Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

Ben Bernanke has spent a good deal of time explaining on his blog why he thinks interest rates are so low (something that Martin Wolf wrote a column on earlier this week). An extremely quick and dirty summary is low nominal interest rates and yields can be explained by low inflation, however this doesn’t explain why real interest rates are also low. Bernanke doesn’t think low real interest rates are down to Fed manipulation (if central banks had deliberately put rates too low then we’d have dramatically overheating economies when in reality we have the opposite) – it’s because the industrialised world generally is seeing weak growth, but in his view this probably isn’t to do with secular stagnation, it’s more to do with ongoing global imbalances.

As bond fund managers, we’re at least as interested in what drives longer dated bond yields versus what affects central bank interest rates and short dated yields. And short term and long term interest rates have been behaving wildly differently of late – market expectations for the first US rate hike have been broadly stable since the beginning of 2014, and yet 10 year US Treasury yields plummeted from 3% in January 2014 to almost 1.6% earlier this year, and have now backed up to 2.2%. As Bernanke explains, it’s all to do with what has been going on with the term premium.

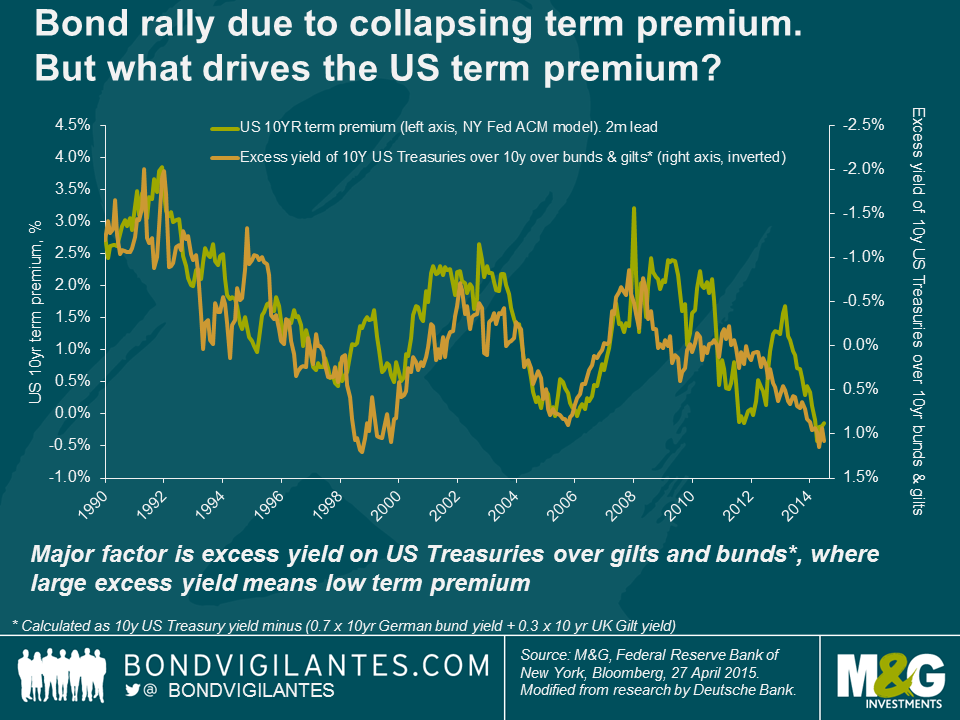

Long dated Treasury yields can be split into three components – expected inflation, expectations about the future path of real short term interest rates, and a term premium, where the term premium is the extra return that investors require to own a long dated bond rather than investing in a series of short dated bonds. You’d normally expect the term premium to be positive since investors should require extra yield to compensate them for the risk of owning longer dated bonds (eg unexpected moves in inflation or the wider economy, uncertainty regarding the future path of central bank interest rates). However, the term premium collapsed through last year and various measures show it to have been outright negative for the first few months of 2015. Indeed, according to the New York Fed’s ACM model*, the rally in US Treasuries in 2014 was entirely due to the collapse in the term premium, and were it not for the collapse in the term premium, in December 2014 the 10 year US Treasury yield would have hit the highest level since 2008. And were it not for the recent jump higher in the term premium since February, US Treasury yields would not have sold off in the last three months but would have rallied!

So the very big, obvious question, is what drives the term premium? Historically the most important factor has been inflation and the perceived risk of unexpected inflation, and a low term premium today suggests investors see little risk of this occurring. The term premium tends to be counter cyclical, being higher in recessions and when there is macroeconomic volatility generally, perhaps because investors are highly uncertain about the direction of future Fed policy.

On the demand side, there’s evidence that the term premium drops if there’s a flight-to-safety bid, eg Russia default and Long-Term Capital Management (LTCM) crisis in 1998 (although the term premium actually spiked sharply immediately post the Global Financial Crisis). Meanwhile the Fed’s QE program probably reduced the term premium, as have regulatory changes that encourage banks, brokers, insurers or pension funds to own more bonds.

And supply factors have also played a part – Greenspan’s ‘conundrum’, where a drop in the term premium meant that 10 year yields fell despite the Fed pushing short rates higher, can be partly explained by US Treasury issuance being heavily biased to short dated bonds from 2001-2006 (although large overseas purchases of US Treasuries likely contributed to a lower term premium – the savings glut – plus surely the predictability of the Fed’s policy contributed to the lower term premium given that they hiked rates by 0.25% in 17 consecutive meetings).

What has stumped Bernanke, along with many investors, was the collapse in the term premium through 2014, at a time when US economic data was robust, QE purchases wound down, and uncertainty and risk aversion were little changed. His two possible explanations are that economic weakness outside the US, and subsequent overseas central bank action, may have spilt over into US Treasuries. Oil prices also fell sharply about the same time as the term premium, but he doesn’t find either of these explanations ‘completely satisfying’ (implying not very satisfying at all).

In contrast, I’d argue that the overseas dynamic has been a key driver of the collapse in the US term premium.

First, the chart below shows that over the last quarter of a century, higher yields in the US relative to German and the UK appear to cause a reduction in the US term premium ,and vice versa. One explanation for this is that higher long dated US bond yields, which are due to expectations of higher Fed funds rate (perhaps due to the relative economic strength of the US) encourage portfolio flows into US Treasuries from abroad, and these flows drive down the US term premium. Lower yields in the US have the opposite effect.

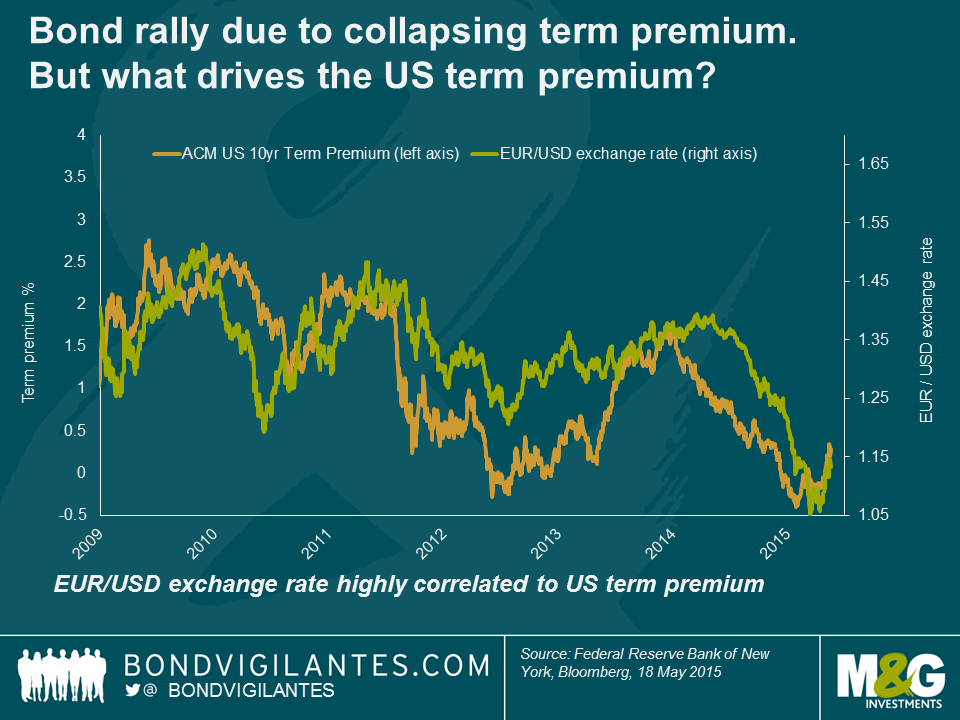

This explanation gains credence if you consider the reasonably close correlation between the US term premium and the EUR/USD exchange rate since 2009 in the chart below. This is related to the point above, given that differentials in short dated bond yields tend to be a major driver of FX movements, but it does suggest that the diverging economic fortunes and diverging actions between the Fed and the ECB has had a major impact on the US term premium on a 10 year US Treasury.

