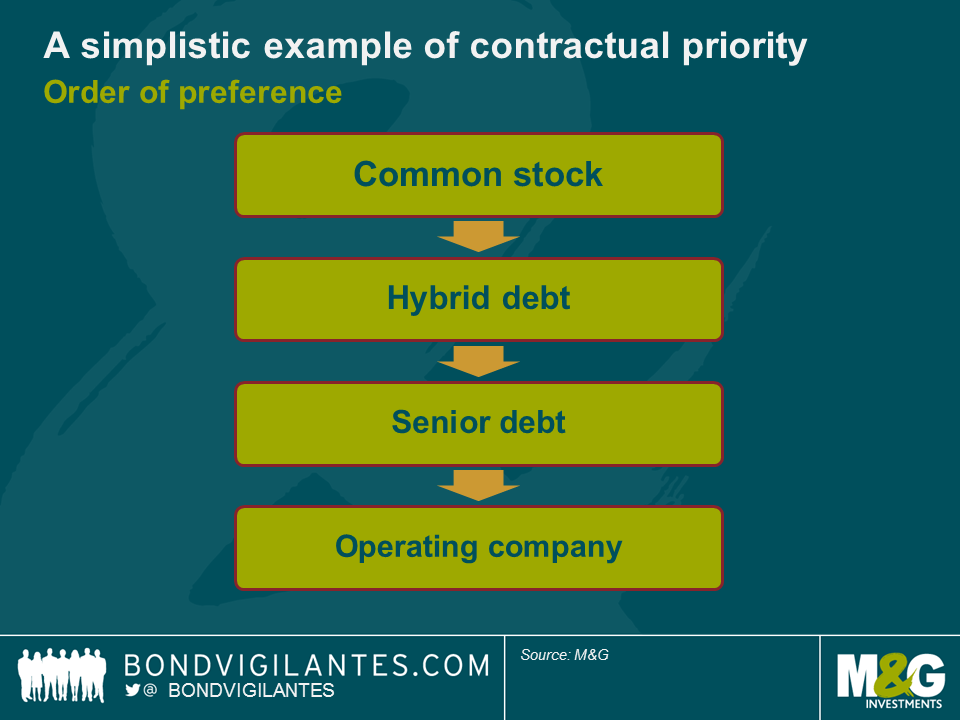

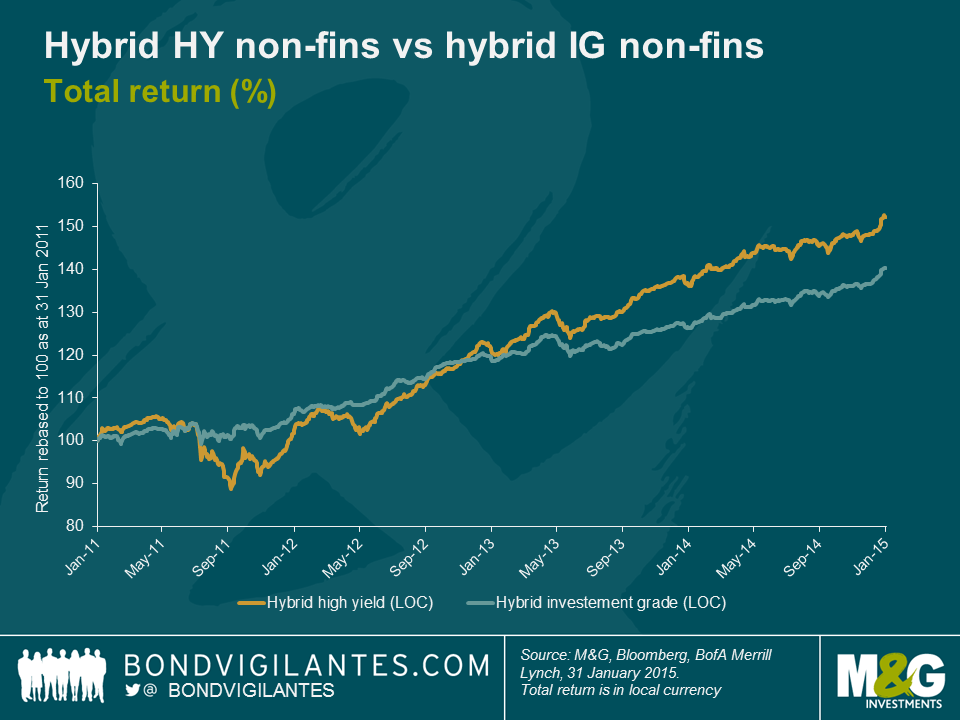

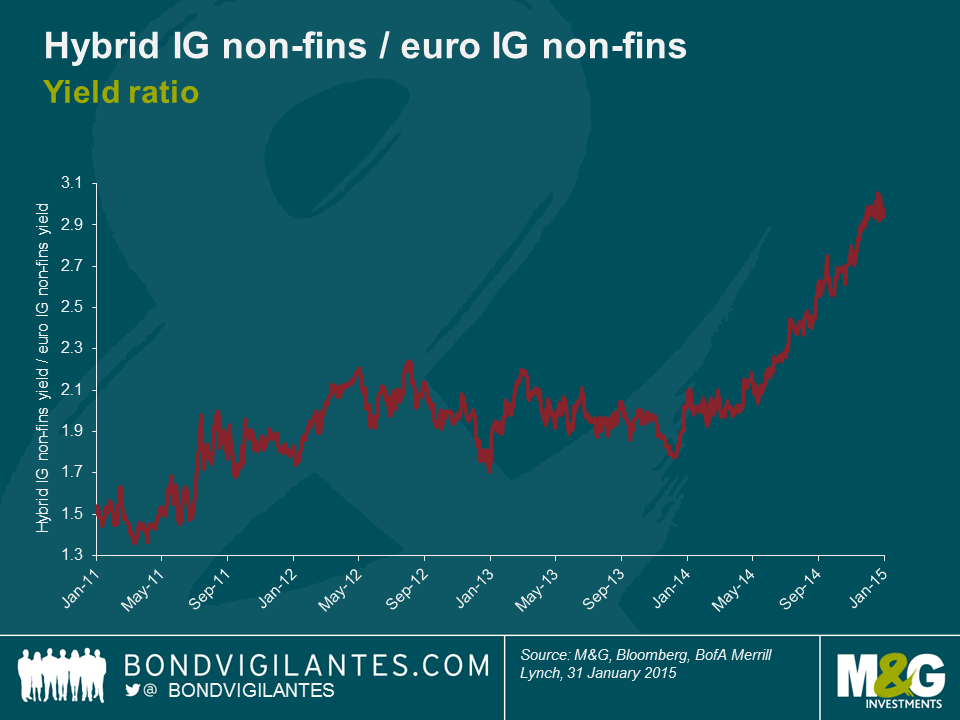

The rapid growth of the hybrid corporate capital market (non-financial) over the last few years has provided fixed income investors with an opportunity to access a quasi-equity income stream. Much like equities, hybrid bonds are perpetual in nature (though an option to call exists), and allow the issuer a degree of discretion over coupon payments. And, whilst they rank ahead of common equity in the event of liquidation, they are contractually subordinate to the more commonly issued senior debt.

As we wrote in 2010, the incentive to issue hybrid capital is clear. The credit rating agencies assume a degree of equity benefit for the hybrid capital that is dependent upon the issuer and structure in question – this enables support for an issuer’s credit rating that would typically otherwise have to come from good old-fashioned equity. Hybrids don’t require existing owners to be diluted nor are any voting rights sacrificed. Furthermore, issuers are also able to treat hybrids as debt for tax purposes, deducting coupons from taxable income.

