If you want to generate economic growth then encourage the rich to spend

In 1714, an Englishman called Bernard Mandeville published his poem entitled “The Fable of the Bees: or Private Vices, Public Benefits”. The satire was about a hive of prosperous bees that were living a life of luxury. One day, some of the bees began to grumble that their lifestyle lacked virtue and the bees subsequently turn away from greed and extravagance. This leads to a rapid loss of prosperity as the bees give up their high-spending ways. This was Mandeville’s paradox; frugality and virtue won’t lead to prosperity and commercial dominance. If people spend more, they would have more.

At the time, the thought was revolutionary. The conventional wisdom was the best way to become prosperous was to save, not spend. However, if people were to buy more, then this could create a virtuous circle where everyone stood to benefit. There would be more jobs, higher wages, increased profits, and higher standards of living.

That was 300 years ago. Today, the developed world is a world of consumption. In general, we stopped producing stuff a long time ago. Companies were quick to offshore manufacturing operations, keen to benefit from the low wages on offer in the emerging markets. The price of goods subsequently got cheaper as companies passed on some cost-savings to the end-consumer.

In the U.S., household consumption expenditure (the market value of all goods and services purchased by households) is around 68 per cent of GDP. In the U.K, it makes up around 65 per cent of GDP. German and Japanese consumption spending is around 56 and 61 per cent respectively. In these huge developed economies, consumption makes up around two-thirds of GDP. Strong consumption growth rates will – by and large – lead to a pick-up in economic growth.

None of this is new in the world of economics and government policymaking. What is new is a working paper entitled “The Rich and the Great Recession” which was released by the IMF late last year. In analysing the U.S. recession of 2008-09, the authors find that the conventional macro explanations offered for the recession are flawed. Indeed, the authors argue that the rich (those households that are in the top 10% of incomes and have an average net worth of $3.3 million or more) were the cause of the swings in consumption during the boom and bust (note that the financial side of the crisis is ignored in the paper).

Even though the financial crisis was more than six years ago, economists are still sifting through the wreckage of the global economy looking for clues as to what caused the crisis. Two key macro narratives have emerged:

- The inequality narrative: Starting in the 1980s, incomes of the high-saving rich soared, while those of the middle class stagnated. The rich lent their savings to the middle class, who used the funds to speculate in real estate and maintain their consumption (something technically referred to as “keeping up with the Joneses”). Eventually, the middle classes became swamped in too much debt and stopped buying properties. House prices subsequently collapsed, causing homeowners to a) default or b) increase their savings rates to pay down their debts. The large increase in gasoline prices in 2004-07 didn’t help the prospects for a consumption-led economic recovery either.

- The wealth narrative: The large increase in asset prices during the boom years encouraged consumers to spend, leading to a fall in the savings rate. When asset prices began to fall, household wealth fell leading to a collapse in consumption.

Both narratives largely focus on the middle class (which is defined as the poorest 90% of American families by household income), and the impact that house prices had on consumption and savings rates. What is interesting about this paper is a new analysis on how the rich behaved in the lead up to the crisis as both narratives ignore the role the rich played in the boom-bust cycle. There are potentially important conclusions for policymakers to draw upon should they wish to kick-start economic growth.

It is largely taken for granted that the rich have a lower marginal propensity to consume than those that are less wealthy. Because the U.S. household saving rate fell over a 30 year period to a low of 2.5%, it would suggest that the wealth narrative is the more correct narrative, as large wealth gains boosted consumption.

For the income inequality narrative to hold true, economists would expect to see an increase in the savings rate as the shift in income distribution towards the rich created excess savings. Most economists explain away this conundrum (rising inequality and a falling savings rate) by suggesting that the reduction in middle class saving outweighed the rise in saving by the rich. The economists from the IMF propose that the more likely explanation for the fall in the saving rate was actually an increase in consumption by the middle class which was accompanied by a decline in the saving rate of the rich.

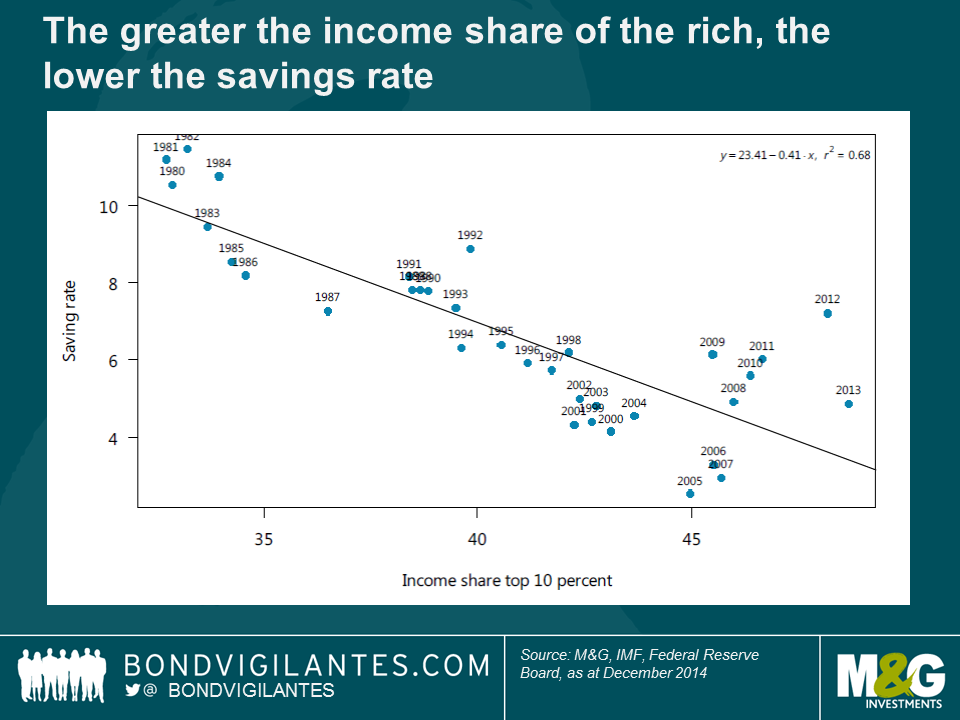

The theory that the fall in the saving rate which ramped up house prices was caused by the middle class is wrong. For starters, the decline in the savings rate had been ongoing for decades before the 2008 recession. Additionally, the rich now own such a large part of income that it is very difficult for their saving rate to deviate too far from the average. The below chart shows the correlation between the income share of the rich and the savings rate is strongly negative. That is, the greater the income share of the rich, the lower the aggregate savings rate.

The key conclusion is this: the rich must have played a key role in driving the consumption boom-bust cycle because they were the group that received the bulk of the income and wealth gains during the period. Today, income inequality in the U.S has never been greater and America’s richest 10 per cent of families own 85% of financial assets. Quantitative easing and record low interest rates have pushed up the value of these financial assets even higher as investor portfolios have been rebalanced towards higher yielding investments.

The authors conclude “the rich now account for such a large part of the economy, and their wealth has become so large and volatile, that wealth effects on their consumption now have a significant impact on the economy. Indeed, the rich may have accounted for the bulk of the swings in aggregate consumption during the boom-bust.” This conclusion is in stark contrast to the conventional narratives put forward for the economic cycle, which focus on the role of the middle-class.

The rich are increasingly driving the bulk of overall consumption growth, which is the main component of economic growth in the developed economies. If policymakers want to generate GDP, then they should encourage the rich to consume and reduce their savings rate.

Mandeville’s observations from 300 years ago still ring true; developed economies in the 21st century depend on the rich.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox