Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

Economic policy hawks love inflation expectation surveys. As do bond fund managers, who like to keep a close eye on inflation to ensure that fixed income returns aren’t being eroded away. Provided that inflation expectations are close to target, we tend to argue expectations are well anchored and thus central bankers can rest easy. However, the monetary policy actions undertaken by many central banks this year suggests some have had a few restless nights pondering the future of their respective economies. Given the nature of the policy moves which have been largely easing in nature, it suggests that central bankers are concerned that price stability is under threat.

Of course, price stability is not under threat to the upside. This would have had the hawks screaming. Rather, the spectre of deflation haunts central bankers in 2015. The collapse in oil prices (which are not only a function of excess supply, but also deficient demand) has quickly fed through into official inflation numbers. Deflation is a reality for many consumers across the euro area, prompting the European Central Bank to embark upon an aggressive quantitative easing programme. Deflation in the UK is a distinct possibility, with the CPI unchanged in the year to February. Interest rate hikes in the UK now appear further away and may not happen this year at all.

The results of the M&G YouGov Inflation Expectations Survey carried out in February 2015 reveal that consumers’ short-term (one year ahead) inflation expectations continue to moderate across most regions. In the UK, short-term inflation expectations fell to 1.5%, down from 2.0% recorded in November last year. Over the long term (five years ahead), median expectations remain stable at 3.0%. In Europe, inflation expectations have generally remained flat or fallen over the short and long term. Similarly in Asia, households’ expectations for price increases have moderated across the board.

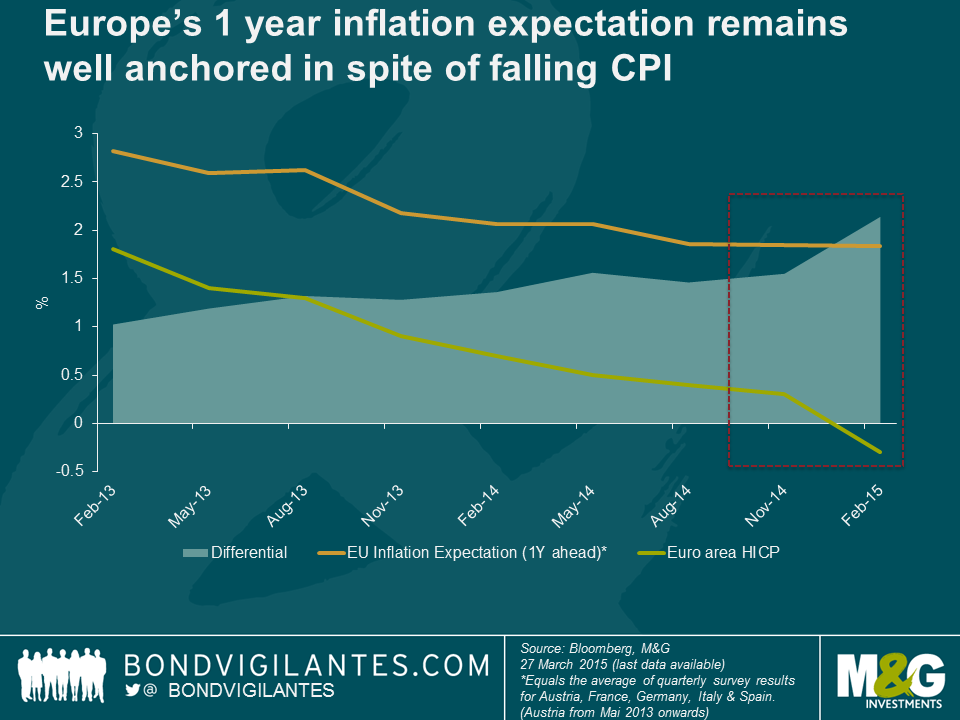

Despite inflation expectations being well anchored in the euro area, it is interesting that the differential between inflation expectation and realised inflation has been widening since the inception of the survey. This will comfort Mario Draghi and the ECB. Despite deflation in the euro area, short-term inflation expectations remain firmly around the ECB’s price stability target of close to 2%.

Central bankers should be encouraged by these results. Whilst our results show a moderation in expectations, they remain at or close to central bank targets over the longer term. In the UK, Mark Carney will be happy that confidence in the Bank of England is at an all-time high with one out of every two consumers confident that the BoE can deliver price stability. Consumers retain a high degree of confidence in the Swiss National Bank as well, despite the collapse of the peg between the Swiss franc and the euro in mid-January.

The full report and data from our Q1 2015 survey is available here. In addition to short-term and long-term inflation expectations, it contains details on central bank price stability, government economic confidence (only 36% of UK respondents think the government is following the right economic policies – up from 23% in Feb 2013), family finances and net incomes.

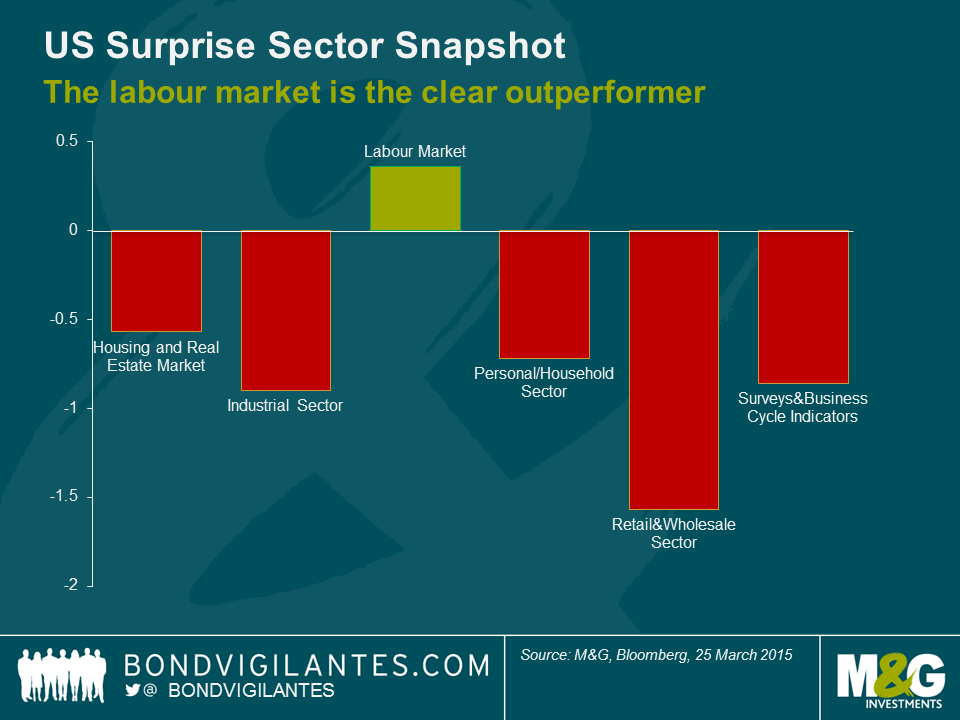

The condition of the US labour market is one of the hot topics in the ongoing “will they / won’t they” Fed rate hiking debate, and as Bloomberg’s Economic Surprises screen shows, this sector is the only area of the economy outperforming expectations of late.

Labour market indicators continue to impress, with employment indicators strong on many measures. Initial Jobless Claims have dropped to 282,000 (market estimate: 290,000), the four-week average declined 7,750 to 297,000 and the number of people filing Continuing Jobless Claims for unemployment benefits fell 6,000 to 2.416m. We blogged last year about the fall in Initial Jobless Claims and noted that the absolute number alone understated the strength of the labour market, since as a percentage of the US labour force population, this statistic had hit multi-decade lows. If we consider Initial Jobless Claims to be a proxy for the flow of labour, then what has happened to the stock – i.e. the Continuing Claims – of labour?

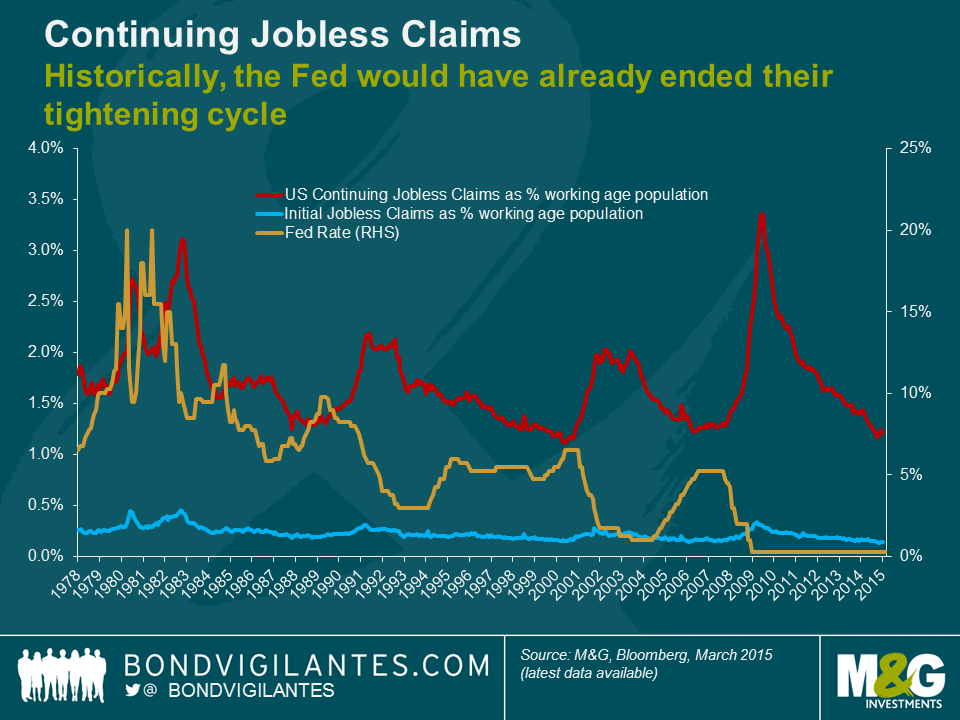

The graph below shows both the flow and stock of labour as a percentage of the working age population aged 15-64. While Initial Jobless Claims has fluctuated within the 0-0.5% band over the last forty years, Continuing Claims move unsurprisingly within a much wider range. What is surprising however is that Continuing Claims as a proportion of the labour force hasn’t been any lower (1.22% at the beginning of this year) since the boom years at the turn of the century.

Historically, Continuing Claim cycles have bottomed out when the Fed has reached the top of its monetary tightening cycles (see the late 1980’s, early 2000 and in 2007). In recent years however we have seen a break from trend; an improvement in the labour market, without the corresponding policy tightening. It appears that by historical standards, the Fed are behind the curve. The new conundrum however, is that average hourly wage growth was 3.8% in the first quarter of 2000, compared to just 1.6% today. This weak wage growth, and the still elevated level of U6 unemployment (which includes discouraged workers and those working less than they’d like to) relative to the headline unemployment level, implies that the lack of a Fed rate hike is due to a preoccupation in the quality of jobs rather than just the quantity.

Almost two years ago to the day we wrote about a return of animal spirits, the LBO of Heinz by Berkshire Hathaway and 3G, and the significant role debt had to play in the transaction. Yesterday Heinz announced that it is to merge with Kraft Foods to create the fifth largest food and beverage company in the world. The transaction will see Berkshire Hathaway and 3G invest an additional $10bn in the form of a special dividend to Kraft shareholders, in order to take a controlling 51% shareholding in the combined company.

In the Berkshire Hathaway 2014 Annual Report Warren Buffet spells out the acquisition criteria he looks for, most of which is satisfied here. These are that the purchase be large, that the company has demonstrated consistent earning power and good returns on equity whilst employing little or no debt, that it has strong management in place, a simple business, and an offering price (i.e. a business that is readily up for sale). I say ‘most’ as one could readily argue that $8.6bn of current long term liabilities at Kraft (as at the end of the financial year 2014) doesn’t satisfy that ‘little or no debt’ criteria. And Heinz also carries its fair share of debt at $14bn, though both figures need to be taken in context.

In the same Annual Report referenced above Buffett extols the virtues of Berkshire Hathaway and its ability ‘to allocate capital rationally and at minimal cost.’ He goes on to say that Berkshire can ‘ move huge sums from businesses that have limited opportunities for incremental investment to other sectors with greater promise.’ No doubt he and his partner Charlie Munger have an enviable record in doing exactly that, but recently it could be argued the pendulum has been swinging increasingly in their favour.

The mega LBOs that saw the likes of Caesars, TXU, Freescale & Clear Channel acquired pre-Lehman by multiple private equity shops acting in concert are unlikely to be contemplated today. And even if they were, satisfying the requisite 15-20% return on capital would prove challenging on the back of several up years for most equity markets.

Berkshire Hathaway on the other hand has cemented its position as a behemoth that can continue to call on massive cash reserves and an exceptional reputation. And so can it call on super cheap funding from the bond markets. Despite articulating a general distaste for debt its increasing willingness to do so saw the holding company lose its AAA/Aaa status a few years back. And more recently it would seem that the super cheap funding available from bond markets has proven too attractive to ignore. Only this month, Berkshire Hathaway borrowed €3bn from the European credit markets. At a weighted average cost of funding of 1.2% for up to 20 years the company has a huge arbitrage available that can’t be matched elsewhere. Despite the re-rating that has occurred in equity markets, an implied earnings yield of 6-7% still looks attractive if a decent portion of your term funding costs are close to zero.

With central banks continuing to ensure that liquidity remains plentiful Berkshire Hathaway is likely to sit pretty. Meanwhile, the arbitrage opportunities look set to continue. Other large deals will be on the horizon.

For years the Western world mocked Japan’s attempts to recover from its spectacular debt-fuelled boom and bust, blaming the Bank of Japan for doing far too little and far too late, and lamenting Japanese fiscal stimulus as extreme recklessness, where the only achievement has been to propel Japan’s debt levels into the stratosphere.

Now, seven years after much of the developed world’s own debt fuelled bubbles went pop, some people (us included) are starting to wonder if Japan’s post bubble experience was actually a good outcome, relative to today’s exceptionally dark prognosis for not just the Eurozone but other economic blocs too.

Richard Koo is developing a cult following as someone who has long seen the parallels between the Japan of the 1990s and where we are today. With theories rooted in Keynesianism, he has consistently argued that Japan’s lost decade and the 1930s Great Depression came about because of ‘balance sheet recessions’, where the private sector’s determination to delever in the aftermath of a debt-fuelled bubble means households and/or companies can’t be encouraged to borrow and spend at any level of interest rate. Instead, the private sector’s desperation to save means that it is up to the government to step in to prevent the downward spiral of debt deflation.

Richard’s very accessible recent book, Escape from Balance Sheet Recession and the QE Trap, provides a broad update on his previous work, applying his theories to the problems faced today in Japan, the US, Europe and China. We discuss aspects of this in the brief interview below.

We have 10 copies of Richard’s book to give away in our competition.

Question: In 1937, US President Franklin D Roosevelt reacted to an improvement in the US economy by aggressively cutting back the budget deficit, which arguably caused a 30% slump in industrial production, a surge in unemployment, and a 50% crash in equities that saw the Dow Jones return to 1933 levels. Sixty years later, encouraged by the IMF and OECD among others (and despite Richard’s warnings at the time!), Japan repeated the same mistake, which had similar consequences – Japan’s economy contracted an unprecedented 5 quarters in a row as reported at the time, helping to trigger a banking crisis (although other events in Asia in 1997 undoubtedly greatly exacerbated the damage). Who was the Japanese prime minister at the time?

Please email your answer to bondvigilantes@mandg.co.uk.

This competition is now closed.

The spectre of deflation currently haunts central bankers around the world, though many of us would question whether the true effects of falling prices are being felt in the real economy and more importantly in consumers’ wallets.

According to the results of the M&G YouGov Inflation Expectations Survey over the past two years, European consumers often believe that inflation in one and five years’ time will run well above the official inflation rate. There is a reason consumers often think “felt” inflation is higher than the “real” measure.

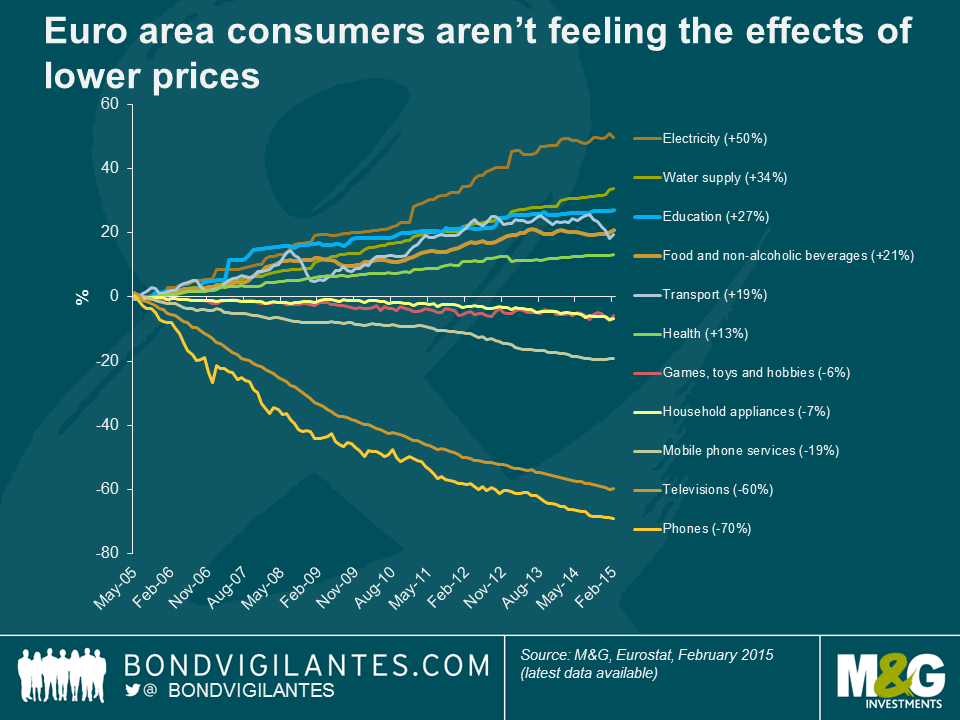

The chart below highlights the difference in the prices of “needs” versus “wants” over the past decade for euro area consumers. As can be seen, the prices of “needs” such as electricity, water and food have increased by between 20-50%. In contrast, the prices of “wants” such as phones, televisions, and games have fallen and are actually cheaper.

From this analysis, it appears consumers are entirely rational in estimating that inflation is higher than the officially reported measure. This is because individuals and families are reflecting their actual cost of living, rather than a basket of goods and services. The majority of their incomes (which have risen by only 8.5% over the past 5 years) are spent on the staples of modern life and as these staples have been appreciating in value, household finances have come under sustained pressure.

This potentially has implications for those anticipating that falling prices will result in an improvement in the real spending power of European consumers. If the prices of “needs” remain sticky or increase further then it appears unlikely that the ECB will be able to generate a consumer-led economic recovery. Whilst a fall in the oil price should help ease electricity and gas prices, energy companies often buy their supplies up to three years in advance to ensure supply. Consequently, moves in wholesale prices do not feed through immediately to retail prices. When it comes to energy prices, what goes up doesn’t necessarily come down. In addition, fuel for cars represents only 4.5% of the Euro area Harmonised Index of Consumer Prices (HICP) basket. The falls that we may see in fuel and energy prices will certainly increase consumer disposable income, but will it enough to repair household balance sheets that have suffered from limited real income growth since the financial and European crises?

Next week, with the release of the Q1 2015 M&G YouGov Inflation Expectations Survey, we will see whether consumers are still “feeling” higher inflation. Unfortunately for policymakers, the fall in the inflation and oil prices may not be the boost to growth many are hoping it could be.

As the old adage goes, markets don’t like uncertainty. And yet in just under two months we have a UK election, about which the only degree of confidence that anybody has is that the UK will have a second successive hung parliament – the key question is whether the UK ends up hung to the left, or to the right, or we get a potentially painful outcome somewhere in between.

So we thought it worthwhile to host a UK politics event for clients recently, and drafted in YouGov’s pollster Anthony Wells, along with Alex White of political consultancy Politikos. After the event we recorded a short video to discuss some of the key points.

If you want to keep up to date with Anthony’s and Alex’s views, you can follow them at @anthonyjwells and @AlexWhite1812.

I am just back from a fascinating investor trip to the Middle-East, where I spent a week meeting with corporate and government bond issuers as well as market participants in the United Arab Emirates (UAE). We spoke at length about Islamic finance, the oil price impact and geopolitical risk.

When I asked the question of the oil price impact on the region to corporate issuers and government officials the response was “there is no impact”. In contrast, most unbiased investors and bankers living in the UAE acknowledge that the new oil price context (down 60% in the past 6 months) will result in the Gulf Cooperation Council’s (GCC) growth rates moderating in 2015 and 2016, following a strong 2014.

The impact of lower oil prices on countries within the GCC is not uniform. Saudi Arabia will be challenged most as the economy has little buffer due to social spending needs (the government need to deliver 2 million jobs to Saudi nationals by 2025). This is a contributing factor to my view that Saudi Arabia should cut oil supply by the end of the year. Tourist destinations such as Dubai, and to a lesser extent Abu Dhabi, will be less affected should oil prices remain at current levels. However, the indirect impact will nevertheless be negative. There are a number of reasons for this view:

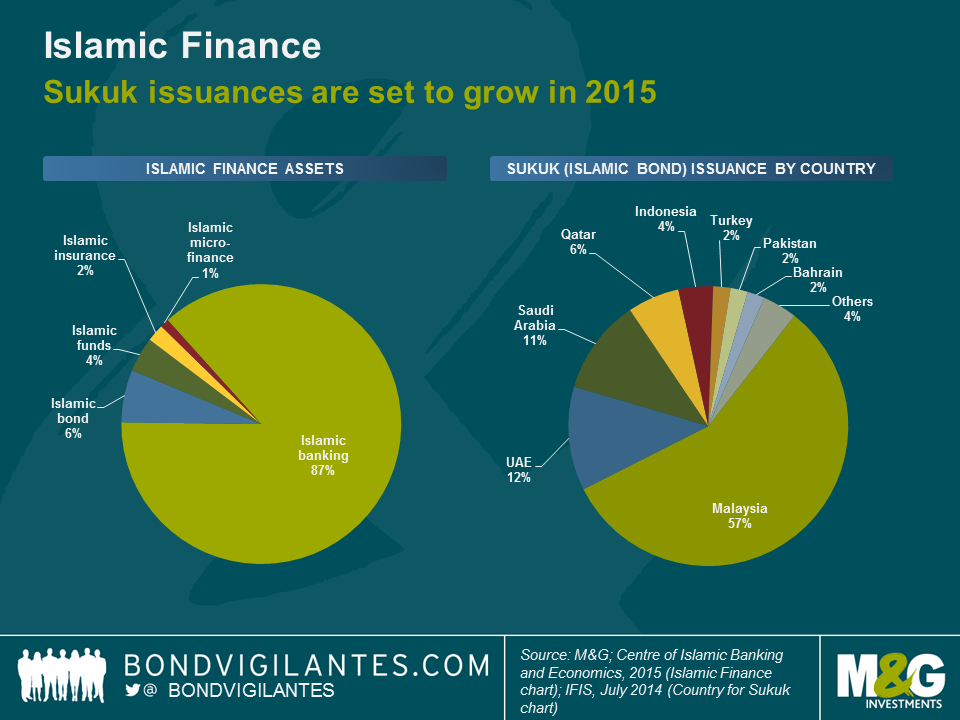

Moving on, Islamic finance has grown at a fast pace (average +20%) since the 2008 global financial crisis and was estimated to be worth USD2.1 trillion of assets in 2014 by the Centre of Islamic Banking and Economics (CIBE). In 2015, the Dubai-based CIBE has estimated that global Islamic financial assets will reach USD2.5 trillion, of which an expected USD150 billion will be sukuk (Islamic bonds) issuance.

Muslim countries obviously dominate the sukuk market – as per the chart below – and Islamic finance is not expected to be a major game-changer in the near future of global financial markets. However, investors have recently seen increasing supply from Western (non-Muslim) countries. Last year, the UK issued its first ever £200 million sukuk bond which has been trading well in the secondary market. On top of this, three banks (Societe Generale, Bank of Tokyo-Mitsubishi and Goldman Sachs) set up sukuk programmes in 2014 which, if successful, will improve liquidity in the global sukuk market.