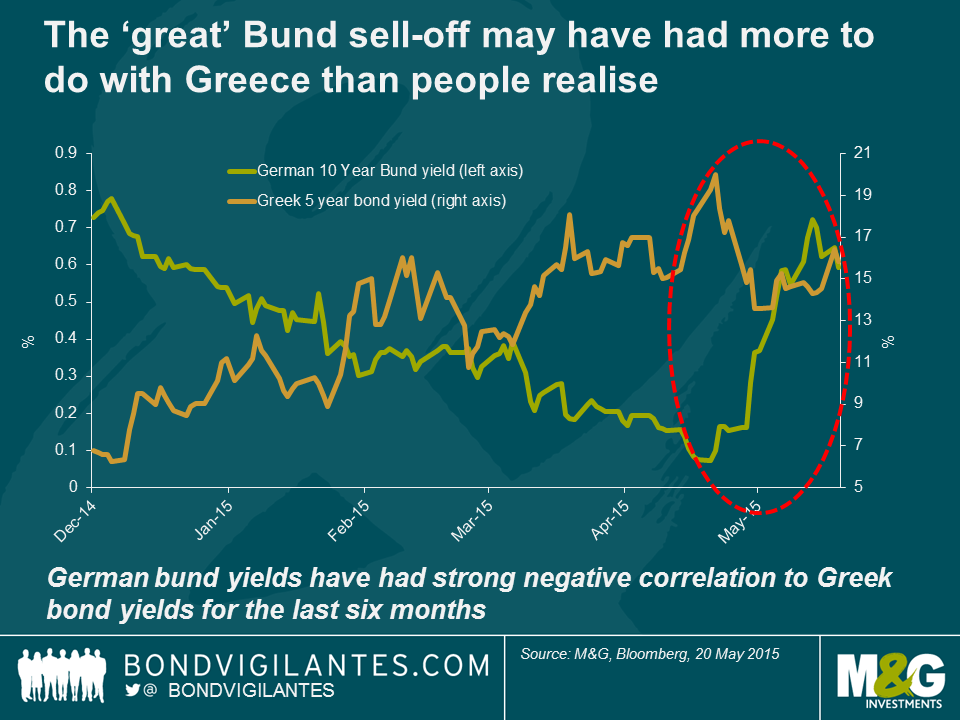

Focusing on just the past few months, the global bond sell off has surprised many given that US economic data has been consistently woeful. As already mentioned, this sell off can be entirely accounted for by the recent rise in the term premium. Again, I would argue that Europe has probably played a key role. European government bonds had already enjoyed a strong rally through 2014 on the back of sustained weakness in Eurozone economic data and expectations of ECB QE, expectations that were eventually validated. However the flaring up of the situation in Greece in October, and particularly since December, appears to have resulted in a significant safe haven bid for core Eurozone government bonds as suggested by the strong negative correlation between bund yields and Greek bond yields.

What are the implications of all of this? The main takeaway is that there are a number of factors that can drive the US term premium up or down, and previous studies have highlighted the correlation of term premia across markets, but Europe and the ECB seem to have recently played a key role. Just as exceptional US monetary policy measures up to last year were exported abroad (especially to emerging markets), the loosening of ECB monetary policy (and to a lesser extent Japan) is now being imported into the US.

So the implication for the investor is that longer dated US bond yields have, at least recently, had little to do with US specific factors. The behaviour of Eurozone bond yields has not been all about QE – crowded positioning may have exacerbated the recent bund sell off, but Greece has likely been a bigger driver of term premia globally in the past six months than many realise. The implication for the Fed is that the US is far from being in complete control of its own monetary policy, bearing in mind that monetary policy does not just include short term interest rates (led by the Fed Funds rate), but also the long term interest rate (Matt wrote a blog on an excellent BIS paper on this in 2013). If global factors are pulling US long term interest rates too low, resulting in excess stimulation of the economy (the most obvious feed through is via the housing market) then the Fed needs to take action. Either it needs to talk up long term rates , and Janet Yellen seems to have tried to do precisely this a few weeks ago (yesterday’s FOMC minutes also mentioned the term premium). Or if that doesn’t work, and it probably won’t if the term premium is indeed dominated by global factors, then it’ll probably need to hike short rates more aggressively than it otherwise would need to. Alternatively, if US data improves and it really wants to engineer a jump in the term premium, then the Fed can hint that it will look to sell back its stock of US Treasuries, which is something that Richard wrote about recently on this blog.

*The term premium is not directly observable, and there are multiple definitions and models that attempt to describe and model the term premium. The Kim- Wright model of the term premium, another widely used model, gives broadly similar results to ACM, although BIS use a model giving a considerably lower level of -2% in early 2015, albeit the general trend has been similar.

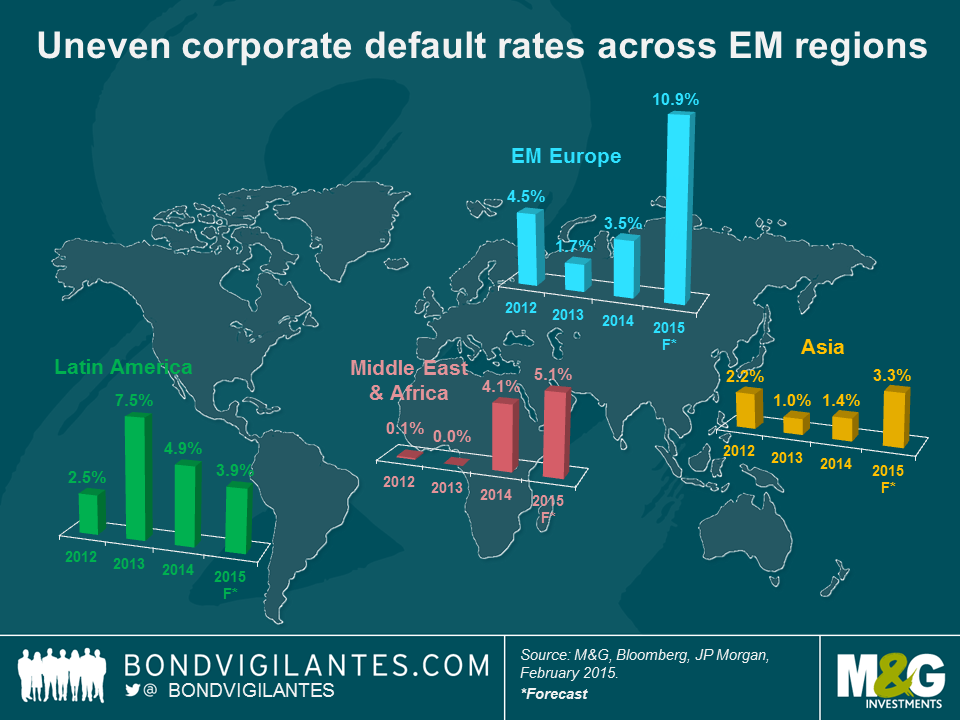

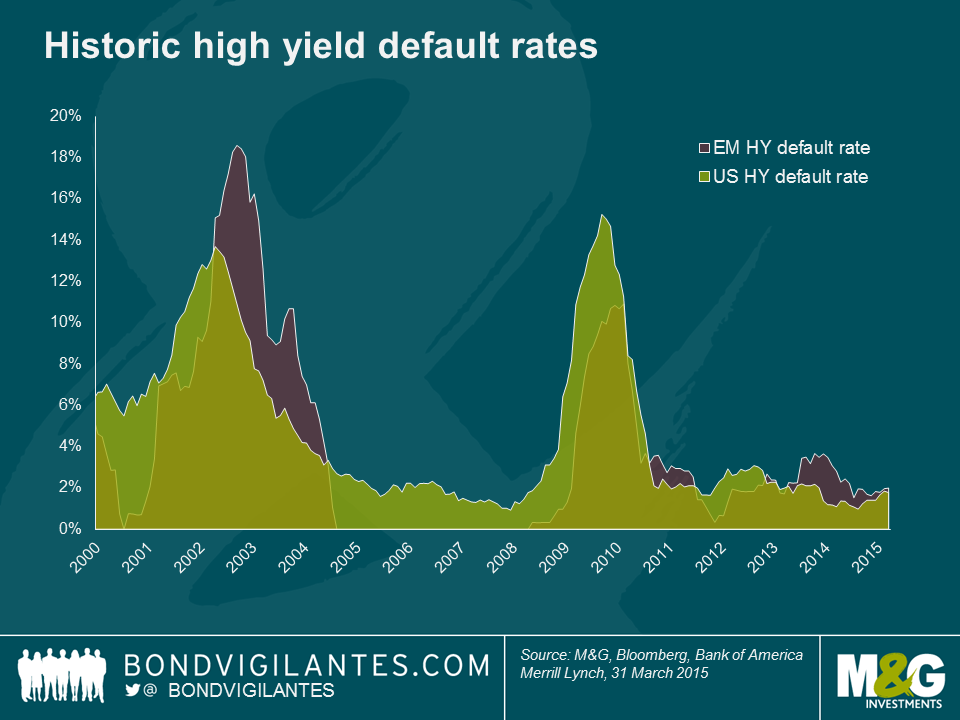

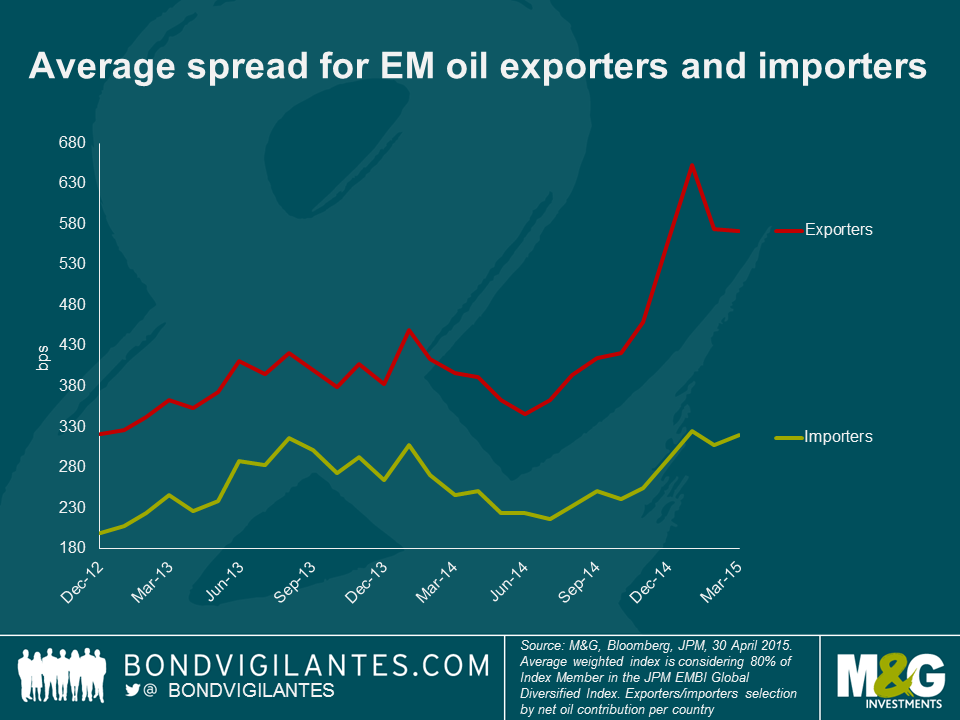

While generating a lot of concerns, one of the benefits of the strong growth of the emerging market (EM) corporate bond universe in the past decade has been the diversification of issuers. The asset class, which at $1.6 trillion is now larger than the US high-yield market, offers a vast number of countries and industries to invest in. Contrary to the EM rhetoric that has been making headlines in 2015, not all emerging countries are experiencing a softening in economic growth: India’s economic outlook is positive and Central America is benefitting from a stronger US economy. Likewise, a number of corporate exporters that have US dollar revenues but domestic costs are actually benefiting from weakness of local currencies against the dollar. In addition, credit quality and default risk is uneven across regions, as per the chart below. There are significant opportunities for the EM corporate bond stock pickers out there.

Interestingly, EM corporate defaults have historically been in-line with those of the US high-yield market and follow similar economic cycles. Since the beginning of the year, at least seven EM corporate issuers have defaulted. In the same period, 20 US and 7 European and other developed market issuers defaulted in the bond market.

As is often the case, region and country selection is paramount when investing in the EM world. In addition, assessing the impact of macroeconomic factors on EM corporate creditworthiness is a critical component of the investment process. For example, Argentina, Brazil and Mexico account for over 42% of all EM corporate defaults in value since 2000. These countries have defaulted multiple times on their sovereign debt obligations, proving that when the creditworthiness of the sovereign deteriorates significantly it is very likely that the corporate will encounter difficult times too. In general, an actual (or likely) sovereign default or a sharp deterioration of economic conditions would likely prompt a number of corporate issuers to either (i) opportunistically restructure debt, like the Ukraine-based iron-ore pellet producer Ferrexpo (which in February 2015 launched an exchange offer of its $500m 2016 bonds with new terms), or (ii) literally go bust on the back of an unsustainable economic environment (as has been the case many times for Argentine corporates in the past).

Sometimes, there is a very fine line between sovereign and corporate. Kazakhstan illustrates this point. While Kazakhstan has never defaulted on its sovereign debt, the 2010 restructuring of $16.6bn of government-controlled BTA bank of Kazakhstan – which led to a 70% haircut on creditors – was seen as a sovereign default and seriously tarnished the reputation of the country with investors.

These factors do not mean that EM investors should use a top-down approach only and avoid emerging countries with poor macro dynamics in order to limit corporate default risk in their portfolio. For example, Russian corporates are currently facing a very challenging macroeconomic environment but their solid credit fundamentals and export-driven nature have been acting as a buffer to these poor economic conditions. EM credits can also default due to bottom up factors, unrelated to the health of the local economy. For example, Brazil’s sugar and ethanol producer VGO defaulted this year due to industry and company specific factors – record-low sugar prices resulted in significant cash burn and a weak liquidity position, triggering unsustainable short-term refinancing risk.

In 2015, there is very little doubt that default rates will increase in the emerging market corporate universe and sorting the micro from the macro will be even more important than it was in 2014. Fundamentals have deteriorated and credit rating downgrades outpaced upgrades in 1Q15. Nonetheless, I still think that EM debt is attractive. Macro risks have fallen since the beginning of the year, and the high yields on offer in the marketplace mean there are opportunities for investors to generate decent returns.

CPI in the UK today fell into negative territory for the first time, posting a 0.1% decline year-over-year. Airfares presented a meaningful drag on the April figures, owing to the timing of Easter compared to last year. Carriers increase their prices over Easter holidays, so when Easter moves between months this causes flight prices to move around, thereby affecting the headline inflation numbers. However, petrol prices were up slightly on the month which slightly offset some of this effect of flights.

The market expects that deflation will be short lived in the UK. By the end of 2015, on the assumption of oil’s stabilising here or hereabouts, CPI will be 0.8% to 1% higher than today’s numbers, as the negative drag of oil’s decline will fall out of the year over year comparisons.

Also noteworthy is that with RPI in April registering a gain of 0.9% year over year, the ‘wedge’ (the extent of the difference between RPI and CPI) has increased to 1%, which is slightly higher than the long-term average. Whilst most of this difference owes to different calculation methodologies (the formula effect), some of this also owes to RPI’s greater inclusion of housing than CPI. Indeed, following the election result and the early signs of a relief rally in the housing market, one should potentially be watchful for the wedge trending higher in the medium term. This is especially important for investors in UK inflation linked bonds, as RPI is the benchmark. In other words, holders of inflation linked bonds are a safe distance away from a deflationary outcome, and the aforementioned base effects should mean RPI moves higher towards the end of the year.

If anyone is looking for potential reasons to see upside inflation surprises, they should be mindful of real wage growth accelerating from here, as well as consumer confidence. Both of these indicators are suggestive of a benign disinflation in the UK at the moment rather than anything worse, with wages on the rise (and having just increased by 0.1% in real terms today), and with consumers indicating that they are more, not less, inclined to make major purchases at this point.

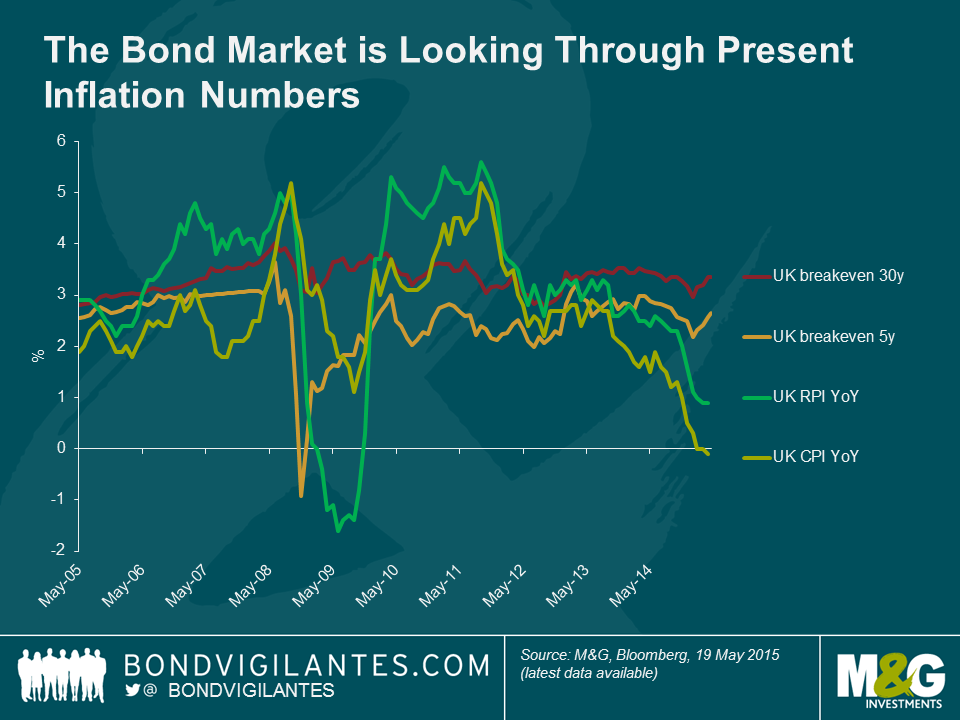

With 5yr breakevens in the UK at 2.65% today, it is very evident that the bond market is looking through the present headline inflation numbers to a more normal environment on average for the next 5 years. Whilst UK breakevens are not as cheap as they were at the turn of 2015, we still feel that the next 5yrs’ inflation outcomes are more likely than not to make an investment in inflation linked bonds a better one than in nominal bonds. Further illustration of the fact that the bond market is less than overly concerned with current low headline inflation numbers can be clearly seen from observing the 30yr, long term, inflation breakeven. At a cost of 3.35% for long term inflation protection, the fixed income market is paying more than the average price of the last 5yrs to protect against long-term inflation, at the very moment that CPI turns negative for the first time.

We’ve seen a swift and rapid re-pricing of the bund curve in recent weeks, highlighting again the risk to capital that bond investors face when yields start to rise. All major bond markets in Europe have been impacted to some degree. Nevertheless one corner of the bond market has remained very resilient: floating rate notes.

We have highlighted before how these instruments have some potentially useful features in a rising yield environment, most notably a very low sensitivity to moves in government bond markets. To put it another way, a bond with little or no interest rate duration has been a good bond to hold over the past few weeks.

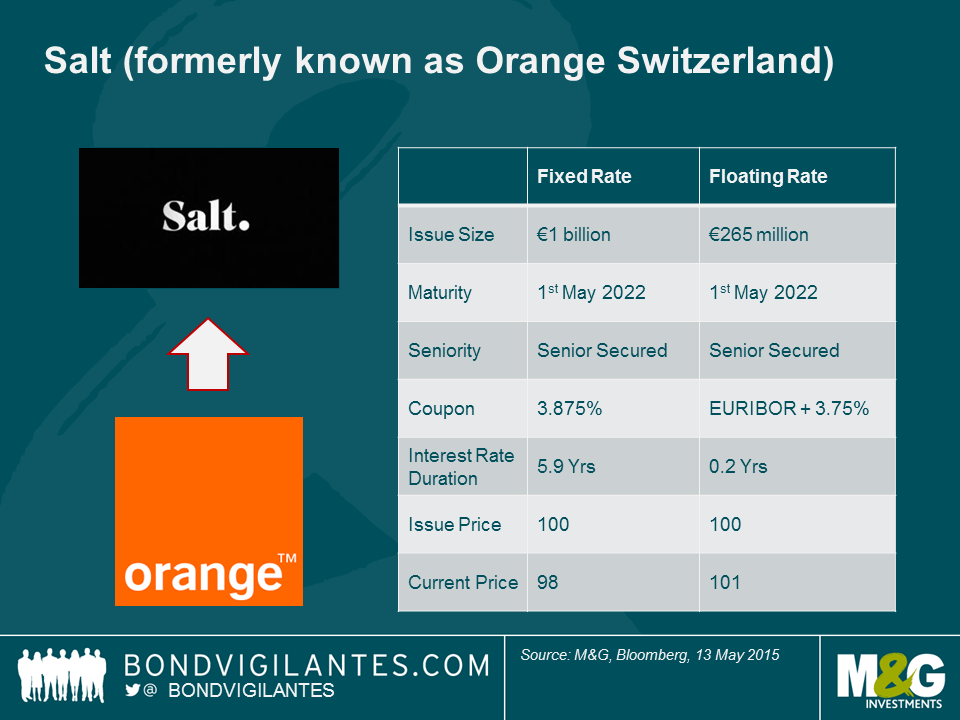

We can see this in action by looking at two bonds recently issued by the Swiss mobile phone business Salt (formerly known as Orange Switzerland). The company refinanced its debt in April, issuing four different bonds. The two of interest here are identical in many ways – they are both denominated in euros, both are senior secured instruments, both have the same maturity date – except for one very important difference: one has a fixed 3.875% coupon, the other has a variable coupon that resets every three months to the prevailing three – month EURIBOR rate plus a fixed margin of 3.75%.

Both instruments have the same credit risk associated with them (the risk that Salt defaults on its debt obligations), but the move from a fixed coupon to a floating coupon drastically changes the bond’s sensitivity to moves in the wider government bond market (this is the interest rate duration number in the table above – it drops from almost six years, to close to zero). The impact of this small but important difference can be seen in the relative price performance of the bonds in the month following their issue.

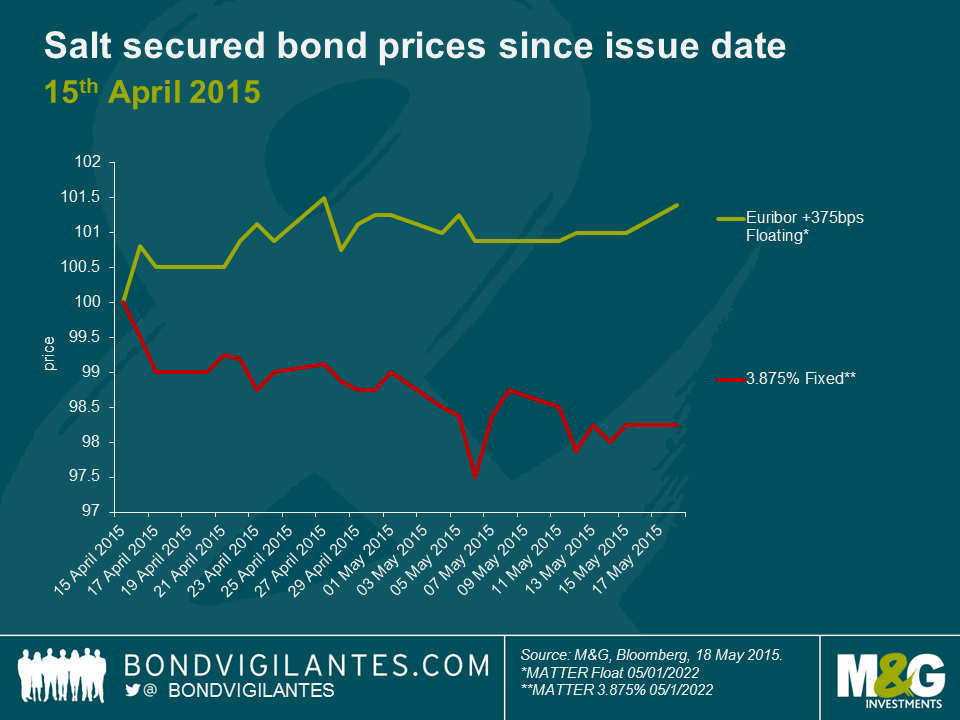

As we can see, the floating rate bond has effectively been immune to the move in the bund market, and in fact it has traded up by around 1%. In contrast the fixed rate bonds have suffered and seen a 2% capital loss. This difference in interest rate sensitivity has meant a 3% relative differential in capital return over the space of just a few weeks.

We can see that in recent weeks floating rate bonds issued by companies have been well worth their salt.

Full disclosure: M&G funds own bonds issued by Salt

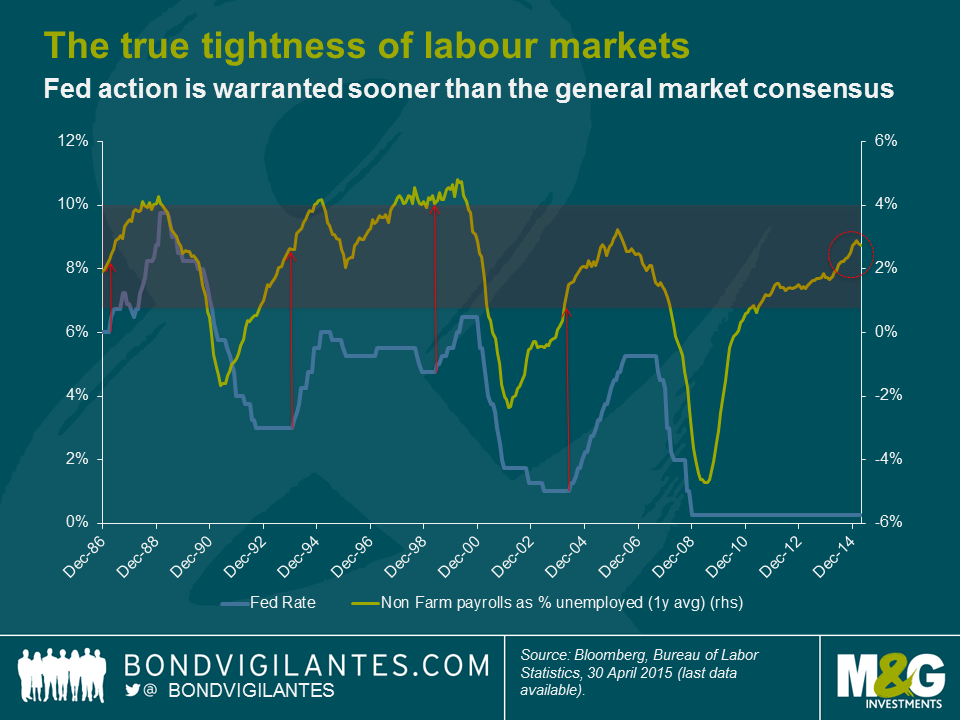

The US unemployment report for April highlighted the continuation of the economic recovery. The market is now in the habit of viewing a job creation number of anything less than 200,000 as a weak result for the labour market and anything more than 300,000 as a strong result. Anything in between and the conclusion amongst economists is this: the Federal Open Market Committee (FOMC) is on hold, economic growth is reasonable, inflation is not a concern, and interest rate increases are not imminent.

To me this seems a bit complacent.

As the unemployment rate falls the US economy will get closer to the point where the low supply of labour will cause wages to increase. Inflation will get an upward push, and the FOMC will likely feel like it has to remove some of its ultra-loose monetary policy by raising interest rates. In the theoretical extreme, were we to get to full employment, then focusing on the absolute payroll jobs number does not make sense. By definition, at full employment very few jobs can be created, as there is no spare labour. An employment report of 100,000 or less when the US economy is operating at full capacity would indicate a vibrant economy with inflationary pressures.

In order to analyse the labour markets as they approach full capacity we have created the chart below. The chart shows the ratio of jobs created as a percentage of the spare labour available. This is an attempt to move the focus away from a headline payroll number, to the true tightness of labour markets.

As can be seen, labour markets by this measure are historically very tight, and I therefore think wage pressures are stronger than the market consensus. Pre-emptive FOMC action is warranted sooner than the market is currently expecting (Eurodollar 90 day futures are pricing in a rate hike in December). Plotted alongside historic fed rates, we can see how far the normal FOMC interest rate response is to the labour market data in this cycle. Historically, when non-farm payrolls as a percentage of those unemployed has been this tight (around 2% level), the FOMC has begun a tightening cycle (in 1986, 1993, 1999).

In economics it is easy to focus on the absolute number, however one should always delve beneath this to analyse the relative. Given the strength in the US economy I would not be surprised to see higher wage growth numbers, rising inflationary pressures, and FOMC action despite the non-farm payroll number staying well behaved in absolute terms. At some point, strong job creation and low unemployment rates will result in higher compensation, and this would not be taken well by the bond markets.

Government bond yields are extremely low across the globe. The highly unusual phenomenon of negative bond yields – even on debt issued by countries that still face a debt crisis – is now commonplace. In addition, investors are looking to protect themselves from the carnage in bond markets we have seen in recent weeks (for example, the “risk-free” German 2.5% 2046 bond is down -19% since the high price was registered on April 20). The much quoted German 10 year bund yield has risen from a low of 0.075% on April 20th to 0.56% at the end last week, but to put this in perspective, it has only taken 10 year bund yields back to where they were at the beginning of 2015.

So where should fixed income investors invest, particularly after the moves in yields we have seen in recent weeks? Should they remain in government bonds and enjoy the perceived safety of owning a risk-free asset, or should they be willing to accept higher levels of risk in order to chase the higher returns on offer in investment-grade and high yield corporate bond markets? Perhaps a more relevant question is: what is the potential downside of owning bonds?

Of course, it is not simply a matter of trying to maximise the return on investment. Another major consideration is the volatility an investor is willing to accept in pursuit of higher returns.

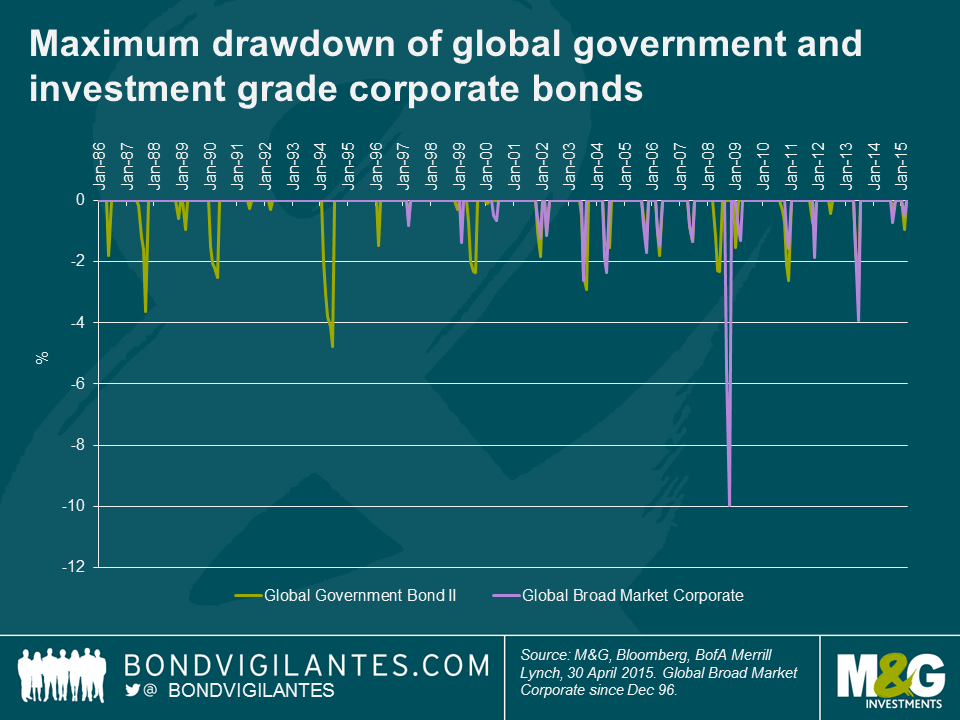

The chart below compares the drawdowns (peak to trough movements) in global government and global investment-grade corporate bonds since their respective inception dates (1986 for the government index and 1996 for global investment-grade corporates) and is based on monthly total return data.

Since 1986, government bond investors have lost money in three calendar years. The magnitude of those losses is as follows: -3.1% (1994), -0.8% (1999) and -0.4% (2013). The reason that total returns have rarely been negative is because investors were receiving relatively high coupons and had a significant income cushion to protect against any capital downside. These days, total returns in government bond markets will largely be a function of capital movements, with income providing little support in a bear market for government bonds. Interestingly, the year after a negative returning year has historically been a fantastic time to own global government bonds with the asset class enjoying a total return of 16.9% in 1995, 8.1% in 2000 and 8.4% in 2014.

Government and investment grade corporate bond investors typically experienced a pretty smooth ride, though many will remember the great bear market sell-off of 1994. Even though there was a sell-off in government bonds in 1994, investors experienced a drawdown of around 5%. A drawdown of this magnitude in government bond markets has only occurred once in the past 29 years. The average maximum drawdown per calendar year since 1986 is only 1.5%. Hence government bonds enjoy a unique position in many investors’ portfolios, as they have been viewed as safe, they have been liquid, and they have let many investors sleep well at night.

Investment grade corporates have historically appeared to be a good alternative to government bonds with similar risk and return characteristics. They are more closely correlated to government bonds but are characterised by a lower interest rate risk profile. In addition, the historical default rate on investment grade corporates has been very low. Since 1970, the 5 year cumulative default rate on USD investment grade non-financial corporate bonds has been 1.1%. Given the global macroeconomic backdrop, we continue to believe that investment grade corporate bonds represent good value relative to government bonds, particularly as we think investors in the corporate bond market are being adequately compensated for a) default risk and b) liquidity risk.

Since 1997, the maximum drawdown was 10% in 2008, not helped by the historically very large weighting to financials as the world went into a major banking crisis. The average maximum drawdown since 1997 is 1.9% with an annualised return of 7.7%. Over the same time period, government bonds generated an annualised return of 7.0%.

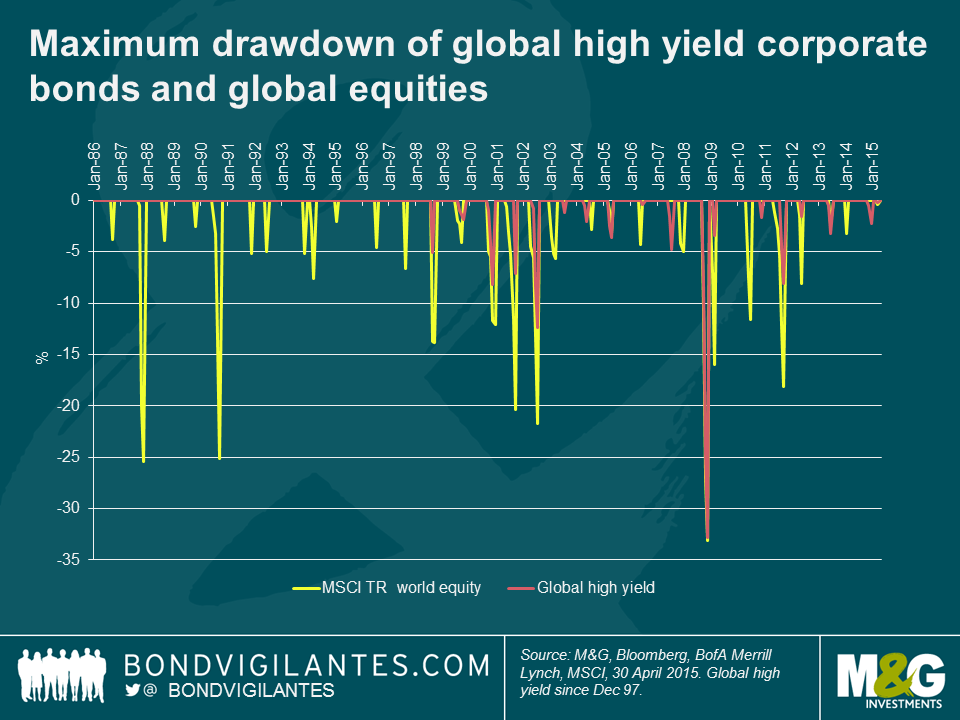

Looking at the maximum calendar year drawdowns it quickly becomes apparent that high yield corporate bond investors suffer through greater volatility than the more defensive fixed income asset classes. There have been no less than six occasions since 1998 when the maximum drawdown in high yield was over 5% with an average annual maximum drawdown of 5.6%.

Over the past 29 years, the average annual maximum drawdown in the global equity market has been 9.4%. In this respect, high yield corporate bonds have a greater correlation to equity markets then traditional fixed income markets. The reason is high yield bonds and equities tend to respond in a similar way to macroeconomic developments, which can lead to similar return profiles over the course of a full market cycle. Equities are obviously a different asset class to high yield corporate bonds, but to a bond investor equities can be viewed as perpetual securities and therefore have a huge amount of credit spread duration. Additionally, unlike bonds, the owner of an equity usually has little or no security over a company’s asset base. High yield bonds tend to be less volatile than equities because the fixed income component of the total return provides an added measure of stability and the potential for capital appreciation means that high yield corporate bonds can offer equity-like (or better than equity) total returns in the long-run.

However, during bouts of market risk aversion, high yield bonds generally underperform the broader fixed income market. In 2008, facing a storm of forced selling global high-yield corporate bond investors experienced a 33% decline in the value of their investments. High yield also performed poorly because these highly levered companies have a lot more credit risk than investment grade companies (since 1970, the 5 year cumulative default rate on USD high yield non-financial corporate bonds has been 20.5%), and the macroeconomic outlook in Q4 2008 was the worst it has arguably ever been. Over the same period, government bonds appreciated in value by almost 5%. This highlights a benefit of government bonds – they tend to be uncorrelated with riskier assets.

Those high yield investors that avoided the temptation to sell during the dark days of 2008 have been duly rewarded by the market. From November 2008 until March 2015, global high-yield corporate bonds have generated a total return of 172% in an environment where global high yield default rates have been exceptionally low. Over the same time period, global equities have experienced a total return of 135%. In this sense, high yield corporate bonds have behaved more like equities rather than traditional fixed income assets like government bonds.

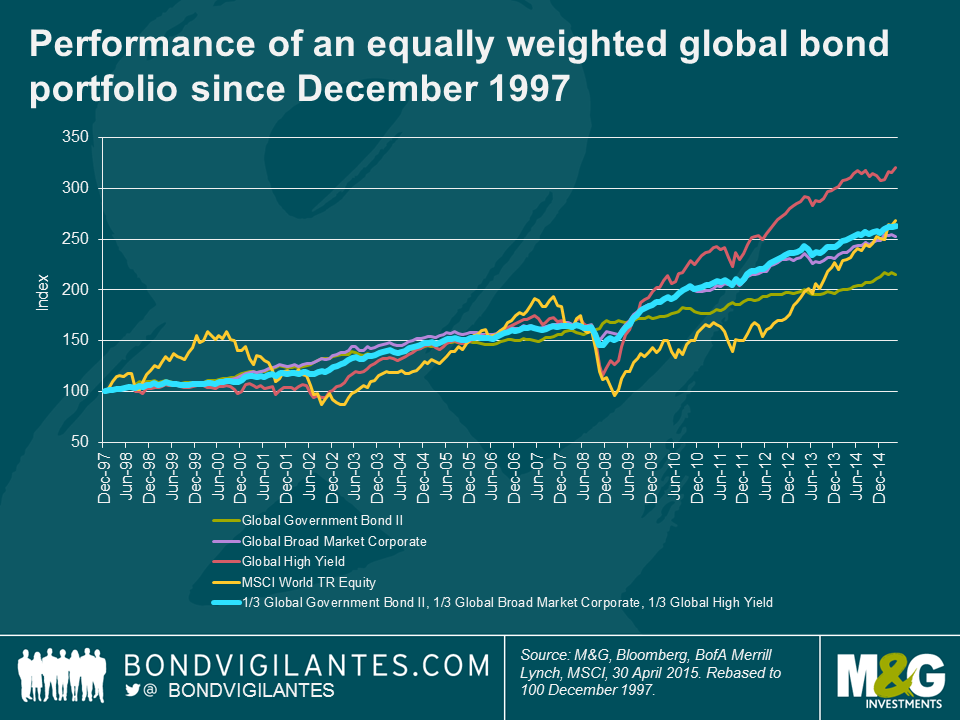

For those that are curious, the blue line in the chart below shows the performance of an equally-weighted portfolio of global fixed income assets since December 1997. This portfolio generated an annualised return of 7.9% (similar to global equities) with less than half the volatility of being invested fully in high yield or equities.

Whilst an historical analysis is interesting, is there anything that can be gained in order to assess potential future returns from fixed income assets?

It is possible to model (with some simplifying assumptions, like any move in rates is a one-off shock and the yields rise across the curve by the same amount and no move in currencies) for any movements of bond yields and corporate bond spreads and compare to the historic return profile for fixed income. It is simplistic but is useful as a rough guide to highlight the impact that lower yields could have on fixed income total returns.

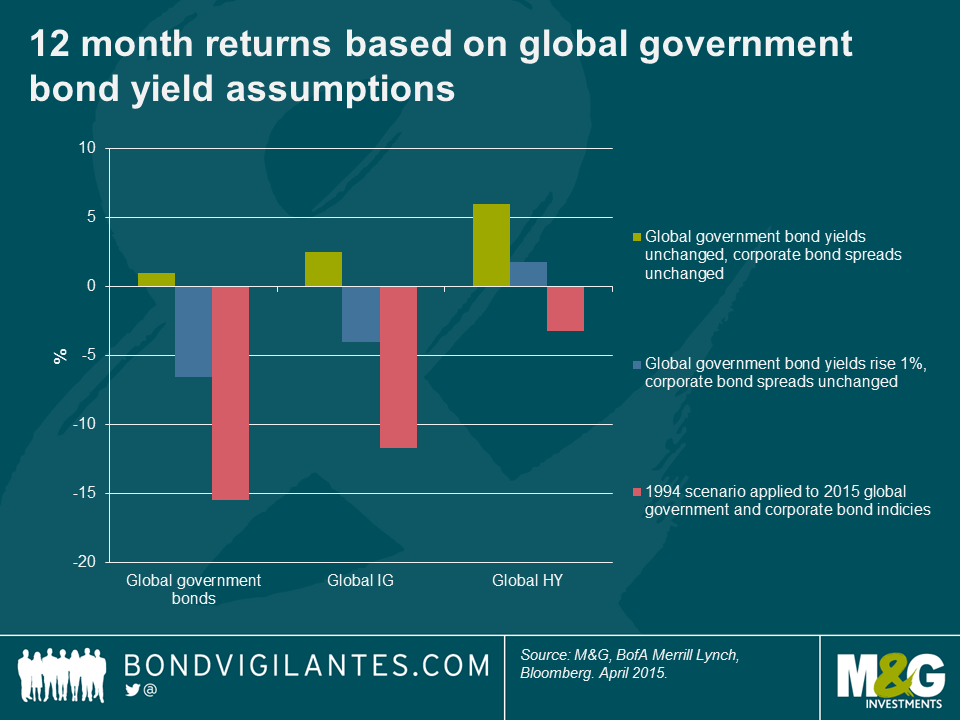

Firstly, assuming that government bond yields and corporate bond spreads do not change and investors receive the current yield to maturity on the fixed income asset classes, the expected 12 month total returns are:

Secondly, looking at a scenario where government bond yields increase by 1% but credit spreads remain stable gives the following total returns over 12 months:

Given that yields are at historic low levels, there has never been less of an “income cushion” to protect against the possibility of a fall in bond prices. Government bond yields only need to increase by 73bps in order to match the record drawdown experienced by government bonds in 1994.

Finally, the yield on the Global Government Bond index rose from January to November 1994 by 219bps. 1994 was the year that generated the maximum drawdown in global government bonds. An equivalent move today (and assuming no change in credit spreads) would result in the following total returns:

The conclusions we can draw from this analysis are:

Of course, there are some very good reasons to own government bonds which I have previously written about. High global debt levels, structural deflationary forces and the global savings glut mean that over the long term, government bond yields may not increase to levels seen a couple of years ago. As the drawdown analysis above shows, government and investment grade corporate bonds tend to be less volatile, have lower drawdowns and have proven to be less correlated with higher risk assets like high yield corporate bonds and equities.

For those looking at moving out of government bonds given low yields, based on a risk and return basis investors might view investment grade corporates as a good alternative, and historically investment grade assets have shown a relatively low probability of generating a negative return in a calendar year. However, investors should be aware that investment grade corporate bonds have proven to be closely correlated to government bonds. Subsequently, any sell-off in government bond markets will likely hit IG corporate bond returns as well. The collapse in corporate bond yields to extremely low levels has reduced the income contribution of total returns, though the credit spread on offer is rewarding in an environment of low defaults and solid economic growth.

In a world of ultra-low yields and lower future returns from fixed income, many may be tempted to invest in riskier assets. High yield corporates are more closely correlated but exhibit lower volatility to equities. High yield corporate bonds experience far greater volatility than more defensive fixed income asset classes and hence investors should be prepared to experience drawdowns in their portfolios over the course of a market cycle. That said, the higher yield on offer does protect against any possible increase in yields, as does the shorter duration profile of the high yield asset class.

Looking at historic returns, drawdowns and correlations give a useful guide to how fixed income returns might be impacted in a world of rising yields. However, the collapse in yields across the fixed income spectrum now means that investors are at greater risk of higher drawdowns than ever before, and the income component of their total return is unlikely to adequately compensate for any hits to capital returns like it would in the old days.

Here are a few quick thoughts about things that happened last week.

First, the UK election and the failure of the opinion polls. Ahead of the General Election we met with several of the big opinion pollsters, and even ran a Bond Vigilantes x Politics event featuring Anthony Wells of YouGov. Without exception they highlighted how unusual it was that, whilst the Conservatives appeared to be neck and neck with Labour in the polls, it would be unprecedented for them not to win the election given that a) David Cameron was far ahead of Ed Miliband when people were asked who would make a better PM and b) the Tories were far ahead of Labour in the polls when asked who would do a better job on the economy. These two issues have always determined who won the General Election. Taken together with the well-known concept of the “shy Tories” (the theory that many Conservative voters are ashamed to admit to voting for what might be perceived to be self-interest, and so either lie, or do not participate in opinion polls) which has consistently led to the polls underestimating the actual Conservative share of the vote, and it should have been obvious that the hurdle for a Labour win was incredibly high. Yet all the pollsters still forecast that Ed Miliband was most likely to be forming a government. It’s a lesson for us all about ignoring noise and spin, and not expecting a different output from well tested inputs. In particular think about Europe – why would we not expect a huge monetary policy easing by the ECB, together with less fiscal austerity going forward, not to have a positive impact on Eurozone growth? It will (not permanently, and maybe not massively, see Japan) – but many expect deflation and depression forever.

Secondly, the Danish government announced plans to let shops stop accepting cash as payments. Officially this is to ease “administrative and financial burdens” and is part of a programme of reforms aimed at boosting growth – and there is evidence that high cash usage in an economy acts as a drag on GDP growth. The article quotes McKinsey which suggests that for the US, use of cash shaves 0.47% per year off GDP growth. Not only is cash handling expensive, and cash payments can easily slip through the tax collecting net, but there’s another reason why Denmark might be encouraging a full move to electronic money. Danish interest rates are currently negative, with the deposit rate at -0.75%. In a world of physical cash it is possible for many economic participants to avoid a negative interest rate simply by withdrawing their money from the banking system and keeping it in a safety deposit box or under the mattress. In Switzerland (another country with negative rates) 60% of banknotes in circulation are held in the largest CHF 1000 note, perhaps for ease of storage outside of the banking system. Only by doing away with physical money and moving to electronic money can a central bank fully control monetary policy. This paper by Trond Andresen of The Norwegian University of Science and Technology (and which hat-tips Krugman’s work on e-money) additionally suggests that the use of electronic money would allow central banks to control the velocity of money rather than just the supply. A world of negative interest rates will accelerate the movement towards the abolition of paper money by the authorities.

Next, Tesla. I’ve had enough of oil prices sending my bond investments up and down on the whim of dictators and cartels as they increase or decrease production. We may soon be over all that nonsense. Tesla last week announced that they have had $800 million of orders (38,000 orders) for their new home and business storage batteries – they are sold out now until the middle of next year and are trying to increase their manufacturing capacity to cope with demand. Each domestic battery can power a home for 5 hours (not long) and is expensive (up to £2300), but the pace of improvement in both metrics is really encouraging. I think this is huge for the energy security of the world – I’d pinned my hopes on nuclear fusion but it’s gone a bit quiet of late. Instead, Europe has been quietly installing a massive amount of solar capacity. In 2014 there were 7.3 GW of solar additions, of which 2.2 GW was residential rooftop. To put that in context a large nuclear power plant produces 1.6 GW of energy (although that runs 24/7, not just when the sun is out). The ability to store energy in an increasingly cheap and efficient manner will produce big economic benefits. It’s not just Tesla leading the way here. Samsung is also building much bigger batteries (articulated lorry sized), which are now being used by power generation companies. For me, it’s not just the reduced reliance on fossil fuels that appeals; it’s the reduced reliance on a national grid. This means that the chances of mankind surviving a global catastrophe (nuclear war, meteor strike, zombie attacks) greatly increases as micro-generation eliminates reliance on a handful of highly complex power stations and distribution networks. With solar and batteries we won’t have to start science and technology from scratch if the worst happens. Or at least we can watch House of Cards DVDs on telly whilst we await the next wave of zombie assaults.

Finally, if you haven’t seen it yet, we’ve got a YouTube channel. At the moment we’re putting up our economics focussed videos on it – our War Loan film, Mike Riddell’s chat with Richard Koo about balance sheet recessions, and interviews with Diane Coyle (on the concept of GDP) and Ed Conway (on Bretton Woods). Please take a look.

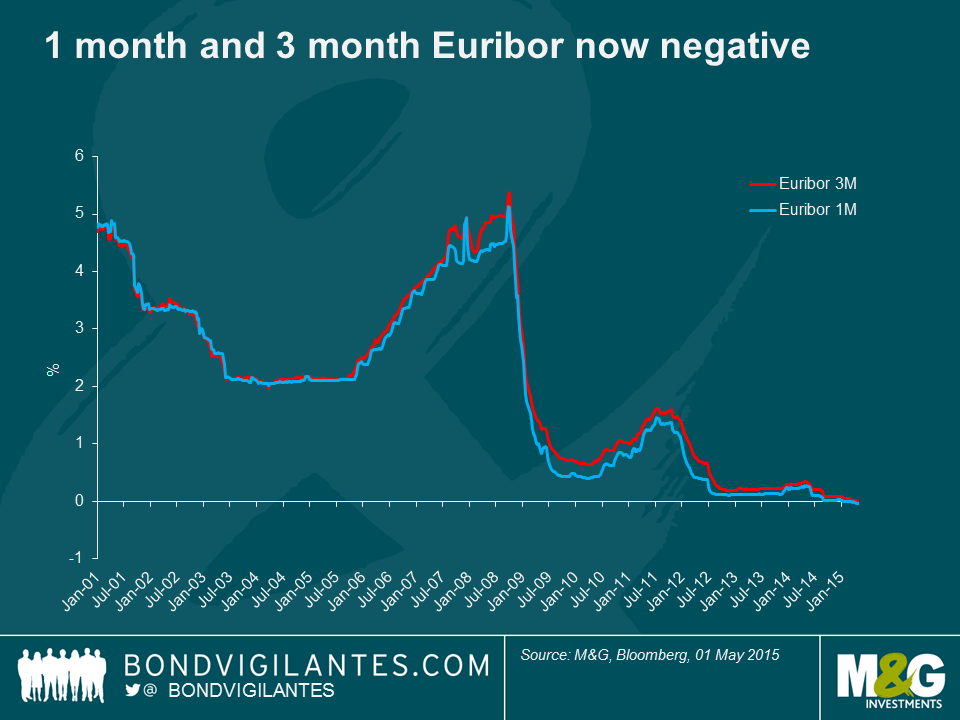

Negative interest rates have become increasingly prevalent in Europe owing to the expansionary monetary policy measures with a number of central banks implementing negative base rates (Switzerland, and Sweden). Two weeks ago 3 month Euribor, (the reference rate for the majority of Pan-European Asset-Backed Securities (ABS)), followed 1 month Euribor (largely the preserve of most European Auto ABS transactions), into negative territory. Where the reference rate has turned negative, noteholders can expect to receive the net amount (i.e. the positive coupon on the notes offsets the negative reference rate).

The concept of negative interest rates wasn’t previously envisaged by the authors of securitisation documentation. The working assumption in the market is that interest payments to noteholders will be floored at 0% – we saw the first confirmation of this theory when issuers of two Spanish transactions issued an investor notice that they will apply a coupon of 0% instead of the negative coupon that would result from applying Euribor. In addition, Moody’s canvassed legal practitioners in most European jurisdictions and concluded that that the consensus, as far as note interest goes, is that there is a real or effective floor as there cannot be a payment obligation of the noteholders to the issuer implied by negative interest rates on the notes.

In contrast, ancillary monetary obligations (swaps, account banks etc.) are not usually floored at zero. For instance, under a typical fixed floating swap (a derivative instrument that enables the parties involved to exchange fixed and floating rate cash flows), the issuer would pay the fixed rate payments received from the collateral pool and receive floating rate payments from the swap provider (which are then passed on to noteholders). If the 3 month Euribor plus spread becomes negative , the issuer could also end up paying on the floating leg of the swap (which does not typically have floors). The read through to cross currency swaps involving euro liability payments against non-euro denominated assets could result in similar issuer special purpose vehicle (SPV) shortfalls.

This misalignment introduces negative carry whereby the issuer’s cashflows are less matched than before the negative rates situation. As ancillary monetary obligations rank as senior costs within a SPV cash flow waterfall (the senior classes have first claim on the cash that the SPV receives, and the more junior classes only start receiving repayments after the more senior classes have been repaid), this therefore reduces cashflows to subordinated noteholders, or at best reduces excess spread which otherwise would flow back to the originator.

On the whole, for legacy transactions with little excess spread and/or credit enhancement, the negative impact can be significant as Euribor gets increasingly into negative territory as the issuer may have no way of recovering shortfalls in cashflows.

For most ABS deals in 2015, new offer documents have seen language inserted to either floor the interest rate at 0% or floor the reference index at a predefined rate.

The consensus view on the outlook for Emerging Market (EM) bonds is bearish. Many point to risks posed by a Fed rate hike, falling commodity prices, possible Grexit and a slowing China as reasons to reduce investment allocations to the asset class. However, there is a solid investment case for EM debt at this point in time for those willing to have a closer look.

Firstly, geopolitical events appear to have stabilised in several regions across the globe. For example, there are encouraging early signs from the Ukrainian sovereign and corporate restructuring process, with successful negotiations between creditors and the government to extend the repayment terms of the state owned bank Ukreximbank. In Brazil, Petrobras has at last released its financial results, delayed by several months over its bribery scandal, which eliminates the risk of acceleration and technical default on its bonds. And in Tunisia and Kenya, where terrorist attacks have recently taken place, bonds have recovered to their previous levels after a brief period of underperformance. We would argue that these reduced tail risks are yet to be factored into investors risk assessment for these countries.

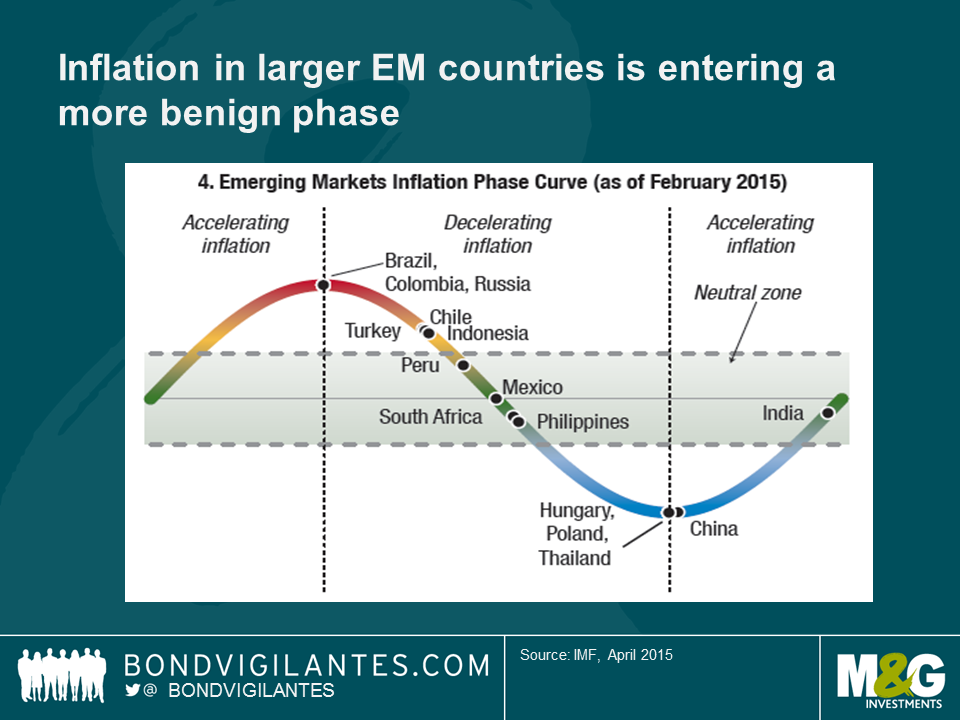

Secondly, inflation in some of the larger emerging market countries is now at a more benign phase. This will give the central banks some additional monetary policy flexibility, and they won’t be required to hike interest rates before the Fed starts doing so.

Thirdly, recent oil price developments also suggest more cheer in some emerging markets. Countries such as Venezuela, Ecuador and Iraq, heavily reliant on oil for export and fiscal earnings, would have faced a particularly negative macro environment, had oil prices continued declining into the USD40 range. With the oil price recovery, a Venezuelan default largely priced in for 2015 earlier in the year has now been pushed into 2016, removing another immediate tail-risk. Oil exporters such as Nigeria who have not yet allowed their currencies to depreciate have lost a considerable amount of foreign exchange reserves in defending their currency – but as oil prices have rebounded towards the USD50-60 range, earlier underperformance has been reversed. Additionally, the still generally low oil price is also a welcome tonic to the US consumer, helping emerging markets with close ties to the US economy such as Central America and the Caribbean, Mexico, and some Asian exporters.

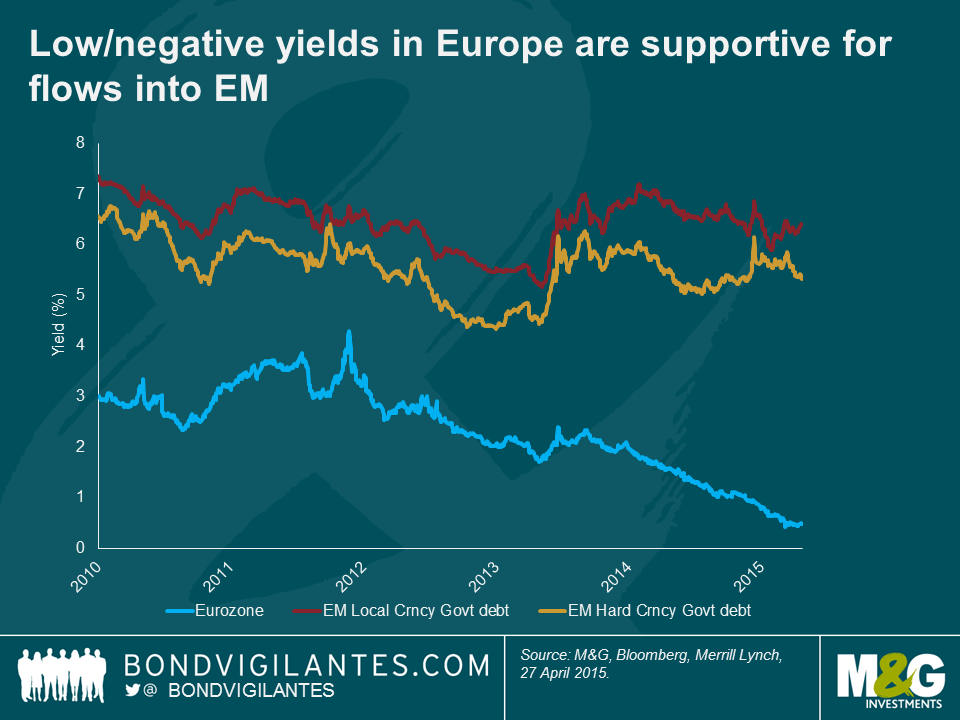

Fourthly, EM bond yields are still attractive on a relative basis and investors still have the opportunity to acquire assets with yields over 7%. The relative value opportunity is especially the case given the very low level of developed market government bond yields. Additionally, EM issuers are exploiting the lower yields on offer in Europe and have started funding in EUR, as opposed to USD. Of course, some sovereign and corporate credits with large balance sheet mismatches are vulnerable in this environment, but there are also winners in the space, such as exporting corporates. Other winners include sovereigns that are already advanced in their current account rebalancing, such as India, Chile, Pakistan, Poland and Hungary.

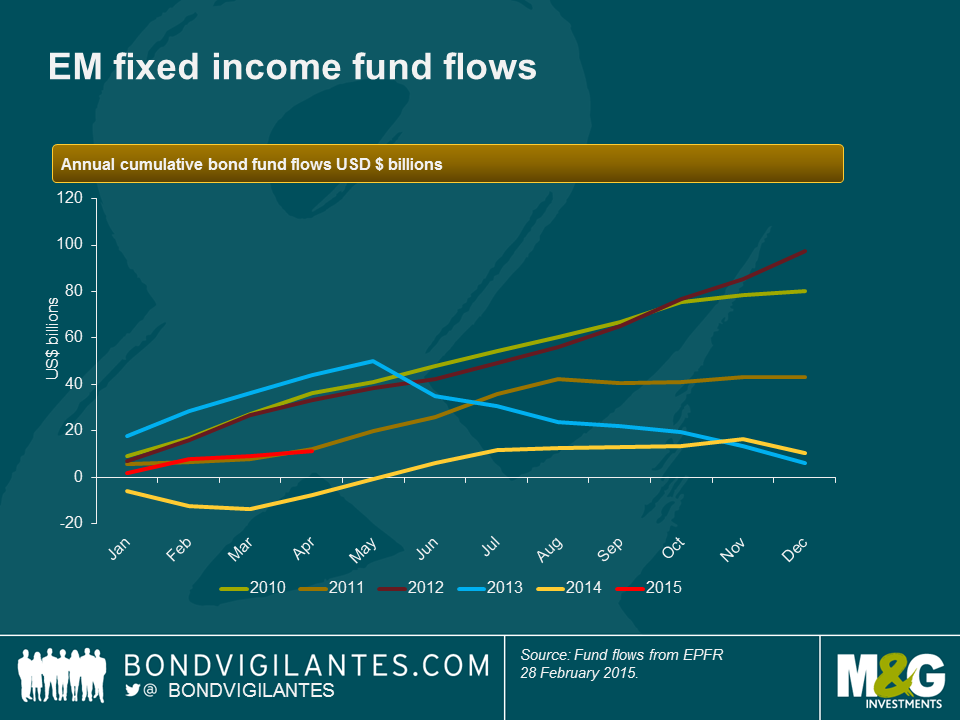

Finally, flows into emerging market debt markets have slowed materially since 2013, thereby reducing the risk of Taper Tantrum-esque outflows should the Fed begin to hike rates. Arguably, some of the “hot-money” has already retreated from the asset class potentially reducing any future volatility.

I expect that EM debt will continue to look attractive in a world of ultra-low interest rates and loose monetary policy. The receding of geopolitical risks, low inflation, stabilisation in the oil price, strong relative value dynamics and reduced risk of outflows are solid tailwinds for the asset class in the remainder of 2015.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.