The economics from an issuer’s perspective may look something like the following. Let’s make a few basic assumptions: a European company can on average issue equity at 7% and senior debt at 1.5%, which translates to 1% after tax. Let’s also assume that the rating agencies allow 50% equity credit for hybrid capital.

So, to achieve a 50/50 equity/debt mix a company treasurer can either issue a hybrid at, say, 3% whose true cost is 2% after tax; or issue a mix of 50% equity at 7% and 50% senior debt at 1% after tax. The blended cost of the latter is 4%, which is approximately 2% more expensive than issuing a hybrid.

Thus the argument for issuing hybrid capital is a fairly compelling one and is likely to feature for years to come in fixed income markets. However, from an investor’s perspective, the case is perhaps a little more nuanced.

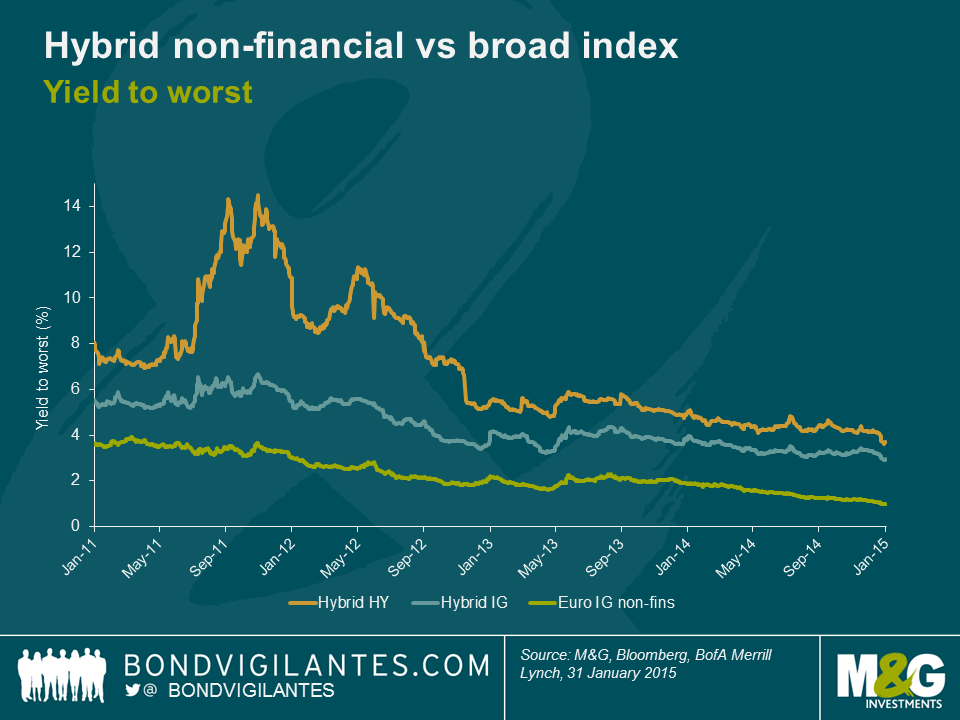

Like all financial market assets the hybrid capital market has been supported by an extremely benign discount rate in recent years. In a world of scarce yield and a desire for exposure to large, multi-national corporates the hybrid market ticks many boxes. In fact, to replicate the average yield available from corporate hybrids with an average rating BBB/BBB- , an investor would need to invest in the senior debt of BB-/B+ rated companies – essentially giving up four notches, not forgetting that hybrid notes are already rated several notches lower than their parent ratings due to the contractual subordination.

Hybrid capital has already been one of the principal beneficiaries of central bank balance sheet expansion in recent years. In January alone, the universe returned 2.73% after the ECB’s QE announcement. And with high-quality industrial corporate bond yields practically at zero, the ratio between hybrid capital and senior debt looks as attractive as ever, though some caution should be applied given that the denominator is so close to zero.

With European investors as keen as ever to own quality yield we can continue to expect both issuers and investors to look upon the market favourably. Whether both sides of the equation will look back on these securities with the same fondness in several years’ time is anyone’s guess.