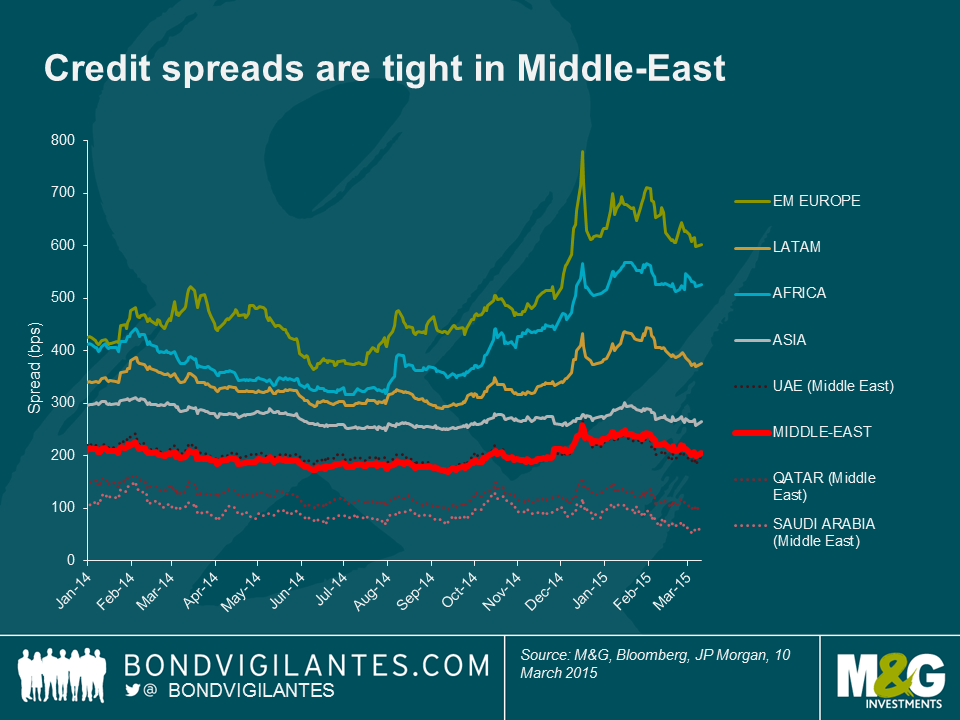

Turning to valuations, from an emerging market perspective, credit spreads have been tight for a long time in the Middle-East due to two major reasons: (i) historical excess cash from oil revenues that fuelled the GCC economies and ultimately supported the corporate bond market, and (ii) political stability in the UAE which account for most of the bond market in the Middle-East.

First, I believe current spreads are not pricing in the new oil price context and the above mentioned negative impact it will have on the real economy of the GCC countries. As a result, relative value looks expensive and some of the most vulnerable bonds could widen significantly by the end of 2015. In addition, I believe that bond investors have been underestimating the increasing geopolitical risk in the region, evidenced by the UAE’s direct military involvement in the Arab coalition against the Islamic State (IS) militant positions in Syria. While the IS is by all means more a direct threat to Syria, Iraq, Libya, Egypt and even Jordan than the UAE, the Arab allies’ involvement in the conflict is to me a risk of spreading the conflict in these countries.

That said, it appears that a large correction across the board is unlikely as the region remains a relative safe haven compared to other EM regions that have their own problems: Russia geopolitics in EM Europe, Brazil weaknesses in Latin America, and China slowdown in Asia. In terms of sectors, bonds issued by banks may weaken due to the soft economic outlook and the residential property sector – particularly privately-held issuers – could come under selling pressure. The commercial real estate sector could prove resilient for investors, as could any corporates benefitting from strong government support. Bond technicals will also be key in the region and a strong local and sticky investor base could provide some protection against more volatile times ahead.

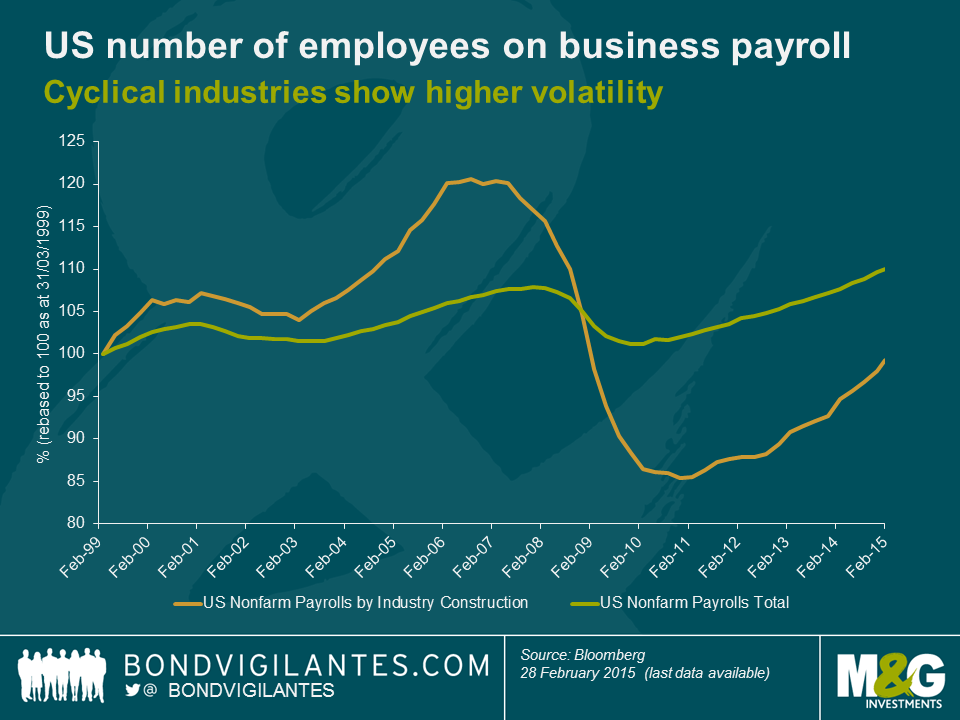

The declining unemployment rate in the US has renewed the debate on the timing and pace of monetary tightening by the Fed. While wage pressures have been muted thus far, the risk is rising that further declines of unemployment will lower the rate below non-inflationary (NAIRU) levels and prompt the Fed to start hiking.

For emerging markets, one of the main transmission mechanisms is through weaker EM currencies versus the US dollar. Additionally, many are concerned about higher funding costs as US Treasury yields rise further. These are significant concerns for EM investors. Despite the recent increase in euro bond issuance (a result of the lower yields on offer in Europe), most corporate external funding is still denominated in USD.

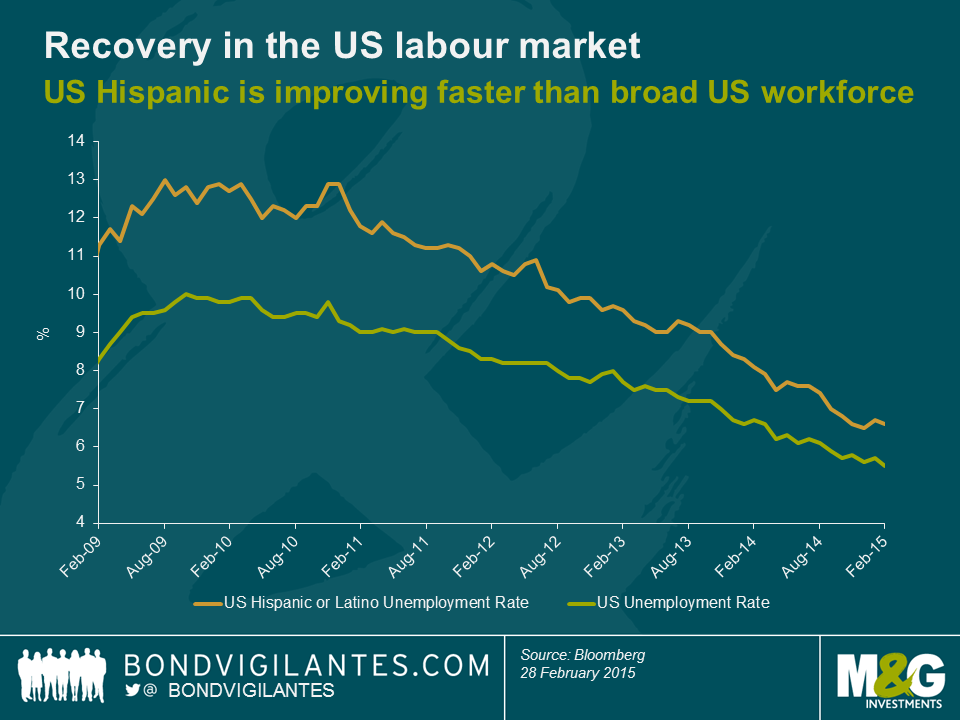

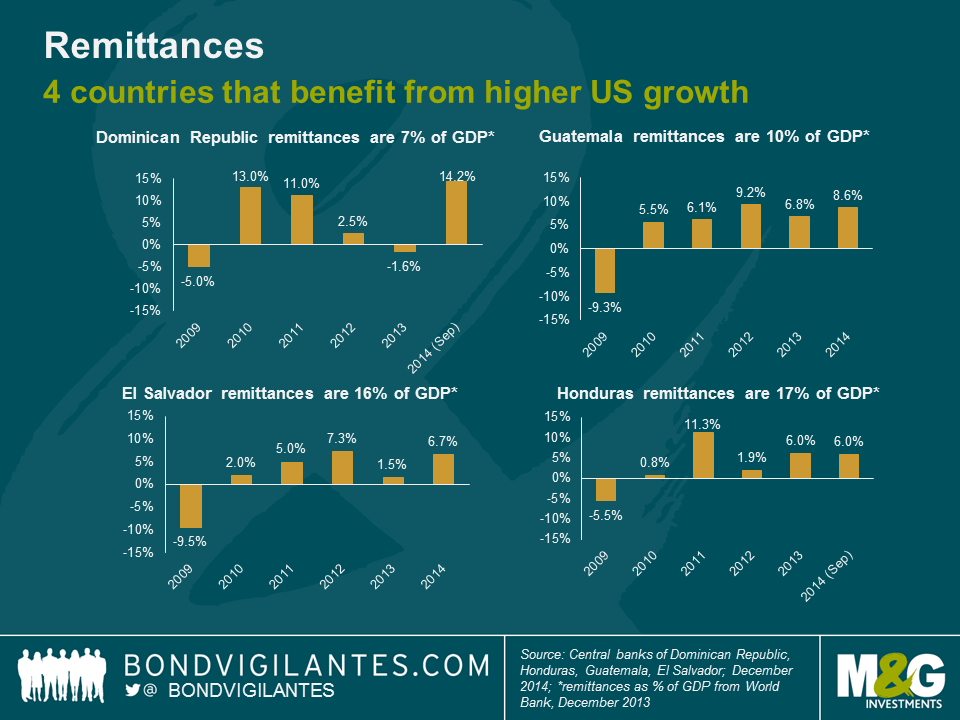

However, another transmission from the US recovery is through remittances. Remittances by US based workers to families in their home countries is highly correlated to economic activity in the US and it can disproportionally benefit a few countries. We can see from the chart above that the unemployment rate amongst the US’ Hispanic population (a proxy for their savings and eventual remittances) is improving at an even faster pace than the broader US workforce, which by itself is recovering at a solid pace. Part of this is because Hispanics are overrepresented in cyclical industries, such as construction.