One of my favourite economic reads of 2014 was Diane Coyle’s book about an economic statistic – GDP. Whilst monarchs had been trying to take inventories of the national wealth since the Doomsday Book and earlier (so they could tax it!), the idea that you should rigorously measure economic activity is under one hundred years old. But the concept of Gross Domestic Product has now become central to the management of all economies (remember the Maastricht Criteria which based participation in the Euro area on debt and deficit ratios related to GDP? Diane’s book tells how Greece’s dubious GDP number was generated in one room above a parade of shops and without the aid of a computer).

Even with banks of computers GDP is challenging to measure, subject to big revisions, and in a world of rapid technological change, arguably measuring the wrong stuff. But for us bond market participants watching Bloomberg screens, or Prime Ministers announcing triumph, it’s the big one.

In this 10 minute video Diane Coyle (@diane1859), Professor at the University of Manchester and responsible for Enlightenment Economics discusses the history of our most used economic statistic, and asks whether it’s the best we can do.

We have 10 copies of Diane’s excellent book to give away in our competition. Question: he’s regarded as one of the creators of modern GDP statistics, but in 1934 he told Congress that “the welfare of a nation can scarcely be inferred from a measurement of national income”? Who is he?

Please email your answer to bondvigilantes@mandg.co.uk by 5.00pm Monday 16th February. The first ten correct answers drawn at random will win a copy of the book. This competition is now closed.

Matt’s and James’s recent blogs outlined some of the issues markets face when rates go negative. This is obviously no longer just a theoretical debate, but has real investment implications. Why do investors accept sub-zero rates when they can hold cash ?

To recap using Swiss Francs for example, it makes sense for a saver from a purely economic view not to deposit a Swiss Franc note into a negative yielding bank account, as it will be worth less when it gets returned, due to negative rates.

However, the saver faces risks by holding physical cash as they don’t receive the security benefits from using a bank account (ie paying for an electronic safety box). The use of the old fashioned lock and key is not as convenient as a bank account, but would make increasing sense to use as deposit rates get more and more negative. This demand for owning physical as opposed to electronic cash is not confined to cash accounts. In theory, as the term structure of interest rates falls below zero, bond investors should sell their bonds and own “cash in a box” instead. How efficient is it to do this ?

The great problem with using paper money as a saving instrument is that its inherent best in class liquidity also makes it vulnerable to fire and theft. From an individual’s perspective, the use of a secure fire proof safe deposit box in a bank or a secure location away from home is the best starting point. The optimum solution however relies on economies of scale. Is this easily achieved?

As an investor, diversity makes sense. Therefore, an individual should spread their cash over a wide selection of safety deposit boxes in a wide variety of very secure locations. An improvement, but currently not that practical. But there could be a way to achieve the above goals relatively efficiently and cheaply.

In a negative interest rate environment there are likely to be enough investors who want to own bearer cash for a network of highly secure safe deposit boxes to be developed by a bank or institution. This means there would be a high degree of security and diversification regarding the location for the cash. In order to make the cash available to the investor easily, certificates of deposit could be issued physically or preferably electronically. This would allow the investor to transfer money easily, as they would only need to go to their nearest depository to deposit or access the cash, or their nearest bank if a bank agrees to physically deposit or withdraw cash for them. Basically this ends up being a bank account where the cash does not get lent, but has a custodian holding charge. In theory, in the extreme, you could even develop markets in exchange traded derivatives issues that are linked to cash held in a depository, to allow individuals and large institutions to manage cash as a saving instrument with no negative yield. A new efficient savings industry could be developed in a negative yield environment, so limiting the downside to the sub-zero bound for short and long term interest rates.

One side effect would be that all these savings would have to be held in real cash, which will mean an increase in the demand for physical notes. If cash is held in custody and is not lent on then the supply of money in the economy for normal transactions will fall. This begins to sound deflationary, and runs counter to why sub-zero policy is being pursued.

As long as cash exists in a physical bearer form it is hard to see how you can have significant negative rates of interest in an economy where government debt and cash are the obligations of the same entity, as they are truly fungible. At its worst, monetary policy of sub-zero rates could encourage a deflationary spiral. Maybe the only policy left to create inflation is real and not conservative QE (see my last blog).

Picture the scene: a meeting room, 40 floors up, plate glass floor-to-ceiling windows with views of central London in the background. At the polished mahogany table sits Hans Schmidt, the CFO of a major consumer global goods company. In walks Chad “Ace” Jefferson III, the latest in a long line of investment bankers assigned to cover his company. Behind Chad follows an entourage of five impeccably dressed junior bankers, whose sole purpose seems to be to carry Chad’s presentation packs.

“Hans! Buddy! High five!” Chad almost shouts as he bounds across the room with his hand raised.

Hans looks at him blankly, refusing to reciprocate the vulgar greeting. Instead he gets up and offers a handshake.

“Hello Mr. Jefferson,” he mumbles, already slightly irritated.

“I love you Swiss guys, so formal! It’s awesome!” says Chad beaming widely, shaking his hand.

“Yes, well, I agreed to this meeting because you said you had a once in a generation opportunity for our business Chad, if you don’t mind, let’s get on with this yes.”

“Alriiiight! Let’s get to it.” Chad turns to one of his entourage. “Jean-Philippe” he barks, “Get your ass in gear, give Herr Schmidt a presentation, chop chop!”

“OK so I’ll cut to the chase,” he says, pushing aside the presentation that Jean-Phillippe had worked on until 4am that morning. “Now that the ECB has finally got with the programme and done some good ‘ol fashioned QE, a good chunk of the European government bond market is now trading at negative yields. This means the scope for funding your business on the cheap is better than ever my friend. Here’s the thing …”

Chad leans towards Hans and almost inaudibly delivers his killer blow.

“With our help, your company, Hans, could issue a bond with no cost to the company.” Chad leaps to his feet and starts pacing around.

“I’m talking no coupon Hans! Free money! No interest rate! This is a thing of beauty. Think about it, a €500m bond issued at zero cost of financing. We can re-finance a big chunk of your debt and reduce the interest costs to zero. This baby feeds straight to the bottom line. I’m talking major EPS benefits buddy. Your board will love you for it Hans. It’s a no brainer! BOOM!” To emphasise his point, Chad slam-dunks the presentation into a nearby bin, causing Jean-Phillippe to wince.

Hans turns to Chad and says, “OK, so you have my attention. This sounds interesting. But why would any investor buy my company’s bonds without a positive coupon? Does that not defeat the whole point of a corporate bond?“

“Great question Hans! It’s a case of choosing the lesser of two evils here. If you are a bond investor, buying a corporate bond from a respected company like yours for zero return, it may well be a better option than buying a government bond with a guaranteed negative return to maturity. You still get a positive credit spread after all. Also, if you think we are going to experience deflation in the Eurozone, a zero return in nominal terms still means a positive real return, either way, you are better off – crazy I know, but true!”

Chad finishes and sits down, smiling even more broadly than before, supressing the urge to punch the air.

Fin

Now, I hasten to point out that all of the above is total (and poorly written) fiction, but we may be getting closer to the point where such conversations are possible.

In his daily note to investors on 4th Feb, Jim Reid at Deutsche bank pointed out that Nestlé’s EUR 2016 bond closed at a yield of negative 0.002%.

The market is essentially sending out an unprecedented pricing signal to highly rated corporate issuers. It’s saying “we will not demand a nominal positive return for lending you money.”

The immediate consequence of this is a further reduction in potential funding costs for short term debt, particularly for investment grade companies. This could lead to yet another round of financing cost efficiencies. Additionally, we may even see zero yield short term corporate bonds being issued for the first time – a brave new world indeed.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.