Remittances have been found to contribute to lower growth volatility in the recipient country (as this recent IMF report pointed out). It also serves as a major social safety net, as the recipient countries generally have very low levels of income and savings and the availability of key services such as health and education is often scarce. Finally, remittances reduce a country’s current account deficit and external funding requirements, which is supportive should capital inflows into emerging markets decline.

The eventual Fed hikes will remain a key concern for many emerging markets. However there are countries that will benefit from the stronger US labour market, particularly those that stand to benefit from US employee remittances.

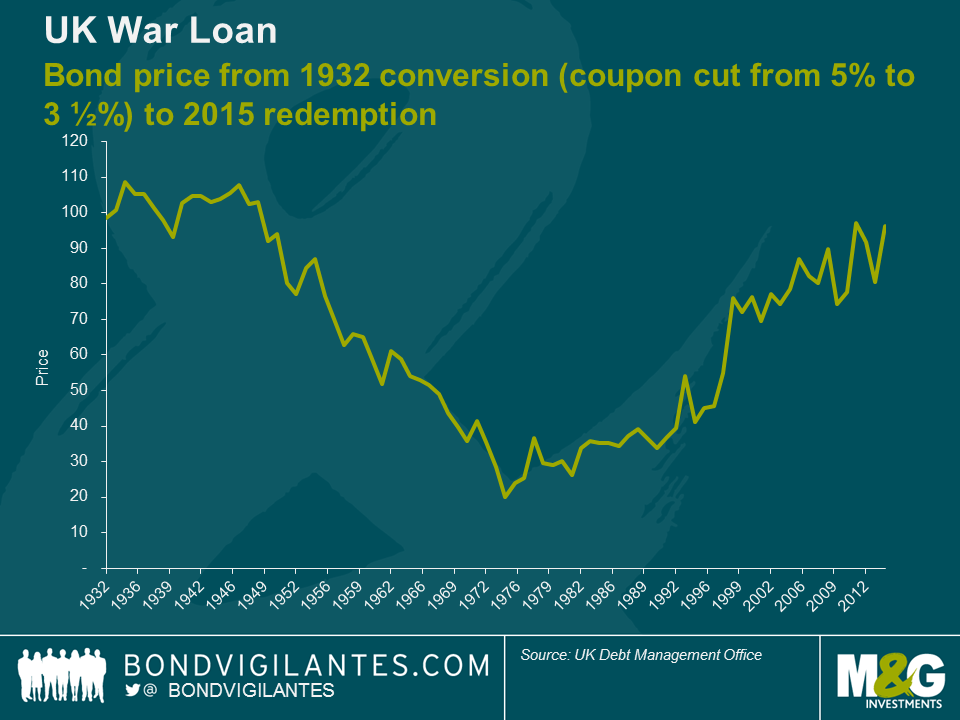

Today, the War Loan issued in 1917 to help finance Britain in World War 1 is finally redeemed. We’ve written about it repeatedly over the years as it has always fascinated us. Was its coupon cut in 1932 a form of default from the UK government? Does George Osborne’s claim that it is being redeemed this year as a result of a tight grip on the public finances ring true?

To commemorate this most interesting of gilts we have made a film about War Loan – one that tells the economic history of the UK through wars, default, the re-joining and leaving of the gold standard, the inflationary 1970s, the loss of the UK’s AAA credit rating, and finally the deflation that has followed the Great Financial Crisis.

Have you seen the film The Day After Tomorrow? The one where U.N. officials foolishly ignore climate scientist Jack Hall (Dennis Quaid) and a super-storm plunges New York into a new Ice Age? Well it was colder than that last week when Mike and I made a research visit over there. With wind-chill it was a billion below. I was only able to survive by laughing at Mike forgetting to wear a hat and gloves on day one. It was that bad.

We saw the full range of Street economists – at one end, one predicted that Yellen would pre-announce rate hikes at her testimony the next day (she didn’t), whilst others saw no chance at all of any action from the Fed for at least a year. The consensus though remains for a June or September hike. In this short video we can barely talk, through cold, but we run through some of the arguments in both directions. In short the Fed WANTS to hike, to prevent financial instability, to get away from the zero bound, and because of a strengthening job market feeding through into wages. But it SHOULDN’T hike because of the global deflation wave, likely negative CPI prints for the US for many months, and for the small but real chance that hiking now would send the economy back into recession, and consign Fed members to infamy as much as the “liquidators” like Andrew Mellon during the Great Depression.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.